Morning Note: Our Thoughts on the Impact of the Oil Market and an Update on Retailer Inditex.

Market News

Equity markets stabilised and oil held below $90 a barrel after a report on the proposed release of oil reserves to ease higher energy prices boosted market confidence, following recent volatility across assets. The IEA proposed the largest ever release of oil reserves, bigger than the 182m barrels deployed after Russia invaded Ukraine. Member countries are expected to decide today, the WSJ reported.

Gold held at around $5,200 an ounce. The 10-year Treasury yields 4.16% as traders reduce expectations for policy easing by the Federal Reserve to just one rate cut this year. Christine Lagarde said the ECB will ensure the Iran war doesn’t cause the same inflation surge as Russia’s Ukraine invasion did. However, an ECB rate hike is potentially closer than thought, Governing Council member Peter Kazimir says.

US equities were little changed last night: S&P 500 (-0.2%); Nasdaq (flat). Oracle jumped 11% post-market after its Cloud revenue beat expectations. JPMorgan told private credit lenders that it marked down the value of some loans, the FT reported.

In Asia this morning, the oil price retreat helped to boost equity markets: Nikkei 225 (+1.4%); Hang Seng (-0.4%); Shanghai Composite (+0.3%). Nintendo rose 10% following surging sales of a Pokémon game. According to a Reuters poll, the Bank of Japan will raise interest rates next quarter with expectations unchanged by the war. China’s vehicle deliveries fell 15% in February, as the end of government subsidies worsened the usual holiday slump.

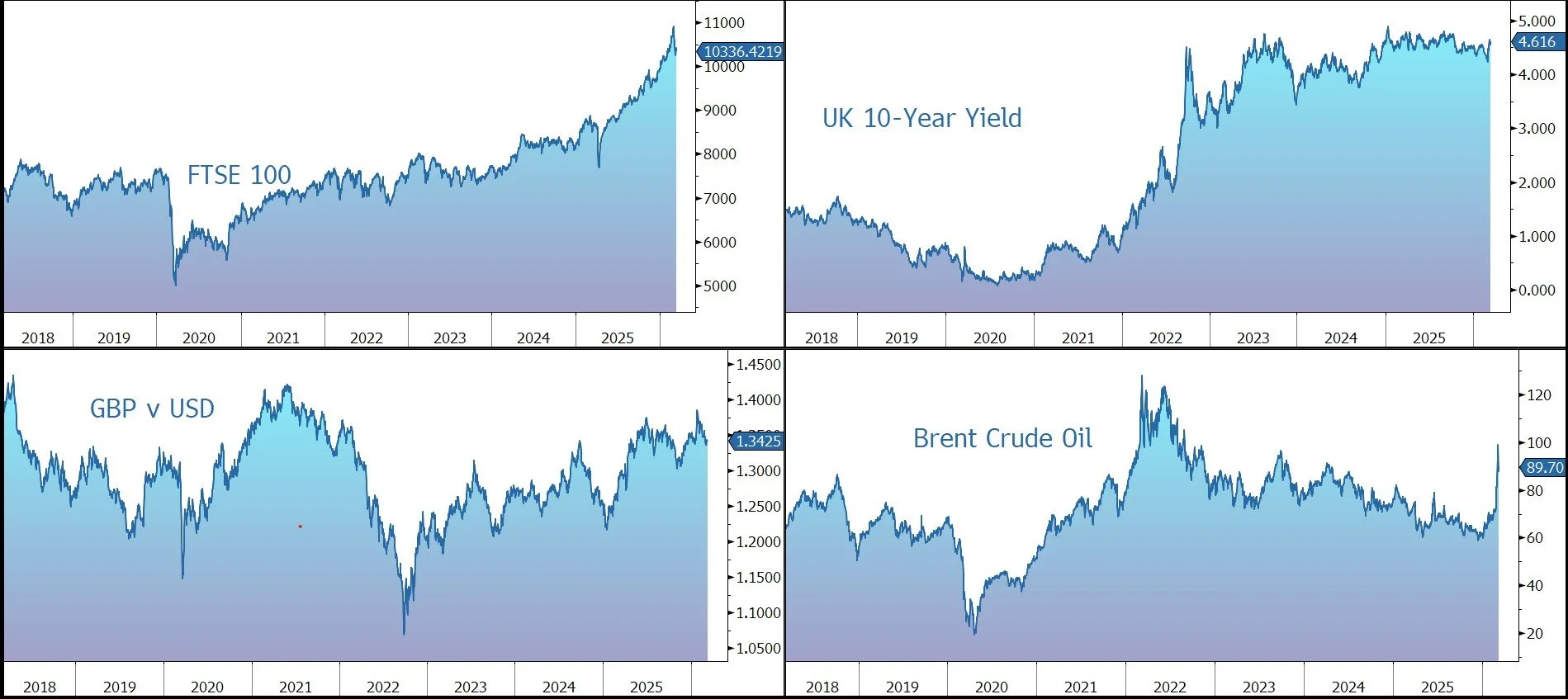

The FTSE 100 is currently 0.7% lower at 10,336. Legal & General is trading down 4% as the company missed annual profit expectations. Sterling trades at $1.3435 and €1.1565.

