Morning Note: Market News and an Update from Smith & Nephew.

Market News

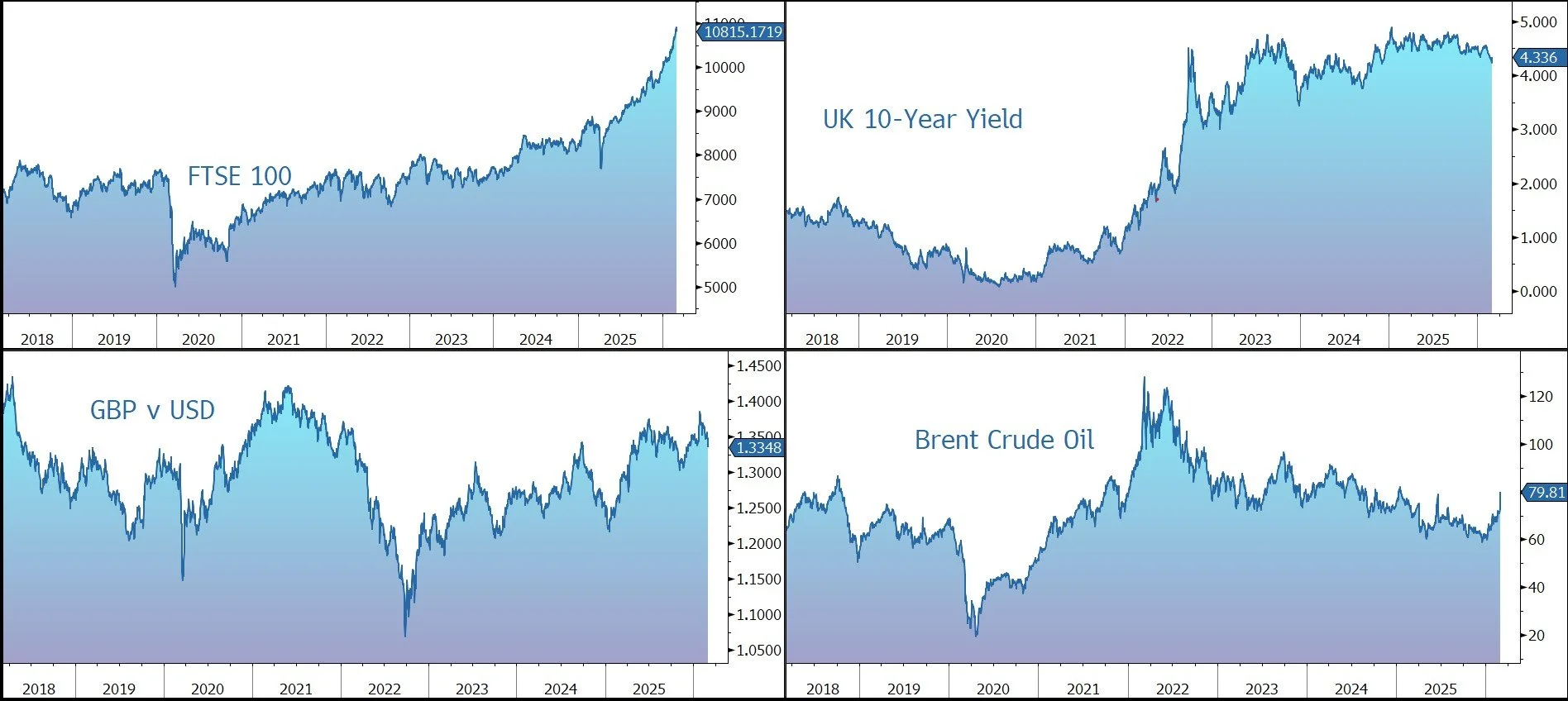

Brent Crude is trading 9% higher at $79 a barrel, after an earlier spike of nearly 13%. The rally followed strikes by the US and Israel, heightening fears of supply disruptions in the Middle East. Markets are particularly focused on the Strait of Hormuz, a vital choke point that handles roughly one-fifth of global oil shipments and significant volumes of natural gas. Iran said it doesn’t intend to shut the key lane but shipping there virtually halted over the weekend. Saudi Arabia and the UAE can reroute some oil via pipelines, but Kuwait, Qatar and Bahrain have no option but to use the waterway.

