Morning Note: Market News and Updates from Visa, AstraZeneca, and Atlas Copco.

Market News

Donald Trump instructed his aides to prepare for an extended blockade of the Strait of Hormuz, the WSJ reported. The US Treasury warned financial institutions of sanctions risks tied to Chinese refineries handling Iranian oil.

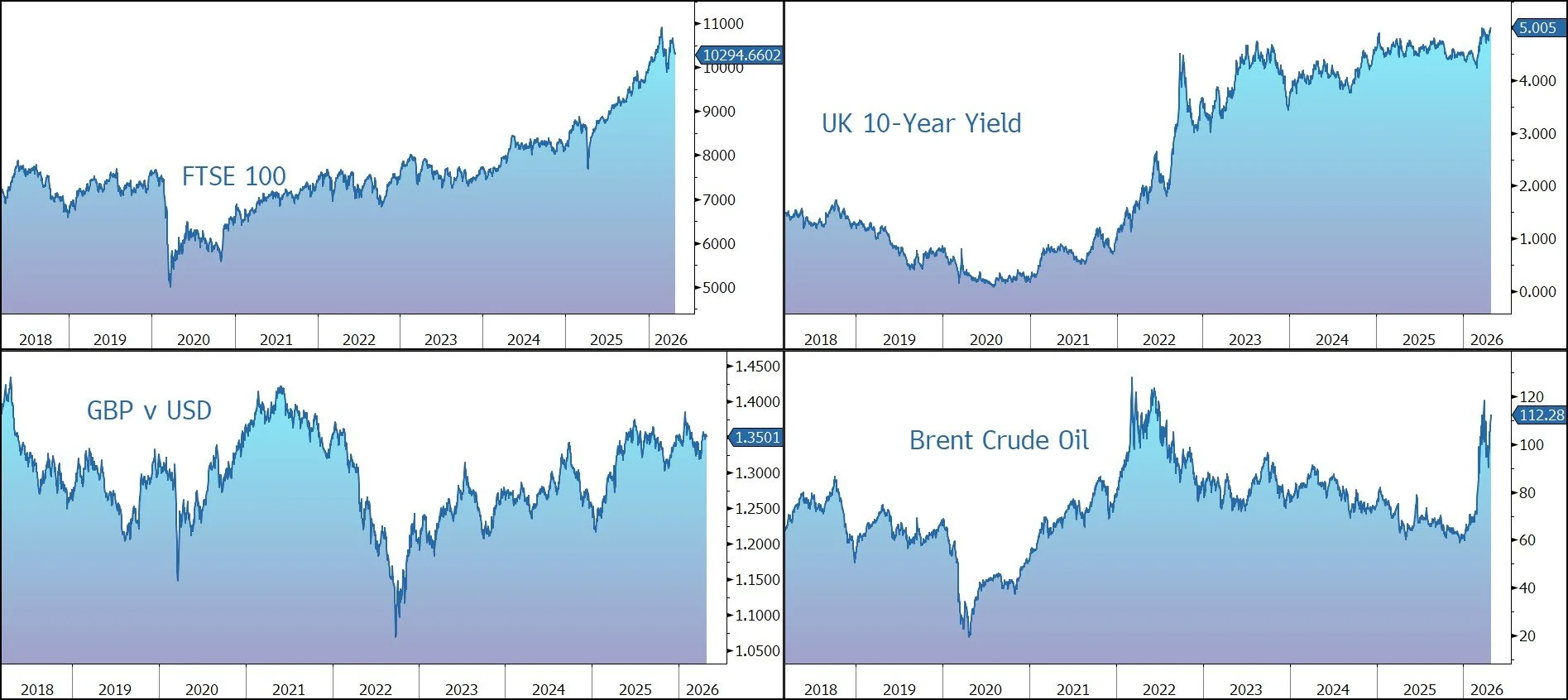

Brent crude futures held above $111 per barrel after gaining around 3% in the prior session, supported by mounting uncertainty around global supply. Elsewhere, the ongoing conflict has prompted the UAE to announce its exit from OPEC next month for greater flexibility in adapting to shifting market conditions.

Gold continued to drift lower – it currently trades at $4,570 an ounce – while the yield on the US 10-year Treasury stands at 4.35%.

US equities traded lower last night – S&P 500 (-0.5%); Nasdaq (-0.9%) – although positive results from Visa (see below) and Starbucks helped support the market. Traders now look forward to the Fed’s rate decision and earnings from four of the Mag 7 (Alphabet (Google), Meta, Microsoft, and Amazon)).

