Morning Note: Market News and Updates from Diploma and Prudential.

Market News

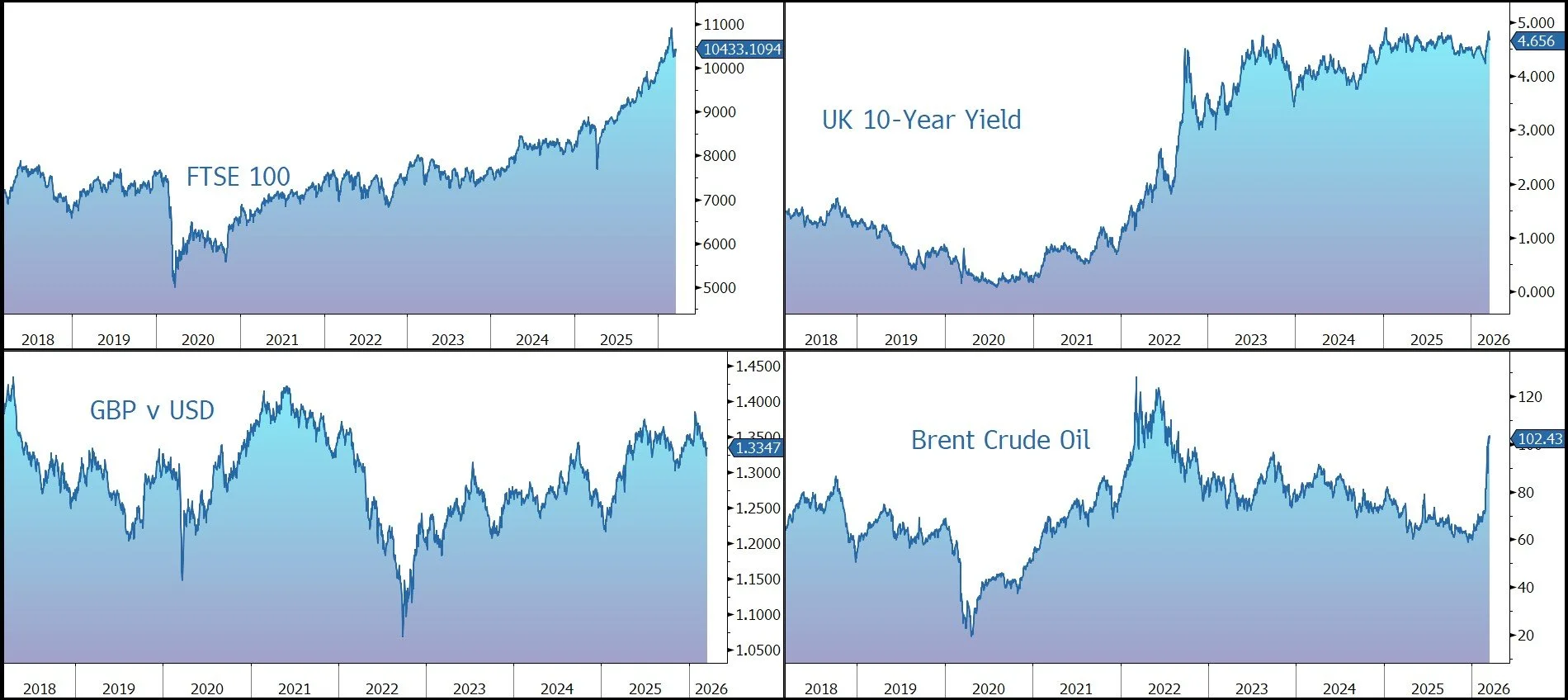

Global stocks rose for a third day as investors sought signs of stability even as the Iran war continued to roil energy markets. Brent dropped to $101 a barrel as Iraq struck a deal to resume exports via Turkey, avoiding the Strait of Hormuz.

