Morning Note: Market News and an Update from German Property Company Vonovia

Market News

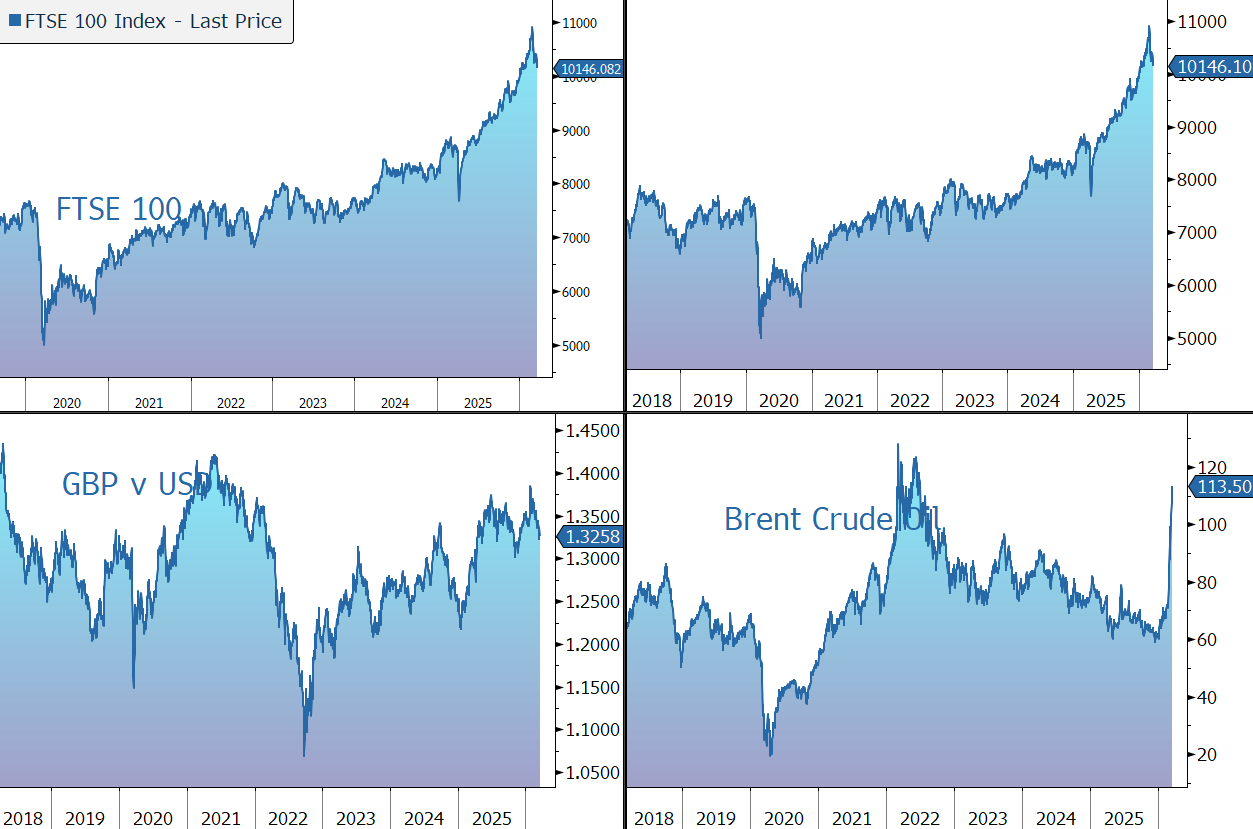

Brent moved up to $115 a barrel while European natural gas prices jumped 35% as fresh attacks on key energy infrastructure in the Middle East heightened concerns over disruptions to global oil and gas flows. Iran launched missile strikes on a Qatari facility housing the world’s largest LNG export plant, marking one of several energy assets Tehran vowed to target following an Israeli strike on Iran’s South Pars gas field. Donald Trump pressed for a de-escalation of attacks on Middle East energy sites. He said Israel will refrain from further strikes in the South Pars gas field and threatened retaliation if there are more attacks by Iran on Qatar’s LNG facilities.

Jerome Powell said higher energy prices will push up overall inflation in the near term, but it’s too soon to know the potential effects on the economy. The Fed kept rates on hold as expected. The 10-year Treasury yields 4.28%. The ECB is projected to hold rates steady, with traders fully pricing two hikes later this year amid the threat of rising inflation. The Bank of England is also set to stand pat, at 3.75%. The dollar remained firm and gold continued its recent pullback and currently trades at $4,730 an ounce.

Global equities retreated. In the US equities last night, the main indices fell – S&P 500 (-1.5%); Nasdaq (-1.6%) – and are currently expected to drift lower at the open this afternoon. In Asia this morning, markets were also weak: Nikkei 225 (-3.4%); Hang Seng (-2.0%); Shanghai Composite (-1.4%). The yen steadied near 160 after the Bank of Japan kept rates unchanged, as expected.

The FTSE 100 is currently 1.5% lower at 10,146, while Sterling trades at $1.3260 and €1.1575. The UK will increase tariffs on steel imports to 50% and reduce import quotas by 60% from July, following similar protectionist measures by the EU, Canada and the US.

