Morning Note: Market News and Updates from Imperial Brands and Barrick Mining.

Market News

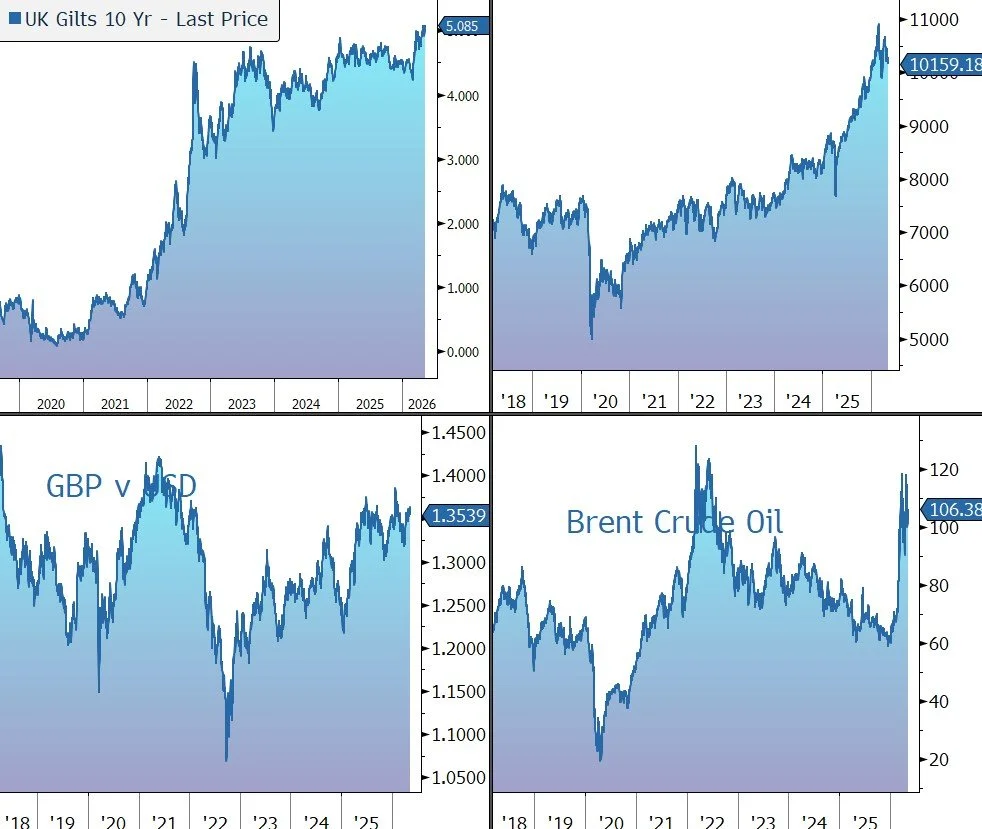

Oil rose after President Donald Trump cast doubt on the Iran ceasefire, fueling concern that the closure of the Strait of Hormuz will be prolonged. Separately, the WSJ reported that the UAE had been secretly carrying out attacks on Iran. Brent Crude trades at $106 a barrel, while the yield on the US 10-year Treasury rose to 4.42%.

Gold trades at $4,700 an ounce. Indian Prime Minister Narendra Modi's call to avoid gold purchases for a year to help protect foreign exchange reserves fuelled concerns of higher import tariffs on the metal, sending shares of Indian jewellery retailers lower.

US equities rose slightly last night – S&P 500 (+0.2%); Nasdaq (+0.1%). In Asia this morning, equities were mixed: Nikkei 225 (+0.5%); Hang Seng (-0.1%); Shanghai Composite (-0.3%). The Korean Kospi saw wild swings — shedding more than $300bn in value over 97 minutes, and then paring losses — after a top South Korean official floated the idea of a ‘citizen dividend’ using AI profits but later clarified it would be funded by excess profits

The FTSE 100 is currently down 1.0% to 10,159, while Sterling trades at $1.3515 and €1.1505. UK 10-year gilt yields climbed above 5.1%, reaching their highest point since July 2008, as political instability in the UK deepens. Over 70 Labour MPs have urged Prime Minister Keir Starmer to resign following the party’s poor performance in last week’s local elections, with investors worrying that a leadership change could lead to higher fiscal spending in an effort to regain voter support.