Bond traders pared bets against Fed rate cuts this year ahead of today’s rate decision. The Fed is expected to hold rates steady, with investors looking to Jerome Powell for clues on how policymakers are weighing Middle East risks and the trade-off between inflation and slowing growth. The 10-year Treasury currently yields 4.18%, while gold is trading just below $5,000 an ounce.

Equities moved higher in the US last night – S&P 500 (+0.3%); Nasdaq (+0.5%) – with gains continuing in Asia this morning: Nikkei 225 (+2.9%); Hang Seng (+0.6%); Shanghai Composite (+0.3%). The move was led by technology stocks, as optimistic comments from Nvidia CEO Jensen Huang lifted chipmakers. Samsung Electronics rose 4%.

The FTSE 100 is currently 0.3% higher at 10,433, while Sterling trades at $1.3350 and €1.1575. Unilever is said to be weighing a separation of its food assets. As previously announced, Compass will change the trading currency of its shares on the LSE from sterling to US dollars, effective 1 April 2026. The change will not affect the company’s FTSE index inclusion or its LSE listing. Dividends will continue to be paid in Sterling unless shareholders elect to receive them in dollars.

Source: Bloomberg

Company News

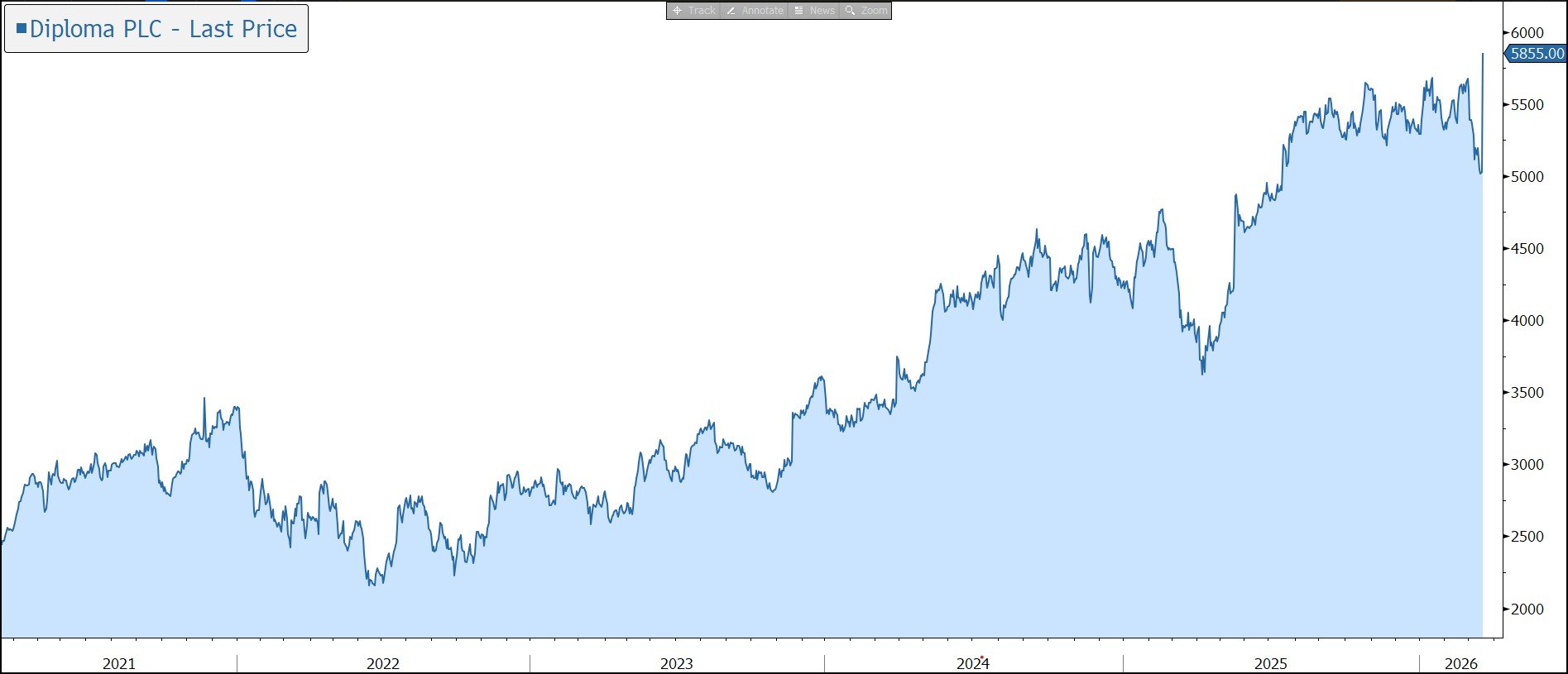

Diploma has this morning released a brief update which highlights that trading remains very strong. As a result, the company has upgraded its guidance for the financial year to 30 September 2026, representing a 13% upgrade to consensus operating profit forecast. In response, the shares are trading up 15% in early trading.

Diploma operates a decentralised collection of distribution businesses which supply specialised industrial and healthcare products and services to a wide range of niche end markets, in which service, rather than price is the key reason business is won and retained. The focus is on the supply of low-cost, but essential products, such as a seal for a hydraulic cylinder. Most of the revenue is generated from consumable products, usually funded by the customers’ operating budgets rather than their capital budgets, providing a recurring revenue base. By supplying essential solutions, not just products, Diploma has built strong long-term relationships with its customers and suppliers, which support attractive and sustainable margins (c. 20%) and consistently strong cash flow.

The strategy is to build high-quality scalable businesses that deliver sustainable organic growth. Acquisitions are an integral part of the strategy, with a disciplined focus on acquiring value-added businesses in fast growing niches, with great management teams, to accelerate organic growth and generate attractive returns on investment.

