Morning Note: Market News and Updates from Alphabet, Unilever, and Glencore.

Market News

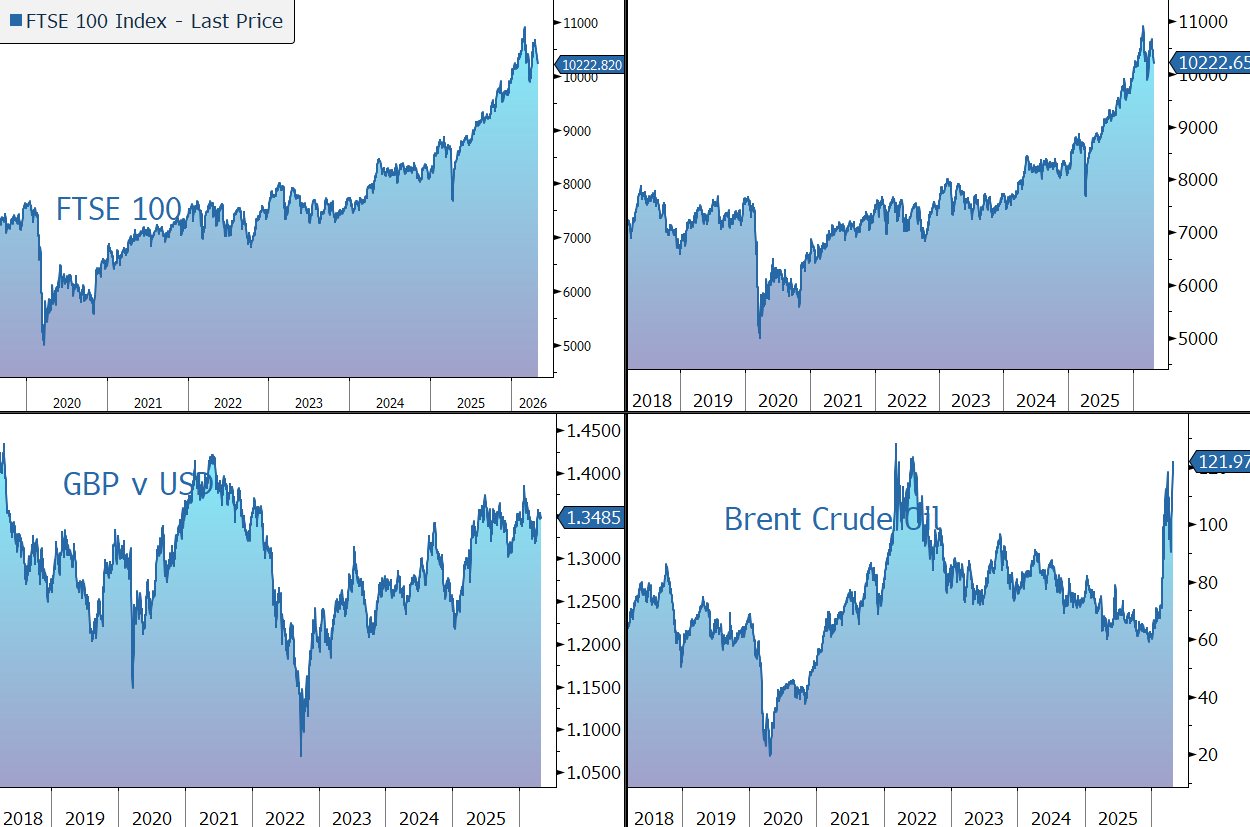

Brent hit a wartime high above $125 a barrel (before falling back to $112) after Axios reported that Donald Trump will be briefed today about new military options in Iran. Trump earlier told the news outlet that he would not lift his naval blockade without a nuclear deal. Meanwhile, US inventory data showed steep declines in crude and fuel stockpiles, while exports surged to record levels above 6m barrels per day, signaling tightening global supply conditions amid ongoing geopolitical disruption.

The Fed was deeply divided at Jerome Powell’s last meeting as chair, with some dissenting over its easing bias — indicating members may resist immediate rate cuts as Kevin Warsh moves closer to heading the central bank. Yields on front-end notes climbed after the policy decision. The yield on the US 10-year is 4.41%. The ECB and BOE are up next, with both set to hold rates today as policymakers assess the impact of the Iran war. Gold trades at $4,625 an ounce.

