Morning Note: Market News and Updates from Heineken and EssilorLuxottica.

Market News

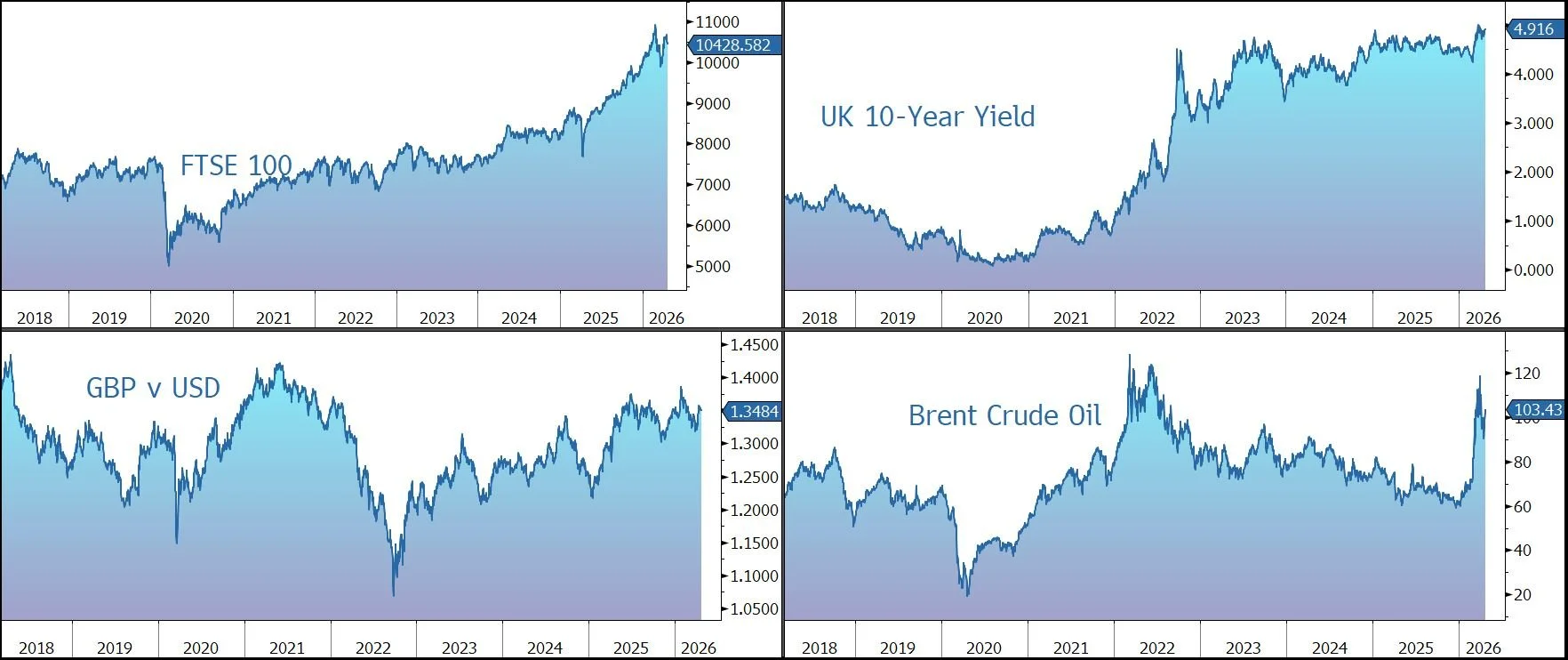

Stocks and bonds fell while oil rose as stalled US-Iran talks kept markets on edge and Hormuz traffic ground to a halt. Only one ship was seen moving through the waterway today. The White House said Donald Trump has not set a firm deadline to receive an Iranian peace proposal. Tehran says it has no plans to take part in negotiations imminently.

Brent crude climbed 1% to $103 a barrel, putting it on track for a fourth straight day of gains. Bonds fell on inflation concerns – the yield on the US 10-year Treasury ticked up to 4.31%. Gold slipped to $4,720 an ounce.

US equities gained last night – S&P 500 (+1.1%); Nasdaq (+1.6%) – although the main indices are currently expected to come off somewhat at the open this afternoon. Tesla erased gains post-market despite a first-quarter profit beat, after saying capital expenditures will exceed $25bn this year – $5bn more than previously estimated.

In Asia, equities drifted lower: Nikkei 225 (-0.8%); Hang Seng (-1.0%); Shanghai Composite (-0.3%). Japan’s manufacturers ramped up production in April to the highest level in 12 years, a sign of frontloading.

