Morning Note: Market News and an Update from Spirax Group.

Market News

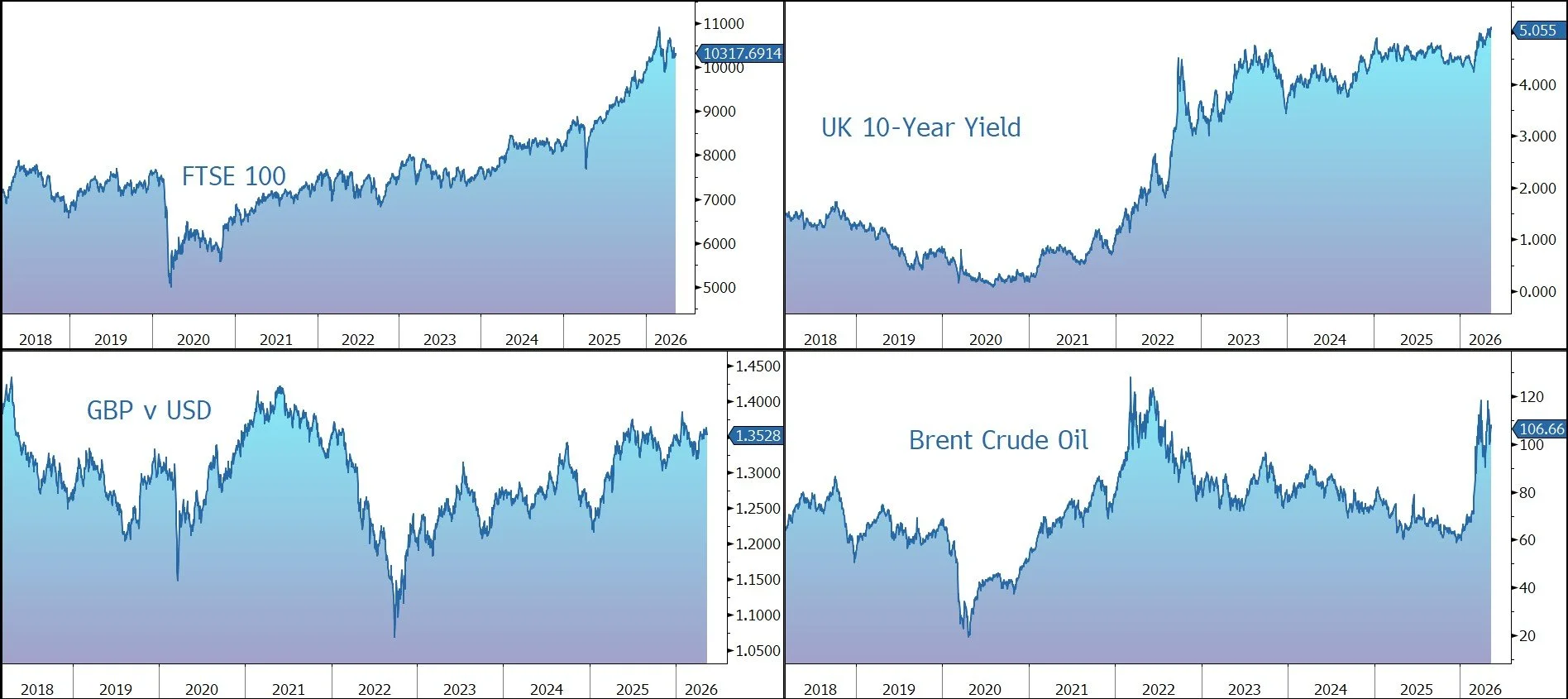

Brent Crude dipped below $107 a barrel after rising almost 8% over the past three sessions, as Iran peace talks remain at an impasse with a US Naval blockade of the Strait of Hormuz.

US inflation jumped to 3.8% in April, its highest level in three years, driven by the effects of the conflict in the Middle East. The core rate, which strips out volatile food and energy prices, rose from 2.6% to 2.8%. The reading was higher than market expectations and the yield on the US 10-year Treasury rose to 4.46%. Gold moved back above $4,700 an ounce.