US equities were little changed last night – S&P 500 (-0.04%); Nasdaq (+0.04%). Google parent Alphabet soared 6% in extended trade after smashing forecasts (see below). Microsoft and Amazon.com delivered as well, but Meta Platforms disappointed on concerns over its AI spending. Apple will report after the close.

In Asia, equities drifted lower: Nikkei 225 (-1.1%); Hang Seng (-1.3%). The yen touched its weakest level since July 2024. China’s April manufacturing PMI came in at a slightly better-than-expected 50.3.

The FTSE 100 is currently little changed at 10,222, while Sterling trades at $1.3495 and €1.1540. Whitbread is down 6% after announcing a restaurant transition plan.

Source: Bloomberg

Company News

Last night, Alphabet released Q1 results which were well above market expectations, driven by strong growth in Search and Cloud as the company continues to benefit from its full stack approach to AI. Although capital investment continued to expand substantially, and is expected to do so again next year, the order backlog jumped to $462bn of which more than 50% will convert to revenue over the next 24 months. In after-hours trading, the shares jumped by 6%.

Alphabet is the public holding company for Google, one of the world’s most recognised and widely used brands. In addition to the core search engine, the group owns digital video platform YouTube, Google Cloud, web browser Chrome, mobile operating system Android, Gmail, Google Maps, AI personal assistant Gemini, Fitbit, autonomous driving company Waymo, and drone delivery company Wing.

The group has a strong track record of innovation, leaving it well placed to capitalise on multiple technological themes, such as digital media, e-commerce, video advertising, the cloud, the internet of things, driverless cars, and AI.

The company has seven products with more than two billion users each and another eight with more than 500m users, most of which we believe are far from being fully monetised. The group’s structure allows it to own a portfolio of businesses with different time horizons, while its broad offering provides customer stickiness and a competitive edge. Capital allocation is spread across capital expenditure, internal R&D, bolt-on M&A, and massive shareholder returns.

We believe Alphabet is very well placed for the world of AI – the company has been incorporating AI functionality into its search capabilities and other products for years. As a result of its vertically integrated ecosystem and immense financial strength, the company now holds several competitive advantages in the AI race.

· Google develops its large language models (LLMs) on its own semiconductors (Trillium) which are far more cost effective than comparable Nvidia models, providing it with a substantial cost advantage versus other AI players. The TPU v6 offers 4.7xbetter performance-per-dollar on LLM inference than Nvidia H100s. Overall, the company reduced Gemini’s serving costs by 78% in 2025.

· Google’s position in cloud services – it is one of the big three public providers, generating more than $60bn in annual revenue – leaves it well placed to provide the infrastructure and computing power needed for AI.

· Google owns the world’s largest and most robust personalised data and user histories from its scaled applications: YouTube, Maps, Gmail, Chrome, and traditional Search.

Gemini 3 is the latest iteration of its family of AI LLMs. It is designed to be highly multimodal, built from the ground up to understand and operate across different types of information simultaneously, including text, code, audio, images, and video. External testing indicates Gemini 3 is the best publicly available model in terms of raw intelligence. It has been rolled out across Google’s distribution channels including AI Mode in Search and the Gemini App. In January, Apple and Google announced Gemini will power the next generation of Siri and Apple Foundation Models on iPhones in a deal estimated to be worth $1bn annually to Google as a licensing fee. Although Gemini (with over 750m MAUs) still trails ChatGPT (with 800m MAUs), it is catching up and increased engagement is expected as Google’s pace of innovation continues.

Overall, following a period of investor concern regarding the threat to the company’s competitive position, we believe Google has the infrastructure and application vehicles to fully monetise AI. This is supported by data on AI Mode and AI Overviews which shows overall query growth, including increased user engagement and greater query depth, supporting both monetisation and advertiser return on investment. The main concern is the huge ramp-up in the level of capital investment to support AI growth (see below).

Political and regulatory headwinds will always exist. However, the remedies issued last year in the Google search monopoly case were much less onerous than feared and removed a significant regulatory overhang. The break-up of the company was avoided (in particular, a forced sale of Chrome), the Apple distribution deal was largely untouched (although it must be re-bid annually), and the scope of data sharing was reduced (although it must share ‘click-and-query’ data). The US District Court Judge considered the potential impact on consumers and the rise of AI-driven rivals in reaching a decision.

