Morning Note: Market News and an Update from Nike.

Market News

The yield on the 10-year US Treasury note is trading at around 4.46% after climbing 10 basis points yesterday, as signs of a resilient economy reinforced expectations of a hawkish Federal Reserve. Data showed US job openings rose to a two-year high in May, indicating labour demand remained strong despite signs of softer hiring. Markets are now pricing in at least one Fed rate hike this year, with the first potentially coming as early as September. Gold slipped below $4,000 an ounce, trading near its lowest level in almost eight months, as the threat of higher rates reduces the appeal of the non-interest-bearing metal.

Traders are now awaiting key speeches from a number of central bankers, including Federal Reserve Chairman Kevin Warsh, and tomorrow’s US non-farm payrolls data.

Brent Crude steadied above $73 a barrel after posting its steepest quarterly decline since 2020, as investors awaited updates on ongoing peace talks between the US and Iran in Doha, with both sides seeking to ease tensions over the Strait of Hormuz following recent clashes. Washington and Tehran are working toward a lasting resolution to the conflict, although Iran has maintained its position on controlling maritime traffic through the strategic waterway. Tehran’s top negotiator said the release of $12bn in frozen Iranian assets is underway.

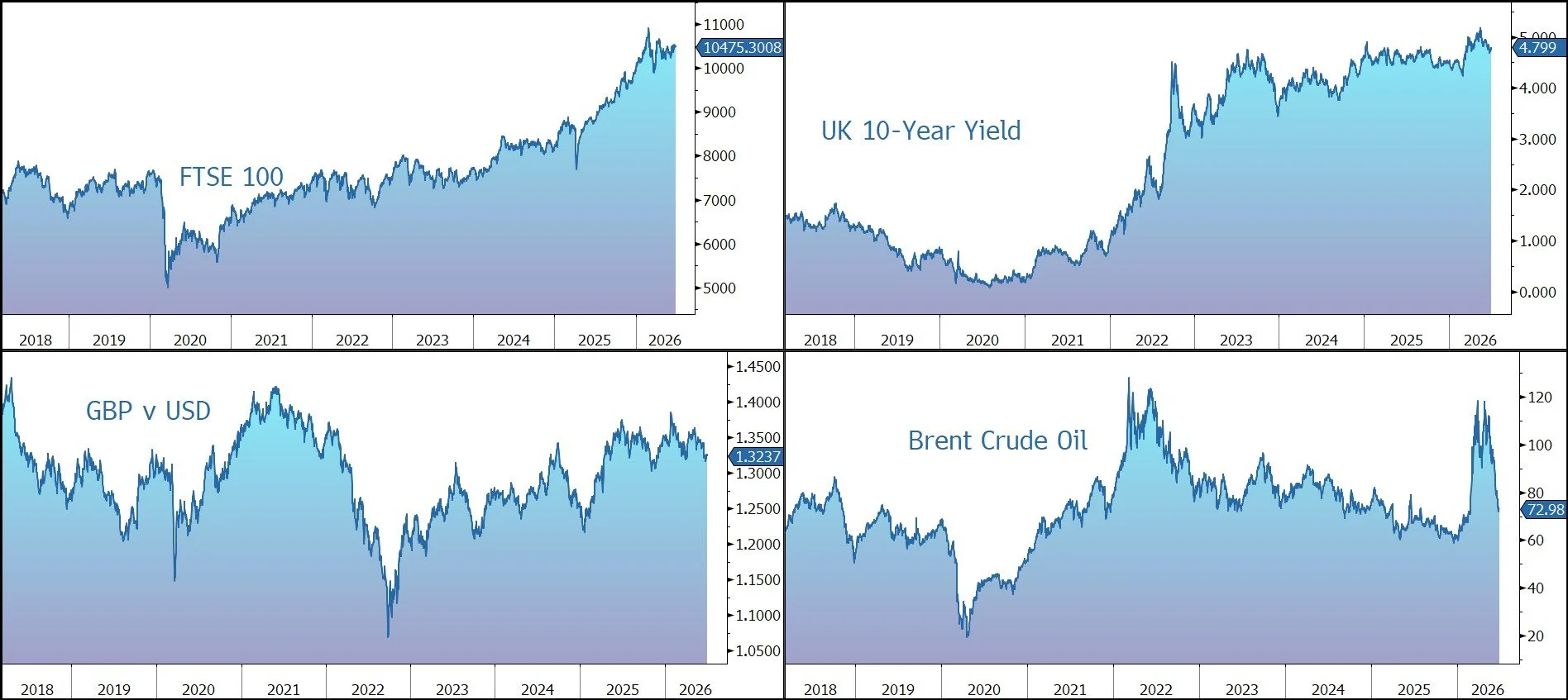

US equities rose last night – S&P 500 (+0.8%); Nasdaq (+1.5%) – with the positive momentum continuing in Asia this morning: Nikkei 225 (+0.5%); Shanghai Composite (+0.2%). The FTSE 100 is currently little changed at 10,495, while Sterling trades at $1.3240 and €1.1615.