In Asia, equities were firm: Nikkei 225 (closed); Hang Seng (+1.7%); Shanghai Composite (+0.7%). The FTSE 100 is currently 0.3% lower at 10,294, while Sterling trades at $1.3505 and €1.1535. Rachel Reeves won a battle for the authority to force pension funds to invest a proportion of their assets in the UK after the House of Lords dropped its opposition.

UBS’s Q1 profit topped estimates. The bank confirmed its intention to add to the $3bn tally of share buybacks this year. Santander’s net income also beat, while Deutsche Bank posted higher-than-expected profit and revenue, with fixed-income and currencies trading roughly flat from a year ago. Kone agreed to acquire TK Elevator for €29.4bn, including debt, in what will be one of Europe’s biggest ever PE exits.

Source: Bloomberg

Company News

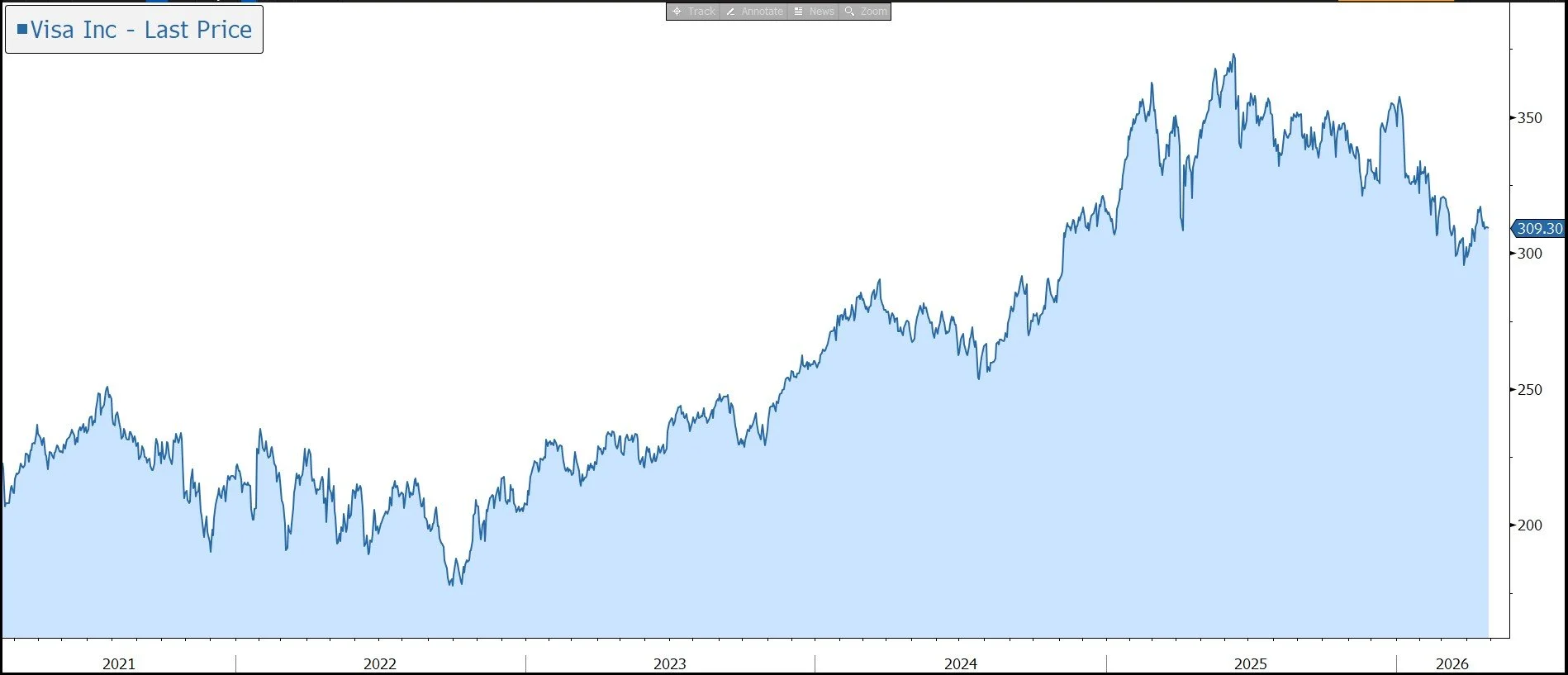

Yesterday evening, Visa released results for the three months to 31 March 2026, the second quarter of its FY2026 financial year, that were better than forecast. Revenue growth was the highest since 2022, driven by resilient consumer spending and continued strength in consumer payments, commercial and money movement solutions, and value-added services. Guidance for the full year was raised and, in response, the shares were marked up 5% after hours.