Back to last night’s results. In the three months to 31 March 2026, revenue grew by 19% on a constant currency basis to $110bn, above the consensus forecast of $107bn, reflecting an acceleration of growth in both Google Search and Google Cloud. This compares to the 17% growth rate in the previous quarter.

The group reports its results across three segments: Google Services, Google Cloud, and Other Bets. Google Services is the largest division (81% of revenue), generating revenue primarily from digital advertising and the sale of apps, digital content products, hardware, and YouTube subscription fees. During Q1, Google Services revenue grew by 16% to $89.6bn, reflecting strong growth across all product areas.

Google Search (which accounts for 78% of ad revenue) increased by 19%, versus 17% last quarter. Advertising from Google Network Members’ websites (9% of ad revenue) fell by 4%. The group separates out YouTube, which accounted for 13% of ad revenue in the quarter and grew by 11%. According to ratings firm Nielsen, YouTube accounts for more than an eighth of all television usage in the US and there are currently more than 200bn daily views on YouTube Shorts.

Other sales within the Services division (known as Google Subscriptions, Platforms, and Devices) include Play, content products, hardware, service, licensing fees, Nest, and YouTube’s non-advertising revenue (which now accounts for a third of YT revenue). Google surpassed 350m paid subscriptions in Q1, led by growth in Google One & YouTube Premium. Revenue grew by 19% in Q1 to $12.4bn.

Traffic acquisition costs (TAC) are the fees Google pays to other companies (such as Apple) to carry its search service and adverts (i.e., cost of sales). During Q1 they grew by 11% and currently account for 19.7% of advertising revenue.

Google Cloud includes Google’s infrastructure and data analytics platforms, collaboration tools, and other services for enterprise customers. In Q1, the division grew by a stellar 63% to $20bn, versus the market forecast (50%) and the previous quarter (48%). Performance was led by growth in Google Cloud Platform (GCP) across core products, enterprise AI Infrastructure, and enterprise AI Solutions. Gemini Enterprise paid MAUs (monthly average users) rise 40% quarter on quarter. The supply-demand balance remains tight – the backlog is up to $462bn – and the group continues to invest to grow the business. Despite this, Cloud quarterly profit grew from $2.2bn to $6.6bn, with a margin of 33%.

The group’s Other Bets division (less than 1% of revenue), which is effectively an incubator fund for new products and technologies, made a quarterly loss of $2.1bn. The group continues to wind down non-priority projects and focus investment on viable businesses like Waymo, the autonomous driving technology company, which has a potentially huge total addressable market – during the quarter, Waymo raised $16bn at a $126bn valuation.

Alphabet continues to ‘durably engineer’ its cost base to support its investment in long-term growth opportunities, most importantly AI. The number of employees rose by only 5% in Q1 to 195k, while actions are being taken to optimise global office space and use AI to increase business productivity and efficiency. The group has previously highlighted that 25% of new code is being written by AI. The company reiterated its warning that the ramp up in capital investment (see below) is now feeding through to higher depreciation, which rose by 44% in Q1.

In the latest quarter, operational gearing and continued efforts to improve efficiency drove a gain in the margin from 33.9% to 36.1%. EPS grew by 82% in the quarter to $5.11, versus the consensus forecast of $2.63, albeit helped by a gain on equity securities of $36.9bn.

As expected, capital expenditure rose sharply as the company continued to pour money into infrastructure for AI products – up 107% to $35.7bn in the quarter. The company nudged up its 2026 capex guidance from $175bn-$185bn to $180bn-$190bn due to the impact of the Intersect acquisition. On the call, management also warned of another significant step-up in 2027, without quantifying the exact amount. The company has justified the spend by the existing monetisation of previous investment across the business and the huge order backlog which has now hit $462bn, of which more than 50% will convert to revenue over the next 24 months. The company has previously said that 95% of the top 20 SaaS companies now use Gemini, and the models are processing over 10bn tokens per minute. The company also said that 40% of the spend is in longer duration assets like physical land and power infrastructure.

Although the increase in spend comes from a position of financial strength (see below), it equates to 1.2x consensus 2026 profit. The concern is the shift toward a more capital-intensive, asset-heavy model and the potential risk of technological obsolescence and return on investment. However, for now demand continues to exceed supply, justifying the continued ramp-up in investment. We also note the group has a strong track record for generating return on investment – together, Cloud and YouTube exited 2025 at an annual revenue run rate of $130bn.