In today’s update, the company has highlighted that trading remains very strong and management is confident the positive momentum will continue in the group’s second half to 30 September 2026.

In Controls, the group supplies specialised wiring, cable, connectors, fasteners, and control devices used in a range of technically demanding applications. At the Peerless unit, aerospace demand and supply characteristics are favourable and sustainable, and the group expects another outstanding organic growth performance in the first half, with the second half returning to more typical growth rates against very strong comparators. The other Controls businesses also growing strongly. IS Group and Clarendon continue to execute well in structurally growing markets like energy, defence and aerospace. Windy City Wire is performing very well, with strong growth in markets including datacentres and digital antenna systems. The company expects H2 growth to be good against strong comparators.

In Seals, the group supplies a range of seals, gaskets, filters, cylinders, components, and kits used in heavy mobile machinery and specialised industrial equipment. The North American division continues to show good progress, with strong core growth in infrastructure and exciting developments in nuclear power generation. International Seals remains challenging - particularly in the UK - and will somewhat hold back overall Seals H1 growth rates.

The Life Sciences business supplies a range of consumables, instrumentation, and related services to the Healthcare and Environmental industries. The division is performing consistently in a tough healthcare market, with share gains in MedTech and in vitro diagnostic markets.

Overall, group organic growth excluding the Peerless business is strong and well ahead of the group’s financial model. Group margins continue to expand driven by accretive contribution from Peerless and steady accretion across the rest of the group.

As expected, there was little detail on the group’s profitability and financial position in today’s statement. Note that the company is financially strong – at the last balance sheet date (30 September 2025), gearing was 0.8x net debt to EBITDA, well below the 2.0x target.

Acquisitions continue to be an integral part of the group’s growth strategy. As reported in January, the company completed eight acquisitions in the preceding two quarters for c.£130m with expected annualised operating profit contribution of c.£20m. With a healthy short-term pipeline, management is optimistic about this momentum continuing in the months ahead. Potential acquisitions are not reflected in the group’s guidance.

