Morning Note: Market News and an Update from Halma.

Market News

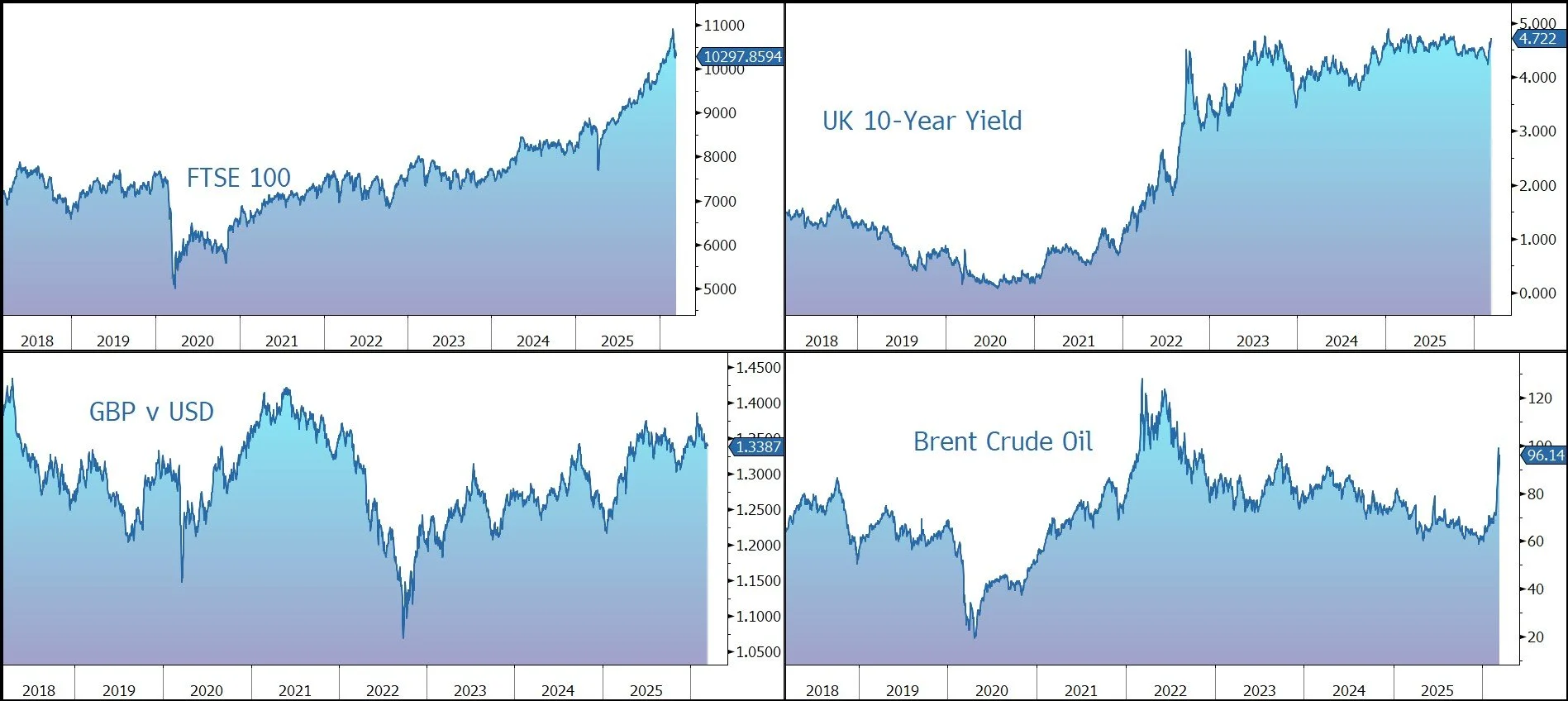

The oil price rallied back up to $100 a barrel (before falling back) on renewed supply fears after an attack on tankers in Iraqi waters highlighted the threat to energy infrastructure in the Middle East. The US plans to tap 172m barrels as part of the IEA’s reserve release plan of 400m barrels. The dollar firmed, while gold trades at $5,180 an ounce.