Free cash flow generation fell from $18.9bn to $10.1bn in the quarter, driven by the increase in capex, while the group’s large cash pile (including marketable securities and long-term debt) stands at $49bn. In February, the company raised $32bn in a heavily oversubscribed debt issue, including a 100-year Century Bond in Sterling. The company pays quarterly cash dividends (+5% to 22c), putting the company on an equal footing with Microsoft and Apple in the minds of investors looking for yield.

The shares continue to trade on a reasonable valuation relative to most of the other tech majors and at a level we believe is very attractive for a company exposed to several areas of long-term secular growth.

Source: Bloomberg

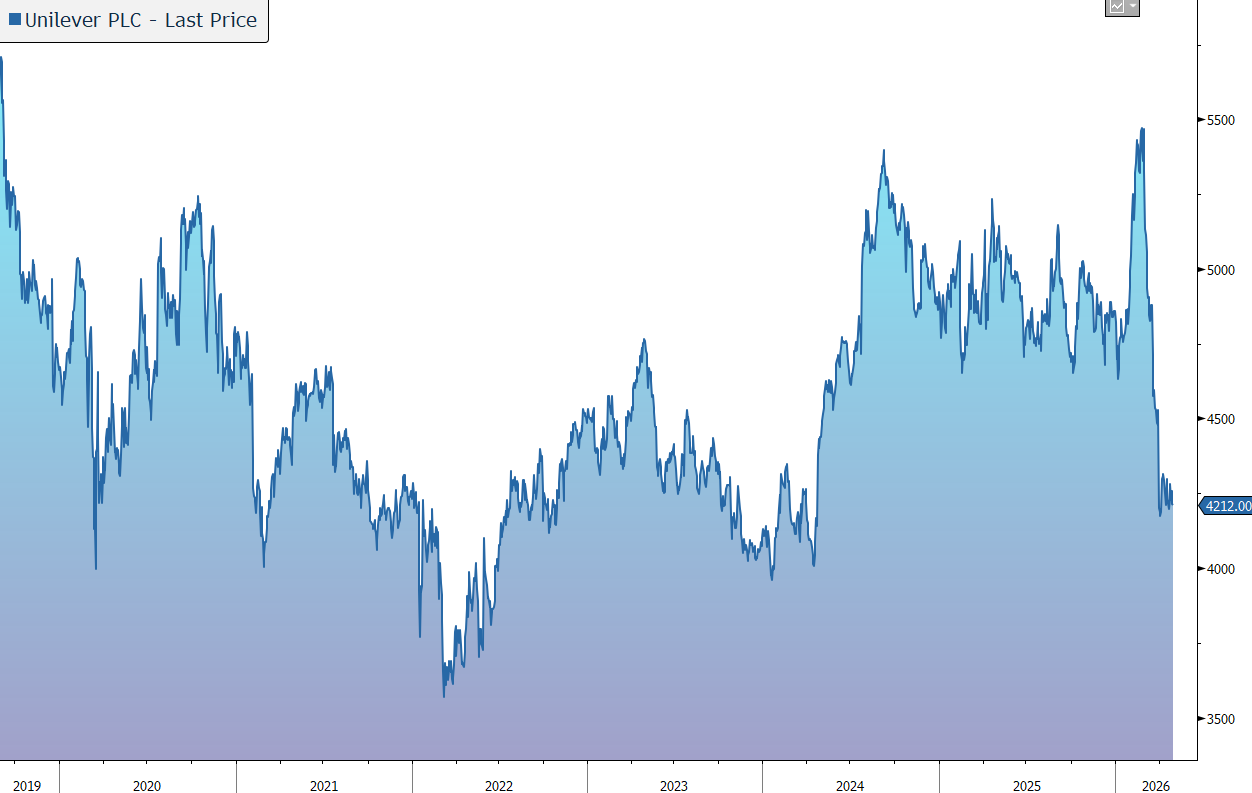

Unilever has today released Q1 results which were slightly better than market expectations and confirmed its full-year outlook. Importantly, growth was driven by volume, particularly in emerging markets. In response, the shares are little changed in early trading.

Unilever is one of the world’s leading suppliers of consumer goods, with annual sales of more than €50bn. Its products are low-ticket, repeatable purchases, with 3.4bn people using a Unilever brand every day. With unique routes to market, the company has an unrivalled emerging market presence and generates 60% of its sales from those parts of the world expected to experience strong long-term growth in demand. In particular, the group’s 62% holding in India-listed Hindustan Unilever Limited provides exposure to the largest consumer goods company in India.

