Morning Note: A Round-up of Global Financial Market News.

Market News

Stocks advanced and oil pared gains following a report that Iran offered the US a proposal to reopen the Strait of Hormuz, easing concern that efforts to restart peace talks had stalled. President Trump will send two envoys to Pakistan with the intention of talking with Iranian officials.

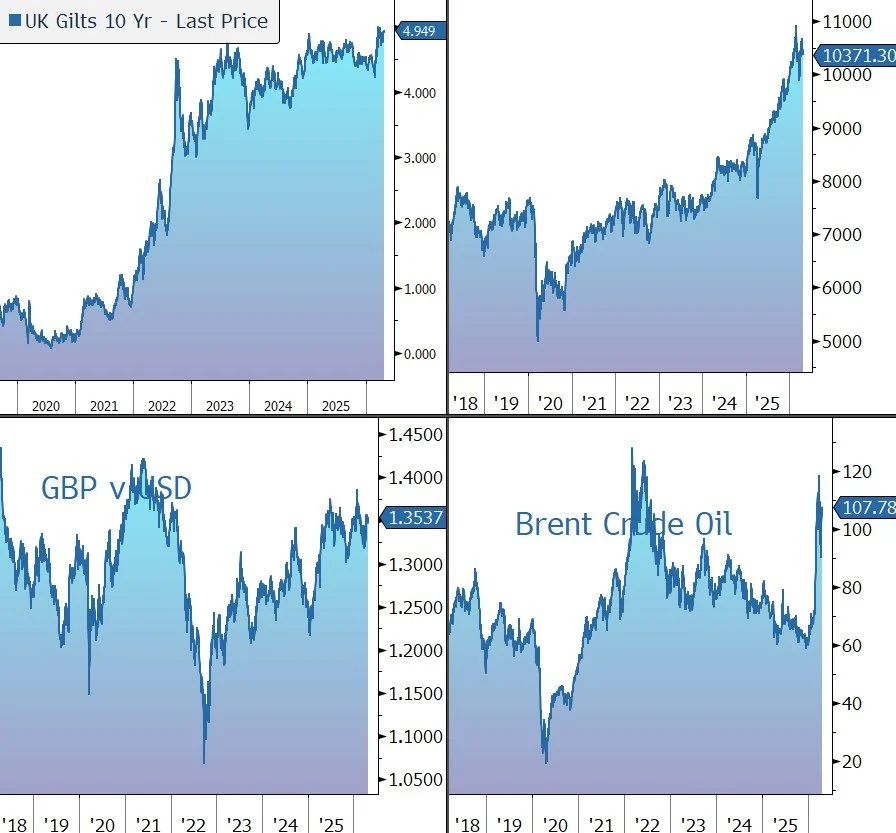

Brent Crude currently trades just above $107 a barrel. Persian Gulf crude output is 57% below pre-war levels. Goldman has raised its oil forecasts, seeing Brent at $90 in the fourth quarter, as Hormuz disruptions drive an estimated 9.6m b/d deficit this quarter. Gold ticked up $4,715 an ounce.

US market closed higher on Friday ending just off the best levels: S&P 500 (+0.8%); Nasdaq (+1.6%). Stocks were also helped by the US Department of Justice ending a criminal probe targeting Fed Chair Jerome Powell, while Senator Thom Tillis said he’s dropping his blockade of Kevin Warsh’s Fed nomination. The yield on the US 10-year Treasury trades at 4.32% as traders increased bets on rate cuts.

In Asia, equities were mixed this morning: Nikkei 225 (+1.4%); Hang Seng (-0.3%); Shanghai Composite (+0.2%). The FTSE 100 is currently little changed at 10,371, while Sterling trades at $1.3535 and €1.1535.

It’s a bumper week for earnings, with reports from BP, Assa Abloy, Atlas Copco, Visa, Alphabet (Google), Glencore, and Unilever.

The FT reports that UK Chancellor Reeves is preparing to set out a fresh push for fiscal discipline, closer ties with the EU, and planning reform, in an effort to boost growth in the aftermath of an expected defeat for Labour in the elections next week.

Source: Bloomberg