ECB rate hikes are “increasingly likely” amid elevated energy prices, Bundesbank President Joachim Nagel told Handelsblatt

US equities drifted lower last night – S&P 500 (-0.2%); Nasdaq (-0.7%) – although futures rose after the White House said Jensen Huang will join Donald Trump’s China trip starting today.

Asia stocks rose, erasing losses as dip buyers stepped in following weakness in chipmakers: Nikkei 225 (+0.8%); Shanghai Composite (+0.7%). Japan’s 20-year yield hit the highest since 1997.

The FTSE 100 is currently 0.5% higher at 10,318. Traders are the most bearish on the pound – currently $1.3530 and €1.1550 – in five weeks as Keir Starmer clings to power after ministerial resignations, with odds putting his chances of surviving beyond 2026 at one in five. The turmoil comes ahead of the King’s Speech, where a packed legislative agenda now faces uncertainty. The political uncertainty also continues to weigh on the Gilt market – the 10-year yield rose to 5.10%.

Source: Bloomberg

Company News

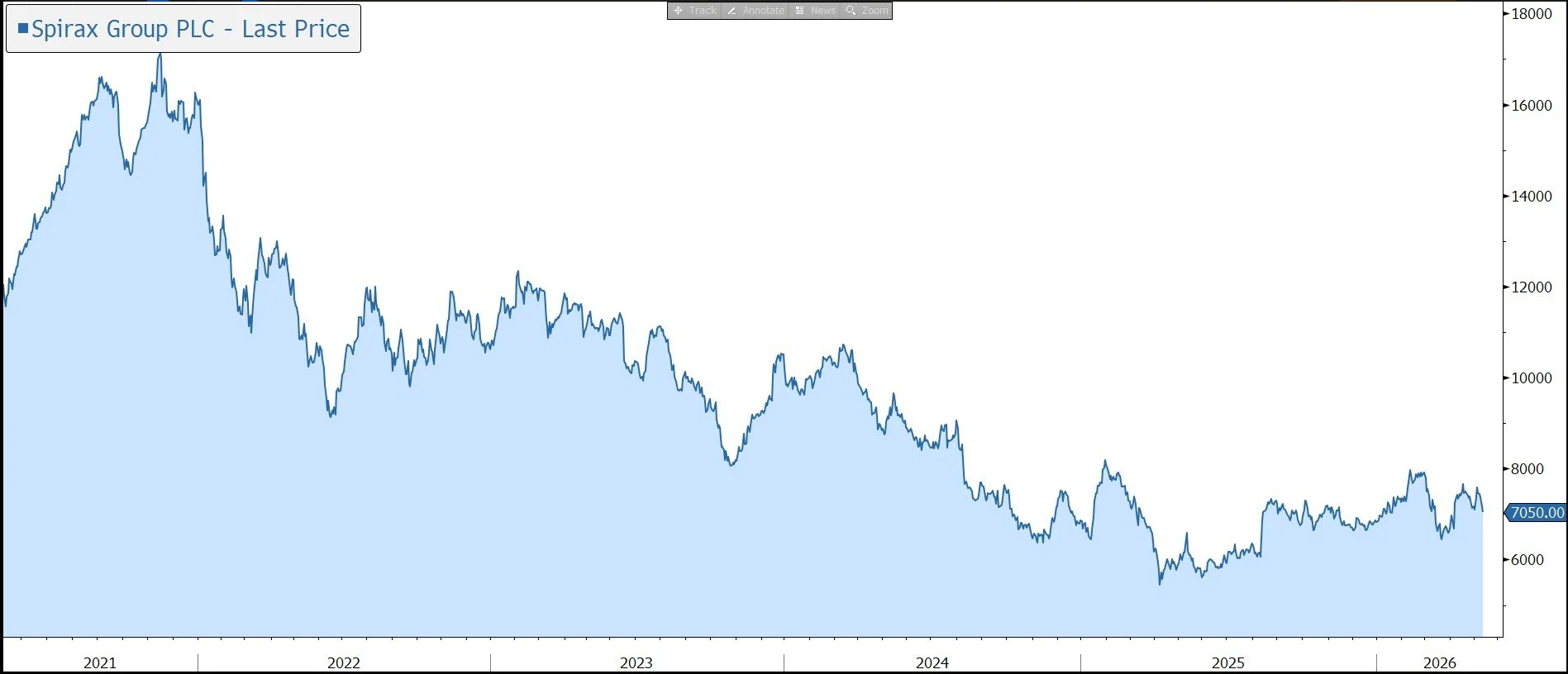

Spirax Group has released a trading update in respect of the four months ended 30 April 2026. Despite the challenging macroeconomic environment, organic growth is running in line with expectations across all businesses and guidance for the full year has been reiterated. In response, the shares are little changed in early trading.