Following last year’s demerger of its Ice Cream unit Magnum, in which it has retained a 19.9% stake, Unilever recently announced the combination of its Foods division with US flavours company McCormick. The new company will house leading, iconic brands including McCormick, Knorr and Hellmann’s, and high growth potential brands including Cholula, Maille, and Frank’s, as part of a global portfolio with revenue of $20bn. The combined group is expected to realise $600m of annual run rate cost synergies net of growth reinvestments, and incremental cost and revenue synergies of $100m that will be reinvested to further drive growth. Work is already underway to support the delivery of these synergies. Unilever expects no revenue or operational dis-synergies from the separation of Foods given the operational and go to market independence of Foods relative to the other Business Groups. Unilever expects €400m-€500m of stranded costs post the separation, which will be offset with savings over 2027 to 2029, incurring one-off restructuring costs of €500m over that period. Overall, although the valuation of the deal was reasonable, the structure has been poorly received, particularly the fact that Unilever shareholders will own a direct stake in US-listed company. The deal isn’t expected to close until mid-2027 and is subject to McCormick shareholder approval and the receipt of required regulatory and other approvals.

Following the separation of its Foods division, Unilever will become a leading pure-play Health and Personal Care (HPC) business spanning Beauty, Wellbeing, Personal Care, and Home Care. Resources will be focused towards categories with strong structural growth and the highest returns. 25 Power Brands will account for 78% of revenue. The pro-forma portfolio generated revenue of €39bn in 2025 and delivered a compound annual growth rate of 5.4% underlying sales growth in the last three years, alongside a gross margin of 48% and an underlying operating margin of 19%.

The main focus will be to generate more sales in the US, India, the beauty sector, premium markets, and the e-commerce channel. The remaining 100+ smaller markets will be run on a ‘One Unilever’ basis to benefit from scale and simplicity, further enhancing the group’s focus.

Overall, over the medium term, Unilever is still aiming to deliver mid-single digit underlying sales growth, underpinned by at least 2% underlying volume growth and continued modest improvement in operating margin fuelled by gross margin expansion.

Back to today’s results. Against a backdrop of heightened macroeconomic uncertainty, the company has made a good start to the year. In the first quarter, turnover fell by 3.3% to €12.6bn, slightly better than the market forecast of €12.4bn.

Underlying sales growth (USG) – adjusted for the impact of currency headwinds (-7.7%) and M&A (+0.9%) – was 3.8%. As expected, this was slightly below the full-year run-rate due to phasing issues and the expected uplift in Q2 performance due to marketing spend for the World Cup. On an encouraging note, growth was driven by volume which rose 2.9%, with underlying price growth adding 0.9%. The strong volume growth was led by Power Brands, which grew underlying sales by 5.0%, with 4.0% volume growth.

In emerging markets, USG was 5.7%, spurred on by digital initiatives and a shift in focus towards more premium products. Growth was broad based, and included 7% growth in India, sequential improvement and a return to volume growth in Latin America and continued good progress in China and Indonesia. Developed markets grew by 1.0%, reflected growth in North America, led by Personal Care and Beauty, offset by a subdued European market.

All Business Groups delivered volume growth:

· Beauty & Wellbeing (+3.6% USG to €3.3bn) – led by continued strength in Dove and Vaseline, good momentum in our prestige brands, and a return to volume growth in Sunsilk. Wellbeing declined low-single digit against a very strong comparator versus last year.

· Personal Care (+3.7% to €3.1bn) - driven by mid-single digit growth in deodorants and skin cleansing. Dove's continued strong performance in both categories was supported by premium innovation.

· Home Care (+6.1% to €3.2bn) - reflecting improving momentum and competitiveness across key markets, including strong volume-led growth in India and Brazil, partly offset by weaker markets in Europe.

· Foods (+2.2% to €3.0bn) - led by continued strength in Hellmann’s and sequential improvement in Unilever Food Solutions.

The group’s productivity programme, launched in 2024, continues to run ahead of schedule in its delivery of €800m of savings by the end of 2026. Unilever delivered €750m of savings by the end of the first quarter.

As this was only a sales update, other than the commentary on the productivity programme there is no detail in the statement on profitability or the group’s financial position.