Source: Bloomberg

Property News

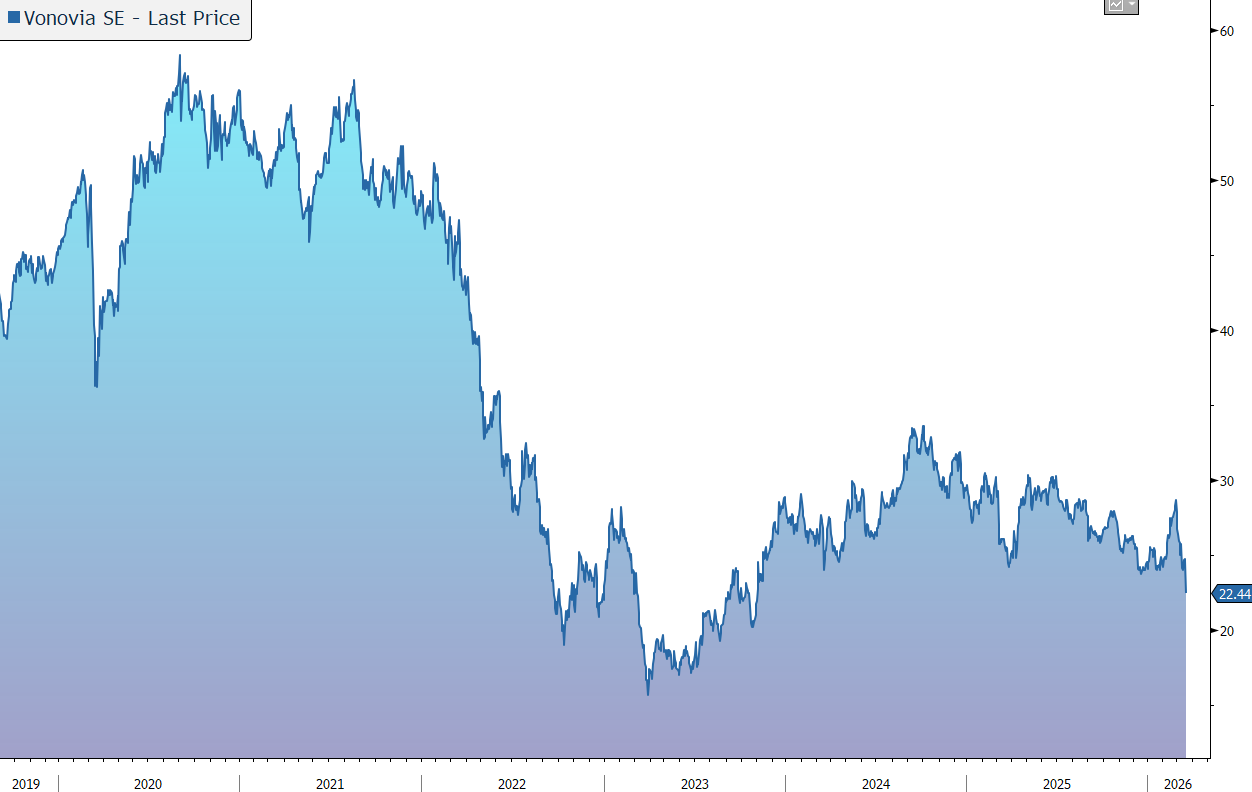

Vonovia has released its 2025 full-year results which highlighted improved earnings across all segments and stable cash flow despite sustained high construction and financing costs, a smaller portfolio, and regulatory uncertainties. Guidance for 2026 and 2028 have been reiterated and, given the higher interest rate environment, the company has set out more ambitious leverage targets. The dividend has been increased by 2.5% and the policy going forward simplified. Despite the improved sector outlook, the shares have been weak over recent weeks, tracking the upward move in bund yields, driven by inflation concerns arising from the conflict in the Middle East. Ahead of this afternoon’s analysts’ call, they are down 8% in early trading, leaving them on a 50% discount to NAV.

Vonovia is Europe’s largest residential real estate company with a market cap of around €19bn. The group owns around 531k units worth around €84.4bn across Germany (c. 85%), Sweden, and Austria. The group also manages a further 76k units owned by others. Despite its size, in Germany Vonovia still only owns 2% of a highly fragmented market. The focus is on multi-family housing for low- and medium- income tenants in metropolitan areas. The aim is to benefit from residential megatrends such as urbanisation, energy efficiency, and demographic change.

Following a number of acquisitions, Vonovia now enjoy the benefits of increased scale – over the last 12 years, its adjusted EBITDA operations margin has risen by 20 percentage points to 80% and its cost per unit has fallen by two thirds.

Luka Mucic has recently become CEO. He was CFO of Vodafone and previously the CFO and COO of SAP – with long-term experience in the technology and telecommunications industry, on the face of it the appointment appears a strange one. The rationale appears to be an expertise in digitalisation and process efficiency. With his first set of results, the CEO has laid out some new strategic priorities including tighter leverage targets, enhanced disclosure, improved transparency, and an amended dividend policy.

