Morning Note: A Round-up of Global Financial Market News.

Market News

Markets continue to be driven by news flow on developments in the Middle East. Some optimism was seen yesterday sparked by reports of some limited shipping activity through the Strait of Hormuz. However, this has given way to more pessimism about the still-subdued flows through the strait and the seemingly rising risk of a protracted war.

President Trump said he had requested that China delay a summit with Xi Jinping for about a month, saying it was important for him to remain in Washington to oversee the war. Some commentators suggested this may be taken as a sign that the war is likely to drag on longer than expected.

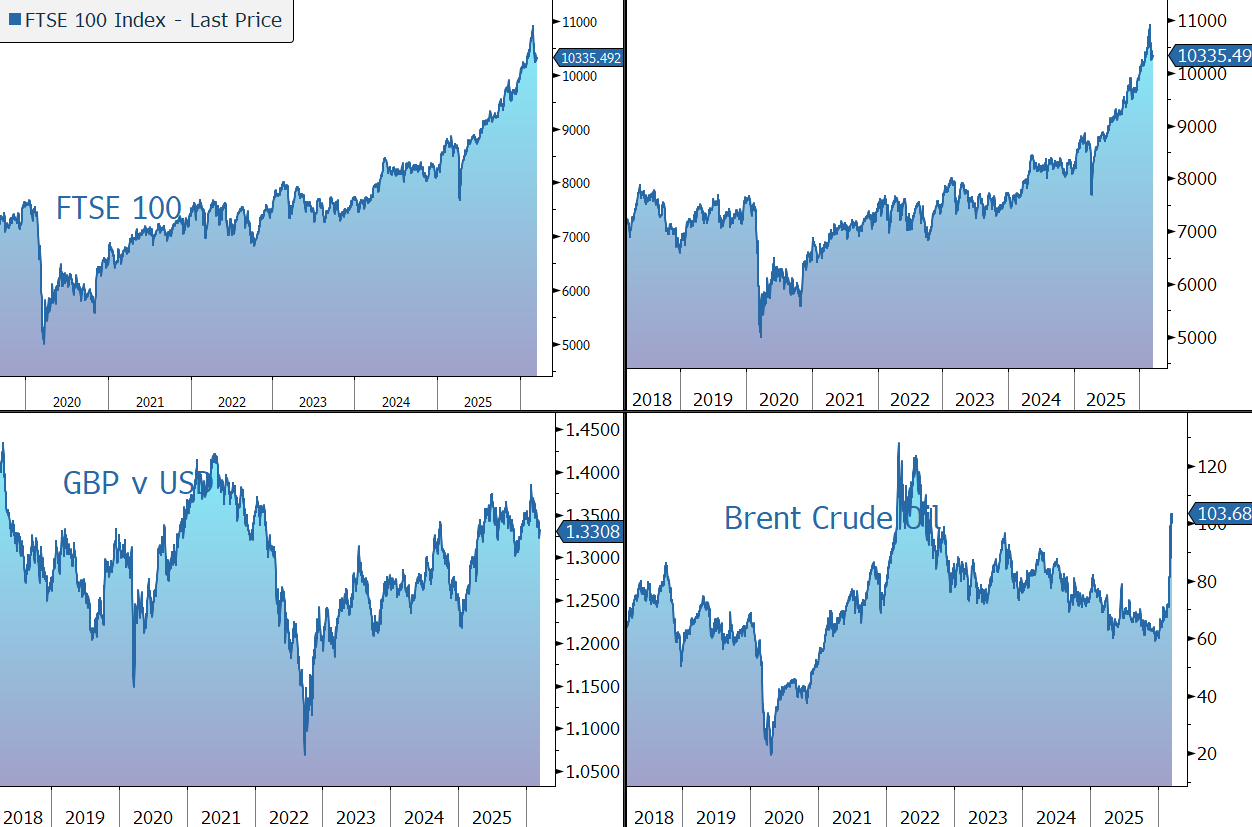

Brent crude rose 4% to about $104 a barrel, rebounding from Monday’s 3% drop, as Iran stepped up attacks on energy infrastructure. Operations were suspended at the Shah natural gas field in the UAE due to a fire while a drone attack temporarily shut the Fujairah port. An Iraqi oil field and a key Emirati port were also targeted.

Treasuries fell across the curve, with the 10-year yield climbing three basis points to 4.25%. Gold moved back up to $5,020 an ounce. Traders remain focused on how policymakers from the Federal Reserve to the European Central Bank and the Bank of England will respond this week to inflation concerns.

US equities rose last night – S&P 500 (+1.0%); Nasdaq (+1.2%) – but have slipped back in futures trading. Nvidia was firm as Jensen Huang said AI chips will help generate $1 trillion in revenue through to 2027. In Asia this morning, equities were subdued: Nikkei 225 (-0.1%); Hang Seng (+0.2%); Shanghai Composite (-0.9%). The FTSE 100 is currently 0.2% higher at 10,335, while Sterling trades at $1.3310 and €1.1575.

Private credit default rates will climb to 8% as AI advances disrupt the software industry, according to Morgan Stanley. Commerzbank’s potential €35bn takeover by UniCredit was dismissed as ‘unacceptable’ by Germany.

Source: Bloomberg