As a reminder, in 2025 the group generated a gross margin of 46.9%, reflecting continued efforts to drive structural gross margin improvements and benefitted from higher-than-expected net productivity and procurement savings. The underlying operating margin of 20.0%. Net debt ended the year at €23.1bn, 2.0x EBITDA and in line with guidance of around 2x.

The company’s capital allocation framework is prioritising disciplined investment behind organic growth and productivity and allocating €1.5bn a year to bolt-on acquisitions. Capital returns will include a dividend payout ratio of approximately 60%, alongside €6bn of share buy‑backs expected to run between 2026 and 2029. The latest quarterly dividend has been increased by 3% to €0.4664, although in Sterling terms it is up 4% at 40.46p. A €1.5bn share buyback commences today and is expected to complete on or before 6 July.

Looking to the full-year, the company still expects underlying sales growth to be within its multi-year guidance range of 4% to 6%, albeit at the bottom end of the range. Underlying volume growth is expected to be at least 2%. The company also anticipates a modest improvement in underlying operating margin for the full year versus 20.0% in 2025 as the remaining €130m of the target €800m productivity savings are delivered.

Source: Bloomberg

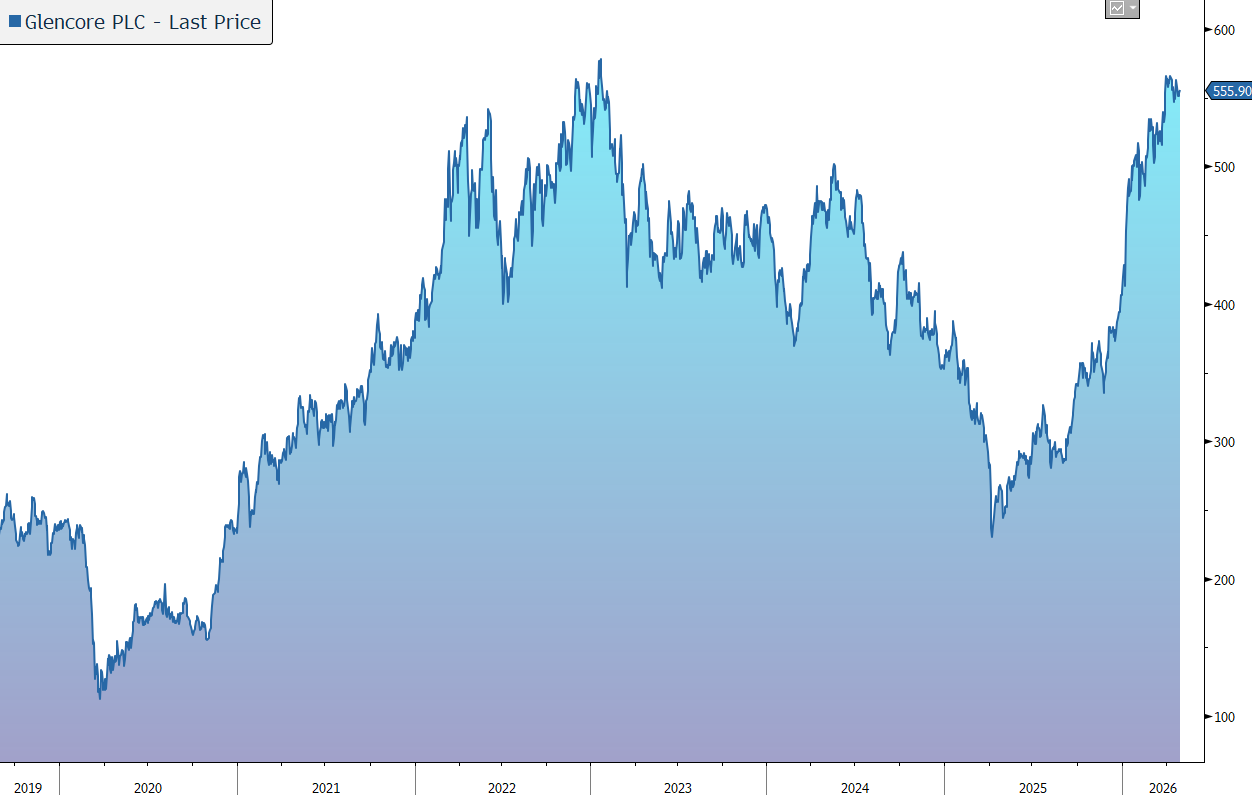

Glencore has this morning released its Q1 2026 production report. Overall production is largely in line with expectations and full-year guidance is unchanged. The company anticipates that current stronger commodity prices will more than offset increased input costs from Middle East conflict disruptions, potentially leading to margin expansion and the marketing segment’s profit exceeding the top end of its annual guidance. The shares have been very strong over the last year, driven by the (now withdrawn) bid from Rio Tinto and the ongoing strength in commodity prices. As a standalone company, we believe Glencore is well placed, with a strong position in copper, a cash generative coal unit, and unique marketing business. In response to today’s update, the shares are up 1% in early trading.

