Morning Note: Market News and an Update from Rio Tinto.

Market News

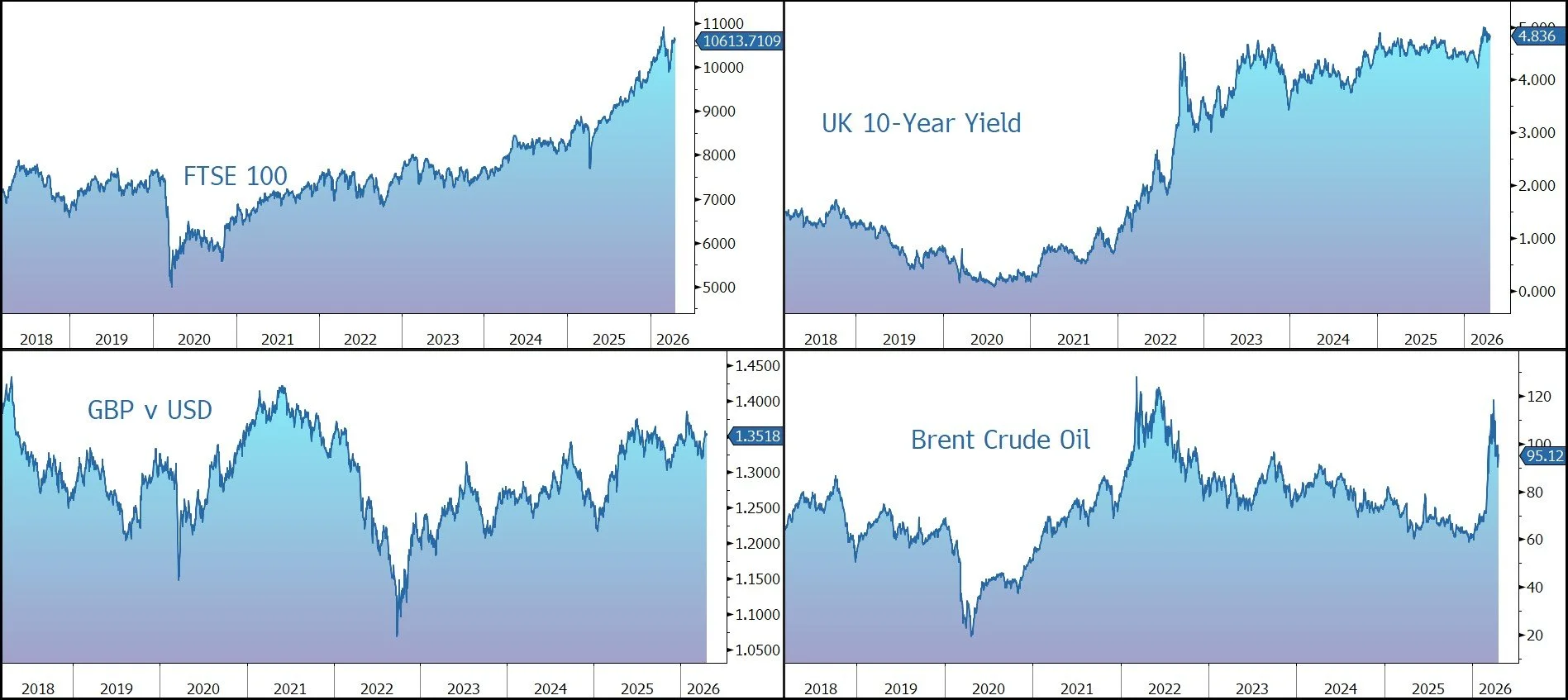

Global equities resumed after a brief pause, as signs Iran may join talks with the US added to optimism over progress in the Middle East ahead of a looming ceasefire deadline. President Trump said he’s not likely to extend the two-week ceasefire with Iran, increasing the urgency for negotiators to conclude a deal to end the war. Trump said the ceasefire will expire Wednesday evening, Washington time.

Meanwhile, transits through the Strait of Hormuz were reduced to a trickle as Iran tightened control in retaliation for strikes. Brent Crude fell 1% to $94.50 a barrel as expectations that diplomacy will prevail lifted sentiment. Gold slipped to $4,780 an ounce, while the US 10-year Treasury yield is 4.25%.

US equities slipped last night – S&P 500 (-0.2%); Nasdaq (-0.3%) – although the futures market moved higher overnight. Apple named John Ternus as its next CEO, signalling continuity over strategic change.

Hydrogen stocks such as Plug Power (+15%) and Bloom Energy (+5%) rose sharply as the US Department of Energy (DOE) took steps to secure billions of dollars in funding for several regional clean hydrogen hubs that were previously under review and at risk of termination.

In Asia, equities rallied: Nikkei 225 (+0.9%); Hang Seng (+0.4%); Shanghai Composite (+0.1%). The FTSE 100 is currently little changed at 10,614, while Sterling trades at $1.3515 and €1.1480. AB Foods (-4%) is to proceed with a demerger of Primark from its food operations.

UK wages excluding bonuses rose 3.6% in the three months through to February, slightly above expectations, while unemployment saw a surprise fall to 4.9%. Twin reports from top accounting firms highlight that a quarter of a million people could lose their job by the middle of 2027 as UK flirts with recession.

