Morning Note: Market News and an Update from Reckitt Benckiser.

Market News

Donald Trump extended a ceasefire with Iran and kept a US blockade in place, while JD Vance called off a trip to Islamabad for negotiations that Iran refused to attend. Tehran received “some sign” that the US is ready to break the blockade, Iran’s semi-official Tasnim news reported, without elaborating on the timing.

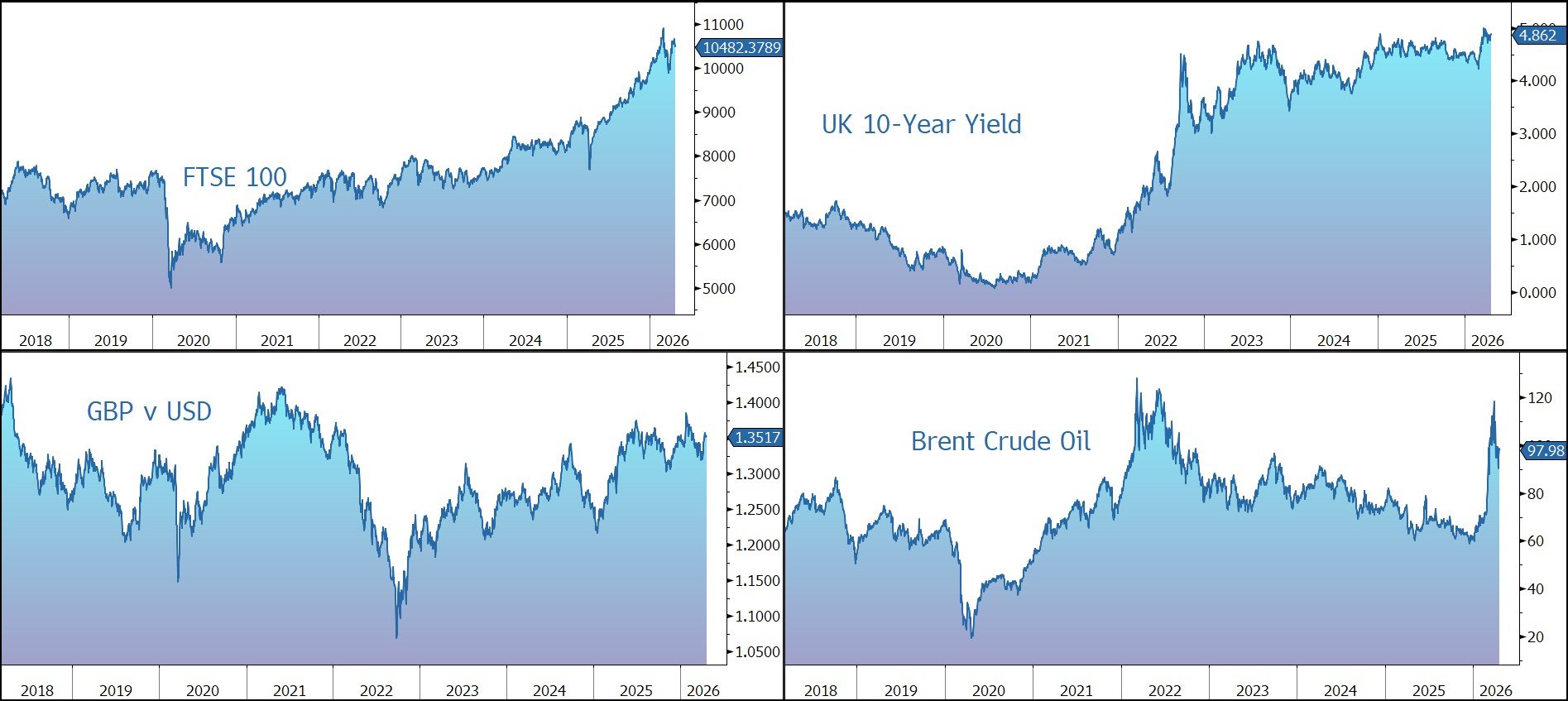

Brent Crude trades at $98 a barrel. US crude stockpiles fell 4.5m barrels last week, the API is said to have reported. Gasoline and distillate inventories dropped by a combined 9.8m barrels.