Glencore is a vertically integrated commodities business, with a strong position in the production of copper, coal, nickel, zinc, cobalt, and precious metals, and a unique marketing business which markets and distributes commodities sourced from internal production and third-party producers to industrial consumers. The group’s strategy is to own large-scale, long-life, low-cost Tier 1 assets.

Following a period of portfolio simplification, the company has sold or shut 35 assets since 2021. In the meantime, it has undertaken selective M&A in key/core commodities, including copper/alumina/bauxite and high-quality steelmaking coal. As part of this process, Glencore has uncovered opportunities to streamline its operating structure and identified at least $1bn of cost savings (against a 2024 baseline). These are expected to be fully delivered by the end of 2026, with more than half generated in 2025.

Glencore is a leading producer of critical minerals that are used in low-carbon and carbon-neutral technologies, such as electric vehicles and renewable energy, the outlook for which is underpinned by robust demand and persistent long-term supply challenges. Most notably, this includes copper. Last December, the company set out plans to expand its copper production from 0.85mt in 2025 to 1mt by 2028 and 1.6mt by 2035, making it one of the largest producers in the world. Growth will be driven by new mines, the expansion of existing mines, and the restart of dormant mines. Glencore’s position in Copper was one of the main motivations for the interest from Rio Tinto earlier in the year.

Given the company’s somewhat patchy production record in recent years, investors will be looking for signs of improved operational performance. It is therefore helpful that the copper expansion plans are derisked to some extent as the production targets are not dependent on one mine or process and are often a bolt-on to existing infrastructure. The major greenfield project is El Pachón in Argentina, one of the world’s largest undeveloped resources which the company hopes will underpin its long-term growth.

Earlier in the year, the company announced the sale of a 40% stake in their Congolese copper and cobalt assets (Mutanda and KCC) to a US-backed consortium (Orion CMC) at an implied enterprise value of $9bn. Through this partnership, Glencore will be able to support the ambitions of the US government and private sector with the supply of two critical minerals, while derisking the political volatility associated with its African operations. The cash injection – estimated at over $3bn for Glencore’s interest – also provides headroom for organic growth investment and shareholder returns. The company has also finalised the KCC land access package with Gécamines, unlocking life of mine extension, productivity and cost improvements, and a pathway to c.300kt pa of copper production.

Glencore is also the world’s leading seaborne energy (thermal) coal business, a top-tier steelmaking (coking) coal producer, and has a rapidly growing LNG, power, gas, and carbon business. As a result, the company will play a strategic role in supporting the world’s energy needs of today and tomorrow. The company believes global population growth, increased urbanisation, a growing middle class, AI infrastructure growth, and the energy transition will all continue to drive long-term demand for thermal coal. For now, however, the company is balancing immediate energy security needs with a commitment to a net-zero trajectory by undertaking the responsible decline of its thermal coal operations.

Glencore’s 77% interest in Teck’s steelmaking coal business (EVR) complements existing production in Australia, Colombia, and South Africa. Following consultation with its shareholders, Glencore is retaining its coal and carbon steel materials business. The company believes the cash generative capacity of the business significantly enhances the quality of the overall portfolio, by commodity and geography, and broadens the company’s ability to fund the growth of its copper portfolio as well as accelerate shareholder returns. Management sees potential upside through synergies as the EVR assets are integrated into the portfolio.

Now to today’s production update which comes against the backdrop of volatile commodity prices and geopolitical tension. While the Middle East conflict has created numerous dislocations, particularly around the supply of crude, refined products and sulphuric acid, Glencore’s energy marketing business has supported the supply of fuels to its assets. Although the impact of the conflict on the group’s industrial business was limited in Q1, recent and emerging impacts are now manifesting, primarily as an increase in input costs, most notably diesel and acid consumption, and the generally weaker US dollar.