The FTSE 100 is currently trading 0.4% lower at 10,429, while Sterling trades at $1.3485 and €1.1525. Companies trading ex-dividend this morning include BAE Systems (1.06%), Fresnillo (2.33%), Legal & General (5.79%), Rightmove (1.45%), Rolls-Royce (0.42%), and Spirax (1.62%).

The UK budget deficit totalled £132bn in the fiscal year through March, in line with the budget watchdog’s forecast. The gap was a higher-than-expected £12.6bn in March.

European car sales jumped 11% in March, the most in nearly two years, on strong growth for fully electric and hybrid models.

Source: Bloomberg

Company News

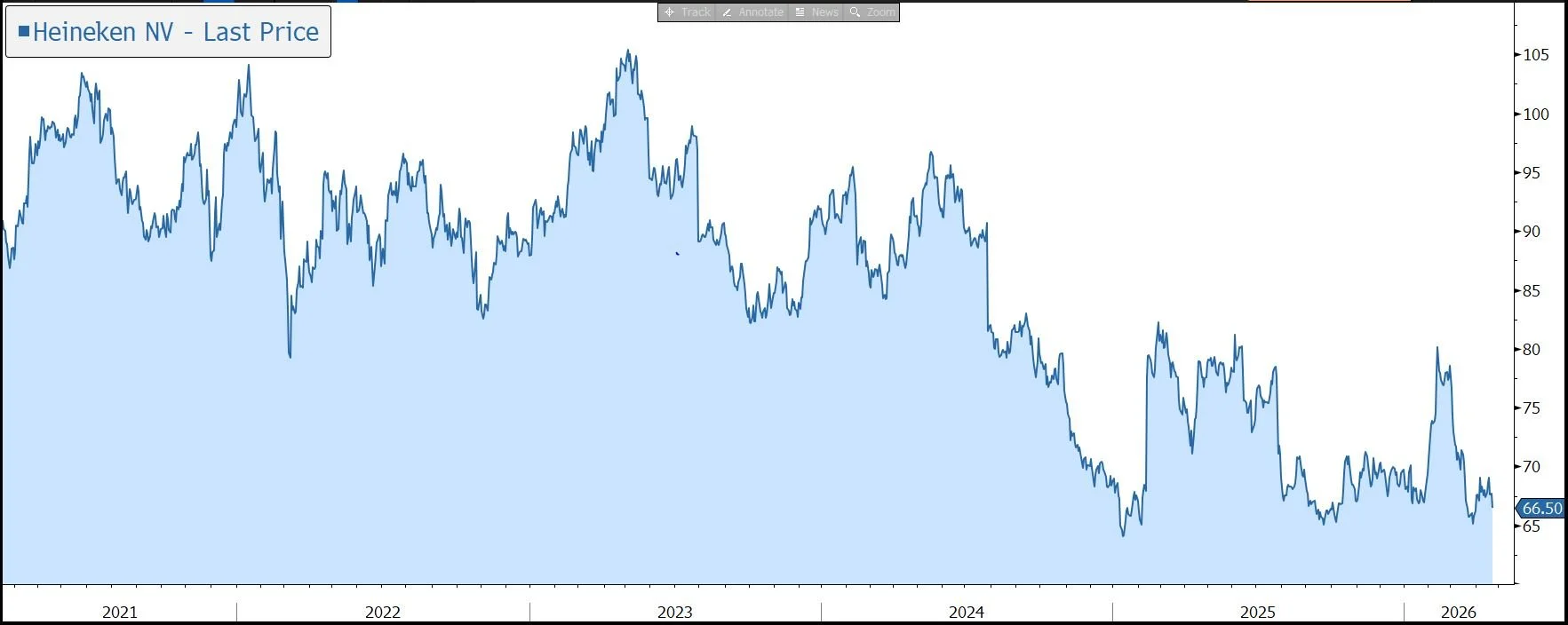

Heineken has released Q1 2026 results which were slightly better than market expectations. This was the last report by the current CEO – for now there is no update on a new appointment. Heineken’s balance sheet is robust and the second tranche of its share buyback programme is ongoing. Based on current assessment, the company has confirmed that operating profit is expected to grow in the 2% to 6% guidance range. However, the statement warns that inflationary pressures might affect consumer sentiment and beer market growth. In response, the shares are trading 2% lower.