Also important is whether oil infrastructure in the region is damaged – we note the Saudi Arabia Ras Tanura Refinery has shut down after a drone strike. Meanwhile, OPEC+ agreed on Sunday to increase production by 206k barrels per day (bpd) in April, ending a three-month pause, but well below the 411k-548k bpd that had been previously considered.

Donald Trump said the bombing campaign against Iran will continue until objectives are achieved. The president claims his picks as possible candidates to lead the Middle Eastern state were killed in the initial attack. The US is open to dropping Tehran sanctions if the new leader is pragmatic, the NYT cited Trump as saying. Iran’s national security chief said his country won’t negotiate with the US.

The dollar climbed, hitting a five-week high, while gold climbed more than 2% back above $5,400 an ounce, reaching an over one-month high. Meanwhile, data on Friday showed US producer prices rose more than expected in January, indicating that companies are passing tariff costs to consumers and complicating the path for Federal Reserve rate cuts. Clearly an elevated oil price will do little to help inflation.

Global equity markets sold off in Asia this morning – Nikkei 225 (-1.3%); Hang Seng (-2.1%) – and the futures market is currently expecting a fall at the US open this afternoon: S&P 500 (-1.5%); Nasdaq (-1.8%).

The FTSE 100 is currently 1.0% lower at 10,815. Unsurprisingly, the oil majors BP (+4%) and Shell (+4%) are firm, as are other commodity stocks. Sterling trades at $1.3316 and €1.1380. We note the UK natural gas price used by the regulator OFGEM to set the energy price cap has surged by 25%. Ofgem has recently confirmed a significant drop in the energy price cap for the upcoming spring quarter, this points to upward pressure come the summer.

At the end of last week, OpenAI raised $110bn at a $730bn pre-money valuation from Amazon ($50bn), NVIDIA ($30bn), and Softbank.