Source: Bloomberg

Oil Market – Update and Thoughts

- The continued conflict between the US/Israel and Iran and resulting disruptions to oil flowing through the Strait of Hormuz led oil prices to spike. WTI Crude peaked at $119 in the early hours of Monday.

- These most extreme levels were quickly reversed. In the morning, the G7 revealed plans for a coordinated release from strategic reserves. Towards the US market close, Donald Trump indicated that the US was “very close to finishing” its activities in the region. Prices fell back to around $88 as of Tuesday morning, slightly below their closing level on Friday. Both bonds and equities traded as a mirror image of oil.

- This price action tells us that the market cares much less about whether the fighting is continuing than it does about whether the oil flowing. It also tells us that the authorities understand that a prolonged period of extremely elevated prices is bad news for asset prices and their economies. The degree of control that they can exert if Iran is determined is unclear. However, it is noteworthy both that the US is floating the idea of taking control of the Strait and China, Iran’s main supporter in terms of its ability to stay in the fight and with the most to lose from a disruption in supplies, is pushing for a deal.

- Attacks that do lasting damage to oil infrastructure are in the medium term, more damaging than the closing of the Strait of Hormuz in the sense that once the issue with the latter is resolved, it can come back online quickly. The same is true when production is curtailed as restarting it again can take months.

- These events demonstrate firstly, how critical oil still is to the global economy and secondly how little exposure investors have to energy with the sector making up such a small part of the market capitalisation. A major curtailment of energy supply is a shock to the economy that both increases price (inflation) and reduces output (GDP). Bonds hate the former, equities hate the latter and a traditional portfolio of equities and bonds becomes correlated rather than diversified as both asset classes do poorly. This was the story of 2022.

- Energy prices going up a bit is inflationary. Energy prices going up a lot is deflationary because it sets in motion a cycle of demand destruction. This is why it’s so hard to protect oneself.

- The number one job of any investor is to efficiently collect “risk premiums” and diversify well by making smarter, more thoughtful allocations to different assets. The only reason there is “premium” is because there is “risk”. Current events are a manifestation of this. You must either accept the latter or forgo the former. The number one job of a trader is to make many “bets” over time and have some combination of the number and size of winners versus losers that reflects an underlying edge that compounds over time. Guessing and getting it right on a one-off event isn’t an edge, it’s a fool’s errand.

- Therefore, our recommendation is that a portfolio should include more assets that can benefit from these dynamics than exist in traditional benchmarks such as energy and resource equities. Not necessarily because their return expectations are higher than other sectors but because their capacity to be uncorrelated lowers overall portfolio risk. It includes more idiosyncratic assets such as precious metals, trend following strategies that can be long appreciating commodities and macro hedge funds that can structure trades with long volatility exposure.