Heineken is the world’s second largest brewer, generating net revenue of €29bn from a portfolio of iconic brands, many of which have been quenching the thirst of consumers for decades. In addition to the core Heineken brand, the company owns several well-known beers and ciders, including Sol, Tiger, Amstel, Murphy’s, and Strongbow, as well as more than 300 or so local brews. The company also owns around 2,400 pubs in the UK, runs a wholesaling operation in Europe, and has a strong global distribution capability. Over time, the group has expanded and developed its global footprint through investment in new breweries, partnerships, and acquisitions. It has also exited several businesses to refine the portfolio, most recently the company exited its business in the Democratic Republic of Congo to an asset-light licensing model.

We believe the company is well placed to benefit from long-term growth opportunities in emerging markets (which generate 55% of revenue), where young and growing populations, low per-capita beer consumption, and increasing wealth are expected to drive growth. The company believes the biggest opportunity is in India, with strong prospects in Mexico, Brazil, China, Vietnam, and South Africa. Most recently, the group strengthened its position in Central America through the $3.2bn acquisition of the multi-category beverage portfolio and retail business of FIFCO, a deal that is expected to be immediately accretive to EPS.

The group generates more than 40% of its revenue from premium brands, where volume is growing faster than mainstream beer because consumers turn to better brands as they grow older and wealthier. Premium brands tend to have greater pricing power. Finally, the group is benefiting from the growth of low and no-alcohol products, where it is the global leader, and products ‘beyond beer’ such as seltzers and ready-to-drink products.

We believe the shareholding structure, supported by family ownership, ensures the company is run for the long term and in the best interests of all shareholders.

The EverGreen 2030 Strategy is targeting 18 priority markets and fewer, bigger brands (5 global and 25 local). This also involves a transition from a federation of local units – a legacy of multiple acquisitions over the years – to a more centralised, data-driven machine. By using Freddy.ai, the company's in-house digital marketing agency, Heineken expects to significantly improve marketing efficiency, pricing agility, and speed-to-market across its global footprint.

The aim is to grow ahead of the Beer category’s +1% volume CAGR, which combined with pricing above input cost inflation, as well as positive mix, underpins the mid-single-digit revenue guidance. Productivity savings of €400m-€500m p.a. are expected to underpin organic profit growth ahead of sales growth. EPS growth is expected to outpace EBIT growth, while the cash conversion target is 90%.

In the near-term, however, the global industry environment is challenging, with headwinds from the impact of weight-loss drugs on alcohol consumption and the request by the US Surgeon General for alcoholic drinks to carry warnings of their links to cancer. Other structural threats include Gen-Z moderation and cannabis cannibalisation, while political risk comes from the proposed US tariffs.

However, these structural concerns are not set in stone – last summer, investment bank Jefferies commissioned a survey of 3,600 US consumers to better understand their attitudes towards alcohol, finding that although moderation was becoming increasingly important, money was the biggest impediment rather than health concerns. This implies that the biggest consumption headwind is cyclical, not structural, and that a macroeconomic recovery could be an inflection point. In addition, the industry has increased its lobbying to counter the message coming from health authorities

Earlier in the year, the company announced that its Chairman of the Executive Board and CEO Dolf van den Brink would step down from his position on at the end of May. The timing came as a surprise given the CEO’s recent commitment to the financial targets. The company has been incredibly firm that this leadership change does not signal a pivot in strategic direction. The role will involve disciplined execution rather than strategic reinvention. The search for a successor is the Supervisory Board’s number one priority, but the management team is effectively ‘running on rails’ provided by the existing strategy. This strategy is not just the current CEO’s plan, but a collective blueprint co-authored by the entire Executive Team. That said, until there is more visibility over the appointment, the market will remain wary, especially given it is unclear whether the new CEO will be internal or external.

On to today’s results. The company highlights that global trade has become more complex and volatile, with impacts on energy availability and costs in certain markets. This leads to inflationary pressures, which might affect consumer sentiment in the medium-term.

In Q1 2026, net revenue grew by 2.8% on an organic basis to €6.7bn, slightly better than the 2.3% market forecast. Growth was driven by a 3.0% increase in net revenue per hectolitre as pricing was used to mitigate inflationary pressure.

Total volume grew by 1.2%, better than the flat expectation. With that, total consolidated volume decreased by 0.2%. Price-mix on a constant geographic basis increased 2.9%, led by pricing and positive portfolio mix. Licensed volume grew 26.1%, led by the growth of Heineken and Amstel by the group’s associate partner China Resources Beer (CRB) in China, as well as by strong performances in Cameroon and the reclassification of volume at contract brewers in India.