Source: Bloomberg

Company News

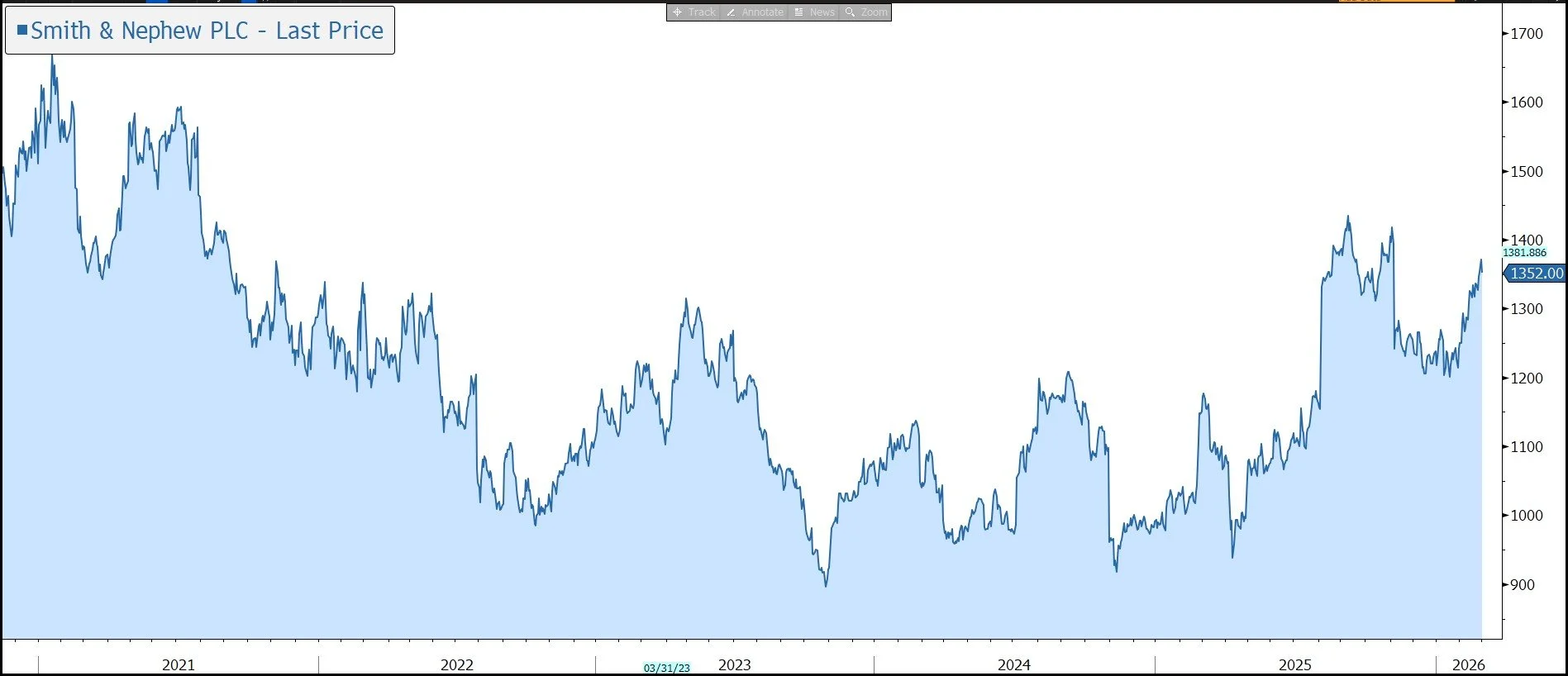

Smith & Nephew has released its 2025 results. A strong fourth quarter helped the company meet or exceed its 2025 targets for revenue growth, profitability and cash generation. The dividend was raised by 4.3% and the guidance for 2026 set out in December was reiterated. The group’s growth plans are ambitious, and given the poor track record of meeting guidance, the market is unlikely to fully re-rate the shares until there is more evidence of execution. In response to today’s results, the shares have been marked down by 3% against a weak overall market backdrop.

Smith & Nephew (S&N) is a UK-listed medical products company with three specialist global franchises: Orthopaedics (global No.4), Sports Medicine (No.2) & ENT (No.4), and Advanced Wound Management (No.2). In total, the group’s addressable market is around $55bn, growing at 6%.

We believe the S&N is well placed to benefit from the increased incidence of obesity and related conditions, such as diabetes and osteoarthritis, given its strong market position in joint replacement, trauma and diabetic ulcer treatment. Meanwhile, the shift to more active lifestyles in some quarters is expected to lead to increased wear and tear on joints and more sporting injuries, a trend which should benefit S&N. Finally, the group should benefit from an ageing population, who consume more medical products and are more prone to chronic diseases, and growth in emerging markets, as a growing middle class look to access higher-quality healthcare and adopt ‘western’ lifestyles and habits.

However, over the last few years, the business has been impacted by the continued delay to elective surgeries, supply chain issues, higher input cost inflation, and the impact on pricing of volume-based procurement (VBP) in China. There is also a concern over the impact GLP1 weight loss drugs will have on the industry which we believe is overdone.

In addition, operational execution at S&N has been mixed, with recurring restructuring charges and under-performance relative to its global rivals. In response, in 2022 the company set out a 12-point Strategy for Growth plan which has left the business in a fundamentally stronger position. However, there is more to do and, last December, the company set out a new strategy (RISE) with four elements:

· To Reach more patients by driving adoption of the group’s differentiated portfolio and taking share across indications, settings, and markets worldwide.

· To Innovate to enhance the standard of care through accelerating new product launches and rapidly scaling existing innovation platforms.

· To Scale through strategic investment, allocating capital to high return and high growth opportunities aligned to the group’s portfolio priorities.

· To Execute efficiently, driving enterprise productivity and asset efficiency to expand margins and returns.

Sports Medicine, Advanced Wound Management, and ENT will drive above-market growth through innovation and disciplined execution, while Orthopaedics, operating in a more mature segment, will aim to deliver market-level growth. The latter target is a bigger demand, as it will require a halt of market share loss to rivals like Stryker and Zimmer Biomet. Broadly half of the growth over the medium term is expected to come from new launches. Overall, the new plan is expected to deliver a further step-change in financial performance between 2025 and 2028.