Global bonds remained weak on inflation fears – the 10-year Treasury yield moved up to 4.23%. On the data front, February inflation came in line with forecasts, showing stable but above-target CPI. However, the full impact of the energy surge from the conflict has yet to be reflected. The Fed is widely expected to keep the federal funds rate steady next week, with traders pricing in only one 25 basis points cut, possibly in September.

Mounting strain in the private credit market also weighed on sentiment as Morgan Stanley and Cliffwater LLC capped withdrawals from their multibillion-dollar private credit funds

US equities were little changed last night – S&P 500 (-0.1%); Nasdaq (+0.1%). In Asia this morning, the yen neared its low of the year against the dollar, and stock drifted: Nikkei 225 (-1.0%); Hang Seng (-0.8%); Shanghai Composite (-0.1%).

The FTSE 100 is currently 0.5% lower at 10,298, while Sterling trades at $1.3384 and €1.1585. The 10-year Gilt currently yields 4.63%. Estate agents are growing more pessimistic about the housing market as the war dashes hopes of lower borrowing costs, a survey found. The Bank of England Governor Andrew Bailey is due to speak today.

Source: Bloomberg

Company News

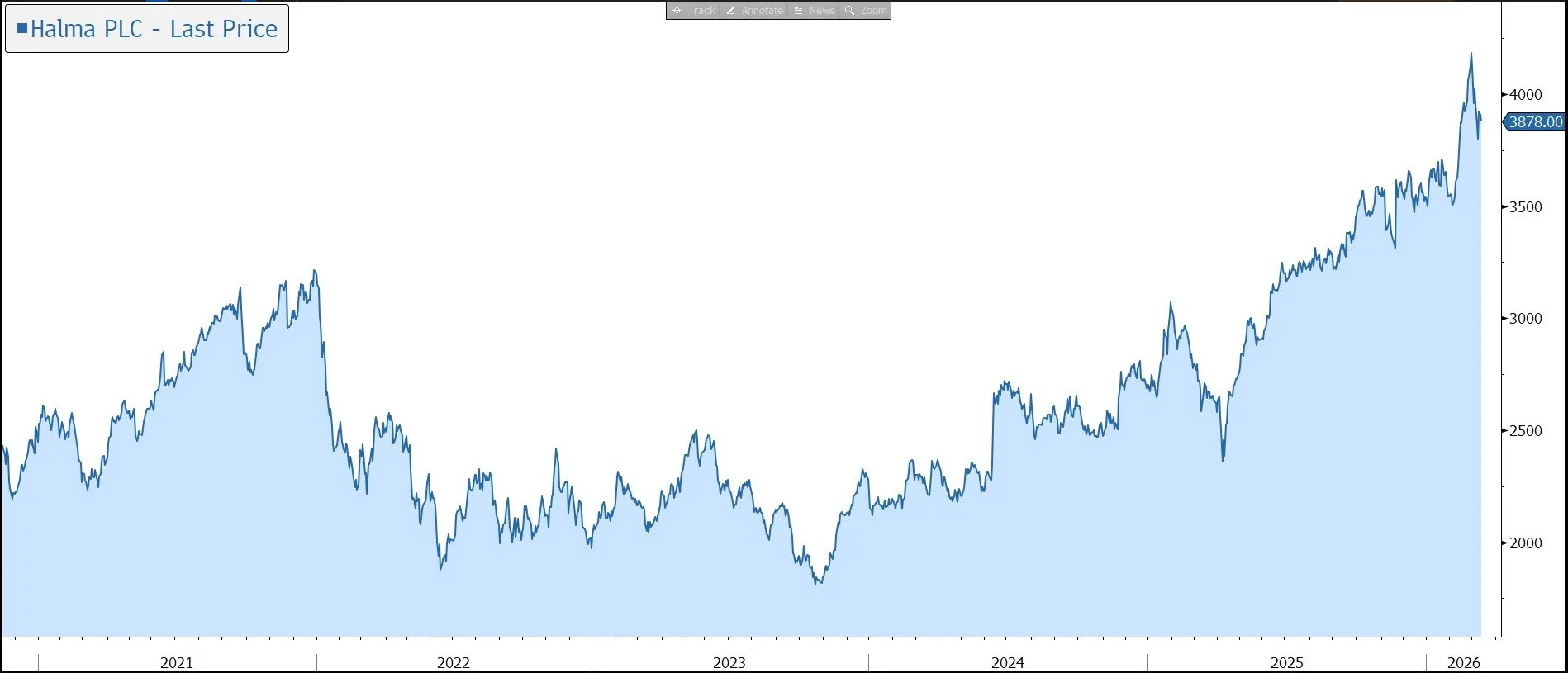

Halma has today released a scheduled trading update ahead of its financial year end on 31 March 2026. The group reports it has made further strong progress in its second half, consistent with existing guidance, and is on track to deliver its 23rd consecutive year of record adjusted profit. The shares have been strong of late and in response to today’s announcement they are little changed in early trading.

Halma is a global group of 50 or so life-saving technology companies, with a focus on safety, healthcare, and the environment. The group’s technology is used to save lives, prevent injuries, and protect people and assets across a broad range of sectors including commercial and public buildings, utilities, healthcare/medical, science/environment, process industries, and energy/resources.

Products include control panels for fire safety systems, corrosion monitoring systems, gas detection systems, moisture control systems, and blood pressure monitoring systems. As a result, the company is highly diversified across different industrial cycles.

The main growth drivers include increasing health and safety regulation, demand for healthcare from an ageing population, and demand for life-critical resources. Strong market positions deliver upgrade and replacement sales opportunities as customers seek to maintain regulatory compliance and conform with best practice. As a result, customer spending is often non-discretionary and drives sustained demand throughout the economic cycle. Over time, this has driven consistent profit growth and shareholder returns.

