Morning Note: Market News and Updates from BP and Assa Abloy.

Market News

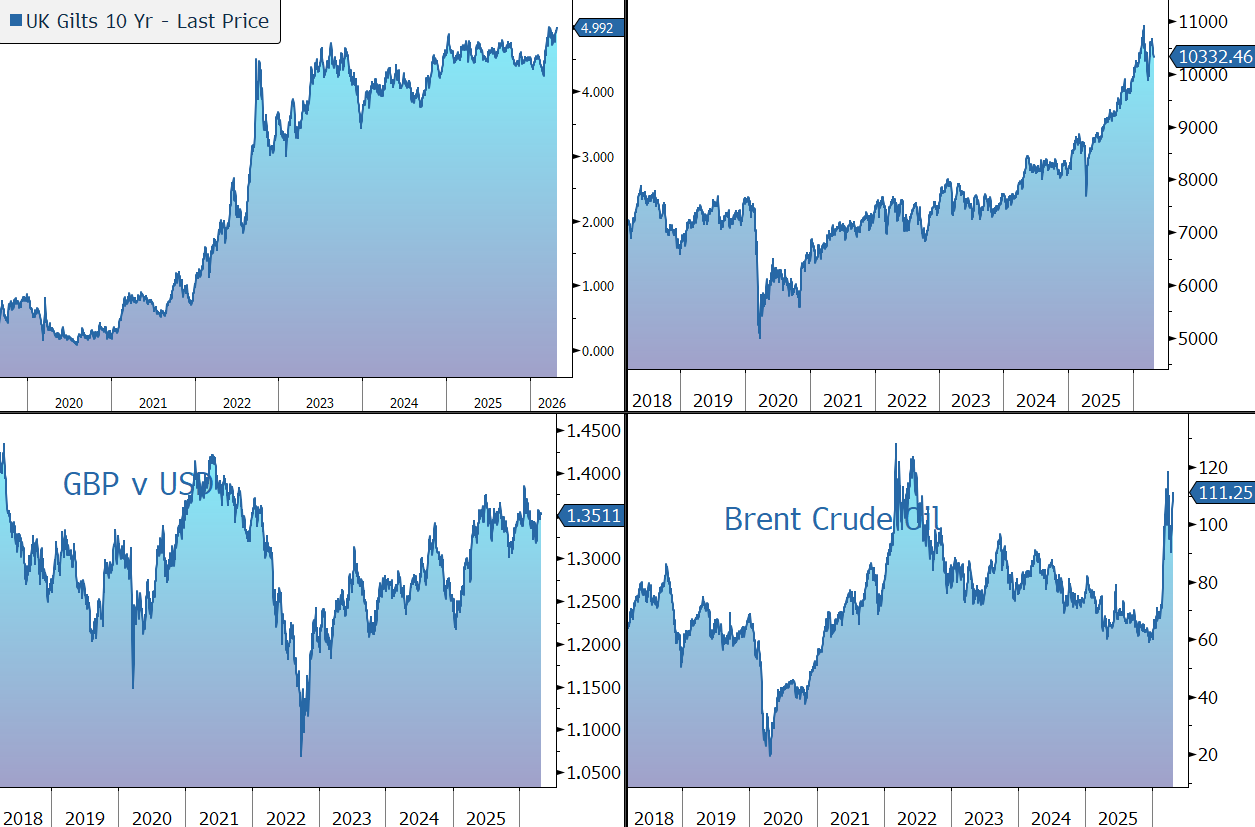

Brent crude futures have risen above $111 a barrel as markets assessed the likelihood of a lasting ceasefire and the potential reopening of the Strait of Hormuz after Iran submitted a fresh proposal to the US. Tehran reportedly signalled via Pakistan that hostilities could cease if Washington lifted its naval blockade, agreed to a revised framework governing transit through Hormuz, and provided assurances against future military action. The US has expressed scepticism toward the proposal and is expected to respond with counteroffers in the coming days, with Iran’s nuclear program continuing to be a key point of contention.

An LNG tanker appeared to exit the Strait of Hormuz, the first to do so since the start of the Mideast war.

BlackRock said higher government bond yields are ‘here to stay’ as the Iran war puts upward pressure on inflation. The yield on the US 10-year Treasury is currently 4.36%. The FT reports that Wall Street dealers’ Treasury holdings have jumped to the highest level since the global financial crisis as the Trump administration’s cut to regulation nudges banks back into the $31tn debt market. Gold has fallen back to $4,625 an ounce.

