Morning Note: Market News and an Update from Sodexo.

Market News

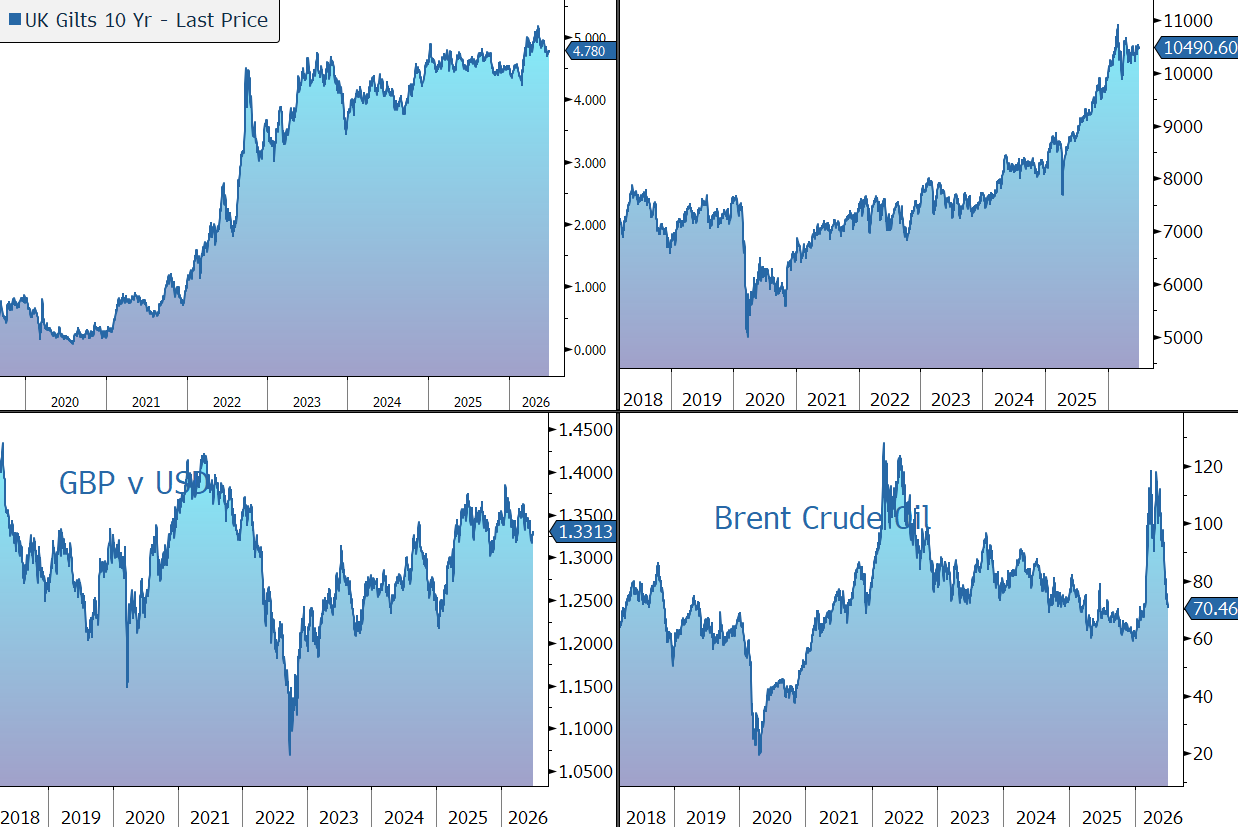

Gold strengthened to $4,070 an ounce as Federal Reserve Chair Kevin Warsh said inflation expectations had eased over the past month, suggesting there was no urgency to raise interest rates. Investors now await the non-farm payrolls report later today for fresh insights into labour market conditions and the Fed’s policy outlook. The forecast is for a 113,000 gain. The yield on the US 10-year Treasury is 4.48%.

