Morning Note: Market News and an Update from Melrose.

Market News

US equities slipped last night: S&P 500 (-0.5%); Nasdaq (-1.2%). Netflix exited the bidding war for Warner Bros., clearing the way for Paramount’s $111bn offer. The streaming giant’s shares rose 8% post-market, while Warner fell. The deal will almost quadruple Paramount’s cash profit, Bloomberg Intelligence said.

In Asia this morning, equities were firm: Nikkei 225 (+0.2%); Hang Seng (+1.0%); Shanghai Composite (+0.4%). Tokyo’s CPI fell below the BOJ’s 2% target in February.

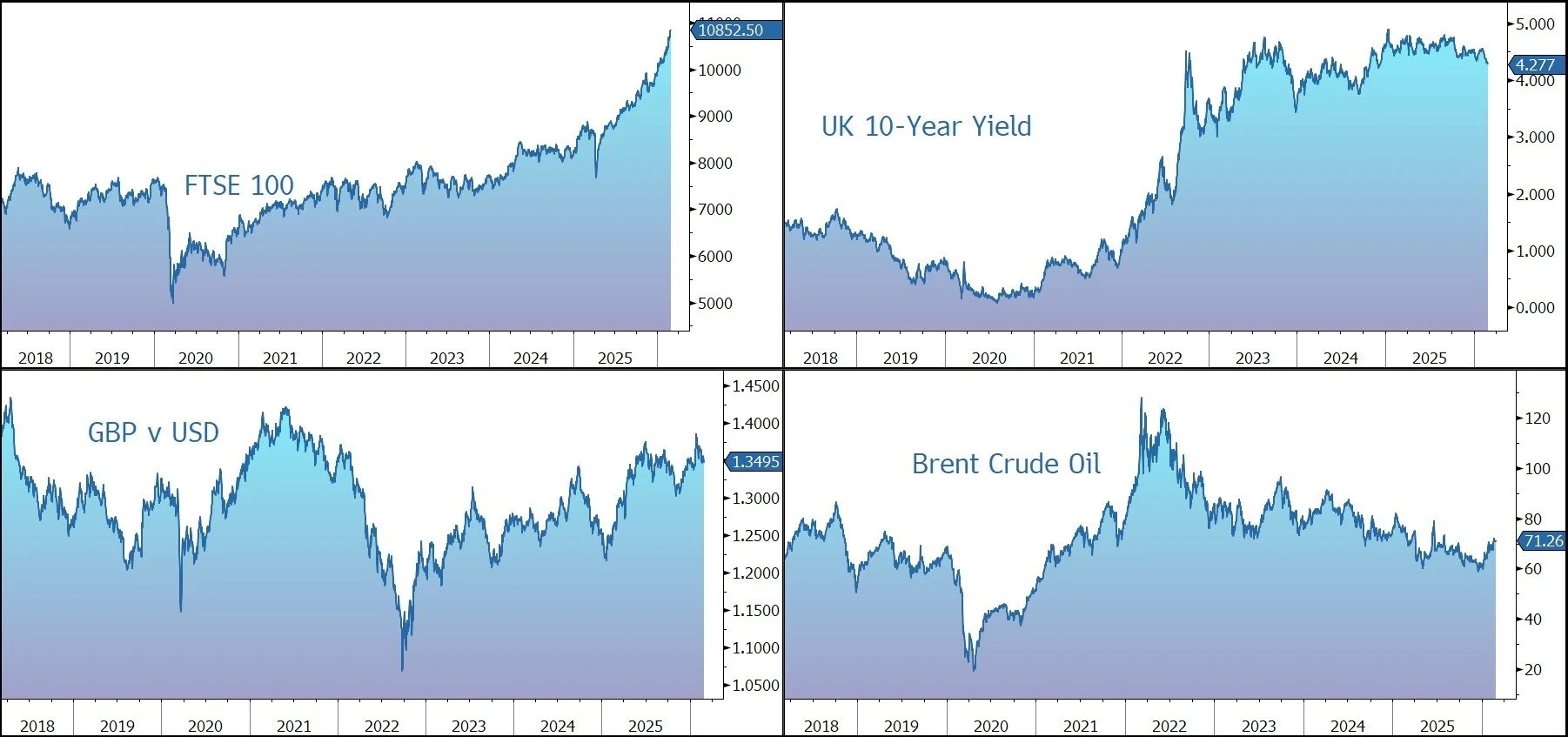

The FTSE 100 is currently 0.5% higher at 10,882. Senior is trading 17% higher after the aerospace company revealed it has received two further, all-cash proposals from other potential offerors.

The Greens won the Gorton and Denton by-election and Reform UK received the second-highest number of votes, underscoring the threat from the left and right that Keir Starmer faces. Sterling trades at $1.3495 and €1.1420. The UK is expected to cut 2026/2027 gilt sales to £245bn, down about 20% year on year and the lowest volume in three years, according to a survey.