Company News

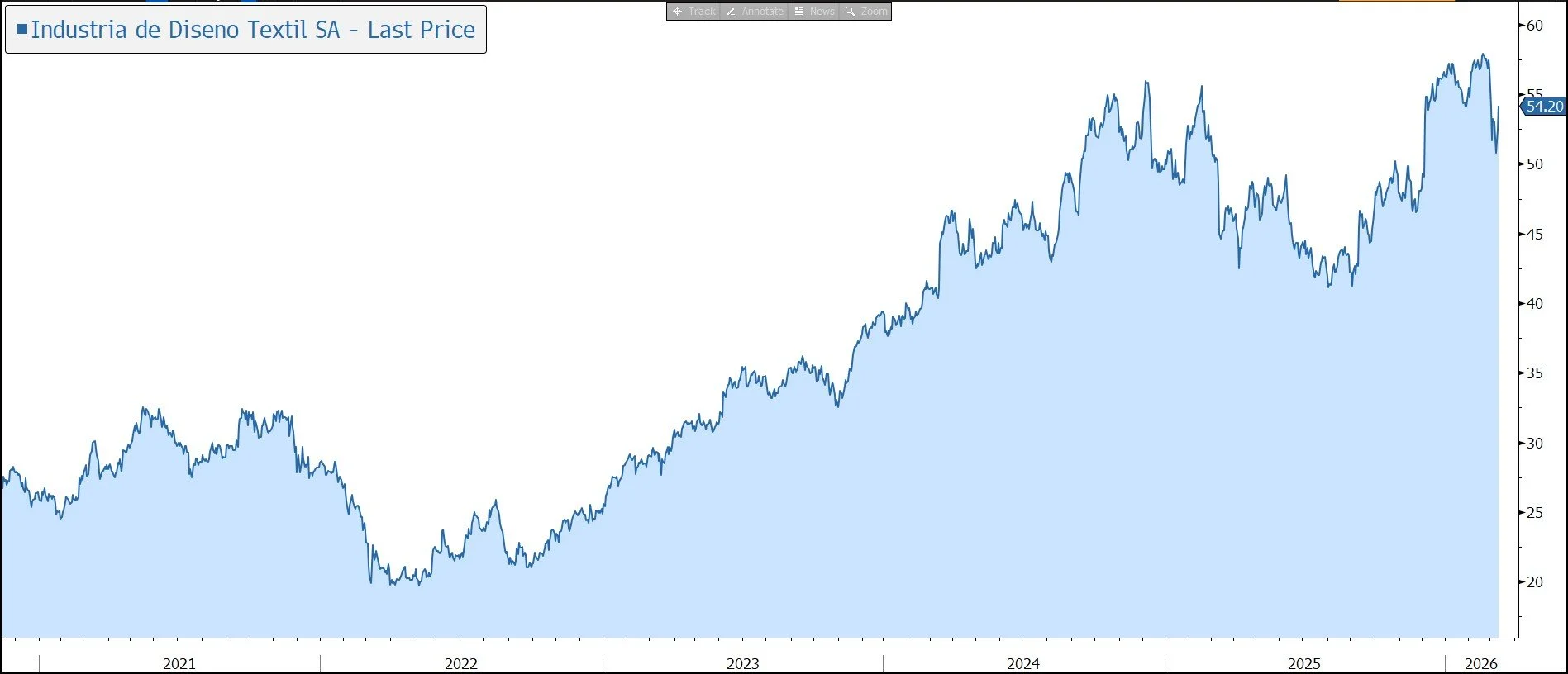

Inditex has today released results for its financial year to 31 January 2026 (known as FY2025). Driven by a robust operating performance, the figures were in line with market expectations, and the dividend was raised by 4%. The company highlights the current year has got off to a good start. In response, the shares have been marked up by 2% in early trading.

Inditex is the world’s leading apparel retailer, with annual sales of almost €40bn. Through brands such as Zara, Pull&Bear, and Massimo Dutti, the group has around 5,460 managed and franchised stores and a strong online presence.

The company’s strategy based on fast fashion at attractive prices has met with headwinds on environmental grounds and, in response, the group has transformed towards a fully integrated, digital, and sustainable business model. With a low share of a highly fragmented market, the company sees strong growth opportunities, with sales productivity in its stores increasing.

The group is undertaking an ongoing store optimisation plan – over the last 3 years, the number of stores has been reduced by 6%, but net space has risen by 6%. In 2025, there were openings in 41 markets and gross new space increased by 5.3%.

In FY2025, sales grew by 7.0% in constant currency to €39.9bn, with growth in all concepts and geographic regions. Online sales grew by 4.8% to €10.7bn, representing 27% of total sales.

Gross profit increased by 3.9% to €23.2bn and the gross margin rose by 42 basis points to 58.3%. The group has continued to ‘rigorously’ manage its operating expenses, which grew by 2.8%, below the rate of sales growth. Net income increased by 6% to €6.2bn.

Despite rising sales, inventory was 2% lower at 31 January 2026 than the year before. Free cash flow generation was strong at €4.7bn, albeit just below the €4.8bn of last year. The group ended the period with net cash of €11.0bn, down 5%. The board is proposing a dividend of €1.75 (3.2% yield), up 4% on last year, and made up of an ordinary dividend of €1.20 and a bonus dividend of €0.55.

In the current quarter, between 1 February and 8 March, store and online sales rose by 9% year on year and Spring/Summer collections “well received” by customers.

The increase in annual gross space in 2026 is expected to be around 5% with a positive net space contribution, in conjunction with strong online growth. Ordinary capital expenditure is expected to be €2.3bn in 2026 and the gross margin is expected to be stable (+/- 50 basis points).

Source: Bloomberg