Morning Note: Market News and an Update from Diageo.

Market News

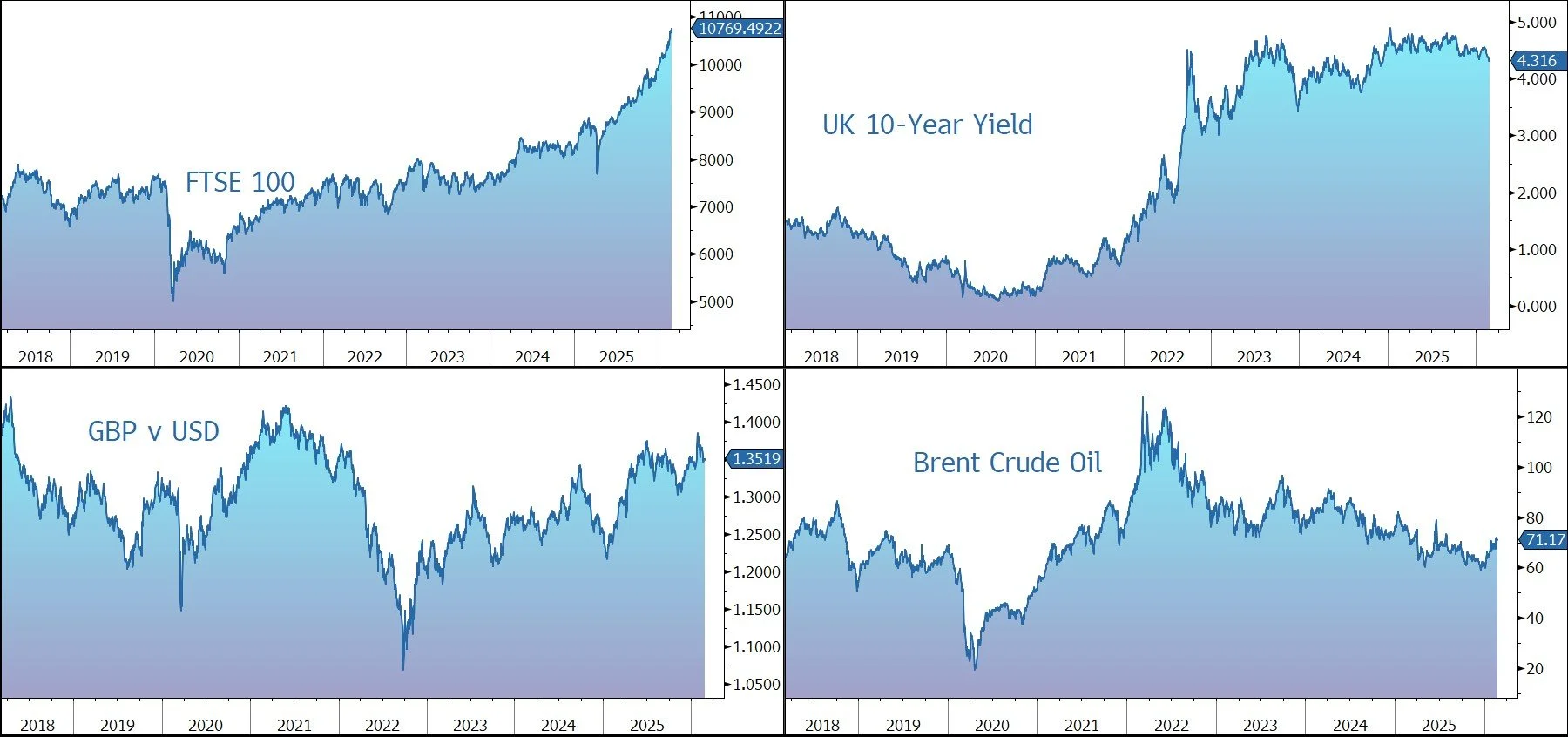

Commentary from the Federal Reserve hinted at uncertainty over the direction of interest rates. Susan Collins said rates are likely to stay unchanged “for some time.” Tom Barkin said he still sees risks on both sides of the central bank’s mandate. However, bond traders are doubling down on Fed rate cuts stretching into 2027 pointing to AI-driven cracks in the labour market. The 10-year Treasury yields 4.05%. Gold moved up to $5,180 an ounce, recouping most of the previous session’s losses, supported by trade and geopolitical uncertainty.