The oil price steadied after the US and Iran agreed to more nuclear talks next week. Brent Crude trades at $71.50 a barrel. The UK has held talks with oil industry representatives about scrapping the windfall tax on North Sea oil and gas before it expires in 2030, a person familiar said. Gold trades at $5,180 an ounce.

Source: Bloomberg

Company News

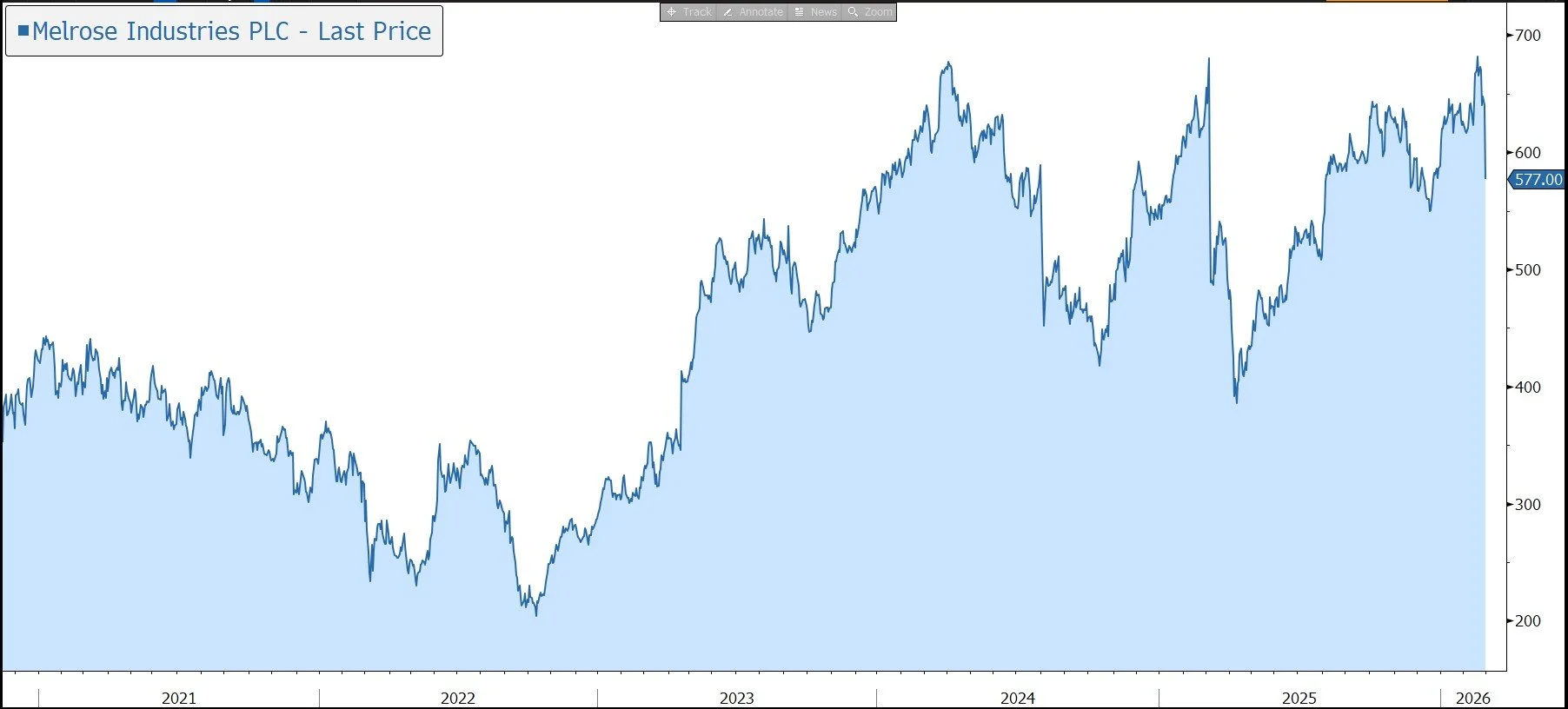

Melrose Industries has released its full-year results which highlight continued positive momentum in both its civil and defence businesses. The company has completed its multi-year transformation programme and has seen a sharp ramp-up in cash flow generation. Although guidance for 2026 is slightly below market expectations due to ongoing sector-wide supply chain constraints, free cash flow is expected to be strong, and the group has initiated another £175m share buyback programme. The shares have performed well in the run up to these results, but the operational niggles have driven some profit taking this morning, sending the stock down 12%.

Melrose is a tier one aerospace technology supplier with established positions on all the world’s high-volume aircraft. Its products are on-board 90% of civil aircraft on the market today (wide and narrow body) and the company generates 95% of its revenue from industry-leading positions (and more than 70% as sole supplier).

Revenue is split 71% civil, 29% defence. The civil industry is expected to enjoy long-term structural growth as airlines upgrade their ageing fleets after years of underinvestment. Backlogs for new aircraft stand at a record level of ~15,000. Air traffic growth and low retirement rates continue to support the aftermarket. Geopolitical uncertainty is driving a step change in defence spending, which is providing a number of new growth opportunities for the group.

