Morning Note: Market News and an update from Nike

Market News

Gold climbed to around $4,370 an ounce, before falling back, as fresh economic data strengthened expectations that the Federal Reserve could deliver further rate cuts. US inflation eased to 2.7% in November, below forecasts, while core inflation fell to 2.6%, its lowest since March 2021.

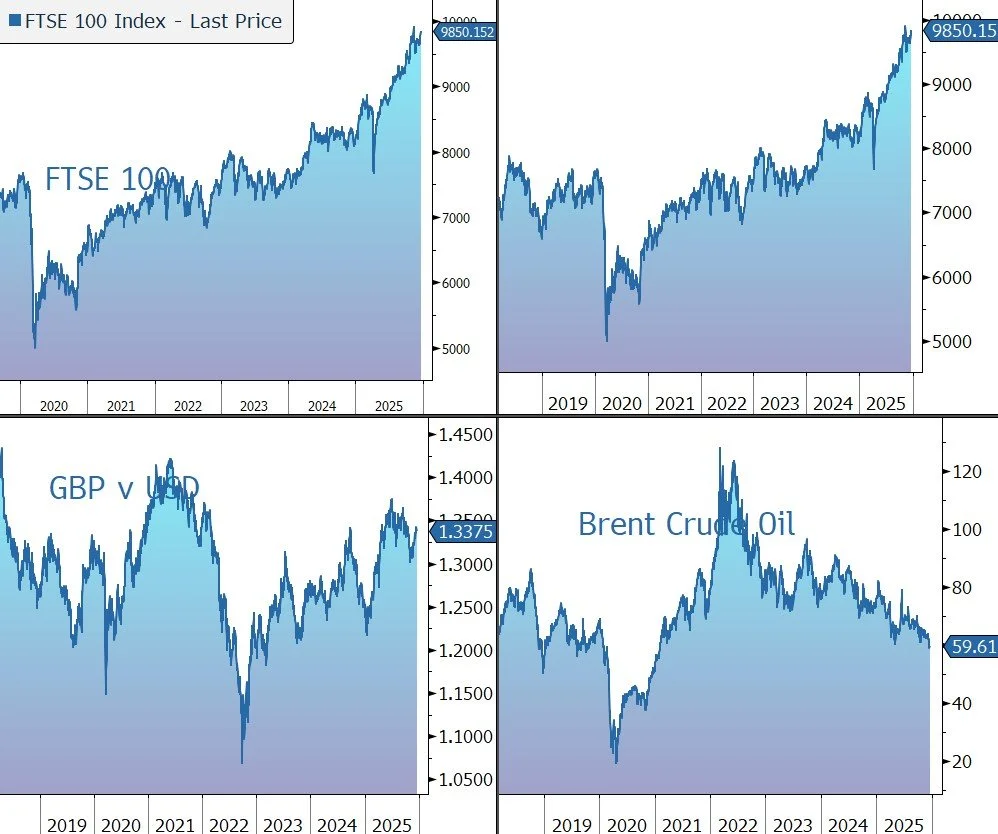

The inflation data also helped buoy US equities last night – S&P 500 (+0.8%); Nasdaq (+1.4%). Nike fell 10% after-hours (see below) following muted guidance for the current quarter. In Asia, stocks followed gains on Wall Street: Nikkei 225 (+1.0%); Hang Seng (+0.8%); Shanghai Composite (+0.4%). Japan’s 10-year bond yields climbed to multi-decade highs after the Bank of Japan raised borrowing costs as expected. Former Bank of Japan official Kazuo Momma told Bloomberg TV he expects two rate hikes in 2026 and one more in 2027, taking the rate to 1.5%.

The FTSE 100 is currently 0.2% higher at 9,850, while Sterling trades at $1.3375 and €1.1415. As expected, the Bank of England cut rates by 25 basis points at its final meeting of the year. The vote split was also as anticipated, at 5–4, with Governor Andrew Bailey backing a cut this time. Policymakers reiterated their guidance for a “gradual” pace of further easing, while noting that future decisions would be more finely balanced. Markets are now pricing in about 62 points of easing from the central bank by the end of next year, compared to about 66 points before the decision.

Brent Crude dipped below $60 a barrel, leaving it on track for a second straight weekly decline, as oversupply concerns outweighed geopolitical risks. Chinese coking coal is headed for its biggest weekly gain since August.