Visa is the world’s largest electronic payments network. It connects nearly 14,500 financial institutions, 175m merchant locations, and around 12bn cards, bank accounts, and digital wallets. Visa is not a bank; it doesn’t lend or take on credit risk. It doesn’t issue cards or place the terminals at the merchant locations. Instead, the company earns a small fee from 258bn transactions processed on its network to generate annual revenue of $40bn. The company is increasingly evolving into ‘Visa-as-a-Service’ which involves unbundling Visa’s product set to support more customers in more ways across its service stack. Revenue outside of traditional Consumer Payments (i.e. Commercial & Money Movement Solutions and Value Added Services now account for more than 30% of revenue)

Outside of the US, Visa is still benefiting from the ongoing shift from cash and cheques to electronic means of payment, and the growth of online retail, contactless, and mobile payment systems. In emerging markets, a lack of physical communication infrastructure traditionally provided a barrier to payments growth, but that has been removed by the emergence of mobile phone technology and a government focus on digitalising cash to reduce the black economy. Finally, there is an opportunity for Visa’s trusted network in agentic commerce where autonomous AI agents act on behalf of consumers to discover, compare, and purchase products or services. In these transactions, security, authentication, and fraud tools that Visa provide will grow in importance. The company is currently working with over 100 partners across the commerce ecosystem to enable agentic commerce, with over 30 partners that are actively building in Visa’s ‘sandbox’ with multiple agents and agent enablers running live production transactions.

In Consumer Payments, Visa estimates a total market of $41tn worldwide, with 56% ($23tn) still available to be served, including $11tn cash and cheques. The company has six areas of focus including: “tap to everything”, token technology, cross-border, affluent consumers, A2A (account to account payments), and credit. Since 2020, the number of Visa tokens has increased from 1bn to 17.5bn, with adoption led by ecosystem benefits including 5% higher authorisation rates and 30%+ lower fraud.

Growth in Commercial & Money Movement Solutions (CMS, formerly known as ‘New Flows’) is expected to outpace the Consumer Payments business over the long term. The company believes the total addressable market of the opportunity is massive – $145tn in B2B payments and $55tn in disbursements/payouts/P2P. Even though yields for these new flows are lower on average than Consumer Payments (often due to high-volume, low-complexity B2B transfers), they utilise Visa’s existing infrastructure and take advantage of the company’s massive scale and fixed operating costs, resulting in higher margins.

The group’s third growth engine is Value Added Services that help its clients and partners optimise their performance, differentiate their offerings, and create better experiences for their customers. The company estimates the total addressable market at $520bn, meaning only 2% has been penetrated so far. Many of Visa’s largest clients now use more than 20 value-added services, such as cybersecurity, fraud, advisory services, identity solutions, data analytics, and AI, all of which enhance the group’s competitive advantage.

During the three months to 31 March 2026, against a backdrop of high oil prices and heightened geopolitical tensions, consumer spending remained resilient, and the group’s strategy and innovations fueled strong performance in consumer payments, commercial and money movement solutions, and value-added services. The company continued to enhance its Visa as a Service stack, including with agentic and stablecoin capabilities, to further strengthen its position as the leading hyperscaler of payments globally.

Trends were strong across key metrics: payments volume (+9% in constant currency, with debit and credit up 8% and 10% respectively), processed transactions (+9% to 66.1bn, slightly below market expectations), and cross-border volume growth (which includes a lot of e-commerce as well as travel, +12%).

Net revenue grew by 16% on a constant currency basis in the quarter to $11.2bn, above the market forecast of $10.7bn. This was the highest growth rate since 2022 and the above company guidance for growth in the low double-digits.

Revenue was made up of service revenue (based on prior-quarters payment volume, +13% to $5bn); data processing (+18% to $5.5bn); international transaction revenue (+10% to $3.6bn); and other revenue (+41% to $1.3bn). Client incentives, a contra-revenue item, were up 14% to $4.2bn, lower than expected.

On the call, the company highlighted that Commercial & Money Movement Solutions grew by 24%, value added services revenue rose by 27%, and Visa Direct transactions increased by 23% to 3.7bn.