The company gained or held share in around 60% of its markets.

Beer category dynamics varied meaningfully across the group’s markets, with the revenue performance as follows:

- Asia Pacific (+8.5%), driven by Vietnam, supported by festive timings, India, and China.

- Africa & Middle East (+9.7%), with robust price-mix and volume growth led by Ethiopia and HEINEKEN Beverages.

- Americas (+0.9%), with solid price-mix offsetting modest volume declines in Brazil and Mexico.

- Europe (-2.2%), driven by mixed performance with volume growth in the UK, France, and Spain, more than offset by phasing in Poland.

The group continues to see an ongoing shift towards product premiumisation, with volume up 5.8% organically. The Heineken brand itself was also up 6.9% in the quarter. Global brands volume was up 5.7%, with Amstel growing by a high-single-digit.

Mainstream volume declined by 1.6%, with the group’s local power brands in growth led by Harar and Cruzcampo.

In the low & no-alcohol category, the company consolidated its market leadership, with volume up double-digits led by Heineken 0.0. The beyond beer segment grew by a mid-single-digit, led by Desperados and Bernini.

During the quarter the company accelerated its EverGreen 2030 strategy and is on track to deliver its €500m target for 2026. As is usual at this stage, there is no other update on the group’s profitability or financial position, although we would highlight Heineken has a strong balance sheet. At the end of 2025, financial gearing was 2.2x net debt to EBITDA, below the long-term target to be below 2.5x. The company’s dividend policy is to pay out 30%-50% of full-year net profit – the 2025 payment was up 2.2% to €1.90 (2.5% yield).

The priority for capital allocation remains organic investment, the dividend, and bolt-on M&A. The company has said it is beyond peak capex and has more to do in terms of working capital improvements. Significant deleveraging has left the company well positioned to return additional capital to shareholders – the second €750m tranche of the €1.5bn share buyback programme is ongoing.

Guidance for 2026 has been reiterated: 2%-6% operating profit growth. This reflects the company’s current assessment of beer market conditions, inflation, and other macroeconomic conditions, as well as the investments and changes required to accelerate the EverGreen 2030 strategy. Gross savings are expected to be at the upper end of the medium-term guidance €400m-€500m. However, the outlook is based on the assumption of a temporary rather than a prolonged disruption in global energy trade from the conflict in the Middle East.