We will resume our Morning Note on Monday 5 January 2026 and would like to wish all of our clients and readers a wonderful time over Christmas and the New Year. Thank you for your support during 2025 and we look forward to the coming year.

Source: Bloomberg

Company News

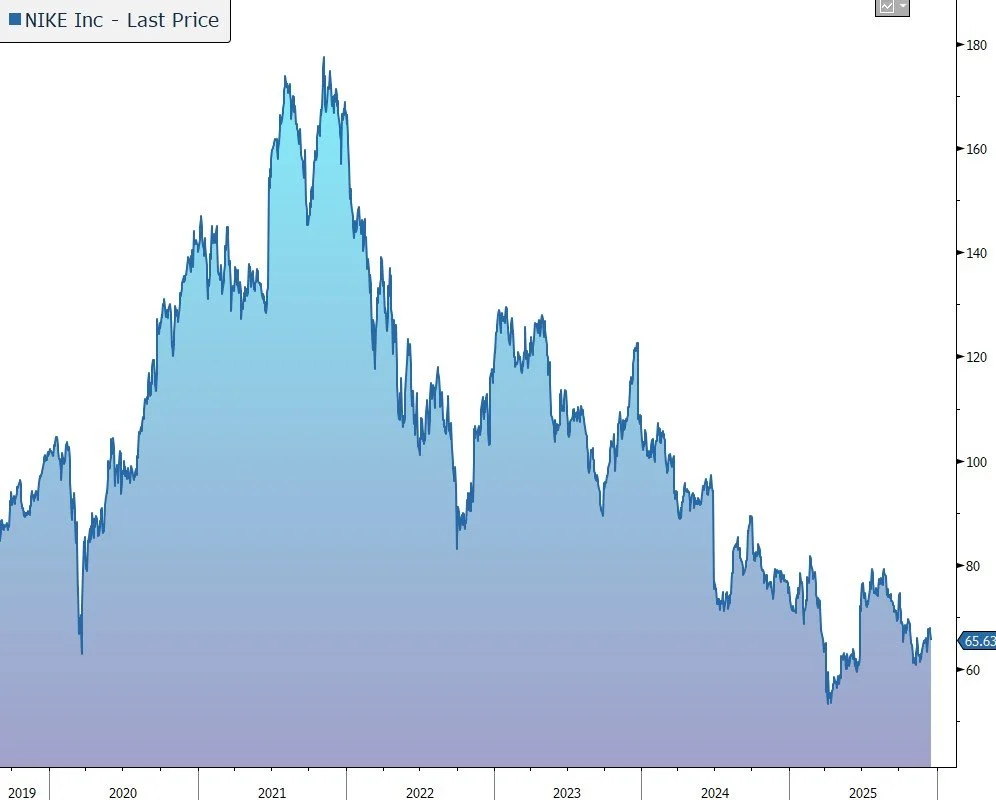

Last night, Nike released results for the three months to 30 November 2025, the second quarter of its financial year to end May 2026. Although the figures were ahead of market expectations, driven by an improved US performance, the result in China was disappointing. On the analysts’ call, the company provided guidance for the current quarter, with the forecast of low single-digit sales growth below current market expectations. Although the CEO had previously warned investors the group’s turnaround would not be linear, as parts of the business recover on different timelines, yesterday’s update was clearly a step backwards. In response, the shares were marked down 10% after hours.

Nike is the world’s leading sports footwear and apparel company. Its products are sold at various sporting goods retailers, as well as company-operated stores and websites. We are positive on the long-term outlook for the business, with the company well placed to benefit from increased consumer demand for healthier living and the shift to personalised products. Nike has a very strong brand and an impressive track record of product innovation.

However, over recent years, the company made a number of strategic errors, the impact of which were exacerbated a subdued macroeconomic backdrop with continued promotional activity and the emergence of competition from new brands such as On and Deckers’ Hoka. In particular:

· an over-reliance on key ‘classic’ product franchises (Air Force 1, Air Jordan 1, and Dunk) at the expense of new innovation.

· An overly aggressive push from a wholesale-driven model to a direct (in particular digital) model which alienated third-party retailers who are essential to elevate the brand and grow the total marketplace.

