Morning Note: Market News and an Update from National Grid.

Market News

Donald Trump and Xi Jinping kicked off talks in Beijing, with the US president saying US and China ties will be “better than ever.” Xi stressed partnership over rivalry but also warned of risks to their alliance if the issue of Taiwan wasn’t handled well. Xi also told US business leaders that China will open its door wider, CCTV reported.

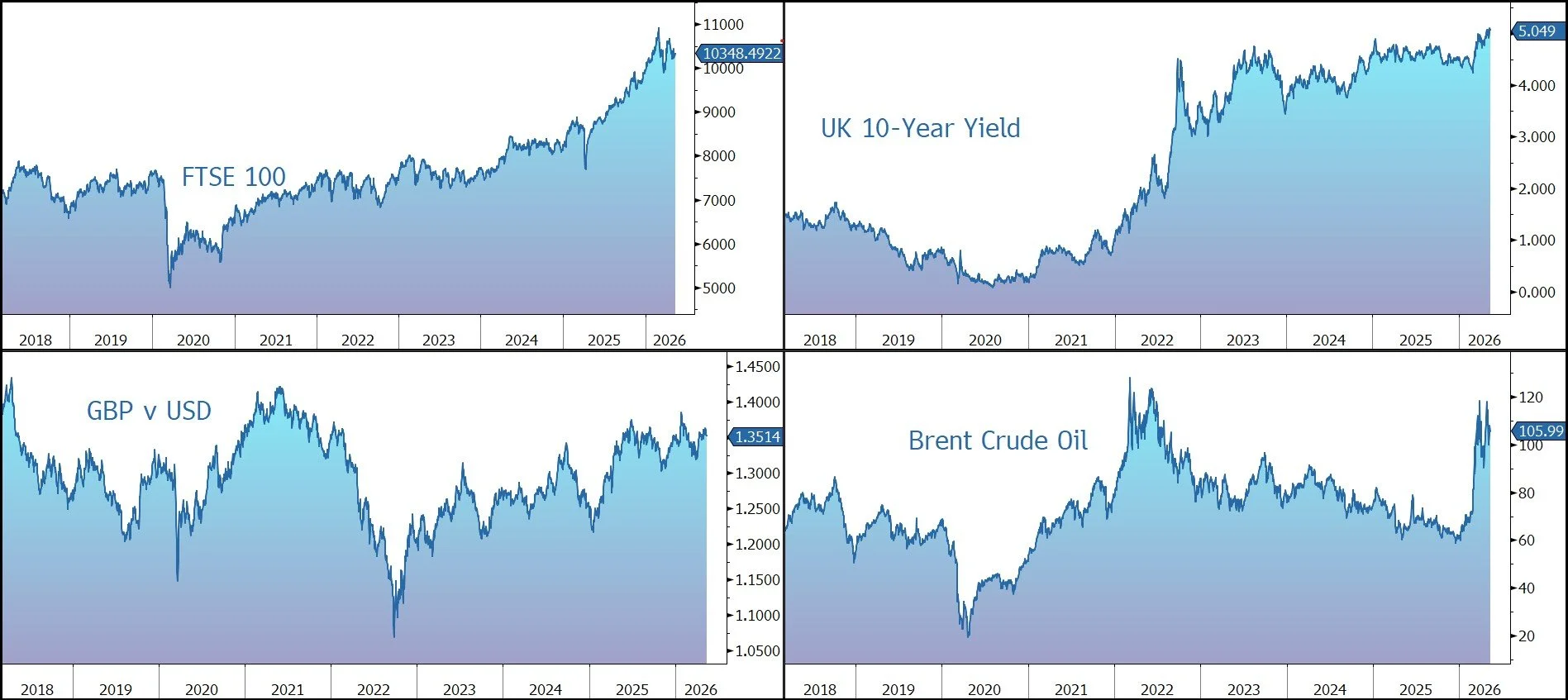

Marco Rubio told Fox News earlier that the US is trying to convince Beijing to get Iran to “walk away” in the Gulf. Brent Crude trades at $106 a barrel. The ‘unprecedented supply shock’ from the closure of the Strait of Hormuz is expected to cause a shortfall of 1.8m barrels a day, according to the IEA.

Kevin Warsh was confirmed as Fed chair in a 54-45 Senate vote, by the slimmest margin ever for the post. The yield on the US 10-year Treasury rose to 4.47%, while gold trades at $4,705 an ounce.

US equities moved higher last night – S&P 500 (+0.6%); Nasdaq (+1.2%) – after a surge in tech shares pushed Wall Street to a record. Cisco soared 20% post-market after the company’s sales forecast topped estimates and it announced plans to cut thousands of jobs.

In Asia, equities generally declined: Nikkei 225 (-1.0%); Shanghai Composite (-1.5%). Longer-dated JGBs fell, with the 30-year yield climbing as much as 10 basis points to 3.915%, the highest since the tenor’s 1999 debut. The FTSE 100 is currently 0.2% higher at 10,348. Companies trading ex-dividend this morning include BP (1.13%), GSK (0.9%), HSBC (0.56%), Tesco (2.12%), and Unilever (0.95%).

