Morning Note: Market News and an Update from Constellation Brands.

Market News

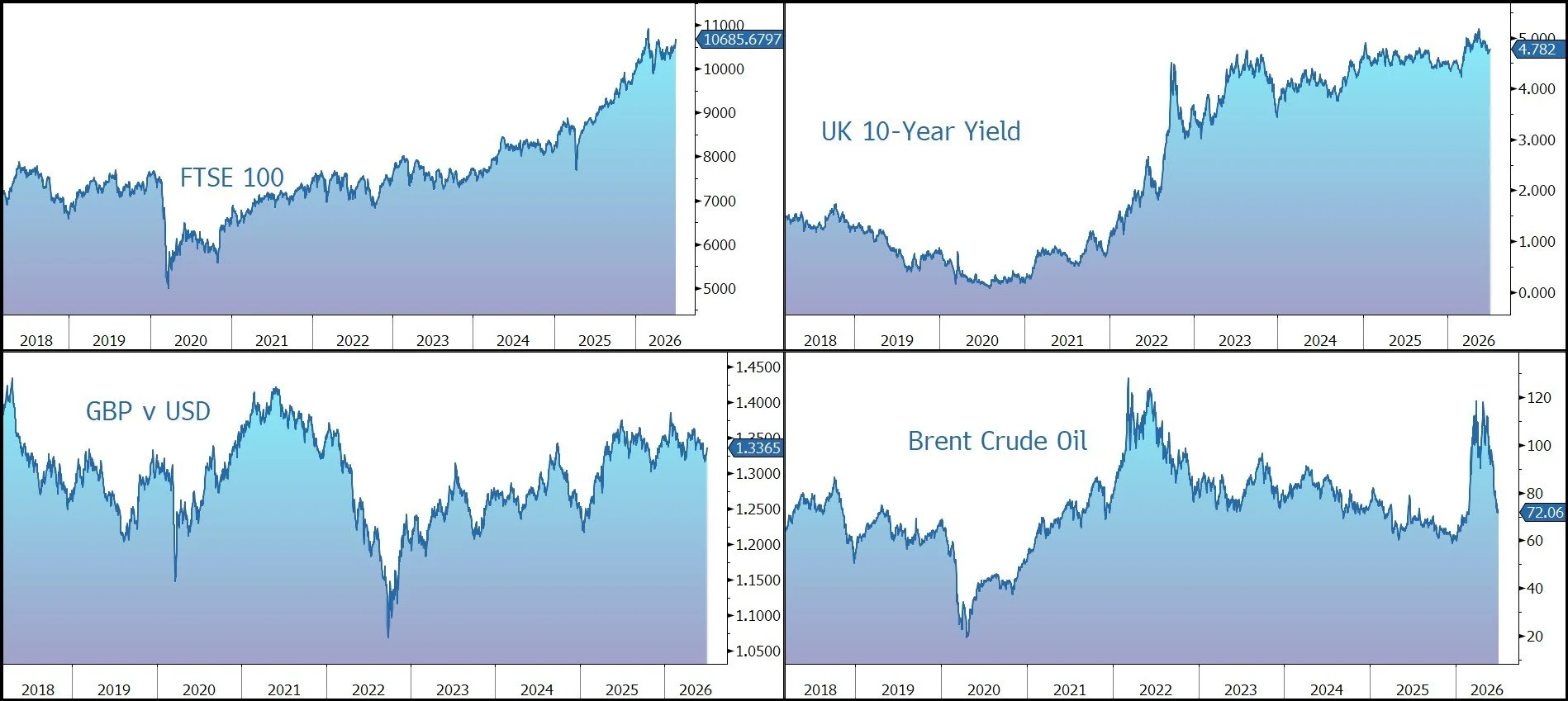

The US dollar fell as markets scaled back expectations for Federal Reserve rate hikes following weaker-than-expected US jobs data. The economy added just 57,000 jobs in June, the fewest in four months and well below the 110,000 forecast, with leisure and hospitality shedding 61,000 jobs despite a World Cup tourism boost. The unemployment rate unexpectedly fell to 4.2% as workers left the labour force, while wage growth edged up to 3.5% year-over-year. Fed funds futures now price in less than a 50% chance of a September rate hike, down from 67% before the report. Gold jumped 2% to $4,170 an ounce, while the yield on the US 10-year Treasury is 4.49%.