In response, former senior executive (and 32-year Nike veteran) Elliott Hill returned to the company as CEO. Given that much of the recent corporate malaise was down to poor management/strategy, the hope is that Nike will return to its roots and the culture that made it so successful. The plan is to ‘lead with sport and put the athlete at the centre of every decision, leveraging athlete insights to accelerate innovation, design, and product creation’.

The group has accelerated its multi-year cycle of innovation and pulled forward several new products, especially in high-volume areas like running, training, football, sportswear, and Jordan. Inventory cleaning has been aggressive, removing stale product from the market. There has been a refocus on the wholesale market and a shift at NIKE Digital to a full-price model, reducing the percentage of the business driven by promotional activity. Nike is also being aggressive in sports marketing across leagues, associations, teams and individuals.

The early results have been encouraging. New products such as the Vomero, Pegasus, and P-6000 running ranges continue to resonate well with customers. The company has launched a new women’s activewear brand in the US in partnership with Kim Kardashian-owned shapewear clothing company Skims. The brand, called NikeSKIMS, includes training apparel, footwear, and accessories for women.

Overall, immediate action has been taken in areas that will make the most near-term impact. The company has admitted change will take time and “turnaround efforts may hurt in short term”, with sales and gross margin in decline. Furthermore, progress is not expected to be linear as parts of the business recover on different timelines. Although AJ1 and AF1 classic lines are stabilising, there is still work to do on the much smaller Dunk franchise.

Although the results from the latest quarter were slightly better than management expectations, headwinds remains, in particular in China, Converse, and a result of tariffs.

In the three months to 30 November 2025, revenue was flat on a currency-neutral basis to $12.4bn. This compares to the company guidance to be down by ‘low-single digits’ and the market estimate of €12.2bn. Once again, the wholesale channel (+8%) and Running category (+20%) were the standout performers.

Nike Brand sales were up 1% at $12.1bn, ahead of the market forecast of $11.9bn, while the Converse brand fell by 31% to $300m.

By region, North America, which accounts for 46% of sales, generated revenue growth of 9% in the quarter. The region has been the early focus on the group’s turnaround plan and the recovery so far provides encouragement for the group as a whole.

Elsewhere, small revenue declines in were registered in Europe, Middle East, & Africa (EMEA, -1%) and Asia Pacific & Latin America (APLA, -4%). The main disappointment was Greater China where revenue fell by 16% as a result of competition from domestic brands. The company has now taken a number of unplanned actions including new management, increased innovation. and improved store layout. Although the company remain very positive on the long-term opportunity in China, management admits the recovery will take time.

Nike Brand sales are split into Direct sales (both online and through Nike-owned stores) and wholesale revenue from third party retailers. During the quarter, Nike Direct sales fell by 9% to $4.6bn, with digital down 14% and stores 3%. Encouragingly, Wholesale grew by 8% to $7.5bn.

By category, a small 1% decline in Footwear was more than made up for by increased in Apparel (+4%) and Equipment (+1%).

The company continues to see pressure from tariffs and its efforts to clear out aged inventory on its margins. The gross margin fell by 300 basis points to 40.6%, versus the company guidance for a 300-375 bps decline. Selling and administrative expenses rose by 1%, with demand creation expense (i.e., marketing) up 13%, primarily due to higher brand marketing expense and higher sports marketing expense. Operating overhead expense fell by 4%, primarily due to lower wage-related expense and lower other administrative costs. The operating profit margin fell from 11.3% to 8.0%, although the company still sees a path to a return to a double-digit margin. EPS fell by 32% to 52c, well above the market forecast of 36c.

Inventories remain elevated across all geographies, albeit down 3% to $7.7bn, reflecting a decrease in units, partially offset by increased product costs, primarily due to higher tariffs in North America. The company had said inventories would be in a ‘clean’ position at this stage, although this is only the case in North America and EMEA.

The group’s balance sheet remains strong – with net cash of $330m. During the quarter, the group returned just under $600m to shareholders through dividends, up 7% from the prior year.

Given where the company is in its restructuring programme, Nike is currently only providing quarterly guidance rather than annual guidance. Over the near term, the net effect of the strategic actions will continue to result in lower revenue, gross margin pressure, and higher marketing expenses. In the current quarter, revenue is expected to decline by low single digits (including a 300bps benefit from currency). Performance in Greater China and Converse is expected to be similar to the previous quarter. The gross margin is forecast to be down 175-225 basis points (including a 315 basis points tariff impact).

Source: Bloomberg