The Labour Party is headed for a bitter fight over the PM’s post as Keir Starmer’s fate hangs in the balance. Sterling trades at $1.3515 and €1.1540, while 10-year Gilt yields remain above 5%. A UK house price gauge fell to minus 34 in April, its lowest point since November 2023, RICS reported.

Source: Bloomberg

Company News

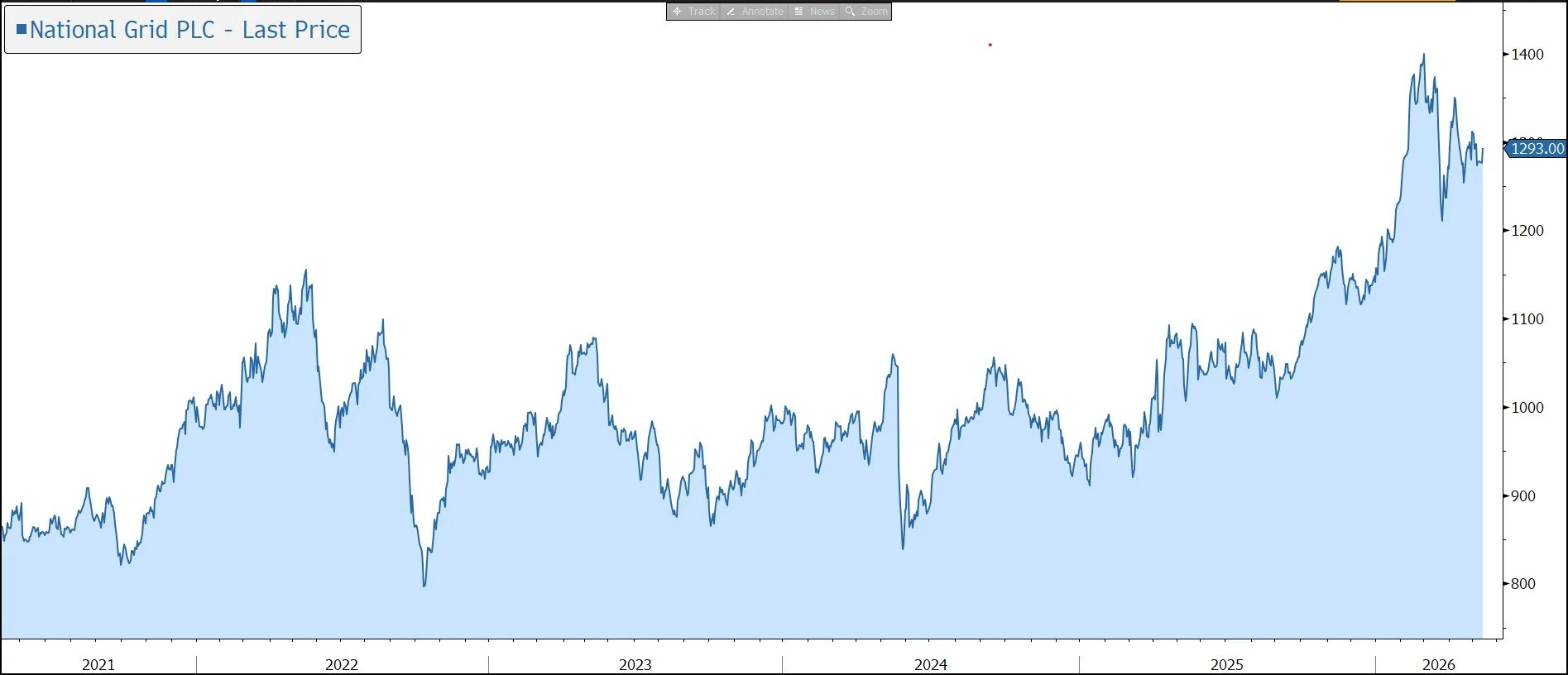

National Grid has today released results for the financial year to 31 March 2026 that were in line with market expectations. During March, the company extended and upgraded its 5-year financial investment framework and accepted the latest regulatory framework for its UK Electricity Transmission Business. As a result, EPS growth is now expected to be 8%-10% p.a., with dividend growth in line with UK inflation. We are positive on the long-term outlook for the business given the company’s critical role in the energy transition and security of supply. As an income stock, the performance of the shares is driven, in part, by bond yields, with the recent increase providing a headwind. However, the dividend yield is now below 4%, implying the stock is now being viewed more as a growth utility than a bond proxy. In response to this announcement, the shares have been marked up by 1% in early trading.

National Grid operates a regulated infrastructure business in the UK and US, with electricity and gas transmission and distribution assets. The group has no direct exposure to volatile commodity prices and relatively little exposure to usage levels.