In light of the strong performance, guidance for the full year to 30 September 2026 has been upgraded: organic revenue growth has been raised from 6% to 9% (remaining weighted to the first half) and the margin expectation lifted from 22.5% to 25%. Net acquisition growth is still expected to be 3%, although this will increase if further acquisitions are made. Overall, this represents a 13% upgrade to consensus operating profit of £377m. The company also expects another year of sustainable quality compounding, with earnings growth over 20% at strong returns on capital.

Source: Bloomberg

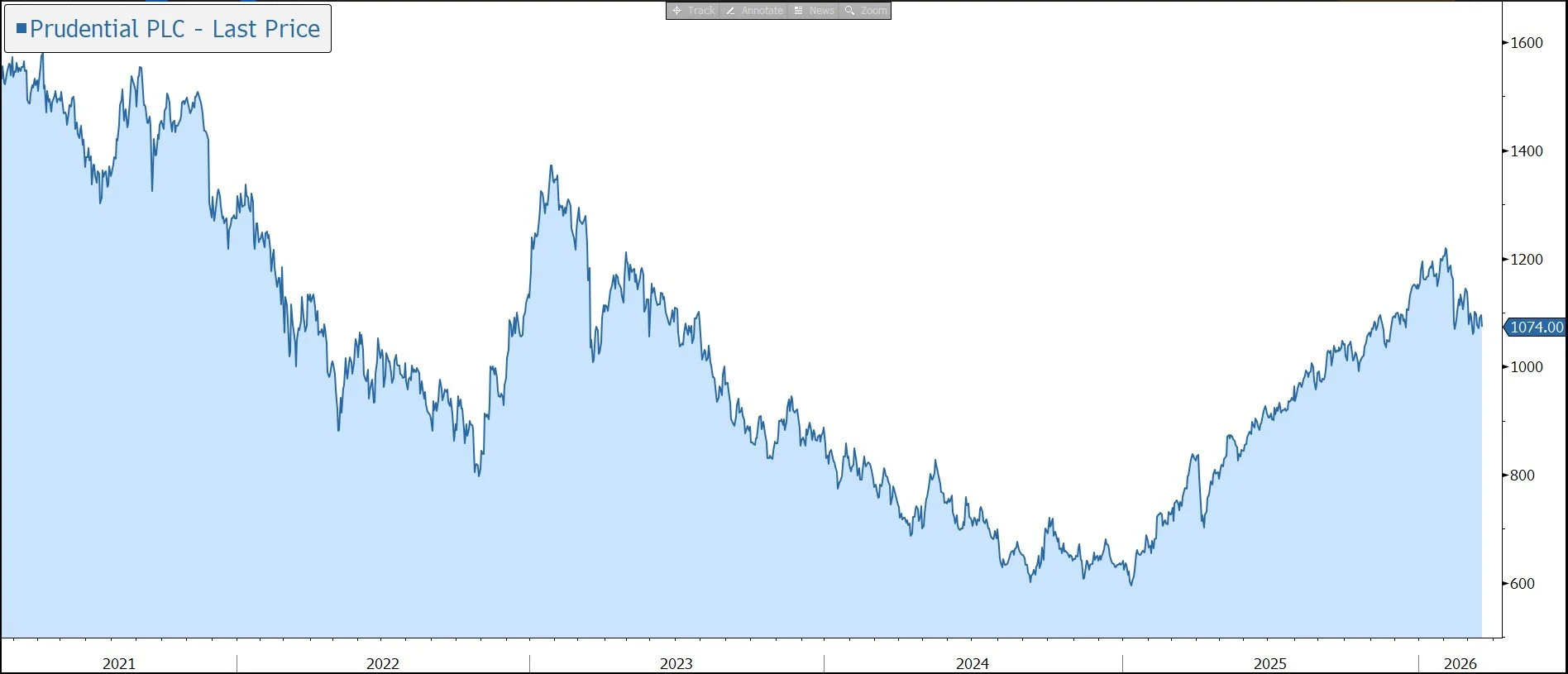

Prudential has today released its 2025 full-year results which highlight double-digit growth across key financial metrics in line with the group’s guidance. The company has also provided updated guidance on capital returns and raised its dividend by 15%. In response, the shares are trading 2% lower.