Brent Crude slipped below $71 a barrel, reaching its lowest level since late February as oil shipments through the Strait of Hormuz continued to increase and investors welcomed signs of progress in indirect US-Iran talks. UK diesel costs tumbled by the most on record in June, a sign that war-led inflationary shocks are unwinding.

US equities fell last night – S&P 500 (-0.2%); Nasdaq (-0.7%) – after a sell-off in chipmakers rekindled concerns that the AI-driven rally had outpaced fundamentals. OpenAI has begun preliminary discussions about giving the US government a 5% stake, the FT reported.

In Asia this morning, South Korean stocks led declines: Kospi (-6%); Nikkei 225 (-2.5%); Shanghai Composite (-2.0%). The yen edged higher after Reuters reported Japanese authorities will stop telegraphing intervention in advance to take more abrupt action against speculators.

The FTSE 100 is currently little changed at 10,491, while Sterling trades at $1.3320 and €1.168. The Bank of England is pushing ahead with its plan to limit how much debt hedge funds may use when trading UK government bonds, the FT reported.

The ECB’s Ulo Kaasik suggested that an additional rate hike is a “reasonable” expectation, while Yannis Stournaras believes it’s “perhaps good to stay where we are for some time.” The retreat in oil prices since US-Iran peace talks began and the drop in inflation to 2.8% in June offers a welcome reprieve for the euro-area economy.