The global power grid is critical infrastructure that requires substantial and sustained investment to integrate an ever-growing pipeline of renewables and support the rising demands of an electrified world. Put simply, the grid needs to be larger, smarter, and more resilient to enable the energy transition to continue at pace.

Over the last few years, National Grid has pivoted its portfolio towards electricity. This has enhanced the group’s role in the decarbonisation of the energy system, with investment in infrastructure that enables higher penetration of renewable energy and low carbon technology. Increased demand will also come from new connections to AI data centres – there is currently a massive queue of data centres waiting for grid connections.

In response, the company is undertaking a significant hike in investment in order to deliver a step-change in critical energy infrastructure in the UK and US in support of energy transition, security of supply, and economic growth objectives.

Back in March, the company set out an extended and upgraded 5-year Financial Framework to March 2031 which replaced its existing framework to March 2029. The cumulative capital investment is expected to be at least £70bn, versus the previous target of £60bn over the five years to March 2029. Around two-thirds of the investment is covered by regulatory agreements.

The plan represents a 70% increase compared to the prior five years, reflecting a doubling of investment into UK electricity networks and an almost 50% increase in investment into US gas and electricity networks. The expected split across the group is: UK Electricity Transmission (£31bn); UK Electricity Distribution (£9bn); New York Regulated (£17bn); New England Regulated (£12bn); and National Grid Ventures (£1bn). The company has secured supply chain and delivery mechanisms for around three-quarters of its investment plan.

The company also continues to streamline its portfolio to focus on pure-play networks across regulated and competitive onshore and offshore networks. It has sold its ESO (electricity system operator), National Gas Transmission, its National Grid Renewables onshore business in the US, and its Grain LNG business.

The target is to generate asset growth CAGR of around 10%, with group assets heading towards £115bn by March 2031. With most of the investment going into the group’s electricity networks, the mix will continue to move away from gas.

Underlying EPS CAGR is expected to be 8%-10% from an FY26 baseline of 78p, more aligned with the group’s asset growth.

Regulatory progress continued during the year. The group has accepted all of the RIIO-T3 price control arrangements proposed by the regulator Ofgem in its Final Determination, which covers the UK Electricity Transmission business for the period April 2026 to March 2031. The company is confident that this price control enables delivery of an overall return on equity above 9% (6.12% real) across the price control.

In addition, the company has also achieved constructive US regulatory outcomes, and combined with progress in securing the supply chain, creates improved visibility and momentum across the group over the next five years.

On to the results. In the financial year 31 March 2026, underlying operating profit grew by 9% on a constant currency basis to £5,680m. This improvement was principally driven by higher allowed revenue in UK and New York, supported by new rates and increased allowances, offset by the one-off impact of customer refunds related to the March 2026 FERC order on New England transmission returns. Underlying EPS rose by 8% to 78p.

Capital investment rose by 18% to a record £11.6bn during the year, driving asset growth of 10.9%. This was principally driven by UK transmission projects, asset replacement, and network enhancements in the US. The regulatory asset value (RAV) rose by 11.7% to £66.4bn, with the UK and US up by 13% and 10% respectively. Group return on equity was up 80 basis points to 9.8%.

National Grid has a robust balance sheet and a strong investment grade credit rating, underpinned by regulatory revenue, which allows the group to secure the required long-term funding needed to invest in its business. The group believes it has the financial flexibility to deliver its strategy over the 5-year financial framework, helped in part by the £6.8bn rights issue in 2024. During the latest financial year, net debt rose from £41.4bn to £44.2bn, reflecting the increased capital investment in the year, partly offset by £2.8bn of net cash proceeds from the divestments of National Grid Renewables and Grain LNG. Regulatory gearing was 61% and is expected to trend back to the high 60% range by 2030/31.

The stock remains popular with investors seeking an attractive income that is growing in real terms – the dividend policy to deliver annual growth in line with the increase in average UK CPIH inflation has been reiterated. The payout for the financial year to 31 March 2026 was increased by 3.8% to 48.49p, equivalent to a yield of 4%.

FY2027, the company expects strong operational performance across the group, with underlying EPS growth of 13%-15%, reflecting higher allowed revenue as it steps up delivery from RIIO-T2 to RIIO-T3 regulatory regimes. The accelerated rate of growth will be helped by a streamlined connection process for AI data centres.

Although regulation provides a framework for the company to operate within, it can be a double-edged sword – at a time when many consumers are struggling to pay their energy bills, the regulator may be under pressure to hold back utility companies’ returns. However, we believe the risk is lower for the grid operators given the essential nature of their business and the fact that the grid only accounts for a small percentage of an energy bill.

Other than regulatory risk, the stock may also be negatively impacted by a rise in gilt yields, the threat of a cyberattack, supply chain and labour inflation risk, NIMBYism, and weakness of the US dollar.

Following the recent strong performance of the shares, the dividend yield has dropped below both the UK base rate and 10-year gilt yield, implying the shares are now being viewed more as a growth utility than a bond proxy.

Source: Bloomberg