Over recent months, although Halma’s companies have continued to experience varied conditions in their end markets and operate in an increasingly uncertain economic and geopolitical environment, the business has delivered broad-based growth.

The group continues to expect it will deliver, in the year as a whole, mid-teens percentage organic constant currency revenue growth for the full year to end March 2026, including a continued benefit from premium growth in photonics within the Environmental & Analysis Sector. This guidance is supported by order intake which remains ahead of both revenue in the year to date and the comparable period last year.

The adjusted operating profit (EBIT) margin has benefitted from positive operational gearing and is still expected to come in at ‘around 22%’. This excludes the one-off profit from the Nuvonic transaction (UV disinfectant systems) which was completed in the first half of the group’s financial year.

In what was a brief statement, there was little detail on the group’s performance by sector or region – more clarity is expected at the time of the results in June. The company did highlight that the appreciation of Sterling is expected to have a negative currency translation effect on the results.

The balance sheet is robust – at the half-year stage last September, financial gearing was only 1.03x net debt to EBITDA, well within the target of ‘up to 2x’. Full year cash conversion is expected to be in line with the group’s target of 90%.

This enables continued investment, both organically and by acquisition, to support continued growth. Halma has completed five acquisitions across the group’s three sectors, with a record £451m invested. The acquisition pipeline remains healthy.

Halma also has a fantastic dividend track record, having increased the payout by 5% or more every year for the last 45 years. The half-year dividend was raised by 7% and we would expect a similar progression to be announced for the final dividend with the results in June.

Source: Bloomberg

Disclaimer

When investing, your capital is at risk, which means the value of your investments can both rise and fall over time. You must be comfortable in the knowledge that you may receive less than you originally invested. Past performance may not repeat itself. This document has been issued by Patronus Partners Limited on the basis of publicly available information, internally developed data and other sources believed to be reliable, but we have not independently verified such information and we do not give any warranty as to its accuracy. This document does not purport to be a complete description of the securities, markets or developments referred to in the material. All expressions of opinion are subject to change without notice. Nothing in this communication constitutes investment advice or a personal or research recommendation.