Prudential provides life and health insurance and asset management in 24 markets across Asia and Africa. The business has dual primary listings in Hong Kong and London. The company is not affiliated with Prudential Financial Inc., a company whose principal place of business is in the US, nor with The Prudential Assurance Company Limited, a subsidiary of M&G plc, a company incorporated in the UK which was demerged from Prudential in 2019 and is now listed in London.

As a diversified international operator, with strong branding, leadership positions, and distribution channels, Prudential is expected to benefit from the favourable structural opportunities in its key markets driven by a growing middle class and ageing population. The company operates in markets with a combined population of four billion people that are expected to collectively generate incremental annual gross written premiums of almost $1 trillion in 2033 compared with 2022.

The company has set out its 2027 financial and strategic objectives, one of which is to grow new business profit at a compound annual rate of 15%-20% from the level achieved in 2022. The group is also aiming to deliver double-digit compound annual growth in operating free surplus generated from in-force insurance and asset management business to deliver at least $4.4bn.

The company prioritises investment in organic new business at attractive returns and in enhancing its capabilities as it executes its strategy. Prudential will pursue selective partnership opportunities to accelerate growth in its key markets. Investment decisions will be judged against the alternative of returning surplus capital to shareholders.

EPS based on adjusted operating profit grew by 12% to 101.4 US cents per share with adjusted operating profit before tax up 5% to $3,306m. New business profit rose by 12% at CER to $2,782m, versus guidance to grow in the double digits, with a new business margin up two percentage points to 42%. Annual Premium Equivalent (APE) sales increased by 6% to $6.66bn.

The group’s largest market, Hong Kong, generated new business profit growth of 12%, driven by sales growth and margin enhancement across both domestic customers and Mainland China visitors and both the agency and bancassurance channels.

Elsewhere, Singapore delivered new business profit growth of 2%, reflecting strong growth in the second half, with a shift in demand towards savings and wealth products. The Mainland China joint venture grew new business profit by 27%, driven by strong APE sales growth in the second half of the year. Indonesia saw new business profit growth of 11%, driven by improvements in margin, supported by a shift towards higher margin products.

The group’s financial position is very robust with a strong capital base to fund growth. Prudential’s historic focus on ‘with profit’ savings, unit-linked, and health and protection business results in a relatively low volatility of free surplus to stress events. Based on the company’s current risk profile and its business units’ applicable capital regimes, Prudential seeks to operate with a free surplus ratio of between 175%-200%. If the free surplus ratio is above the operating range over the medium term and considering opportunities to reinvest at appropriate returns and allowing for market conditions, capital will be returned to shareholders.

At the end of 2025, the estimated shareholder surplus above the Group’s Prescribed Capital Requirement (GPCR) was $17.1bn, equivalent to a cover ratio of 262%. The free surplus ratio was 221%, well above the target range.

As a result, over the period 2024-2027 the company expects to have returned to shareholders more than $7bn out of excess free surplus. This includes the completed $2bn share buyback and the IPO of ICICI Prudential Asset Management Company Limited (IPAMC) in India in 2025. The company has commenced an additional $1.2bn buyback in 2026 and expects a $1.3bn capital return in 2027, comprising recurring capital returns and IPAMC IPO net proceeds.

The target for dividend growth is more than 10% for each of 2025-2027. The 2025 payout has been increased by 15% to 26.6c, equating to a yield of 1.7%.

Looking to 2026, momentum remains positive and the group is confident in its double-digit growth trajectory across its key metrics in 2026, putting the company firmly on track to achieve its 2027 financial objectives.

Source: Bloomberg