Brent Crude held steady around $72 a barrel, as shipping through the Strait of Hormuz continued to recover amid progress in US-Iran talks. Saudi Arabia’s crude exports have rebounded to about 90% of their pre-war levels as more tankers successfully transit the key waterway, signalling that regional oil supply is gradually normalising. President Trump told CNBC the US is still negotiating with Iran, but that he thinks “they’ve agreed to just about everything we need.” US officials believed that Israel may have been plotting to kill Iran’s top negotiators while talks were ongoing to reach an interim peace deal, the NYT reported.

US equities were mixed last night, with the Dow Jones up 1.1% (at an all-time high), the S&P 500 flat, and the Nasdaq down 0.8%. Chipmaker stocks fell for a second day as investors questioned whether AI optimism had pushed valuations beyond reasonable levels. The US is closed for a holiday today. In Asia this morning, stocks rebounded: Nikkei 225 (+1.5%); Hang Seng (+1.3%); Shanghai Composite (+0.4%). The yen traded near 161 per dollar after jumping nearly 1%, as Finance Minister Satsuki Katayama reiterated that authorities stand ready to intervene at any time to support the currency.

The FTSE 100 is currently 0.3% higher at 10,686, while Sterling trades at $1.3366 and €1.1670. Andy Burnham’s delay in announcing key personnel appointments has raised concerns among some Labour Party members that he risks making the same mistake that contributed to Keir Starmer’s downfall — failing to get sufficiently ready for government.

Source: Bloomberg

Company News

Earlier in the week, Constellation Brands released results for the first quarter of its financial year ending February 2027. Despite a discerning and value-conscious consumer environment, the company grew organic net sales. Guidance for the full year has been reiterated and, in response, the US-listed shares were marked up by 4%.

Constellation Brands is a leading international producer and marketer of beer, wine, and spirits, with a portfolio of higher-end brands including Corona and Modelo. Part of the group’s strategy is to supplement organic growth with bolt-on acquisitions, and to focus on premium, margin-accretive, growth opportunities. As a part of that process, the wine business has been restructuring and downsized via disposals. The group recently appointed a new CEO.

While the company continues to navigate a challenging socioeconomic environment that has dampened consumer demand, the results for the latest quarter were slightly better than expected.

During the three months to 31 May 2026, organic net sales rose by 3% to $2.43bn, slightly better than the market expectation of $2.39bn. Comparable EPS was up 7% to $3.43, above the market forecast of $3.20.

By division, the beer business increased net sales by 2% to $2,283m, driven by a 1.8% increase in shipment volumes and continued favourable pricing. Depletions only fell by 0.3%, as declines for Modelo Especial of approximately 2% and Corona Extra of over 5% were partially offset by growth from Pacifico, Victoria, and the Modelo Chelada brands. The beer business continued to lead the category in dollar share gains, outperforming the total beer category by nearly three percentage points in year-over-year dollar sales.

The beer operating margin remained relatively flat year-over-year at 39.0% as growth in shipment volumes and favourable pricing were offset by unfavourable mix and higher marketing and other SG&A spend.

In Wine & Spirits, sales rose by 8% in organic terms to $149m, driven by a 7.7% increase in organic shipment volumes. The unit outpaced the corresponding higher-end wine segment in both dollar sales and volume sales performance. During the latest quarter, depletions were up 6.6%. Although the wine division is still loss-making, the operating margin did improve by 140 basis points to -0.7% as growth in organic shipment volumes and lower marketing and other SG&A spend were partially offset by the impact of the 2025 divestitures.

The overall business is cash generative, with free cash flow up 9% to $485m in the quarter. Net debt gearing remains around the group’s target of 3.0x. The group has returned $324m to shareholders in share repurchases in the year to date and increased its quarterly dividend by 1% to $1.03.

The company is expanding its beer business in Mexico and expects to spend $3.0bn between FY2025 and FY2028 to support the future growth of the core, high-end Mexican beer portfolio with modular additions at existing facilities and a third brewery site at Veracruz.

Looking to the full year, group organic net sales growth is expected to come in between -1% and +1%, with Beer and Wine & Spirits both in the same range. Target comparable EPS of $11.20-$11.90 has been confirmed (vs. $11.82 last year), as has free cash flow of $1.6bn-$1.7bn.

Source: Bloomberg