Source: Bloomberg

Company News

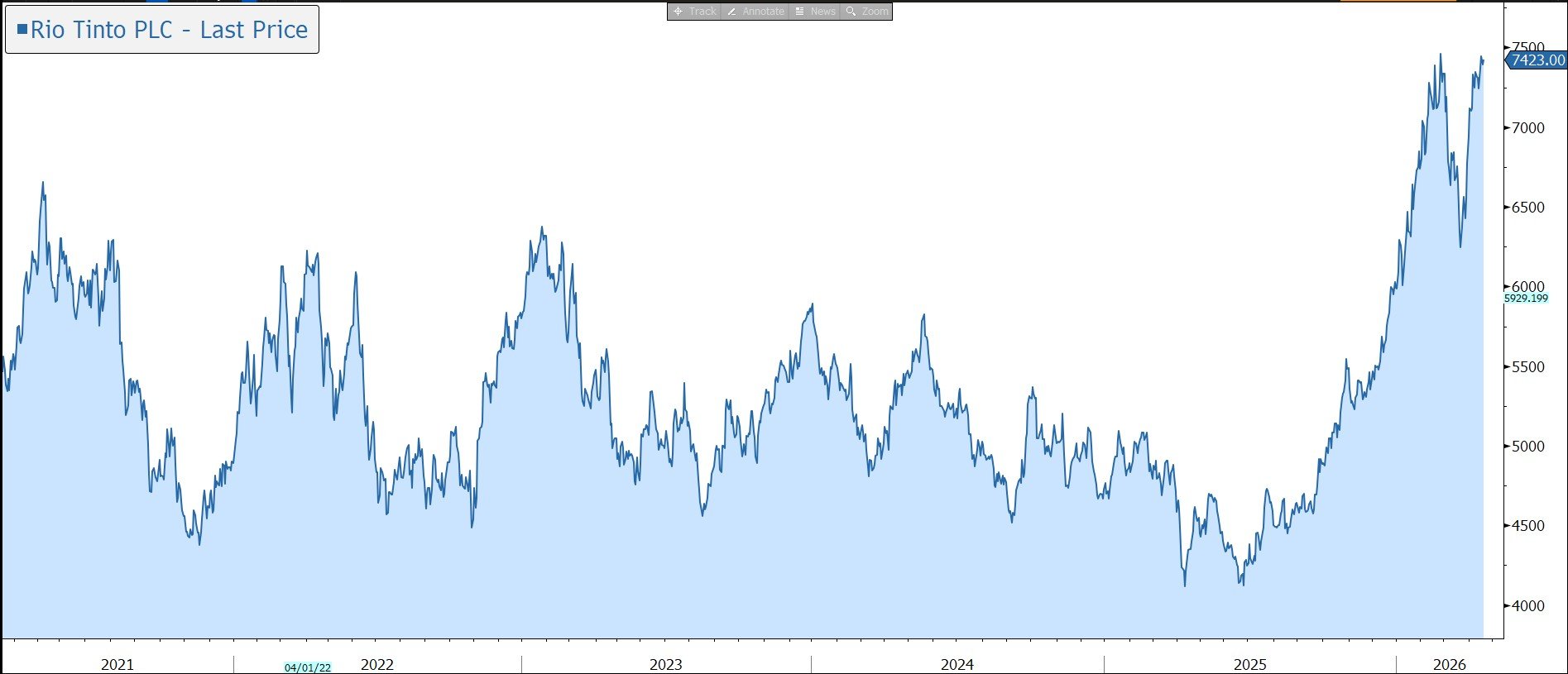

This morning, Rio Tinto released its first quarter 2026 production results. The company has provided an update on the impact of the conflict in the Middle East and reiterated its full-year guidance. In response, the shares are little changed in early trading.

Rio Tinto is a diversified global mining company. It is the second-largest seaborne iron ore producer – a commodity that accounts for around three quarters of underlying product earnings – and a major producer of aluminium, copper, and other minerals and materials. The group currently has more than 100 projects at varying stages of maturity. The target is to generate 3% CAGR production growth between now and 2033.

Rio is looking to pivot toward energy transition materials to reduce its reliance on Chinese steel demand. The company is currently on a path to reach 1 mt of copper production annually by the end of the decade, largely fueled by the ramp-up of the Oyu Tolgoi mine in Mongolia. Further expansion of the group’s exposure to copper was one of the main motivations for the (failed) merger attempt with Glencore earlier in the year.

The strategy is one of value over volume. The focus is on high-quality, long-life assets predominantly located in lower-risk countries and generally positioned in the first quartile of the industry’s cost curve. A combination of capital discipline, increased productivity, maximising cash flow from operations, and portfolio shaping is aiming to deliver strong cash generation and shareholder returns. The first $650m of annualised benefits is now fully implemented, with substantially more underway.

During the first quarter of 2026, Rio reported a 9% year-on-year increase in copper equivalent production.

Copper – production rose 9%, supported by the continued successful ramp-up of Oyu Tolgoi. Drilling at Resolution is now underway following completion of the land exchange in March.

Iron ore – second highest Q1 Pilbara production since 2018, up 13%, with sales up 2%. Tropical cyclones impacted Pilbara shipments by approximately 8Mt, with around half expected to be recovered. The first full SimFer shipment of high-grade Simandou product was successfully delivered to China with first sales realised in April.

Aluminium – Production rose by 1% as strength and agility was again demonstrated across the group’s integrated value chain offset weather-related disruptions in bauxite.

Lithium – Fenix 1B and Sal de Vida achieved mechanical completion as planned, with first production on track for H2 2026.

The statement provides some reassurance on the impact of the conflict in the Middle East. On the supply-side, the direct impacts on Rio’s operations have been limited, while commodity prices have responded favourably. The group’s scale, global reach, and sophisticated supply chains provide a resilient foundation and have enabled the business to operate normally. Guidance for the full year is unchanged for production/sales and unit costs.

Overall, we believe commodities and resource stocks are inexpensive when compared to financial assets and are relatively under-owned in investor portfolios. We believe they also provide something of a hedge against inflation.

Source: Bloomberg