Source: Bloomberg

Company News

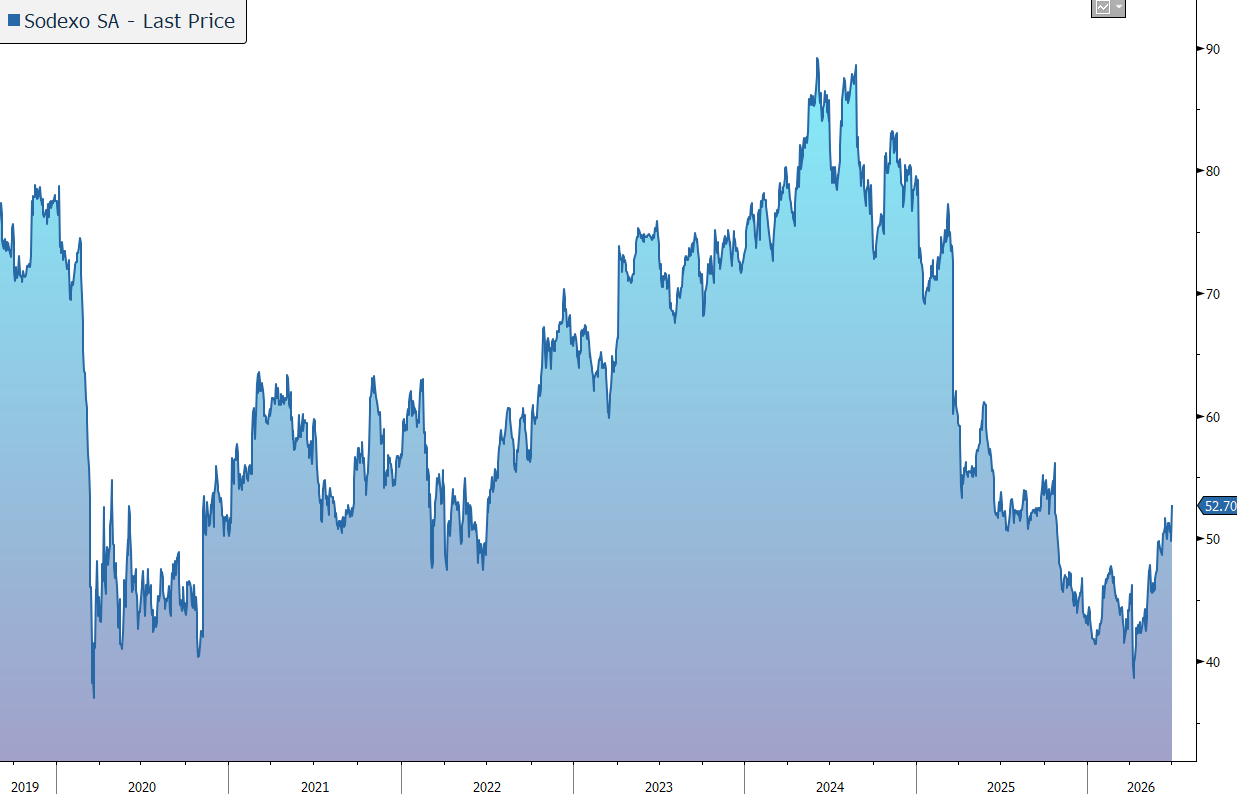

Sodexo has announced results for the third quarter of its financial year to end August 2026 (FY26). Performance came in above market expectations, reflecting resilient demand, focused execution, and strong performance at its premium brand that handles sports, leisure, culture, and major events hospitality. In response, the company has nudged up its full-year revenue guidance and the shares are 7% higher in early trading.

Sodexo is a global supplier of food services and associated facilities management (FM) support functions. The company generates annual sales of around €24bn and is listed on the French CAC 40.

Earlier in the year, the group’s new CEO said the company had underperformed the market and its main competitors. The root causes have been building over time and relate primarily to under-investment and execution: commercial intensity, decision-making and prioritisation, and consistency in delivery. Following a thorough review of its contracts and assets, the company disclosed several short-term financial implications.

Sodexo is planning to present an execution agenda and mid-term ambitions at an Investor Update on 16 July. In the meantime, the company is moving with urgency on its action plan to return to growth, restore competitiveness, and strengthen execution capabilities. So far, the company is seeing encouraging progress in its commercial momentum.

In the three months to end May 2026, revenue rose by 0.9% to €6,174m. Stripping out the impact of currency (-2.5%) and M&A (+1.4%), organic growth was 2.0%. Growth was above expectations, reflecting resilient demand across the business and the continued focus on execution. Although the company entered the quarter with a cautious view of the operating environment, management was able to mitigate a number of risks by capturing opportunities across the portfolio, particularly at Sodexo Live! North America, the group’s premium brand that handles sports, leisure, culture, and major events hospitality.

In North America, revenue fell by 0.1% in organic terms, held back by prior contract losses in Education. Healthcare & Seniors continued to deliver solid growth, supported by new contract wins, and high activity levels across stadiums, conference centres, and airport lounges.

Europe was up 0.6% organically, reflecting the prior loss of a large global FM contract in Business & Administration and continued softer activity in Education. In the Rest of the World, growth was 10.6%, primarily supported by new contract ramp-ups, mainly in Energy & Resources, with broad-based growth across geographies.

As this was a revenue update, there was no commentary on profitability. As a reminder, the company is currently suffering from a decline in margins, driven by operational challenges and mix effects, lower operating leverage linked to softer growth dynamics and the acceleration of investments to strengthen execution. It also reflects the effects of the review of contracts and assets, including specific contract-related provisions, in the light of their actual performance and current market conditions.

Apart from the seasonal changes in working capital, there were no material changes in the group's financial position as of 31 May 2026. At the last balance sheet date (February 2026), net debt was €3.6bn, with the net debt ratio of 2.7x EBITDA. As planned, the group repaid its $328m bond maturing in April 2026 using available cash, simplifying its debt structure and maintaining a balanced maturity profile.

The company has upped its revenue guidance for the full year while maintaining a prudent view of the external environment:

· organic revenue growth is now expected to be between 1.2% and 1.5% (vs. 0.5% and 1.0% previously).

· underlying operating profit margin is still expected to be between 3.2% and 3.4%.

· considering the level of EBITDA implied by the guidance, the group expects to end FY August 2026 with a net debt to EBITDA ratio above its target range of 1x-2x.

Source: Bloomberg