Spirax (formerly Spirax-Sarco Engineering) is a UK-listed industrial company, with annual sales of £1.7bn. The group is a world leader in each of its three businesses. In Steam Thermal Solutions (50% of revenue), Spirax Sarco and Gestra are leaders in the control and management of steam. In Electric Thermal Solutions (26%), Chromalox and Thermocoax provide electrical process heating and temperature management solutions. Finally, Watson-Marlow Fluid Technology (24%) provides niche peristaltic pumps and associated fluid path technologies.

The group’s products are used in almost every industry worldwide: from the food sector where steam products are used in blanching, baking, packaging, and cleaning; to the pharmaceutical industry where pumps and associated fluid path equipment are critical to the production of life-saving medicines; through to the aviation industry where electrical heating elements are used in the de-icing of aeroplanes.

85% of revenue is generated from maintenance and operational (opex) budgets rather than capital (capex) budgets. Of that 85%, 50% comes from essential repair and maintenance activities, while 35% comes from small projects that improve existing systems. As a result, the group has a long history of stable, sustainable growth and strong profitability.

However, in response to a weaker macroeconomic environment, the group took early action across all three businesses to appropriately right-size capacity and overhead support costs, as well as implementing temporary cost containment actions and reducing variable compensation. The company has now completed its restructuring programme and realised annualised savings of £40m, with half delivered in 2025. Most of this will be reinvested in organic growth initiatives.

So far this year, macroeconomic uncertainty has remained elevated, with conflict in the Middle East adding to the ongoing trade tariff developments and higher energy costs weighing on industrial production growth. Global Industrial Production growth (IP) in Q1 2026 was 1.4%, remaining weak in key European markets. Excluding China, IP was 1.5% with the full-year forecast of 1.9% broadly unchanged from February and weighted to the second half. Spirax remains cautious on the IP outlook as reflected in its guidance.

The company has continued to execute against its strategic priorities, delivering organic growth ahead of IP alongside margin progression. Demand trends were consistent with those highlighted in the group’s 2025 full-year results in March.

The company delivered mid-single-digit organic revenue growth and an improvement in adjusted operating profit margin on an organic basis compared to the same period in 2025.

Within the Steam Thermal Solutions business, demand grew ahead of IP and in line with management expectations, supported by sustained strength in MRO (Maintenance, Repair, and Overhaul) and solutions across all regions and some recovery in large project demand. Demand in China and Korea also continued to recover.

The Electric Thermal Solutions business delivered double-digit demand growth across all divisions, including continuing strong growth in Wafer Fabrication Equipment manufacturers (Semicon).

Demand in Watson-Marlow remained robust in both Process Industries and Pharmaceutical & Biotechnology (Biopharm).

The group is financially robust, with net debt at the end of March little changed at £575m and gearing of 1.5x net debt to EBITDA, at the upper end of the target range. The group has a strong track record of dividend growth, with 58 years of progress.

A full-year payout of 170p was declared for 2025, up 3%, equal to a yield of 2.5%, with the final payment of 121.1p to be paid on 22 May 2026, subject to shareholder approval.

Looking ahead, despite the weak IP environment, the company has reiterated its guidance for 2026. The target is mid-single-digit organic revenue growth, well ahead of IP, and an increase in adjusted operating profit margin on an organic basis. The company continues to expect organic growth in revenue and adjusted operating profit margin to be higher in the second half of the year, reflecting the usual seasonal profile. By division, organic sales growth is expected to be: STS (low single-digit), ETS (high single-digit), and Watson-Marlow (high single-digit).

Over the medium term, the aim is to grow ahead of underlying markets, with high-single digit profit growth delivered through mid-single digit organic sales growth (close to 2x IP) and an improving margin reaching between 22% and 23%. This will drive cash conversion of over 80% and an improving return on capital.

Source: Bloomberg