Source: Bloomberg

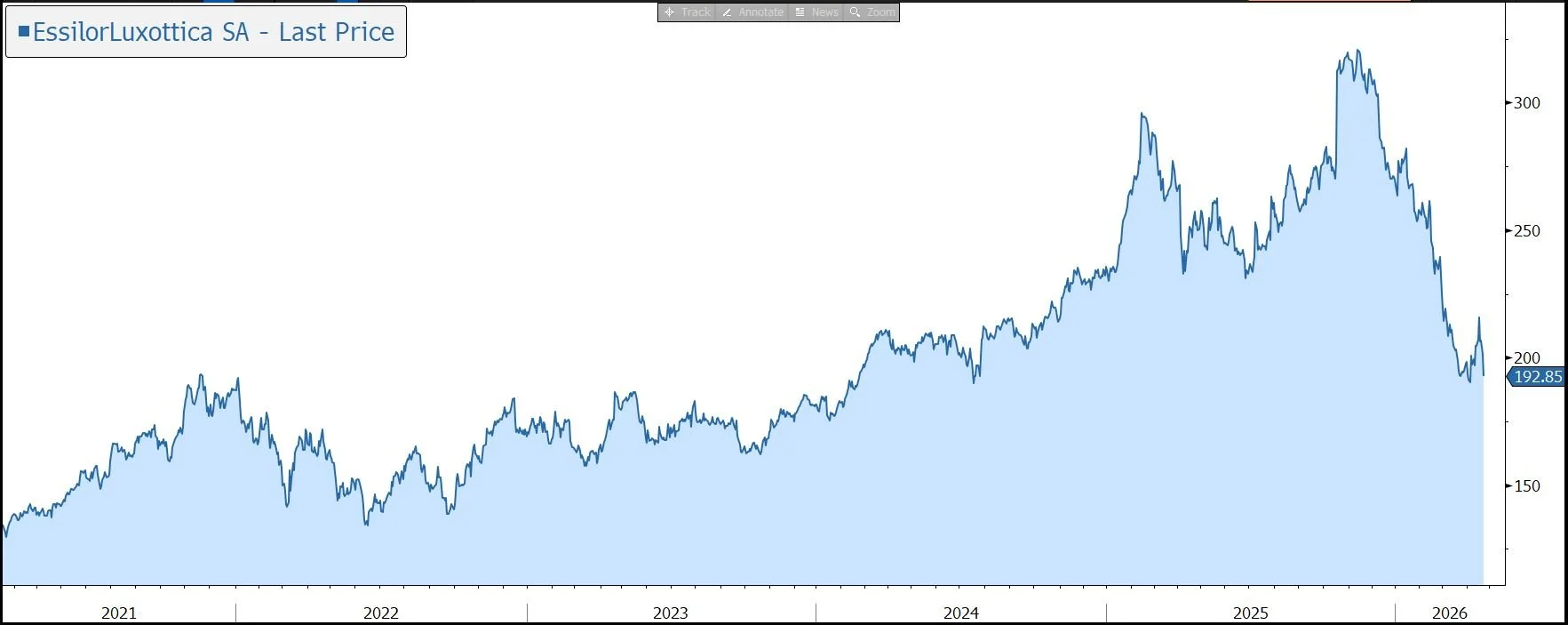

Yesterday evening, EssilorLuxottica released Q1 year results that were in line with market expectations. For the third quarter running, revenue grew by double-digits at constant currency, driven by AI smart glasses and myopia management products. The current quarter is running at the same pace and the company isn’t seeing any disruption in its supply chain as a result of the conflict in the Middle East. Medium term guidance has been reiterated. However, the shares have been marked down 4%, with the focus still on the margin dilution that comes with the explosive growth of AI glasses.

EssilorLuxottica is the global leader (with a 25% share) in the eyecare and eyewear industry with exposure to the design, manufacture, and distribution of ophthalmic lenses, prescription frames, and sunglasses. We believe the long-term outlook for the industry is positive, driven by an ageing population, digital eye strain, a growing emerging market middle class, increased education regarding sun protection, and the growth of eyewear as a fashion and technology accessory. By 2050, uncorrected poor vision is predicted to reach epidemic proportions with over 50% of the world’s population expected to suffer from myopia (short-sightedness), many with serious vision-threatening side effects and long-term implications.

The company’s competitive advantage is based on its scale, portfolio of premium brands (such as Ray-Ban and Oakley), product innovation, flexible manufacturing base, quality service, routes to consumer, and partnerships. Essilor owns long-term licences for some of the best-known luxury brands, including Chanel, Prada, Armani, and Jimmy Choo. The group also owns a majority interest in GrandVision (GV), a global leader in optical retail, expanding its global retail footprint (to c 20k stores) and reducing the competitive risk of retailer consolidation.

In addition to underlying market trends, growth is being driven by strong innovation across existing product line and in new markets. The company’s myopia management product Stellest has clinically demonstrated efficacy in slowing down myopia progression in children. Following strong growth in China, the product has now been launched in the US. In 2025, the portfolio generated global revenue growth of 22%.

In the smart glasses category, the company has a long-term partnership with Meta Platforms to develop multi-generational smart eyewear products. The collection, which includes Ray-Ban Meta and Oakley Meta Vanguard, is performing better than expected (up 3x to 7m units in 2025) with demand outpacing supply. Although the company has said that, in time, wearables will be margin accretive given the increased level of quality lenses in the products and the addition of service revenue, for now growth is margin dilutive, something of a concern for the market. The other concerns are increased competition in the space and privacy issues. We would also highlight that the relationship with Meta has been cemented following the acquisition of a 3% stake in Essilor (worth €4bn), with the prospect of a further investment.

The company has also diversified into the hearing solutions market with a disruptive new technology (i.e., lenses with acoustic technology) to meet the needs of the 1.2bn consumers suffering from mild to moderate hearing loss. The audio component is completely invisible, removing a psychological barrier that has historically stood in the way of consumer adoption of traditional hearing aids. The product (called Nuance Audio) has now been rolled out in the US and Europe.

The company has enhanced its presence elsewhere in the MedTech space through several acquisitions: Heidelberg Engineering (diagnostic solutions, digital surgical technologies, and healthcare IT for clinical ophthalmology); Espansione (design and manufacturing of non-invasive medical devices for the diagnosis and treatment of dry-eye, ocular surface and retinal diseases); Optegra (ophthalmology platform for eye hospitals and diagnostic facilities); PUcore (monomers used in the production of high index ophthalmic lenses), and Ikerian AG (operating under the RetinAI brand, specialising in AI and data management in eyecare).