US equities ticked higher last night – S&P 500 (+0.1%); Nasdaq (+0.2%). In Asia, stock markets drifted lower: Nikkei 225 (-1.0%); Hang Seng (-1.0%); Shanghai Composite (-0.2%). The Bank of Japan voted 6-3 to keep its key rate at 0.75% while raising its inflation outlook significantly, with Bloomberg Economics now seeing a hike in June. The yen gained.

The FTSE 100 is currently little changed at 10,332, while Sterling trades at $1.3510 and €1.1550.

Source: Bloomberg

Company News

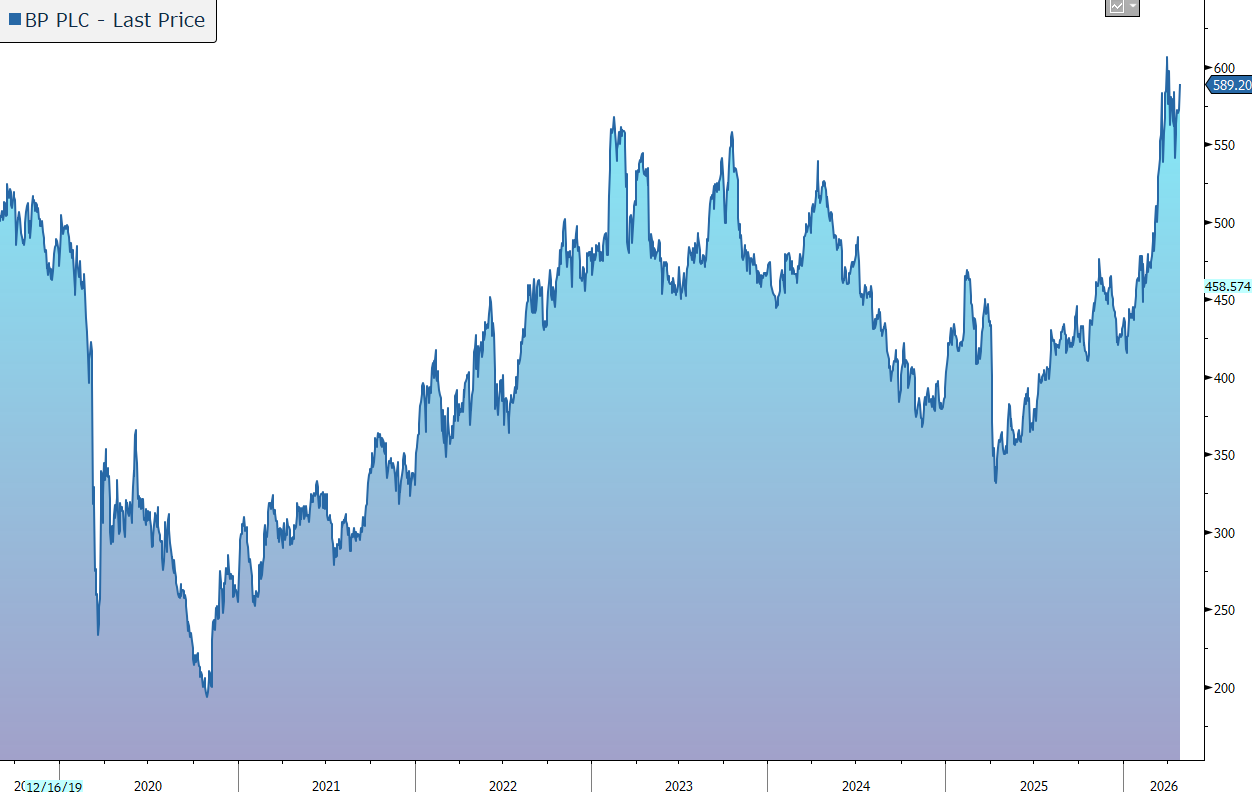

BP has today released Q1 results which were ahead of market expectations, driven by strong operational and financial delivery. The business continues to run well and the company made further progress towards its 2027 targets. The quarterly dividend was raised by 4% and, as expected, the share buyback programme remains on hold. The shares are up 3% in early trading, driven mainly by the strength in the oil price this morning.

BP is a global integrated energy company undertaking a strategic reset involving a reduction of capital expenditure, a reallocation of spend away from low carbon activities, and a significant cost reduction programme, all of which will drive improved cash flow and returns to support a stronger balance sheet and resilient distributions.

