Morning Note: Market News and an Update from NVIDIA.

Market News

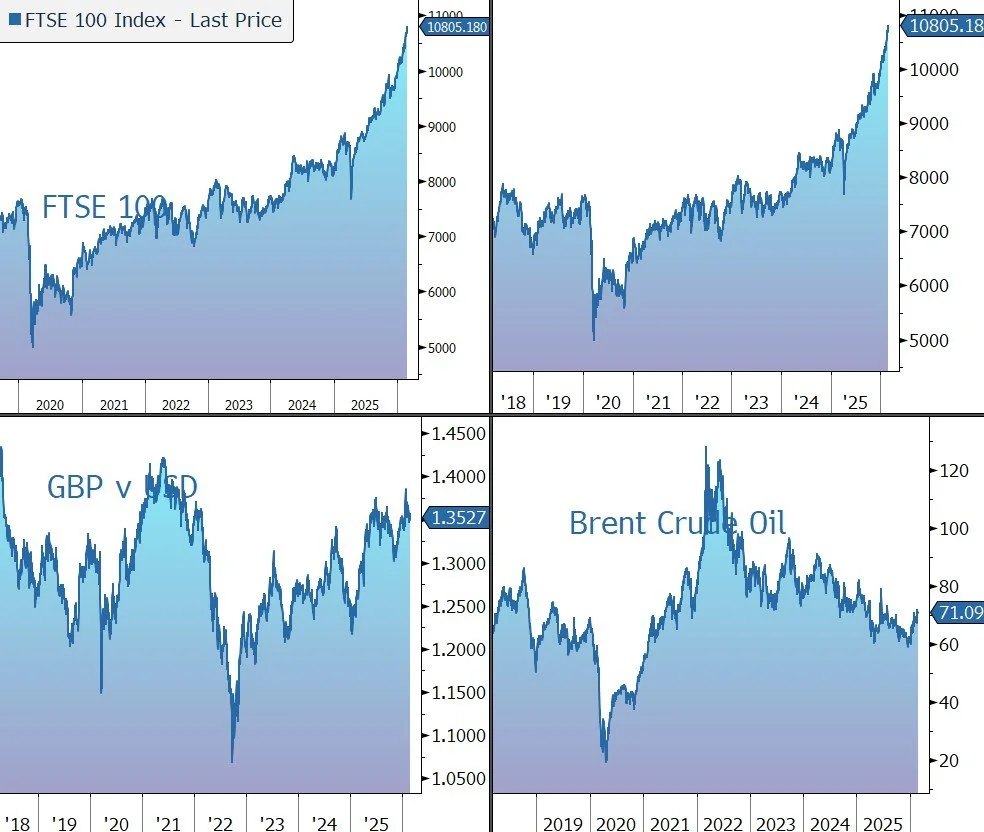

The 10-year Treasury yield slipped to 4.05% as uncertainty over US tariffs bolstered demand for safe-haven debt. US Trade Representative Jamieson Greer indicated that tariff rates for certain countries could rise to 15% or higher from the recently implemented 10%, without providing additional details. Gold sits at $5,180 an ounce, extending gains from the previous session and hovering near an almost four-week high.

The US imposed sanctions on more than 30 entities that support Iranian oil and weapons sales ahead of nuclear talks today in Geneva. The oil price trades at $71 a barrel.

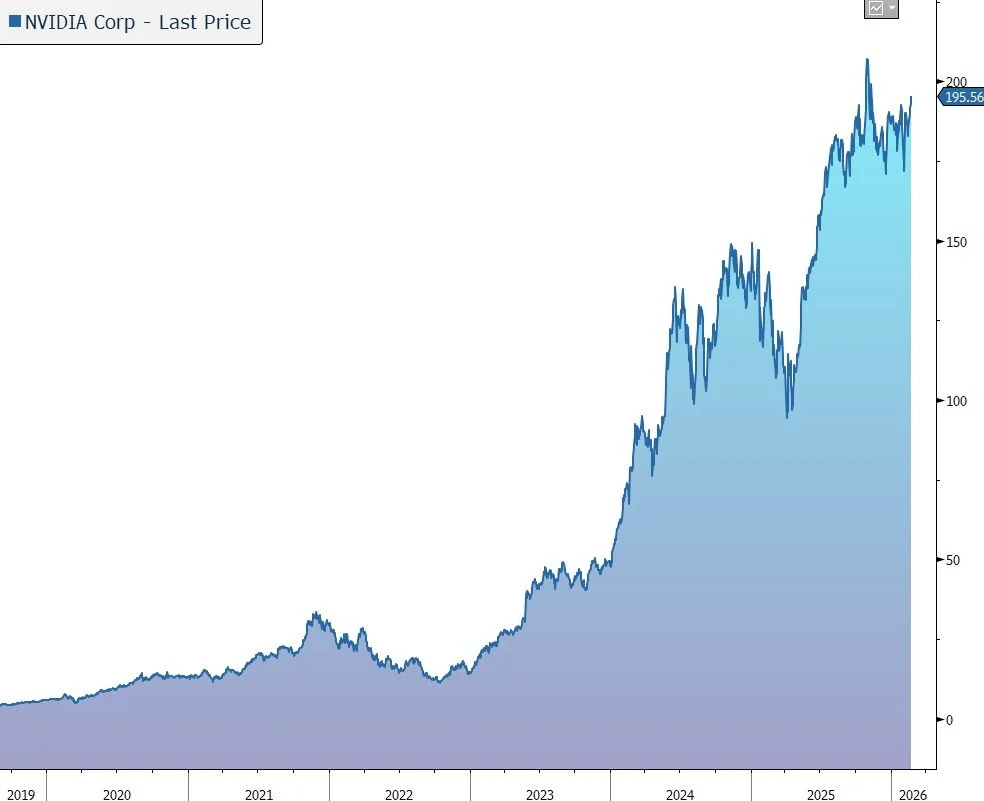

US equities moved higher last night – S&P 500 (+0.8%); Nasdaq (+1.3%). Nvidia (see below) was little changed after hours despite the release of strong results. Salesforce fell by 5% on the back of lacklustre guidance.