· 6%-7% underlying revenue compound annual growth rate (CAGR), significantly above the group historical average.

· 9%-10% trading profit CAGR, driven by operating leverage and efficiencies.

· More than $1bn in free cash flow in 2028.

· 12%-13% post-tax ROIC in 2028, significantly above the group’s WACC.

Management has built a lot of headroom into the guidance to offset any unforeseen macro factors. Growth will be derived from a broad range of products and geographies and is expected to be consistent throughout the period, rather than back-end loaded.

The company has also identified further opportunities to rationalise its product portfolio. Work is ongoing to finalise the product families and individual Stock Keeping Units (SKUs) which will be removed from the portfolio over time, but the company currently estimates it will be able to reduce gross inventory by around $500m. To achieve this significant and ongoing reduction in the capital requirement of the business, the company has taken a $200m non-cash inventory provision in 2025.

Back to today’s results. In 2025, revenue grew 6.1% to $6,164bn. On an underlying basis, which strips out the impact of M&A and currency, growth was 5.3%, versus the guidance to be around 5%. In the final quarter, growth was up 6.2% in underlying terms to $1,702m. This includes the benefit of one extra trading day offset by a 100 basis points headwind from China.

Recent product launches are driving growth across all business units, with 5% of sales spent on R&D. Key products include Cori (robotic surgical system), Journey (knee replacement), PICO (wound therapy), and Leaf (monitoring sensor). New products launched in the last five years account for around half of the group’s growth. The new product pipeline is very full, including the TESSA system (first of its kind arthroscopic video-based navigation) currently under FDA review.

The company disclosed the results by business line:

· In Orthopaedics, the rate of underlying organic growth was 5.1%.

· Sports Medicine & ENT generated growth of 5.2%, including a 4% headwind from China.

· In Advanced Wound Management, revenue grew by 5.6%.

The group’s Established (i.e., developed) Markets were up 5.9%, with the US (the largest market) and other Established markets both up 5.9%. Emerging Markets rose 2.5%, held back by headwinds from China, as expected. The country is now only 3% of revenue and so will have a smaller impact going forward.

The group is undertaking a $325m-$375m cost savings plan, of which $200m was achieved by the end of 2025, with the remainder expected this year.

The trading margin rose from 18.1% to 19.7%, versus guidance of at least 19.5%. Revenue leverage and accelerated operational savings more than offset external pressures including China and commodity prices. Trading profit rose by 15.5% to $1,211m, ahead of the market forecast, while adjusted EPS grew by 21% to 102c.

Trading cash flow conversion was 102%, driven by working capital discipline, particularly inventory management. Free cash flow rose by more than 50% to $840m, well above the guidance of $800m, as expected, helped in part by a $26m property gain. ROIC improved by 90 basis points to 8.3% despite a 160bps headwind from portfolio rationalisation and is now above WACC for the first time in a few years.

The company has a robust balance sheet and access to significant liquidity. In 2025, net debt rose slightly to $2.8bn, with gearing of 1.7x net debt to EBITDA, versus the 2.0x target. The dividend was raised by 4.3% to 39.1c (2% yield). During the year, the completed a $500m share buyback programme.

M&A is expected to remain part of the strategy. Earlier this year, the company added to its growing shoulder franchise through the acquisition of Integrity Orthopaedics and its Tendon Seam product. The cost was $225m up front plus a further $225m of milestone payments.

Guidance for 2026 has been confirmed. Underlying revenue growth is expected to accelerate to around 6%, with profit growth expected to be ahead of revenue growth as operating leverage is delivered. Trading profit growth on an organic basis is expected to be around 8%, with revenue leverage and operational savings offsetting headwinds from inventory revaluation, tariffs, skin substitute reimbursement changes, and ENT pricing in China. Free cash flow is expected to be around $800m, with a post-tax ROIC expected to exceed 10%.

Source: Bloomberg