Following the appointment of Albert Manifold (ex CRH) as Chairman, the company is accelerating the delivery of its plans, including undertaking a thorough review of its portfolio to drive simplification and targeting further improvements in cost performance and efficiency. On 1 April, Meg O'Neill, the ex-CEO of Woodside Energy, became BP’s new CEO – the first outsider to lead the company in its century-plus history. She is expected to drive this transition further and has already disclosed the company will, in time, be reorganised into two main business units – one for upstream and one for downstream.

For now, in the Upstream business (i.e. exploration & production), the company is increasing investment to $10bn p.a. (split 70% oil; 30% gas) and targetting returns of more than 15%. The portfolio will be strengthened, with 10 new major projects expected to start up by the end of 2027, and a further 8-10 by 2030. Production is set to grow to 2.3m-2.5m barrels a day in 2030, albeit still below the 2019 level. The aim is to generate structural cost reductions of $1.5bn and an additional $2bn of operating cash flow by 2027. As a result, the cash flow from the group’s production barrels is expected to be significantly higher due to the ‘high-grading’ of the portfolio.

The Downstream division (i.e. refining & marketing) is being high-graded and will focus on ‘advantaged’ and integrated positions. The focus will be on operating performance with a target to consistently improve refining availability to 96%. Capital investment will be $3bn by 2027, with a target of $2bn in cost savings. Overall, the aim is to generate an additional $3.5bn–$4.0bn of operating cash flow in 2027 and returns of more than 15%. Following a strategic review, in December the company announced an agreement to sell a 65% shareholding in Castrol for an enterprise value of $10.1bn, with expected net proceeds of $6.0bn, which will be used to reduce net debt. BP will retain a 35% stake in a new joint venture, providing exposure to Castrol’s growth and future optionality.

Investment in the group’s ‘transition’ businesses is being slashed from $5bn p.a. to $1.5bn–$2bn p.a., with less than $0.8bn p.a. in low carbon energy. The focus will be on fewer but higher-returning opportunities and more efficient growth. There will be selective investment in biogas and biofuels. In renewables, the focus will be capital-light partnerships, while there will be limited further projects in hydrogen and Carbon Capture & Storage. The group is targeting an annual structural cost reduction of more than $0.5bn in low carbon energy by 2027.

Back to today’s results which have clearly been impacted by the conflict in the Middle East and the current market conditions. This resulted in heightened volatility in crude oil, natural gas, and refined products prices in the latter part of the first quarter. These market conditions have impacted financial results, including trading results and working capital movements.

During the quarter, underlying replacement cost profit – the key measure of the group’s performance – rose from $1.4bn to $3.2bn, well above the market forecast of $2.1bn. Compared with the previous quarter, profit doubled, reflecting an exceptional oil trading contribution and stronger midstream performance.

The commodity price backdrop was mixed: Brent crude averaged $81.13/barrel (compared to $63.73/barrel in the previous quarter); US gas Henry Hub averaged $5.05/mmBtu (vs. $3.55/mmBtu); and the refining margin averaged $16.9/barrel (vs. $15.2/barrel). The environment has remained volatile. As a rule of thumb, the company has disclosed that: a $1 movement in Brent has a $340m profit impact, a $0.1 movement in Henry Hub has a $40m profit impact, and a $1 movement in the refining margin has a $550m profit impact.

By division, the results for the quarter for underlying operating profit were: gas & low carbon energy (+34%); oil production & operations (-32%); and customers & products (up from $677m to $3.2bn).

Underlying upstream production was steady as increased production in the Gulf of Mexico and at bpx Energy, the US onshore business, offset ongoing disruption elsewhere. The company expects second quarter 2026 reported upstream production to be lower compared with the first quarter 2026, due to seasonal maintenance predominantly in the Gulf of Mexico and the effects of disruption in the Middle East. For the full year, the company now expects reported upstream production to be lower due to effects of disruption in the Middle East and underlying upstream production to be broadly flat.

Cost discipline and operational performance have been strong – in the first quarter, upstream plant reliability was 95.7% and refining availability was 96.3%. Overall unit production costs only rose by 1%.

With the sale of its Gelsenkirchen refinery, BP offloaded a complex downstream asset and its associated liabilities (like pension obligations). As a result, the company has raised its structural cost-reduction target by $1bn to $6.5bn-$7.5bn by 2027, versus a 2023 base of $22.6bn. At the end of 2025, $2.8bn had been achieved.