Donald Trump said Iran is working to reconstitute its nuclear programme in his State of the Union address, pledging to “never allow” Tehran to have a weapon. While the comments added to speculation about potential US military action, the president also reiterated his desire for a diplomatic solution. The oil price slipped back to $71 a barrel.

US equities rose last night – S&P 500 (+0.8%); Nasdaq (+1.0%) – with a tech-led rally tempering fears over AI’s disruptive fallout. Warner Bros. said Paramount’s raised bid of $31-a-share could top its existing Netflix deal, saying the sweetened terms clear the bar for renewed talks. Nvidia reports after the market close this evening.

In Asia this morning, stocks also rose: Nikkei 225 (+2.2%); Hang Seng (+0.7%); Shanghai Composite (+0.7%). Chinese travellers set records for spending and trips during the New Year holiday, with domestic tourism outlays rising to about $117bn.

The FTSE 100 is currently 0.8% higher at 10,769. HSBC is up 5% following strong earnings boosted by its wealth division. Sterling trades at $1.3535 and €1.1465.

According to Bloomberg, mentions of “net zero” have collapsed in rich nations’ energy communiques, and with global demand for oil, natural gas and coal at an all-time high the 2050 target now looks effectively dead.

Source: Bloomberg

Company News

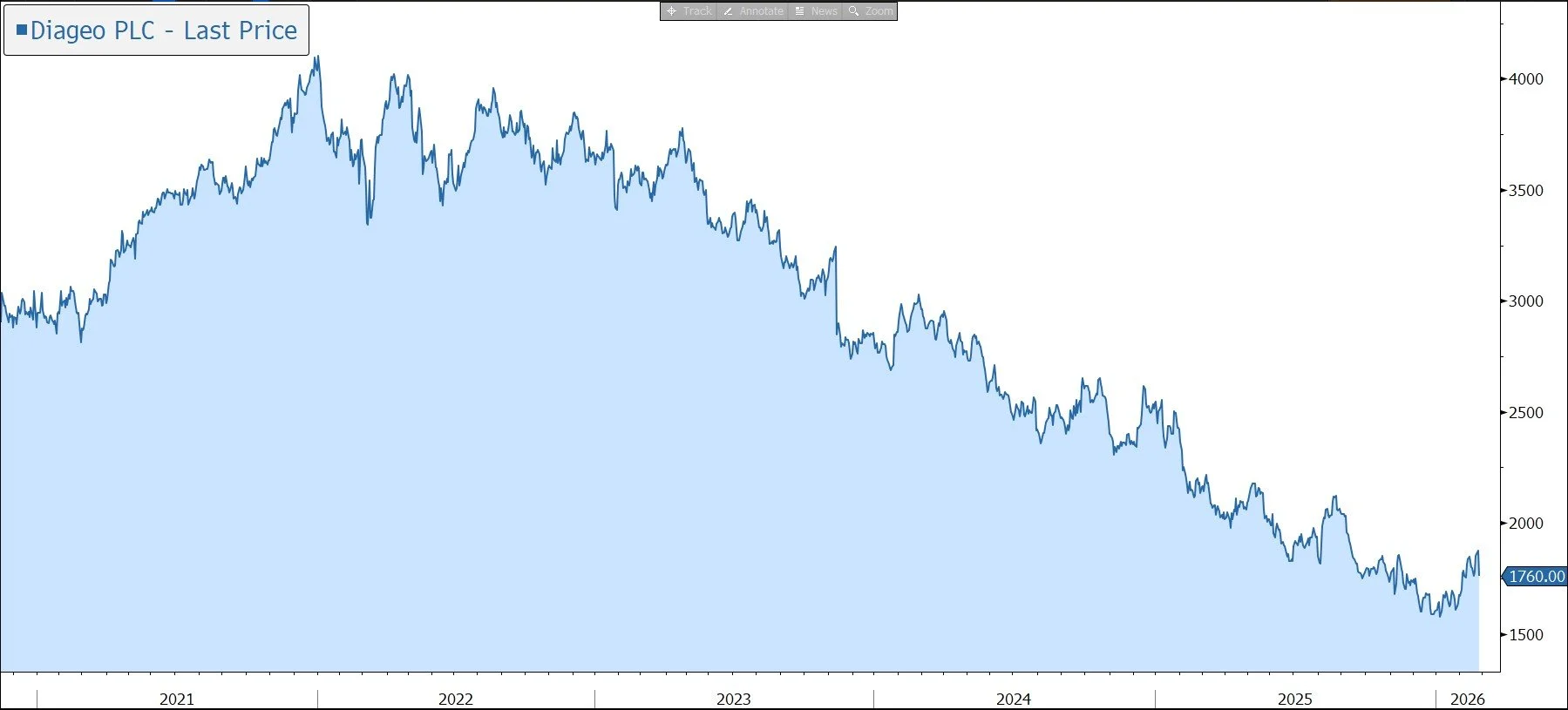

Diageo has released results for the financial half-year to 31 December 2025, the first announcement by new CEO Sir Dave Lewis. Trading remains soft due to weakness in Chinese white spirits and a muted US consumer environment and, as a result, guidance for the full year to 30 June 2026 has been trimmed. On a positive note, the company has accelerated its cost cutting programme and maintained its guidance to generate $3bn of free cash flow. However, in order to create more financial flexibility, the dividend has been reduced. In the run-up to these results, the shares had rallied by 15% so far this year. Ahead of the analysts’ call later this morning, the shares have been marked down by 6%.

Diageo is a leading global drinks company, with a unique portfolio of iconic brands including Johnnie Walker, Smirnoff, Captain Morgan, Baileys, Tanqueray, and Guinness. The company owns 13 billion-dollar brands across a broad range of categories that are gaining share from beer and wine. The group is an integrated operator, producing and supplying drinks at a variety of price points across strong global distribution routes. In the long term, we believe Diageo is well placed to benefit from the trend towards premiumisation – including its 34% stake in Moet Hennessy, the group generates more than 60% of its sales from high margin, premium brands. The group has a strong presence in under-penetrated emerging markets, where the number of people of legal purchasing age is set to increase by over 600m by 2030. Wealth is also increasing in these regions, with the middle class expanding, and consumers shifting from local products to higher-margin premium international brands.