Source: Bloomberg

Company News

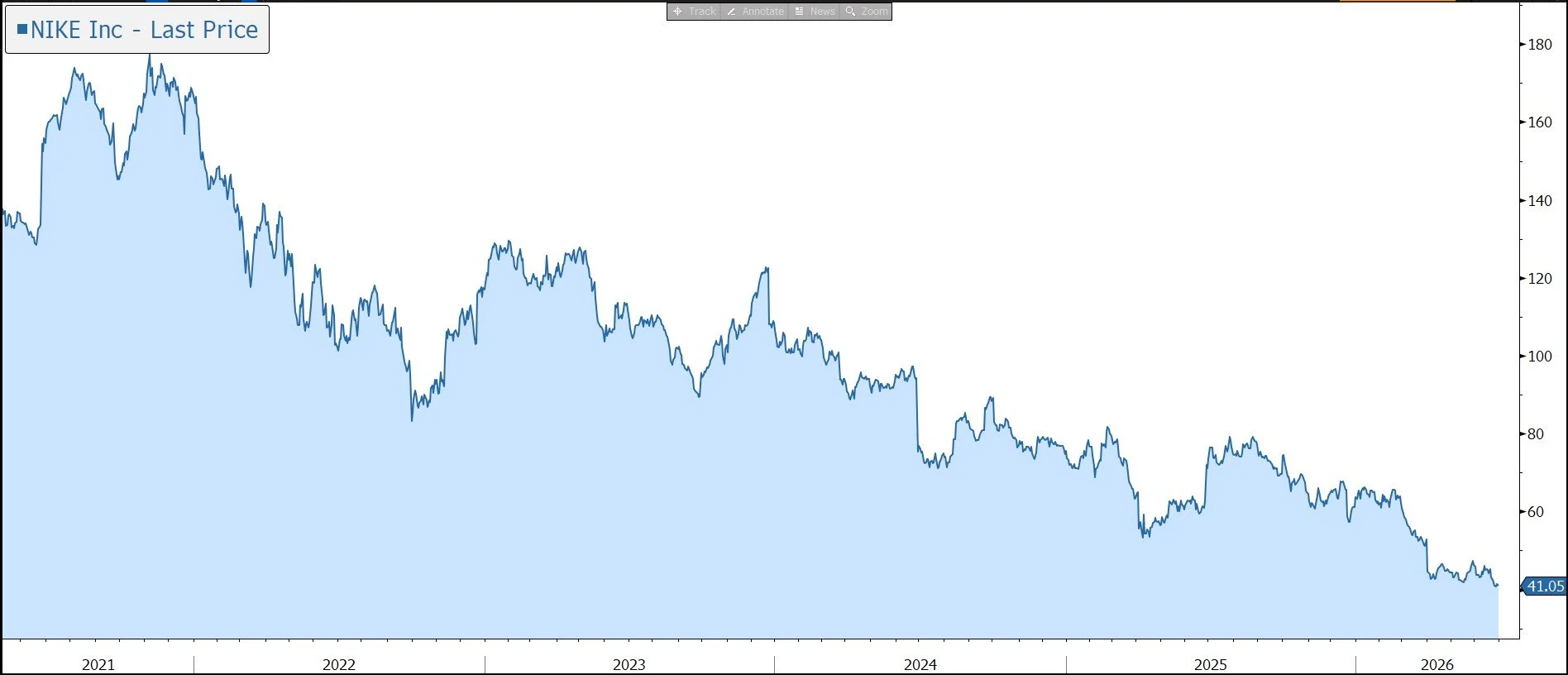

Last night, Nike released results for the financial year to end May 2026. As hinted in last week’s update, the figures were broadly in line with expectations despite an increasingly challenging operating environment. Progress continues in the areas the group prioritised first in its recovery plan: Running, Wholesale and North America. Progress elsewhere – notably Greater China and Sportswear – remains slow, with the recovery taking longer than management would like. Earnings guidance for the remainder of the calendar year has been reiterated albeit the composition has shifted, with revenue lower and gross margin higher. The company continues to deliberately prioritise long-term brand and marketplace health over medium-term earnings growth, meaning investors need to remain patient. In response to the results, the shares were marked down by 2.5% after hours.

Nike is the world’s leading sports footwear and apparel company. Its products are sold at various sporting goods retailers, as well as company-operated stores and websites. In the long term, the company should be well placed to benefit from increased consumer demand for healthier living. Nike has a strong brand and an impressive track record of product innovation.

However, over recent years, the company made a number of strategic errors, the impact of which was exacerbated by a subdued macroeconomic backdrop, intense promotional activity, and the emergence of competition from new brands such as On and Deckers’ Hoka. In particular, there was:

· an over-reliance on key ‘classic’ product franchises (Air Force 1, Air Jordan 1, and Dunk) at the expense of new innovation.