Source: Bloomberg

Company News

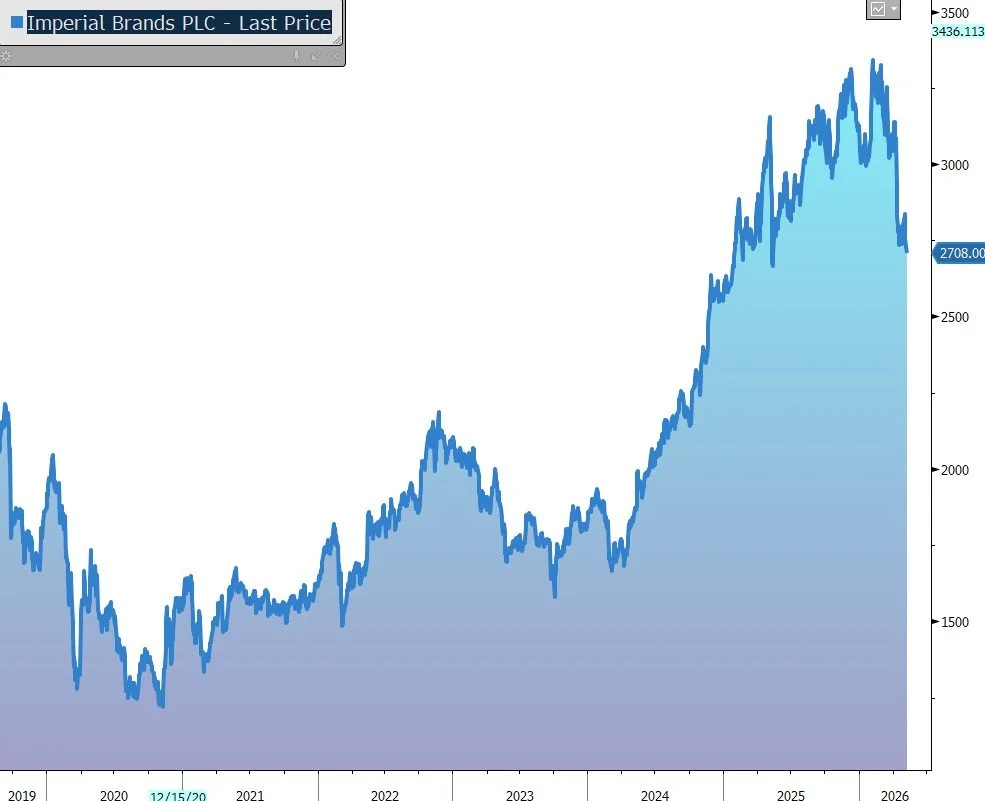

Imperial Brands has released results for the half-year to 31 March 2026 which were in line with market expectations, supported by higher tobacco prices and growing demand for smoking alternatives. As expected, the company highlighted a slight loss of share in its top-5 markets. The company remains on track to deliver its guidance for the financial year to 30 September 2026. The shares have been a good medium-term performer and remain attractive given the level of prospective shareholder returns. Although the admission of market share loss has hit the shares since last month’s trading update, the outlook remains attractive. In response to today’s update, they are up 1%.

Imperial Brands manufactures and sells cigarettes, fine cut tobacco, smokeless tobacco, cigars, and next generation products. The main brands include Winston, Davidoff, L&B, West, Gauloises, JPS, Rizla, and blu.

The 2030 strategy builds on the strong foundations of the previous five-year plan. As a ‘distinctive challenger,’ the company has two focused objectives:

· Drive sustainable value in combustibles where the company will continue to focus on its five largest markets – the US, Germany, the UK, Australia, and Spain – which represent 70% of adjusted tobacco operating profit. Within these markets, Imperial has identified specific areas for further investment by category, brand, and sales channel. Imperial has slightly tilted its strategic objective, highlighting that while market share remains important, the company will continue to balance share and value. Having successfully stabilised aggregate share across its top five markets, the company will continue to evolve its approach to reflect changing market dynamics and a focus on more profitable segments, to deliver long-term, sustainable value creation. Outside the top five markets, the company will apply the same performance-driven, consumer-led approach so that they make a greater contribution to overall performance over the next five years. Most notable is the group’s African cluster which now accounts for 10% of operating profit and is bigger than UK, Spain, and Australia.

· Build scale in next generation products (NGP) – Imperial has a strong platform for a fast growing and agile NGP business with credible brands in all three categories (vaping, heated tobacco, and modern oral) and differentiated products available in all material markets where the group has distribution routes. Imperial will retain disciplined investment and market entry criteria as it builds a meaningful business with additional growth opportunities and strong profit and cash performance. For now, however, the business remains loss-making with the company targeting a breakeven run-rate by early 2028.

To support the delivery of its strategy, the company has identified further opportunities to create a simpler, leaner, and more agile organisation. These initiatives are expected to generate annualised savings of £320m by 2030, the majority of which will be reinvested to support growth. The anticipated cash cost of these initiatives is £600m, £500m of which will fall in FY2027 and FY2028. The company is to cease production at its Langenhagen factory in Germany, either via a sale of the site to a third party or closure of the factory. Costs expected in relation to this process are within the group’s current guidance.