In Asia this morning, stocks were mixed: Nikkei 225 (+0.3% to another new high); Hang Seng (-1.1%); Shanghai Composite (flat). The yen strengthened after Bank of Japan members advocated for more rate hikes.

The FTSE 100 is currently little changed at 10,805. Rolls-Royce is up 5% following its results and the announcement of a share buyback programme. Sterling trades at $1.3525 and €1.1455.

The Financial Times notes that UK government debt issuance is set to decline for the first time in four years—a development that signals Chancellor Rachel Reeves’ commitment to fiscal restraint is beginning to alleviate pressure on the gilt market. According to the consensus of seven major investment banks, gilt sales are projected to total £247bn in the year to March 2027, a notable reduction from the £304bn raised in the current financial year.

Source: Bloomberg

Company News

Last night NVIDIA released results for the financial year to January 2026. The figures came in above expectations and guidance for revenue in the current quarter was above the market forecast. Although the results were strong, they were not good enough to push the shares higher, with little change in after-hours trading.

NVIDIA is one of the world’s largest semiconductor companies, with a leading market share in Graphics Processing Units (GPUs). From its original focus on PC graphics, the company has expanded to several other large and important computationally intensive fields, leveraging its GPU architecture to create platforms for scientific computing, AI, data science, autonomous vehicles, robotics, and industrial AI.

NVIDIA’s Blackwell and newly announced Rubin architectures remain the industry gold standard. According to new SemiAnalysis InferenceX benchmark results, NVIDIA Blackwell Ultra delivers up to 50x better performance and 35x lower cost for agentic AI compared with the NVIDIA Hopper platform. Rubin comprises six new chips to deliver up to a 10x reduction in inference token cost, compared with the Blackwell platform.

The company is benefitting as data centres make a platform shift from general computing, primarily using central processing units (CPUs), to accelerated computing, primarily using GPUs, which brings significant improvements in performance, energy efficiency, and cost.

Accelerated computing’s ability to significantly speed up machine learning and to deal with large data sets has enabled the development of generative artificial intelligence (AI), which offers human-like computing performance, and Agentic AI, AI systems that don't just chat, but can reason and execute multi-step tasks autonomously. This is driving significant investment in new enterprise applications, which is in turn driving new demand for accelerated computing. There has also been an increase in Sovereign AI, where nations build their own domestic AI infrastructure, which generates another source of revenue for NVIDIA.

A concern is Google’s AI ecosystem, which is not reliant on NVIDIA’s GPUs, creating a significant risk to the company’s ability to sustain such high market share and gross margins. This is potentially why NVIDIA is making extensive investments in its customer base, in particular OpenAI, to ensure that the majority of the AI ecosystem continues to be deeply integrated with its own chips.

Another risk is that while demand for Rubin is described as unprecedented, NVIDIA’s primary constraint remains the supply of High Bandwidth Memory (HBM4) and advanced packaging capacity from partners like TSMC.

In the latest financial year, revenue rose by 65% to $216bn. In the final quarter, Nvidia’s revenue rose by 73% to $68.1bn, above the company guidance of $65bn, plus or minus 2%, and the market forecast of $66.2bn. The result was 20% higher than the previous quarter.

The vast majority (90%) of revenue is generated in the Data Centre division, with around half derived from cloud service providers and the remainder from consumer internet and enterprise companies. During the quarter, revenue increased by 75% to $62.3bn, driven by the major platform shifts — accelerated computing and AI. For the fourth quarter, hyperscaler revenue increased and remained the company’s largest customer category at slightly over 50% of Data Centre revenue, while growth was led by the rest of the group’s Data Centre customers as revenue diversified.

The smaller divisions performed as follows in the final quarter: Gaming (+47% to $3.7bn); Professional Visualisation (+159% to $1.3bn); and Automotive and Robotics (+6% to $604m).

The gross margin is high. In the latest quarter, it rose from 73.5% to 75.2%, in line with the group’s guidance of 75%, plus or minus 50 basis points. However, the margin increased sequentially as Blackwell ramped with an improved mix and cost structure.

Operating expenses rose by 51% to $5.1bn, primarily driven by compute and infrastructure costs and higher compensation and benefits due to compensation increases and employee growth. Full-year earnings rose by 60% to $4.77, with the final quarter result up 82% to $1.62, ahead of the market forecast of $1.53.

The business is very cash generative, with free cash flow of $34.9bn in the three months to 31 January. The company’s balance sheet is very strong, with net cash of $54bn at the end of the quarter. The cash is being used, in part, for shareholder returns, including $3.8bn in share repurchases in the latest quarter. As of the end of the recent quarter, the company had $58.5bn remaining under its share repurchase authorisation. The company also pays a dividend, with a payout of $243m for this quarter.

For the current quarter, the company is guiding to revenue of $78bn, plus or minus 2%. This was ahead of the consensus expectation of $73bn. A gross margin of 75.0%, plus or minus 50 basis points is forecast, and operating expenses of $7.5bn.

Source: Bloomberg