Operating expenses were up 17% in the quarter, with the increase primarily driven by increases in personnel and marketing expenses. Adjusted EPS was up 20% on a constant currency basis, to $3.31, well above the market expectation of $3.10 and the company guidance for growth at the high-end of low double-digits.

During the quarter, Visa generated $2.6bn of free cash flow. The group’s balance sheet remains strong, with cash, cash equivalents, and available-for-sale investment securities of $14.2bn at the end of March. The main capital allocation priority is to invest to grow the business, both organically and via acquisition – agentic commerce and stablecoins are areas of investment focus in FY2026.

Visa also has an ongoing commitment to return excess cash to shareholders. The group has a record of strong dividend growth, with the latest quarterly payout raised by 13.6% to $0.67. During the quarter, the company also bought back $7.9bn of its stock as part of its $30bn authorised programme and recently authorised a new $20bn multi-year programme.

Visa has a long-term track record of coping with regulatory challenges and has flexibility in its cost base to mitigate any bottom-line impact. Earlier in the year, President Trump called for a one-year, 10% cap on credit card interest rates, significantly lower than the current market average of over 20%. This will require a legislative change, with Trump formally asking Congress to codify the cap. We believe the 10% cap is a volume risk, not a margin risk for Visa. It threatens the ‘network effect’ by potentially shrinking the pool of active spenders, but it reinforces the strategic importance of Visa’s diversification into New Flows and Value Added Services.

Overall, we believe the long-term growth prospects for Visa remain attractive, more so given the acceleration in recent years in the shift to e-commerce, tap-to-pay, and new digital payments, and in the number of acceptance points at SMEs (particularly tap-to-phone). In addition, the broad application of digital payments by businesses and government agencies provides a huge market opportunity. The long-term revenue growth framework is: Consumer Payments at 5%-7% and Commercial & Money Movement Solutions/Value Added Services at 16-18%, with the latter moving from a third to a half of revenue over time. This implies total net revenue growth of 9%-12%.

The company raised its guidance for the financial year to 30 September 2026 on a constant dollar basis. Revenue growth is now expected to be in the low-double-digit to low-teens (vs. low double-digits previously). EPS growth is now expected to be in the low teens (vs. low double-digits previously).

On the call the company, the company outlined performance in the first three weeks of April, with processed transaction growth of 8% and cross-border volume growth of 10.5%. For the current quarter as a whole, the company expects to generate revenue growth in the low double-digits. With expenses expected to increase in the low teens, in part due to World Cup related marketing, EPS is expected to grow in the mid to high single-digit.

While some short-term economic uncertainty persists, the group remains confident in its ability to execute its strategy and expand Visa’s role at the ‘centre of money movement’. That said, a slowdown in overall consumer spending could be a drag on volumes, although spending across the network is very diversified, be it credit vs. debit, domestic vs. overseas, discretionary vs. non-discretionary spend, and low vs. high ticket spend. However, the company has previously said that if we do go into a recession, Visa is now stronger in debit – the card of choice in tougher times – than it was in the 2008/09 financial crisis. The group also highlights that if there is a downturn, they have plenty of flexibility on costs and client incentives. Note also that half of the group marketing spend is variable.