Finally, Essilor also owns streetwear brand Supreme, known for its lifestyle apparel, footwear, and accessories. The company runs a digital-first business and 17 stores in the US, Asia, and Europe. At first glance, the $1.5bn acquisition looks like a diversification from the group’s core business – the rationale is that it will provide a direct channel to an audience that is very difficult to reach and adds a margin accretive business to the group. In particular, the company intends to use Supreme’s model to test exclusive, high-value AI-eyewear releases to a younger, tech-native demographic. We have some reservations and will watch to see if the move ends up being a misallocation of capital.

The overall business mix is now optical (c. 75% of total revenue), sun (23%), with the remainder from Apparel, Footwear and Accessories (including Supreme brand), smart-glasses, med-tech devices. These new categories are expected to account for a third of sales by 2034.

Back to the results. During the first quarter, revenue grew 10.8% at constant exchange rates (CER) to €7,127m, in line with the market forecast and the third consecutive quarter of double-digit growth. On the analysts’ call, the company said that growth was pretty consistent across all three months of the quarter, with the current quarter currently running at the same rate.

Growth was boosted by AI glasses, with the ‘traditional’ business running at mid-single-digit pace. Price/mix was the main driver, while volume was positive in both frames and lenses. The myopia management portfolio grew by 26%, with the key market of China up 18%.

EssilorLuxottica is a vertically integrated player with two distribution channels. Professional Solutions (PS) includes the supply of products and services to third-party eyecare professionals (i.e., wholesale).

In Q1, revenue grew by 10.8% at CER to €3,362m.

Direct to Consumer (DTC) includes the sale of products and services directly to end consumers (i.e. retail), comprised of brick-and-mortar stores and e-commerce platforms. In Q1, revenue grew by 10.7% at CER to €3,764m, with comparable-store sales up 7%.

By geography, all the broad regions grew strongly. North America, the group’s largest region (45% of sales), grew by 12.5% at CER in the latest quarter. Elsewhere, growth was: EMEA (+9.5%); Latin America (+6.7%); and Asia Pacific (9.8%). China accelerating, up low teens supported by myopia and retail. The company highlighted that the Middle East only accounts for 1% of revenue.

The recent Top Charoen deal expands the group’s retail footprint to the high-potential market of Thailand, adding around 2k stores and bringing the Group’s network to nearly 20k locations worldwide.

The group’s high US revenue exposure versus minimal sourcing in the country means Essilor is exposed to tariffs, particularly for frames which are made in China and exported to the US. In response, the company is implementing two broad measures. Firstly, diversification of the supply chain in a way that doesn’t compromise product quality. Secondly, price hikes, the benefit of which is currently flowing through. However, when the US Supreme Court struck the tariffs down in February, the company didn't immediately lower prices. This triggered a class-action lawsuit and public "price gouging" accusations.

As expected, there was no commentary on margins or profit in today’s update. Gross margins are high (60.9% in 2025), while the operating margin is 16.0%. The recent decline in the margin (13.3% in H2 2025) has unnerved the market somewhat. It is being driven by the mix effect of the AI glasses growth outweighing the accretive impact of Nuance Audio, Stellest, and the MedTech segments.

The business generates strong free cash flow (€2.8bn in 2025) and is financially robust. The group ended 2025 with net debt (including lease liabilities) of €10.85bn, 1.7x EBITDA. A dividend of €4.00 was proposed, 1.3% higher than the previous year, equating to a 2% yield.

Looking forward, on average, over the next five years, at constant exchange rates, the company is planning to deliver a ‘solid growth’ of its total revenue and a ‘broadly aligned growth’ of the adjusted operating profit. The company is still not providing specific margin guidance for 2026 but said the result would be driven by a combination of the full-year impact of tariffs, an ongoing currency headwind, mix effect of the growth of AI glasses, growth of Stellest in the US, and the roll-out of the hearing aid business.

Although the company hasn’t been specific on what ‘solid’ sales growth means, the consensus is for high single-digit growth, while margins are expected to decline at first before picking up as the period progresses.

A further near-term headwind has arisen as a result of Leonardo Maria del Vecchio’s bid to consolidate a 37.5% stake in Delfin aiming to end years of family deadlock. Controlling Delfin’s 32.3% holding in EssilorLuxottica would provide a stable governance anchor, unlock higher dividend payouts, and accelerate the MedTech pivot.

Source: Bloomberg