Gold has risen to $4,765 an ounce, recouping some losses from the previous session. The precious metal is currently down nearly 10% since the conflict began.

In the Senate confirmation hearing, Federal Reserve Chair nominee Kevin Warsh pledged to act independently. He called for a new framework to address persistent inflation but did not provide further specifics. The yield on the US 10-year Treasury is 4.29%.

US equities traded lower last night – S&P 500 (-0.6%); Nasdaq (-0.6%) – although the main indices are currently expected to recoup the losses at the open this afternoon. In Asia, equities were mixed: Nikkei 225 (+0.4%); Hang Seng (-1.2%); Shanghai Composite (+0.5%). China’s property market is likely at a turning point that will help the nation’s stocks outperform their EM peers, according to JPMorgan.

The FTSE 100 is currently little changed at 10,490, while Sterling trades at $1.3515 and €1.1510. UK inflation accelerated to 3.3% year on year in March, matching estimates, while the core CPI came in at a lower-than-expected 3.1%. The Iran war could wipe out most of Rachel Reeves’ fiscal buffer, with a £16bn hit to Britain’s public finances, The Resolution Foundation said.

Source: Bloomberg

Company News

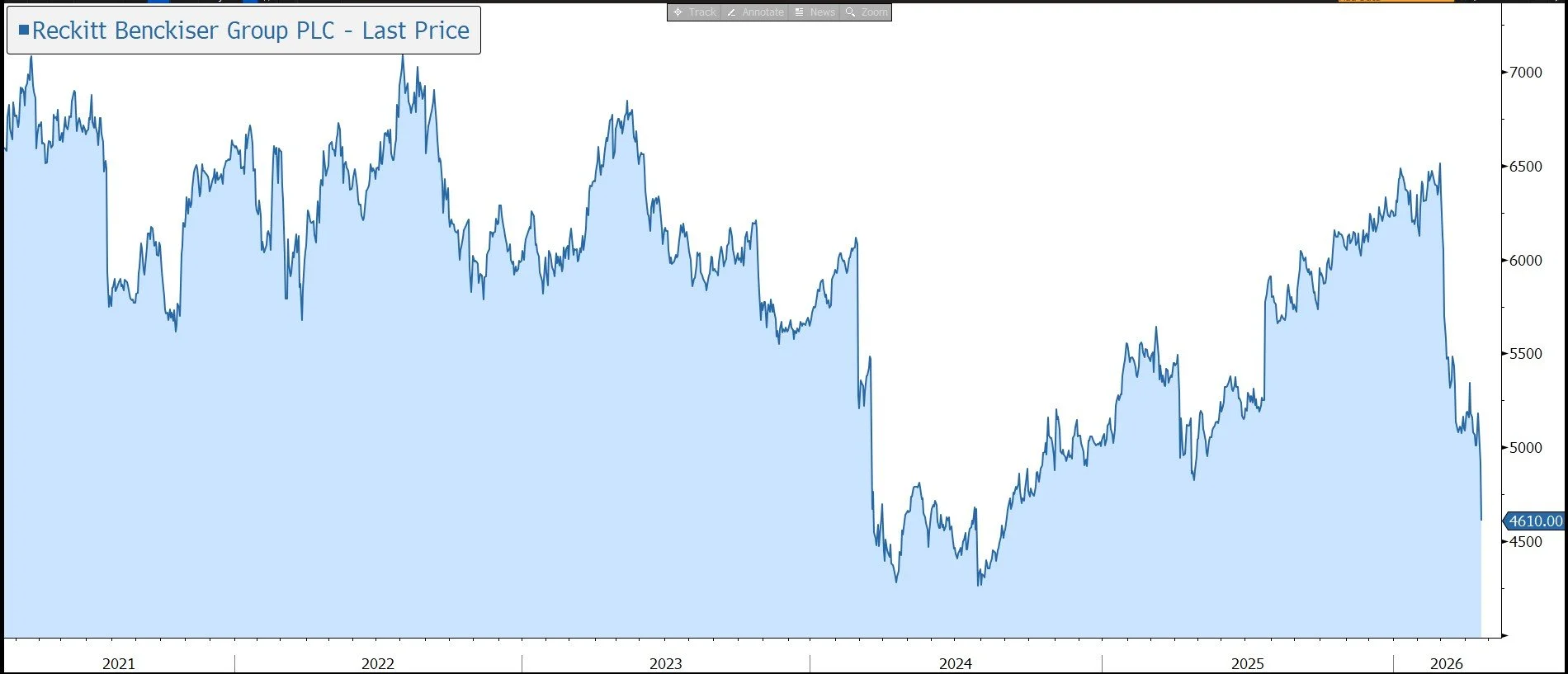

Reckitt Benckiser has released its Q1 2026 results. Although a slower quarter was expected due to weakness of seasonal products and the competitive backdrop in Europe, revenue growth in the Core business came in below the market expectation. However, the company has maintained its guidance for the full year, albeit delivery is still weighted to the second half. With the market is no mood to give the company the benefit for the doubt, the shares have been marked down by 5% in early trading.

Reckitt is a global leader in health, hygiene, and nutrition. Trusted brands, such as Dettol and Lysol, continue to benefit from the shift to healthier and more hygienic lifestyles, particularly in emerging markets. To help ease the pressure on state-funded healthcare systems, we are seeing a transition to self-care and growth of over the counter (OTC) brands such as Mucinex, Nurofen, and Gaviscon, all of which are owned by Reckitt. A focus on immunity, mental health, and overall well-being is expected to drive growth of the group’s preventative treatments, such as vitamins, minerals, and supplements (VMS).

Reckitt is currently refocusing its portfolio and simplifying its organisation to drive accelerated growth and value creation.