Source: Bloomberg

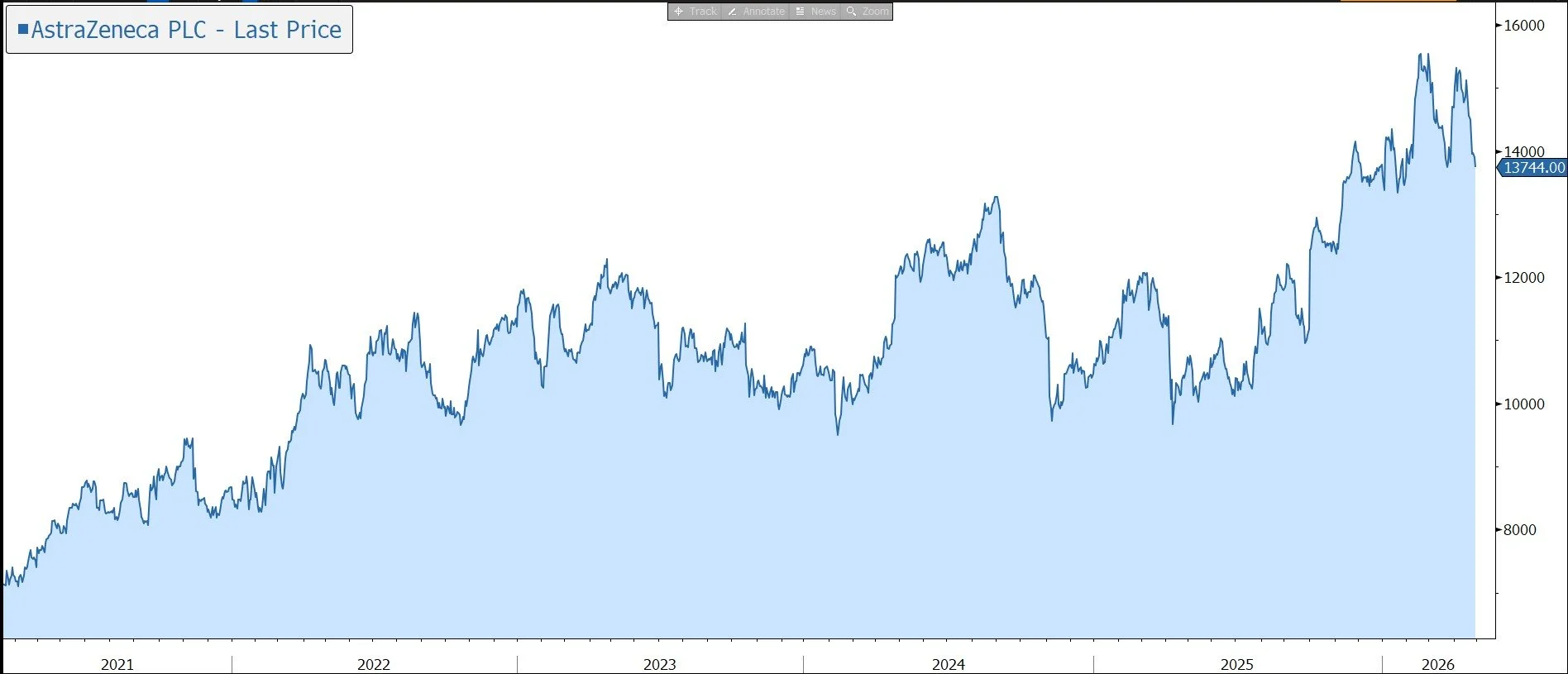

AstraZeneca has released its Q1 2026 results. The figures were slightly ahead of the market expectation, driven by double‑digit growth in Oncology and Rare Disease. Guidance for 2026 has been reiterated, with earnings expected to rise by low double digits, and the company remains on track to achieve its ambition for 2030 and beyond. In response, the shares are down 1% in early trading.

AstraZeneca (AZ) is a global, science-led biopharmaceutical company. The main growth driver has been the group’s key Oncology franchises (including Tagrisso, Lynparza, Enhertu, Imfinzi, and Calquence), which have been supplemented by the other growth platforms of Respiratory & Immunology (R&I), Cardiovascular, Renal, & Metabolic diseases (CVRM), Vaccines & Immune Therapies (V&I), and rare diseases (via the $41bn acquisition of Alexion).

The group’s (tough) ambition is to deliver $80bn of revenue by 2030, up 8.3% p.a. from a 2023 base of $45.8bn. This will be driven by growth across its existing portfolio through geographic expansion and follow-on indications, as well as new products currently in late-stage development, offset by the loss of patent exclusivity in some existing products. The group expects to launch 20 new medicines before the end of the decade, with some products having the potential to generate more than $5bn in peak-year revenue.

Beyond 2030, the company will seek to drive sustainable growth by continuing to invest in transformative new technologies and platforms that will shape the future of medicine. Management’s confidence is driven by the large number of readouts in 2027-29 for assets that are likely to reach peak sales beyond 2030, including camizestrant (breast cancer), rilvegostomig (oncology) and the haematology portfolio.

The aim is to generate a mid-30s core operating margin by 2026, versus 32% in 2023. Beyond 2026, the margin will be influenced by portfolio evolution and the company will target at least the mid-30s percentage range.

AZ currently invests more than 20% of sales in R&D and uses partnerships to gain access to innovative technology. The group has an attractive pipeline of potential new products, the success or failure of which will drive future profitability and the share price.