In 2025, despite sustained high construction and financing costs, a portfolio that is 9000 units smaller, and regulatory uncertainties, the company improved its results across all segments, kept cash flow stable, and successfully continued to pursue its strategic priorities.

Adjusted earnings before tax (EBT) – the group’s preferred profit metric – rose by 4.8% to €1,904m, in the middle of the €1.85bn-€1.95bn guidance range. Operating free cash flow (OFCF) – the key figure for internal financing and thus liquidity management – was down 2.9% to €1,779m, versus guidance to be slightly below last year.

The most recent market data for the German residential sector has seen a positive development of key performance indicators and confirmation of a trend reversal in property values. There is a high level of demand for rental properties and positive rent trend. Thanks to the market recovery, the company can now realise the prices in sales that it has targeted.

The core rental segment continued to benefit from a positive market environment. Earnings grew by 2.5% to €2,445m, despite having 9,000 fewer homes. The vacancy rate remains very low (2.1%) and highlights the ongoing mismatch between supply and demand. The trend towards higher rents continued, while the collection rate was over 99%. This includes all ancillary and energy costs, which management see as a strong sign of affordability.

The organic increase in rent was 4.1%, with new construction accounting for 0.5%. Like-for-like rental growth of 3.6% was driven by market-related factors (+2.6%) and investment in existing buildings (+1.0%). The monthly rent per square metre increased by 4.6% to €8.38. Going forward, under the regulatory system, rent growth is expected to follow inflation higher over time albeit with a lag. For 2026, rental growth is expected to be 4.2%. Further out, the expectation is ‘around 5%’ driven by an additional investment in modernisation.

Each of the three non-rental segments also outperformed the previous year, as the growth initiatives are increasingly bearing fruit: development (up from €30m to €75m), recurring sales (+44% to €83m), and value-add (+17% to €197.5m). Overall, the company is seeing continued signs of increased traction in these segments and is targetting multiple organic growth initiatives to develop non-rental activities. In 2028, the group estimates a contribution of 20%-25% of adjusted EBITDA, versus 13% currently.

Vonovia continued to sell properties of inferior quality or in non-core regions. The volume of recurring sales was 5.5% lower in the period (at 2,333), with the fair value step-up, at 31.8%. Outside of the recurring sales segment, 8,973 non-core units were sold, up 73%.

Capital is being partly re-allocated toward the construction of new properties and the improvement of the existing portfolio to comply with environmental demands which can drive higher rents. In the 2025, the group spent €1973m (+23%), made up of maintenance +6%, modernisation +32%, and new construction +58%. Vonovia completed only 2,090 new apartments (down 44%), 40% to hold to rent and 60% for sale. The company is currently undertaking construction projects for more than 4,200 units. The long-term pipeline comprises around 65,000 units.

The company’s balance sheet remains stretched – loan-to-value (LTV) declined slightly from 45.8% to 45.4% but is still above the 40%-45% target range. Given the higher interest rate environment, the company has today set out tighter leverage targets for 2028 for Net debt/EBITDA (<12x vs 13.8x in 2025) and LTV (c. 40%). Deleveraging efforts will include a more active pursuit of disposal opportunities and a review of minority positions in non-strategic participations both in Germany and abroad.

At present, the group’s long-term and well-balanced debt maturity profile provides a hedge against increasing financing costs: weighted average maturity (6.3 years); average cost of debt (2.1% vs. 1.9% at the end of 2024); fixed/hedged (98%). The strategy is to roll over secured debt and repay unsecured bonds with disposal proceeds.

With today’s results, the dividend policy has been simplified. The company will pursue a progressive policy and will aim for a payout ratio between 50% and 60% of adjusted EBT. This compares to the previous policy to pay out 50% of earnings plus surplus liquidity from operating free cash flow. For 2025, a payment of €1.25 per share has been declared, 2.5% higher than last year. This amounts to a yield of 5% and will be paid in June.

The like-for-like market value of the portfolio rose by 3.1% to €84.4bn in the year. This follows a 0.5% increase in H2 2024, supporting management’s view that the market has now bottomed out. The value is 23.2x in-place rent and a 4.3% initial gross yield. The net asset value (known as EPRA NTA) rose by 2.3% to €46.28.

Guidance for 2026 has been reiterated: EBT of €1.9bn-€2.0bn and adjusted EBITDA of €2.95bn-€3.05bn. The company has also reiterated its target for EBITDA in 2028 of €3.2bn-€3.5bn.

Greater visibility over the outlook for interest rates and property market valuations will be required for the shares to move higher. Clearly, government plans to ease its fiscal rules are unhelpful, with bund yields rising in anticipation of an increase in government debt, a trend that has been exacerbated by the inflation concerns as a result of the Middle East conflict. Not only does this increase the group’s borrowing costs (and reduce free cash flow) but it also has a negative impact on property values and makes bond proxies such as real estate relatively less attractive. In the meantime, however, we are comforted by the outlook for rental growth, the improved transaction market, and the ongoing substantial mismatch between Vonovia’s equity value (€2,361 for the German portfolio), the valuation in the direct real estate market (€3,500), and the cost of newly constructed properties (€5,600).

Source: Bloomberg