Core Reckitt includes a portfolio of 11 market-leading (No.1 or No.2), high margin Powerbrands across four categories of Self-Care, Germ Protection, Household Care, and Intimate Wellness. Brands include Mucinex, Strepsils, Gaviscon, Nurofen, Lysol, Dettol, Harpic, Finish, Vanish, Durex, and Veet. Over the last three years this portfolio has delivered 5% revenue CAGR and in 2025 generated a gross margin above 60%.

Reckitt operates across three geographies: North America, Europe, and Emerging Markets, with the latter expected to grow in the high-single digits.

The company is undertaking a fixed cost optimisation initiative to unlock efficiencies and deliver at least a three percentage points reduction in fixed costs by the end of 2027, of which half was achieved by the end of 2025. The group now has confidence in achieving a fixed cost base below the initial 19% target by the end of 2027, albeit there is a lack of clarity regarding the level of step-up in 2026. Part of the savings are being reinvested into the supply chain and R&D.

Overall, the company now believes it has the portfolio, geographic footprint, and execution capabilities for Core Reckitt to consistently deliver 4%-5% like-for-like (LFL) net revenue growth, while consistently delivering annual EPS growth and creating value for shareholders.

At the end of 2025 the company sold its Essential Home business (now called Vestacy), a portfolio of non-core brands such as Air Wick, Mortein, Calgon, and Cillit Bang. The $4.8bn transaction was fairly complex – it included up to $1.3bn of contingent and deferred consideration, and Reckitt retained 30% of the business. As part of the deal, shareholders received a $2.2bn (£1.6bn or 235p a share) special dividend and the shares underwent a 24-for-25 consolidation.

The company’s third leg is Mead Johnson Nutrition which includes infant formula brands Enfamil and Nutramigen. The company continues to evaluate all strategic options for the business. This means investors potentially face another period of ‘messy’ forecasting once the business is sold.

Back to today’s results. As expected, ongoing weakness in the competitive European market, a weak cold and flu season, and geopolitical disruption held back growth in the first quarter of 2026.

Reported revenue fell by 11.8% to £3,247m, including currency heading and disposals. Stripping out these impacts, LFL growth was 0.6%.