Recent news flow on the pipeline has mainly been positive – in 2025 the company delivered 16 positive Phase III study read-outs and 43 approvals in major regions. The company now has 16 blockbuster medicines (i.e. sales above $1bn). The momentum across the company has continued in 2026, with results of more than 20 Phase 3 trial readouts and more than 100 Phase 3 studies ongoing. The group has announced positive readouts for four high-value Phase III programmes since the Q4 2025 results including Tozorakimab (Chronic Obstructive Pulmonary Disease, COPD); Imfinzi (gastric cancers); and Efzimfotase alfa (hypophosphatasia).

In January 2026, AZ announced plans to invest $15bn in China through to 2030 to expand medicines manufacturing and R&D. These investments build on the company’s substantial footprint in China, including global strategic R&D centres in Beijing and Shanghai.

Back to today’s results, revenue increased by 8% at constant exchange rates (CER) to $15.3bn, slightly better than the market forecast of $14.9bn. By therapy area, product sales grew 16% in Oncology, 7% in Respiratory & Immunology, and 15% in Rare Diseases. The main decline was CVRM, which fell 6%.

Core operating expenses rose by 7% at CER, with R&D and SG&A up 8% and 7%, respectively. The operating margin was up one percentage point to 35%. Core EPS grew by 5% at CER to $2.58, versus the market forecast of $2.52. The slower rate of growth reflected the favourable tax rate in the prior year period.

AZ has a robust balance sheet and generates strong free cash flow. In Q1, net debt increased from $23.4bn to $25.9bn, around 1.3x net debt to EBITDA. The company’s capital allocation priorities include investing in the business and the pipeline.

M&A remains central to the strategy. The company recently closed a new strategic collaboration agreement with CSPC Pharmaceuticals to advance the development of multiple next-generation therapies for obesity and type 2 diabetes. AstraZeneca will pay an upfront payment of $1.2bn.

AZ is also committed to a progressive dividend policy and intends to maintain or grow the payout each year. In 2025, the company raised its payout by 3% to $3.20, equating to a yield of 3%. In 2026, the company intends to increase the annual dividend to $3.30.

Political headwinds have eased somewhat and the company struck a deal with the US administration. In return for a three-year exemption from pharmaceutical tariffs, AZ agreed to implement price-lowering measures in certain channels in the US and announced a huge $50bn investment in the US for medicines manufacturing and R&D. This includes the massive new Virginia manufacturing site (which broke ground in October 2025) focused on the company’s weight-loss and metabolic portfolio.

AstraZeneca has harmonised its share structure and now has a direct listing on the New York Stock Exchange in place of its US ADRs. This will increase the liquidity of the shares and makes the stock much more attractive to US institutional funds. The company remains listed, headquartered, and tax resident in the UK.

Looking ahead to the full year, the company has reiterated its guidance: total revenue growth in the mid to high single-digits and Core EPS growth in the low double-digits, both at CER.

We believe the outlook for the pharmaceutical sector remains mixed despite the backdrop of an ageing population. Although the business provides some protection against macroeconomic uncertainty and R&D productivity is expected to increase with the help of AI, concerns over drug pricing are likely to remain a headwind, especially at a time when governments are looking for ways to reduce debt levels. However, with a pipeline of innovative products targeting unmet patient needs, that can justify higher pricing, AZ is well placed to generate above average revenue and earnings growth. This has been reflected in the strong long-term performance of the shares.