A strategic partnership with Capgemini gives the company access to new capabilities to support growth, including data-led insights and agentic AI, that will enable the business to capture new commercial opportunities and deliver efficiencies

The new strategy will support the company’s medium-term guidance for growth on a constant currency basis: low-single digit tobacco net revenue growth and double-digit NGP net revenue growth; adjusted operating profit growth of around 3%-5%; adjusted EPS growth at a high-single digit rate, supported by a continued reduction in share count through the share buyback (see below); and annual free cash flow generation of between £2.2bn and £3.0bn.

Back to today’s update. In the half-year to 31 March 2026, tobacco and NGP net revenue grew by 1.8% at constant current to £3,729m, driven by robust tobacco pricing and NGP innovation. This was in line with guidance for low-single-digit percent growth.

Tobacco net revenue grew by 1.5%, driven by robust price/mix (+3.0%). Volumes fell by 1.5% (to 85.7bn sticks equivalent), with growth in the group’s AAACE region offset by declines in Europe and the Americas.

As expected, the company suffered a small (16 basis points) aggregate share reduction across the top five markets in the period – Germany (+5bps), Australia (-55bps), the US (20bps), Spain (-20bps), the UK (-55bps). The company has argued they are intentionally walking away from low-margin volume to focus on profitable segments. The market’s concern – and the reason for the negative share price reaction at the time of last month’s trading update – is that share is being lost due to increased competition.

NGP net revenue grew by 7.5% at constant currency, with performance driven by double-digit growth in AAACE and Europe. The company grow share in all three categories of vaping, heated tobacco, and modern oral.

Adjusted operating profit rose by 0.6% at constant currency to £1,644m. The performance reflects a strong performance in Europe and the wider AAACE portfolio, offset by US, Australia, and Logista (-3.0%), the Spanish-based distribution business in which Imperial has a 50.01% stake. NGP operating losses were moderately higher at £40m. Profit growth is expected to accelerate in the group’s second half, underpinned by the usual flow through of embedded combustible pricing taken in the first half and the phasing of investment.

Adjusted EPS grew by 5.3% at constant currency to 127.7p. Growth was supported by the ongoing share buyback programme (see below), partly offset by higher adjusted finance and tax costs as well as increased minority interests, given strong growth in some of the group’s African markets.

The capital allocation framework includes investment in organic growth initiatives in combustibles and NGP, while continuing to evaluate opportunities for small bolt-on acquisitions, which will be focused on enhancing NGP capabilities. The capital intensity of the business is low with modest annual capex needs of £300m-£350m – last year it was £338m.

The 12-month free cash flow of £2.6bn reflected strong cash conversion of 98%. Following the decision of the Supreme Court of Delaware in December 2025, a payment of $150m was made to R J Reynolds in the first half of the financial year, with the remaining $162m to be made in roughly equal instalments over the next three years.

The company aims to maintain a strong and efficient balance sheet to support its investment grade credit rating with a leverage target at the lower end of 2.0-2.5 times net debt to EBITDA. Over the last six months, adjusted net debt has risen from £8.4bn to £10.5bn to leave financial gearing of 2.4x, in line with target. As a result of the improved performance and credit profile, the group’s lenders have removed the leverage and interest cover financial covenants that were a condition of the previous facilities.

The company has a progressive dividend policy to provide a reliable, consistent cash return to shareholders. Dividends per share will grow annually considering underlying business performance. The half-year dividend has been increased by 4%. A similar rate in growth in the full year would generate a yield of 6.2%.

Surplus capital is being returned to shareholders via an ‘evergreen’ (i.e. ongoing) share buyback over the five years to FY2030. The board will determine the quantum of future buybacks on an annual basis, in line with current practice, but has said they will be ‘material’. For FY2026, a £1.45bn programme is expected to complete no later than 28 October 2026, with £809m repurchased in the half-year. Taking dividends and buyback together, the company expects its capital return to shareholders will exceed £2.7bn in FY2026, representing more than 10% of the current market capitalisation.

Although tensions in the Middle East have led to a more uncertain macroeconomic environment, Imperial has not seen a material impact to date. The company has reiterated its guidance for the financial year to 30 September 2026 which is in line with its medium-term targets. On a constant currency basis, the group expects to deliver low-single-digit tobacco and double-digit NGP net revenue growth. Tobacco pricing will continue to more than offset cigarette volume declines. Adjusted operating profit is expected to grow in the 3% to 5% range, on a constant currency basis. In line with previous years, performance will be weighted to the second half of the year because of the phasing of combustible pricing and investment. After restructuring costs, free cash flow is expected to be at least £2.2bn in FY2026. Growth in operating profit combined with the impact of the ongoing share buyback is expected to result in at least high-single-digit adjusted EPS growth for the full year.