Core Reckitt grew revenue by 1.3% in LFL terms to £2,598m. Although a weak quarter was expected, the results came in below the market expectation of 2.9%, although full-year guidance has been maintained. Growth was made up of a 2.3% increase in price/mix and 1.0% volume decline. Excluding seasonal OTC products, Core Reckitt LFL net revenue growth was 3.1%.

The results were led by Emerging Markets (+7.6%), with double-digit growth in China and India, offset be the Russia unit. In Developed Markets, Europe fell by 4.2%, impacted by a challenging consumer environment and the weak cold and flu season. North America fell by 0.9%.

In the Core product segments, LFL growth at Germ Protection (+9.5%) and Intimate Wellness (+0.3%) were offset by Household Care (-7.6%) and Self-Care (-0.1%). Innovation continues to support long-term growth with launches across each category during the quarter including upgrades to Finish premium formats and Vanish Quick Wash formulations.

In the smaller non-core division Mead Johnson Nutrition, net revenue fell by 2.7% on a LFL basis due to the lapping of significant inventory rebuild in North America in Q1 2025. Underlying performance was solid.

As expected at this stage, the group hasn’t provided an update on profitability or its financial position. As a reminder, at the end of 2025, financial gearing was 1.6x net debt to adjusted EBITDA, or 2.5x on a pro-forma basis following the Essential Home special dividend, versus the guidance of ‘below 2x’.

The dividend policy is to deliver sustainable growth in future years – the 2025 payout was raised by 5% to 212.2p (3.6% yield). In response to the weak share price and to reflect the board’s confidence in the continued strong free cashflow generation of the business, Reckitt is currently undertaking the third tranche of its £1bn share buyback Programme which will return up to £540m no later than 27 July.

Although the statement acknowledges the current uncertainty arising from the war in the Middle East, through 2026, the company expects to benefit from the reset of the cold and flu season, as well as the launch of superior innovations across its categories. As a result, guidance has been reiterated:

· Core Reckitt LFL revenue growth in the 4%-5% medium-term guidance range.

· In Q2, the company expects to benefit in seasonal OTC from the initial shipments of the category-creating innovation ‘Mucinex 12 hour Cold and Fever’ in North America in June and lapping the Mucinex Sinus PE reformulation in Q2 2025. In Europe, a sequential improvement in LFL net revenue performance is expected. Q2 growth in Emerging Markets is expected to be broadly in line with Q1.

· Modelling a scenario of oil at $110 a barrel for the remainder of 2026 indicates a £130m-£150m gross impact on the group’s input cost base in 2026 which it sees as a manageable level to offset through flexibility and productivity in its supply chain, hedging strategy, pricing, and its strong gross margin profile.

· Mead Johnson Nutrition - low-single-digit LFL net revenue growth, with a mid-single-digit LFL decline in Q1 as the company laps the retailer inventory rebuild in North America in Q1 2025.

· Further down the P&L, forecasting is more difficult given the complexity stemming from the deconsolidation of Essential Home. However, the company has maintained its expectation for adjusted operating profit margin for 2026, with the delivery of this weighted to H2. In H1, the impact of stranded costs, lower seasonal incidence on the higher margin seasonal OTC business and higher commodity prices are expected to result in Group adjusted operating profit margin around 200 basis points below H1 2025 (24.6%). In H2, Group adjusted operating profit margin will be much stronger than H2 2025 driven by a greater level of stranded cost mitigation from the Fuel for Growth programme, the reset of the cold and flu season, more favourable mix, continued activation of the innovation pipeline, and actions to offset commodity price inflation.

The company reiterated its ambition to deliver long-term, sustainable EPS growth, acknowledging in 2026 headwinds from Essential Home dilution.

The legal case against the company (and industry peer Abbott) relating to its cow’s milk-based infant formula is ongoing. As of early 2026, there were around 800 active cases in the Multi-District Litigation. Reckitt continues to vigorously defend these claims and believes the lawsuit’s claims are not supported by scientific evidence. A bellwether trial in the US federal multidistrict litigation (MDL) is now scheduled for 6 July. The threat of sizeable damages continues to hang over the share price and prevents the company from offloading its Nutrition division. We expect the company to seek some form of settlement.

Source: Bloomberg