Source: Bloomberg

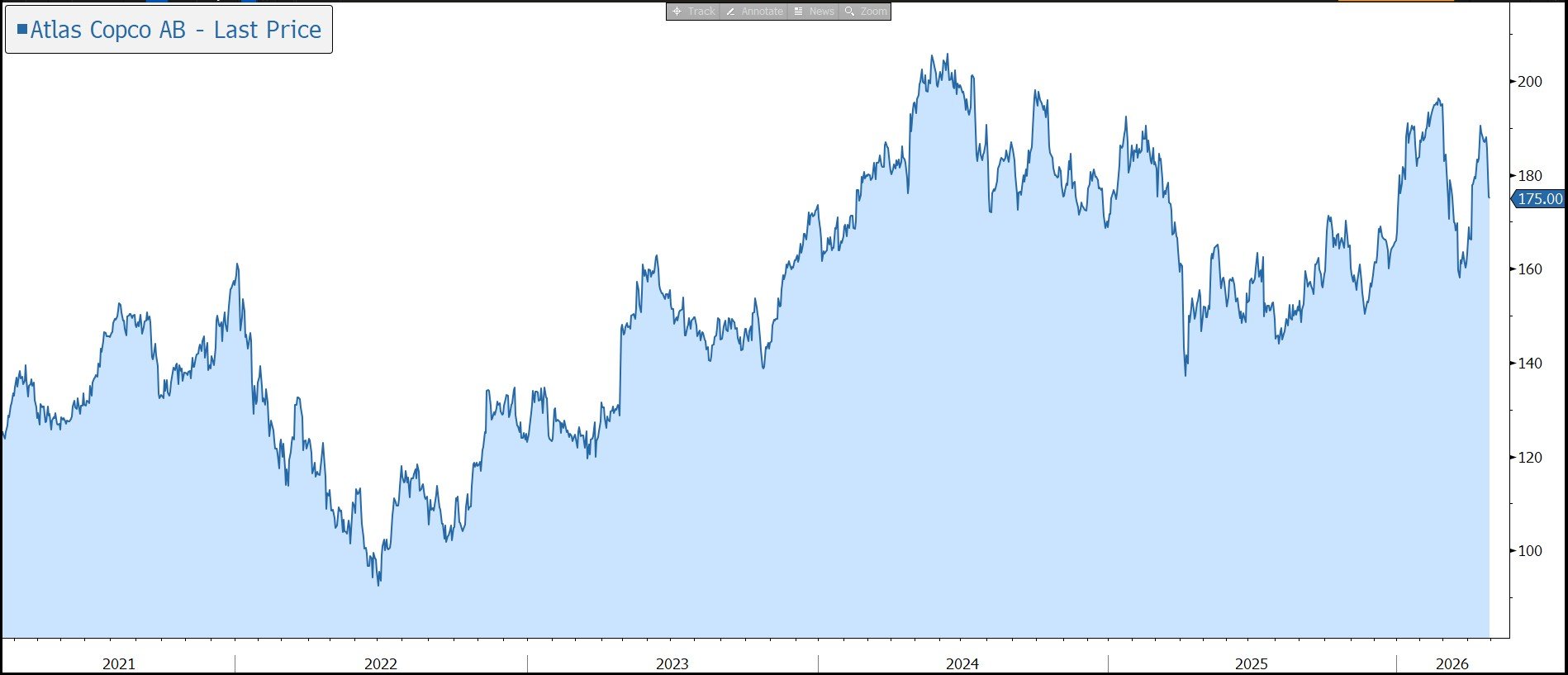

Yesterday lunchtime Atlas Copco released Q1 2026 results which were slightly below the market forecast. Stripping out a large negative currency headwind, organic revenue growth came in slightly below expectations, with strong growth in vacuum equipment, offset by a reduction in orders for gas and process compressors. Looking forward, in the near term the group expects customer activity to remain at the current level. In response, the shares, which are listed in Sweden, were marked down 5%. Note the stock is also trading ex-dividend SEK 2.50 (or 1.4%) today, the first instalment of the full-year payout. We remain positive on the long-term outlook for the company as it is a quality compounder exposed to attractive growth trends.

Atlas Copco is a world-leading manufacturer of innovative compressors, vacuum solutions, generators, pumps, power tools, and assembly systems. The group has a diverse customer base made up of general manufacturing (22%), process industry (20%), electronics/semis (16%), construction (12%), auto (10%), and other sectors (20%). The products help the customer increase operational performance, save energy costs, reduce contamination, cut down on failures in the field, lower noise levels, and extend service intervals. They are almost always critical to its customers’ operations.

As a result, the company provides exposure to a broad range of trends: demand for increased energy efficiency and reduced emissions; increased use of lightweight materials in transport industries; the transition from petrol to electric vehicles; increased use of demanding materials and production environments in processes for semiconductor and industrial production; increased production automation and smart factories; demand for improved ergonomics; and increased demand for digitally-supported service offers. Overall, the company will therefore play a role in the effort to reorganise and improve the resilience of supply chains, bring manufacturing closer to domestic markets, and increase automation in the face of higher labour costs or deteriorating demographics. Finally, over time the vacuum business should benefit from the expansion of the North American semiconductor manufacturing market.

The company is a giant in its niche – it is three times the size of its nearest competitor in Compressors and has a near-50% market share in semiconductor vacuum. The group is also the No.1 in most Industrial and Power equipment niches in which it operates.

The target is to increase revenue by 8% per annum, primarily through organic means, complemented by selective acquisitions of companies in or close to existing core competencies. Using a decentralised structure, the company lets these small bolt-on companies run autonomously while plugging them into its global service network.