Capital expenditure was $3.3bn in Q1 and the company has reiterated its 2026 target of $13.0-$13.5bn, a level it believes supports progressively growing earnings per ordinary share in the long term.

Operating cash flow fell from $7.6bn in Q1 to $2.9bn, although this was after taking into account a $6.0bn adjusted working capital build largely driven by the rising price environment in addition to the seasonal inventory builds.

By 2027, the aim is to generate compound annual growth in adjusted free cash flow of more than 20% at $70/barrel oil price and returns on average capital employed of more than 16%. Note the oil price is currently $110 a barrel.

The group is targetting $20bn of divestments by 2027. In 2026, proceeds of $9bn-$10bn are expected including $6bn from the announced Castrol transaction, all significantly weighted to the second half. There are no plans for major acquisitions.

The company’s first capital allocation priority is a resilient dividend, which is expected to increase by at least 4% per ordinary share a year. Today, the group has declared a quarterly dividend of 8.32 US cents, 4% higher than last year, implying a full-year yield of 4.2%.

During the first quarter, net debt rose from $22.2bn to $25.3bn, with gearing of 24.7%, driven primarily by a significant working capital build. BP remains committed to maintaining a strong investment grade credit rating and a reduction in net debt to $14bn–$18bn by the end of 2027. We note, however, the net debt figure doesn’t include lease liabilities ($13.5bn), Gulf of Mexico oil spill payables ($6.1bn), and hybrids ($13.3bn). Today the company has announced that, subject to market conditions, it now plans to reduce corporate hybrid bond financing by around $4.3bn to $9bn by end 2027.

In a nod to these other obligations, the company is currently not buying back its shares and is fully allocating excess cash to accelerate strengthening of its balance sheet. We believe this is the right decision – it saves $3bn over the next year and will create a strong platform to invest with discipline into the group’s distinctive deep hopper of oil and gas opportunities.

We believe decarbonisation can’t happen at the flick of a switch – oil and gas will remain part of the global energy mix for decades, with demand driven by population growth and higher incomes, particularly in developing countries where the desire for energy intensive goods and services like cars, international travel, and air conditioning is rising. We also believe the production of the materials needed to transition to net zero can’t happen without hydrocarbons. At the same time, reduced investment in new production, partly because of environmental concerns, and natural decline rates, are increasingly leading to constrained supply.

Against this backdrop, investor disillusion with BP’s tilt towards low carbon energy, particularly in terms of capital discipline and returns (as evidenced by ongoing impairments), has had a negative impact on the share price over the medium term relative to the peer group. However, the recent arrival of a new CEO, combined with operational high-grading, reduced financial gearing, and ongoing M&A speculation suggests that the ‘valuation gap’ between BP and its peers could narrow further.