However, the global industry environment has been challenging of late. In addition to a rebasing of consumer spending in the aftermath of the pandemic spending boom, the sector faces potential headwinds from the impact of weight-loss drugs on alcohol consumption and the request by the US Surgeon General for alcoholic drinks to carry warnings of their links to cancer. Other structural threats include Gen-Z moderation and cannabis cannibalisation. Further political risk comes from the proposed tariffs by the Trump administration.

Current research suggests these factors will have less of an impact than currently feared. For example, last summer, investment bank Jefferies commissioned a survey of 3,600 US consumers to better understand their attitudes towards alcohol, finding that although moderation was becoming increasingly important, money was the biggest impediment rather than health concerns. This implies that the biggest consumption headwind is cyclical, not structural, and that a positive macroeconomic turn is likely to be an inflection point for the sector. In addition, the industry has increased its lobbying to counter the message coming from health bodies.

In the medium term, we expect the structural tailwinds highlighted above to more than offset the headwinds, leading to positive industry growth. In addition, Diageo is focused on strengthening the resilience of its business through operational improvement, productivity, the introduction of innovative new products, and strategic investments to win market share. The first phase of the company’s Accelerate programme is progressing well and involves a number of targets including:

- to sustainably deliver around $3bn free cash flow p.a. from this financial year (FY2026), increasing as the business performance improves.

- cost savings of $625m over the next three years, with 50% of the benefit expected to drop through to operating profit and the remainder reinvested in future growth.

- deleveraging the balance sheet to be well within the target range of 2.5x-3.0x net debt/EBITDA no later than FY2028. This will be delivered through a combination of organic growth and positive operating leverage, combined with tighter capital discipline, and appropriate and selective disposals over the coming years.

- opportunities for ‘substantial changes’ to the portfolio by offloading assets that are not ‘core or strategic’. In particular, they are looking at capital intensive businesses that don’t add synergy to the group that can be sold for an attractive price.