Although the conflict in the Middle East has resulted in a more uncertain geopolitical and macro environment, there has been no material business impact to date.

Source: Bloomberg

Yesterday, Barrick Mining Corporation released Q1 results which were ahead of market expectations. Strong commodity prices, production ahead of guidance, and controlled costs all helped to generate significant free cash flow. This allowed the company to initiate a new $3.0bn share repurchase programme, while also making progress on key growth projects. The shares have been a very strong performer over the last year, although they have seen profit-taking of late on the back of the falling gold price. In response to this update, the stock rose by 9%.

Barrick Mining Corp. is the world’s second largest gold producer. The company was created following the 2018 merger of Barrick Gold and Randgold Resources. In addition, in 2019, the group improved its portfolio through the formation of the Nevada Gold Mines joint venture with Newmont, providing exposure to the single largest gold-mining complex in the world.

As a result, the group operates mines and projects in 17 countries in North and South America, Africa, Papua New Guinea, and Saudi Arabia. It now owns six of the world’s Top 10 Tier-One gold assets with the largest reserve base among its senior gold peers. At the end of 2025, attributable gold reserves were 85m ounces, with 10-year mine plans based on reserves and geologically understood resource extensions. The group doubled the gold resource at the Fourmile project in Nevada with further increases expected in 2026. Non-core assets are being sold, including the $1bn disposal of its 50% interest in the Donlin Gold Project.

In order to unlock further shareholder value, the company is undertaking an IPO of its North American gold assets, expected to be completed by the end of 2026. The separate unit will house Barrick’s interests in Nevada Gold Mines, Pueblo Viejo, and its wholly owned Fourmile project in Nevada. Barrick plans to retain a controlling stake in the new entity following the listing.

Overall, Barrick provides an attractive way to gain exposure to the gold price, albeit with the operational and political risks that come with a production company. The company is also well positioned to capitalise on global decarbonisation trends driving the long-term fundamental strength of copper with two world-class projects set to deliver into a rising price and demand market.

In the first quarter of 2026, revenue grew by 67% to $5.2bn, well above the $4.5bn forecast. Revenue was 13% lower than the previous quarter. Adjusted net EPS rose by 180% to 98c, well above the market consensus of 78c.

Gold production was down 5% to 719k ounces. However, this was above the guidance of 640k-680k ounces, driven by strong performances at NGM and Veladero, and the ramp-up at Loulo-Gounkoto.

The gold price has rallied sharply over the last year, driven by global geopolitical and macro-economic uncertainty, exacerbated by the Trump administration, continued central bank bullion buying, and concern over fiat currency debasement. More recently, however, the price has fallen back from its January peak of c. $5,600 an ounce due to the removal of speculative froth and profit-taking since the beginning of the Middle East conflict. During Q1, Barrick realised a gold price of $4,823 an ounce, up 66% on last year.

Barrick has the lowest total cash cost position among its senior gold peers – in the latest quarter, all-in sustaining costs were down 4% to $1,708/ounce. This was lower than expected and driven by efficiencies in mining and processing.

Group copper production rose by 11% to 49k tonnes in the quarter, in line with plan. The realised price was up 28% to $5.79/pound in the quarter, with all-in sustaining costs up 20% to $3.67/pound.

The group generated strong free cash flow during the quarter of $1,575m, up 320%, and ended the period with a net cash position of $2.4bn. This leaves the group with the flexibility to manage its business and take advantage of new opportunities independent of the vagaries of the capital markets. Attributable capital investment rose by 20% in Q1 to $755m.

The dividend policy targets a total payout of 50% of attributable free cash flow, including a fixed quarterly base dividend of 17.5c per share, plus performance year-end top-up. Barrick has also announced a new $3.0bn share buyback programme.

The company reiterated its guidance for 2026: Gold production expected to increase sequentially throughout the year, with Q2 gold production of 730k–770k ounces. Full year production (2.90m-3.25m ounces) and cost guidance ($1,760-$1,950 an ounce) remains unchanged. Copper guidance – production of 190kt–220kt and all-in sustaining costs of $3.45-$3.75 a pound – also remains unchanged.

For 2026, the group is assuming an average gold price of $4,500/ounce in 2026 – it is currently $4,700/ounce. A $100/ounce move has a $450m impact on cash flow. The group is assuming an average copper price of $5.50/pound – it is currently $6.35/pound – and discloses that a 25c/pound move has a $120m impact on cash flow.

Source: Bloomberg