Source: Bloomberg

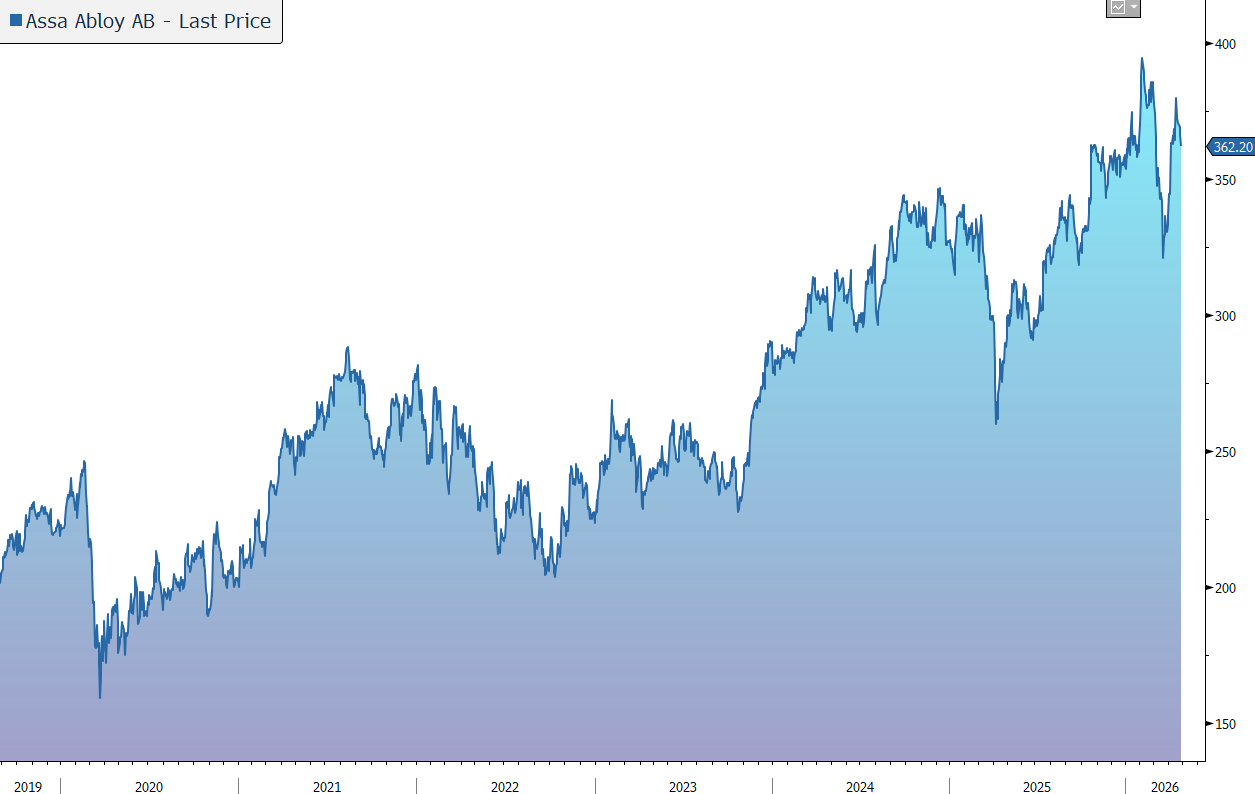

Assa Abloy has today announced its Q1 2026 results which highlighted the benefit of a decentralised operating model. Although sales were a touch below market expectations, profitability was in line. Margins expanded due to strong operating leverage, while cash flow was very strong. The shares are little changed in early trading.

Assa Abloy is the global leader in access solutions to physical and digital places, with a portfolio of well-known global and local brands, such as Yale, Union, HID, and Lockwood. Products include doors, sensors, locks, alarms, fencing, gates, and identity systems. Products are either offered on a standalone basis or combined to form a complete, full-service access offering.

The key long-term drivers of the $100bn industry are:

· increased demand for safety and security

· movement of people and demographic change

· increased wealth in emerging markets

· the shift to digital and electronic technologies which have grown at 4-5x the rate of mechanical products over the last 10 years

· the development of sustainable buildings to meet climate change objectives

· the shift towards touchless (hygienic) activation points, automated doors, and location services

· constantly changing local market regulations which make it difficult for smaller operators to compete.

As the brand leader in most markets, with a large installed base, robust pricing power, and strong distribution channels, we believe Assa Abloy is well placed to take advantage of these trends. The strategy is to actively upgrade the installed base, generate more recurring revenue, increase service penetration, and expand exposure to emerging markets. The group’s broad offering is also well suited to address the fast-growing data centre market.

Assa Abloy has a strong track record of innovation and aims to generate a quarter of sales from products launched in the last three years.

The company has a decentralised operating model and a strong track record of cost control. The latest Manufacturing Footprint Programme (MFP), the group’s tenth, was launched last year, and is proceeding according to plan. It is expected to generate annual savings of about SEK 1bn (c.60 basis points of margin) from 10 factory closures and 1,300 headcount reductions. On the call, the company hinted at the initiation of MFP 11.

Overall, the long-term financial target is to generate annual sales growth of 10%, half organically and half from acquisitions. An operating margin of 16%-17% is the target over the business cycle, although the aim is to be towards the upper end of the range in the coming years. Management have previously said it needs to generate organic top-line growth of 3% to offset inflation and drive the margin forward. The group is on track to exceed its target to generate SEK 25bn of profit from SEK 150bn of sales in 2026, while the 2030 target is SEK 41bn of profit from SEK 250bn of sales.

Assa Abloy is a textbook example of late cycle business – locks are one of the last things in a building and are changed when you’ve moved. The current macroeconomic environment is mixed, especially in the residential market that accounts for a third of sales. However, strong exposure to the aftermarket and operational agility continue to be a great advantage.

During the three months to 31 March 2026, increased global geopolitical tensions and macroeconomic uncertainty have impacted many customer segments and geographies. In this environment, the company has once again shown resilience and strong execution.