The group operates an asset-light strategy – only components that are critical to the performance of the equipment are manufactured in-house. The company has integrated itself with its customers and can provide rapid and extensive support to their installed base of equipment. Almost 40% of revenue (and c. 60% of operating profit) is generated from service (i.e., spare parts, maintenance, repairs, consumables, accessories, and rental). This is more stable than equipment sales and provides a strong base for the business and greater resilience in difficult times. The cost of the group’s equipment is low relative to the customer’s overall operating costs, and as a result, the company has strong pricing power, helpful when trying to pass on raw material cost inflation or tariffs. Atlas Copco is based in Sweden and reports in Swedish Krona (SEK).

The Wallenberg Family (through its holding company, Investor) is the largest shareholder of Atlas Copco, having overseen its entire history, and has a member on the Board. The business is run for the long term in a way that ensures it is passed on to the next generation in better shape than it was inherited, with a focus on consistent operational culture, financial prudence, and sensible capital allocation.

During the first quarter of 2026, the overall demand for Atlas Copco’s equipment and services improved compared to the previous year. The increased order volumes were primarily driven by higher demand for vacuum equipment

Revenue fell 5% in the quarter to SEK 40.5bn, versus the market forecast of SEK 41.1bn. In organic terms, which excludes M&A (+3%) and currency (-11%), revenue was up 3%. This compares to a flat result in the previous quarter. Order intake was up 5% in organic terms in the quarter to SEK 45.4bn.

Atlas Copco operates through four divisions or ‘Techniques’, with the performance in the first quarter as follows:

· Compressor Technique (46% of 2025 sales) is the world leader in the provision of compressed air and gas solutions, such as industrial compressors, gas and process compressors and expanders, air and gas treatment equipment and air management systems. During the latest quarter, organic revenue rose by 1%, while orders fell 3%. Demand for industrial compressors remained essentially unchanged, while order volumes for gas and process compressors decreased notably due mainly to a tough year-on-year comparative.

· Vacuum Technique (22% of sales) provides vacuum products, exhaust management systems, valves and related products. Organic revenue rose by 8%, while orders jumped 32%. Orders for vacuum equipment increased significantly, driven by higher demand from the semiconductor industry, although orders for vacuum equipment to the general industry also increased markedly.

· Industrial Technique (16% of sales) provides industrial power tools, assembly tools, machine vision solutions, quality assurance products, and the associated software and service. Organic revenue was flat, while orders fell 2%. Demand for industrial assembly equipment and vision solutions to the automotive industry remained weak.

· Power Technique (17% of sales) provides a range of portable air and power, industrial and portable flow solutions. The business unit also provides specialty rental and service through a

global network. Organic revenue and orders both rose by 4%. Orders for power equipment increased, driven by higher demand for portable compressors and generators.

Regarding tariffs, the company has previously highlighted that it has 18 production facilities in the US. They are working on a mitigation strategy, with short-term actions focused on pricing and supply adjustments, and expect to be able to fully cover the impact of tariffs.

Atlas Copco generates attractive margins, with gross margin above 40%, providing some shelter against rising raw material costs, and operating margin above 20%. In Q1, adjusted operating profit fell by 6% to SEK 8.33bn, slightly below the SEK 8.46bn market forecast. The margin fell by 30 basis points in organic terms to 20.5%, predominately affected by a negative currency impact, and to a lesser extent, dilution from acquisitions, and costs related to trade tariffs. Volume, price, and mix affected the margin positively. EPS fell by 7% to SEK 1.28.

The return on capital employed during the previous 12 months slipped from 27% to 23% but is still well above the group’s 20% target and 8.0% cost of capital.

The company has a robust balance sheet and continues to generate strong operating cash flow (SEK 4.36bn in Q1), albeit lower than last year due to an increase in working capital. During the quarter, net debt decreased from SEK 20.7bn to SEK 15.9bn, while interest-bearing liabilities have an average maturity of 4.3 years. Financial gearing is a very comfortable 0.4x net debt to EBITDA.

The group continued to consolidate its industry with acquisitions, with 29 deals closed in 2025 and a further four in the first quarter of 2026.

The dividend policy is to pay out 50% of net income. For 2025, the group has approved an ordinary payout of SEK 3.00 per share, in line with the previous year, and an extra distribution of SEK 2.00 per share, resulting in a total combined dividend of SEK 5.00 per share to be paid in two equal installments and equivalent to a 2.8% yield. We believe this sends a strong signal of management confidence.

The group provided brief commentary on the near-term outlook, highlighting that it expects customer activity will remain at the current level.

Source: Bloomberg