At the beginning of the year, Sir Dave Lewis became the company’s new CEO. Lewis was the top man at Tesco and spent 27 years at Unilever. Despite having never worked in spirits before, expectations are high that his strong brand and marketing background can help turn Diageo’s fortunes around. After several weeks in the role, Lewis has today highlighted that he can ‘already see significant opportunities for Diageo to act more decisively to enhance its competitiveness and broaden the portfolio offering leading to higher growth’. As the company refines its new strategy to deliver stronger shareholder value, the ‘immediate priorities … are clear’: Build competitive category strategies, winning with relevant brands; Customer, customer, customer; and Redesign of the Diageo operating framework to drive sustainable returns. The company will update the market later in the summer on the outcome of its strategic review, although we expect some hints during the analysts’ call later this morning.

In the meantime, the company has highlighted that performance in the six months to 31 December 2025 was mixed. Trading conditions remained challenging throughout the period, reflecting macroeconomic and geopolitical uncertainty as well as weak consumer confidence in many key markets, including the US and China.

Reported net sales fell 4.0% to $10.46bn. Organic net sales (which excludes M&A and currency impact) fell by 2.8%, below the 2.0% decline expected. The sales decline was driven by organic volume down 0.9% and negative price/mix of 1.9%.

Strong organic net sales growth in Europe (+2.7%), Latin America and Caribbean (LAC, +4.5%), and Africa (+10.9%) was more than offset by softer performance in North America (the group’s largest market, -6.8%) given pressure on disposable income impacting US Spirits, and the adverse impact of Chinese white spirits (CWS) in Asia Pacific (-11.1%). In particular, US Spirits performance reflected pressure on disposable income, and competitive pressure from more affordable alternatives addressing a more stretched consumer wallet.

The cost reduction programme is progressing well with savings in the first half driven by supply chain agility and related cost savings, A&P efficiencies, and overhead savings. As a result, the operating margin rose by one basis point in organic terms to 31.1%, mainly due to adverse market mix and tariff costs offset by lower marketing investment given efficiencies. Operating profit fell by 2.8% in organic terms to $3.26bn, below the market forecast of $3.46bn. Adjusted EPS fell by 2.5% to 95.3c.

After a period of elevated spend in recent years, capex will decline to $1.2bn-$1.3bn in FY2026. In the first half, spend fell by 6% to $591m. Free cash flow fell by $164m to $1.5bn, driven by lower operating profit and adverse creditor movement year on year, partly offset by lower tax and interest payments.

Net debt ended the period at $21.7bn, with financial gearing of 3.4x net debt to adjusted EBITDA. The company remains committed to returning to its target range of 2.5x-3.0x ‘no later than’ FY2028 and by then gearing will be in the middle of the range.

This will be helped by the sale of the company’s shareholding in East African Breweries and its shareholding in the Kenyan spirits business is expected to raise $2.3bn. On completion in H2 calendar year 2026, net debt to adjusted EBITDA will be reduced by 0.25x. The ongoing strategic review by United Spirits Limited (owned 56% by Diageo) of ownership of Royal Challengers Bengaluru (RCB) cricket team is well advanced. The market forecast is currently more than $1.5bn.

In the meantime, and in order to create more financial flexibility, the company has rebased its dividend – a saving of $1.2bn. The company is committed to growing shareholder distributions over time and is targeting a 30%-50% payout policy going forward, with a minimum floor set for the dividend of 50c p.a., 52% lower than last year and a yield of 2%. An interim payment of 20 cents has been declared today.

Given further weakness through the first half in the US, the company has trimmed its guidance for the financial year to June 2026.

· Organic sales are now expected to be down by 2%-3% versus the previous guidance of ‘flat to slightly down’ and the consensus forecast of minus 1%.

· Organic operating profit growth is now expected to be to be flat to up low-single-digit, versus up ‘low to mid-single digit’ previously and the consensus forecast of +1%. This includes the impact of tariffs and the faster rate of cost savings, with 50% of the Accelerate savings now expected in this financial year.

· On a positive note, the company has reiterated free cash flow guidance of $3bn.

Source: Bloomberg