R&D excellence and long-standing relationships create high barriers to entry and mean the company is well positioned for the next generation of technology, particularly that enabling zero emission flight – additive fabrication technology, uncrewed Defence air vehicles, and electric flight.

There are two divisions: Engines and Airframes (previously Structures, i.e. bodies and wings of planes).

In 2025, Engines contributed over 75% of Melrose’s profit, with over 85% of this being from the accretive and structurally growing aftermarket. The business has OEM-level capability and responsibility for selected engines which gives more technical and commercial advantages than normal for a Tier 1 supplier. The company is partner to all major engine OEMs (original equipment manufacturers) with its lucrative and diverse Revenue and Risk Sharing Partnerships (RRSP) portfolio providing strong cash flow growth. 17 of the 19 RRSPs are already in the cash generation phase, with a total expected lifetime gross cash inflow of £22bn (£6bn net). In Airframes, Melrose has strong embedded positions with over 70% of its content provided on a sole-sourced basis.

The company has announced its Chief Financial Officer will retire in May, with Ross McCluskey (ex-CFO of Intertek) appointed as his successor and joining the Board in May 2026. We are happy with this appointment because Intertek is known for its capital discipline and high margins, something Melrose will need to focus on as it looks to shift from a restructuring play to an operational compounder.

In 2025, revenue was up 8% on a like-for-like (LFL) basis (excluding the impact of exited businesses) to £3,589m. This was above the guidance range of £3,425m-£3,575m and the market forecast of £3,515m.

The group’s multi-year transformation programme has been completed. This has been the key driver of margin expansion – in 2025, the adjusted operating margin increased by 240 basis points to 18.0%, versus guidance 18%+, and with good progress in both divisions. Adjusted operating profit rose by 23% to £647m, versus guidance of £620m-£650m and the market forecast of £643m. EPS rose by 25% to 32.1p, versus the consensus of 32p.

In Engines, revenue grew by 15% to £1,632m on a LFL basis driven by a strong performance in both OE and the aftermarket. Margins rose by 300 basis points to 31.9%, driven by revenue growth and favourable mix. OE growth of 16% was driven by the group’s RRSP portfolio across both narrowbody and widebody platforms. Aftermarket grew by 14% and included a return to robust growth for the parts repair business.

In Airframes, revenue grew by 3% on a LFL basis to £1,957m, with the margin rising by 80 basis points to 8.0%. Melrose saw encouraging growth in Defence (+15%), reflecting strong demand coupled with the group’s business improvement actions – over 90% of the portfolio now sustainably priced. The performance in Civil (-2%) continued to be constrained by well-publicised customer supply chain issues and variability in OE production rates.

As expected, free cash flow is ramping up sharply as a result of increased RRSP cash flows, operational improvements, and reduced restructuring cash spend. In 2025, the company generated free cash flow of £125m, versus an outflow of £74m the previous year, and compared to guidance of ‘more than £100m’ and the consensus forecast of £105m.

Melrose has a strong balance sheet with leverage at the end of 2025 of 1.8x net debt to EBITDA, in line with the target to be between 1.5x and 2.0x. Financial strength is driving attractive shareholder returns through a progressive dividend – the full year payout of 7.2p is 20% higher than last year.

The company is also undertaking a £250m share buyback programme expected to complete in March 2026. There is potential for a sizeable cash return every year until the end of the decade – with today’s results, Melrose has announced a new twelve-month share buyback programme of £175m. The company has said no material acquisitions will be made in the near term.

Overall, the most significant contributor to future Melrose value is profitably capturing the growth from its established positions across civil and defence platforms from record order backlogs, as production ramps and the aftermarket flows through.

Positive momentum is expected to continue in 2026. Guidance for revenue is £3.75bn to £3.95bn, up 10% in LFL terms reflecting OE volume ramp-up and the continued strength of the aftermarket. This is slightly below the current market forecast (£4.0bn) as sector-wide supply chain constraints are expected to persist.

Adjusted operating profit is expected to be between £700m and £750m, reflecting a margin of 19% at the mid-point. The guidance includes variable consideration of between £340m and £380m depending mainly on OE build rates of key engine programmes. Free cash flow is expected to expand to between £150m and 200m, driven by the completion of the restructuring programme and growth in operating profit.

As a result, the company is well positioned to deliver its 2029 targets: revenue of £5bn, operating profit (post PLC costs) of £1.2bn+ (i.e. 17% CAGR), margin of 24%+, and free cash flow of £600m and growing beyond. 90% of revenue will come from existing platforms – growth will be driven by maturing engine RRSP portfolio, margin improvement at structures, and ongoing demand for parts – and 10% from new opportunities.

We note US investment management company Capital Group now own 18% of the shares.

Source: Bloomberg