In Q1 2026, overall production was largely in line with management expectations, accounting for operational conditions and the Lady Loretta (zinc) and Mount Isa copper mines in Australia reaching their planned economic end of lives during 2025. Accordingly, full-year 2026 production guidance remains unchanged from that presented at the Capital Markets Day in December 2025.

- Copper: own-sourced production rose 19% to 199.6kt. This was primarily due to improved grades at African copper and higher throughput and grades at Antamina, partly offset by cessation of copper mining at Mount Isa. Guidance for 2026 is 810-870kt.

- Zinc: own-sourced production fell 17% to 176.9kt, mainly reflecting Lady Loretta end of mine life in late 2025 and a lower contribution from Kazzinc due to sequencing of own sourced feedstock.

- Cobalt: Production fell by 37% to 5,800t, mainly due to the introduction of the DRC’s export quota system in late 2025.

- Steelmaking Coal: production of 6.5mt was 22% lower primarily due to pit sequencing at EVR, wet weather in Queensland and a planned longwall move at Oaky Creek.

- Energy Coal: production was broadly in line at 22.9mt, with higher Australian production offsetting the Cerrejón production cuts.

Average prices for the group’s key commodities were strong during the quarter: copper (+37% vs. Q1 2025), Zinc (+14%), gold (+70%), silver (+163%), steelmaking coal (+27%), and energy coal (+13%). The company anticipates that current stronger commodity prices will more than offset increased input costs from Middle East conflict disruptions, potentially leading to margin expansion.

Glencore’s Marketing business exploits arbitrage opportunities that continuously emerge as a result of different prices for the same commodities in different locations or time periods. It provides a good hedge against commodity price volatility and finances the $1bn base dividend (see below), although clearly there is always a risk of potential losses because of that volatility. Extrapolating the Q1 Marketing performance would see full-year profit performance comfortably exceeding the top end of the group’s long-term Adjusted EBIT guidance range of $2.3-3.5bn p.a.

There is no update on the group’s profitability or financial position. As a reminder, at the end of 2025 net borrowing stood at $11.2bn, including $1.0bn of marketing lease liabilities, leaving gearing at a very comfortable 0.83x net debt to EBITDA, providing significant financial headroom.

Looking forward, the company is looking to strike the “right balance” between its growth ambitions and returns to shareholders. Excluding the various copper growth projects, capex will average $6.5bn p.a. from 2026-2028. Depending on the level of additional capex for new developments, aggregate investment could be $23.7bn. However, the company has said that although its plans can be self-funded, it will look at opportunities to reduce financial and operational risk via passive or active minority stakes or a strategic partner.

The dividend policy is to pay a fixed $1bn base distribution from the Marketing business, reflecting the resilience, predictability, and stability of the unit’s cash flows, plus a minimum payout of 25% of the Industrial free cash flow. Following the decision to retain the coal and carbon steel materials business, the group’s net debt ceiling which shapes its shareholder returns framework is $10bn. When net debt falls below this level (after the base distribution), cash will be periodically returned to shareholders via special cash distributions and/or share buybacks.

Following a merger with its Viterra business, Glencore owns 16.4% of Bunge, the diversified global agribusiness solutions company. The stake is worth $4.0bn at the current share price and is recognised as surplus capital, being warehoused for appropriate monetisation for Glencore shareholders at some point in the future. Underpinned by the value of these shares, the company is paying a top-up cash distribution of $7c/share (c.$0.8bn), taking the aggregate cash distribution of $17c/share (c.$2bn), to be paid in two equal instalments in June and September. This was a touch below last year and equates to a 2.2% yield.

Overall, while there is increased uncertainty around the impact of geopolitics in the near term, Glencore remains of the view that in certain commodities, the scale and pace of global mine project development will struggle to meet demand for the materials needed in the future. Glencore believes it is well placed to participate in bridging this gap, through the flexibility embedded in both its Marketing and Industrial businesses to respond to global needs.

We believe commodities and resource stocks are inexpensive when compared to financial assets and are relatively under-owned in investor portfolios. We also believe they provide something of a hedge against inflation.

Furthermore, the mining sector has a long history of M&A. Although the deal between Glencore and Rio Tinto fell apart earlier this year, we doubt Glencore will be immune from future deal speculation. In fact, Glencore’s share price has outperformed Rio’s recently (due to a coal price rally and iron price decline), which gives Glencore a stronger hand if talks were to resume after the 6-month cool-off period.

Source: Bloomberg