Net sales fell by 6% to SEK 35.8bn, slightly below the market forecast of SEK 36.3bn. In organic terms, which strips out the impact of acquisitions & disposals (+2%) and a significant currency headwind (-10%), sales rose by 2%. Growth was made up of flat volume and 2% price growth.

The group continues to actively upgrade the installed base by shifting customers from mechanical to electromechanical and digital solutions. Organic sales grew 6% in the quarter, with growth driven by demographic changes, with a digital native younger generation and an aging generation in need of care, are accelerating the need for more convenient, reliable, and efficient electromechanical and digital solutions.

The company is organised into three regional units and two global divisions.

· Global Technologies (a separate global division) reported organic sales growth of 4% in the quarter with strong sales growth in Global Solutions and good growth in HID.

· Entrance Systems (a separate global division) achieved stable organic development with the Perimeter Security and Pedestrian segments delivering strong growth, while the Industrial and Doors & Automation segments declined.

· In the geographical divisions, Americas reported strong organic sales growth of 4%, driven by continued strong growth in the North America Non-Residential segment and in Latin America. Sales declined in the North America Residential segment, impacted by continued elevated interest rates, a challenging housing market and short-term effects from snowstorms.

· The EMEIA region delivered organic sales growth of 3%, driven by strong growth in Central Europe, the Nordics, and the MEIA region as the impact from the war was limited to the second half of March. However, the UK/Ireland as well as South Europe experienced declines.

· Asia Pacific was stable, with sales declining in the Greater China & Southeast Asia business unit, offset by good growth in the Pacific & Northeast Asia business unit.

Operating income fell by 3% to SEK 5.46bn, in line with the market forecast. The operating margin rose from 14.9% to 15.3%. Performance was negatively impacted by currency effects and acquisition-related dilution of 40 basis points in total, however this was more than offset by strong operating leverage of 52%. EPS slipped from SEK 3.20 to SEK 3.18.

Operating cash flow rose by 30% to SEK 3,141m, while cash conversion was 66%. The group’s financial position remains robust, with net debt to EBITDA 2.1x. Looking forward, gearing is expected to fall rapidly thanks to strong free cash flow generation.

There was no dividend announcement today. For 2025, the company declared a payout of SEK 6.40, up 8.5%, equating to a yield of 1.7%.

M&A will continue to be a core driver of growth, with over 900 potential acquisition targets identified globally. The focus is on acquiring new customers in the core business, extending the core offering, access new technologies to deepen the group’s competitive position, and increased service capacity.

However, there is some concern that recent M&A has been skewed towards lower value-added segments (e.g. DIY, window and door hardware components, fencing products, gates, padlocks, cylinders, etc). Although these acquisitions fit the purpose of growing earnings at lower multiples than the group average, they also dilute the group’s exposure to the fast-growing and structurally more attractive electromechanical and mobile segments, potentially posing a risk to the long-term valuation multiple.

The 2023 purchase of HHI for $4.3bn filled a strategic gap in the group’s US residential business. Although that market remains subdued, the business is performing well. Cost synergies have been achieved, though sales synergies have yet to be fully realised. The group still expects HHI to be a 16% margin business (vs. <10% at present) as volumes recover. A strategic review of the non-core HHI plumbing business is being undertaken, potentially fetching $1bn. Elsewhere, M&A activity remained buoyant with 23 deals in 2025 and three in the first quarter of 2026. The pipeline remains strong, and the group still plans to make its usual 15-20 acquisitions per year.

Assa Abloy doesn’t usually provide guidance but highlights that it remains confident in the company’s ability to navigate varying market conditions. On the call, the company appeared confident it can pass through any raw material cost increases through higher pricing. A continued focus on innovation, operational excellence, cost discipline, margin expansion, and strategic acquisitions, combined with a strong financial position, provides a solid foundation for continued profitable long-term growth and value creation.

The risk to this optimism is driven by a combination of rising interest rates, labour shortages, and tariffs. Management is dedicated to mitigating any impact from potentially negative changes in demand, through local agility and focus on cost-control. Assa has previously said that during both the global financial crisis in 2008/09 and the Covid-19 pandemic, its decentralised operational model and agile cost base provided flexibility. In addition, the group’s large exposure to after-market service and its structural pricing power leaves the business better positioned to navigate through uncertain times.

Structural tailwinds from the transition to electromechanical locks, increasing recurring and service revenue, data centre growth (collectively 60% of the business) and pricing should drive 5% organic growth.

Source: Bloomberg