· an overly aggressive push away from a wholesale-driven model to a direct (in particular digital) model which alienated third-party retailers who are essential to elevate the brand and grow the total marketplace.

In response, former senior executive (and 32-year Nike veteran) Elliott Hill returned to the company as CEO. Given that much of the recent corporate malaise was down to poor management/strategy, the hope is that Nike will return to its roots and the culture that made it so successful. The plan is to ‘lead with sport and put the athlete at the centre of every decision, leveraging athlete insights to accelerate innovation, design, and product creation’. It remains unclear how much Nike’s sportswear business still needs to shrink.

The group has accelerated its multi-year cycle of innovation and pulled forward several new products, especially in high-volume areas like running, training, football, sportswear, and Jordan. Inventory cleaning has been aggressive, removing stale product from the market although this has further to go. There has been a refocus on the wholesale market and a shift at Nike Digital to a full-price model, reducing the percentage of the business driven by promotional activity. Nike is also being aggressive in sports marketing across leagues, associations, teams, and individuals.

Costs are being reduced as the company right-sizes the business. In April, Nike announced a sweeping internal shakeup to simplify its business model, with roughly 1,400 corporate roles cut, with the majority hitting its Global Technology division.

Overall, immediate action has been taken in areas that will make the most near-term impact. Although early results have been encouraging, the company has admitted change at scale takes time with a negative impact on sales and gross margin. Furthermore, progress has not been linear as parts of the business recover on different timelines.

Last week, the company announced a planned CFO transition in which David Denton, currently CFO of Pfizer, will join the company in August.

Back to the latest results. The company highlighted that it is operating in a more complex macro environment with pressure on consumer spending. Against that backdrop, management were encouraged by clear signals of progress. This includes five quarters of growth in Running, a rebuild of the wholesale relationship, and lower levels of discounting at Nike Digital. The focus is now on consistent execution, improved profitability, and scaling the business to realise its full potential.

In the financial year to 31 May 2026, revenue fell by 2% on a currency-neutral basis to $46.4bn. In the final three months of the financial year, revenue fell 4% at $11.0bn. This was at the lower end of the ‘down 2%-4%’ guidance range but just above the market estimate of $10.85bn.

Nike Brand sales were down 1% in the year to $45.2bn and by 3% in Q4. The Converse brand fell by 32% to $1.2bn in the year and by 34% in Q4.

By region in the final quarter, Nike Brand revenue rose by 3% in North America, the group’s largest unit. As expected, headwinds in Greater China persisted, with revenue down by 17% in the final quarter, reflecting reduced sell-in, as well as accelerated actions to clean up the marketplace. Remedial actions are expected to continue throughout fiscal 2027 and remain a headwind to revenue growth. Elsewhere, revenue fell by 6% in Europe, Middle East, & Africa (EMEA) and by 1% in Asia Pacific & Latin America (APLA).

Nike Brand sales are split into Direct sales (both online and through Nike-owned stores) and wholesale revenue from third party retailers. During the final quarter, Nike Direct sales fell by 9% to $4.1bn, with digital down 12% and stores 7%. Wholesale rose by 1% to $6.6bn

All categories were in decline: Footwear (-4%); Apparel (-1%); Equipment (-5%).

The company continues to see pressure from tariffs and its efforts to clear out aged inventory on its margins. During the last quarter, the gross margin increased by 890 basis points to 49.2%, including a 900 basis point benefit due to the expected recovery of tariffs. The underlying 10 basis points decline to 40.2% was better than guidance for a 25-75 basis points decline. For the full year, the gross margin was 40.8% ex the tariffs.

Selling and administrative expenses fell by 2%, with demand creation expense (i.e., marketing) down 4%. Operating overhead expense fell 1%, primarily due to lower other administrative costs, partially offset by unfavourable changes in currency and higher wage-related expense. Full-year EPS was 158c (ex-tariff refund), versus the consensus forecast of 149c. In Q4, excluding the 52c tariff benefit, EPS came in at 20c, versus the market forecast of 13c.

Inventories remain elevated across all geographies, albeit flat at $7.5bn, primarily reflecting an increase in units, offset by shifts in product mix. The full inventory clean is expected by the end of the calendar year.

Nike’s balance sheet remains strong – with a $1bn net cash balance. During the year, the group returned just under $2.4bn to shareholders through dividends, 5% more than last year. There were also share repurchases of $123m as part of the company’s four-year, $18bn programme.

The company is planning to host an investor day in November at which it will lay out new medium-term targets. In the meantime, guidance has been provided for the rest of the calendar year. The company still expects EPS to be ‘flattish’, although the composition has shifted. The outlook for revenue has moderated – the current quarter is expected to be down in the low- to mid-single digits, while the November quarter will see a slight sequential deceleration due to tough year-on-year comparatives. On a positive note, progress on the turnaround in the gross margin has been brought forward by a quarter, with the current quarter now expected to see expansion.

Source: Bloomberg