Morning Note: Market News and an Update on BH Macro.

Market News

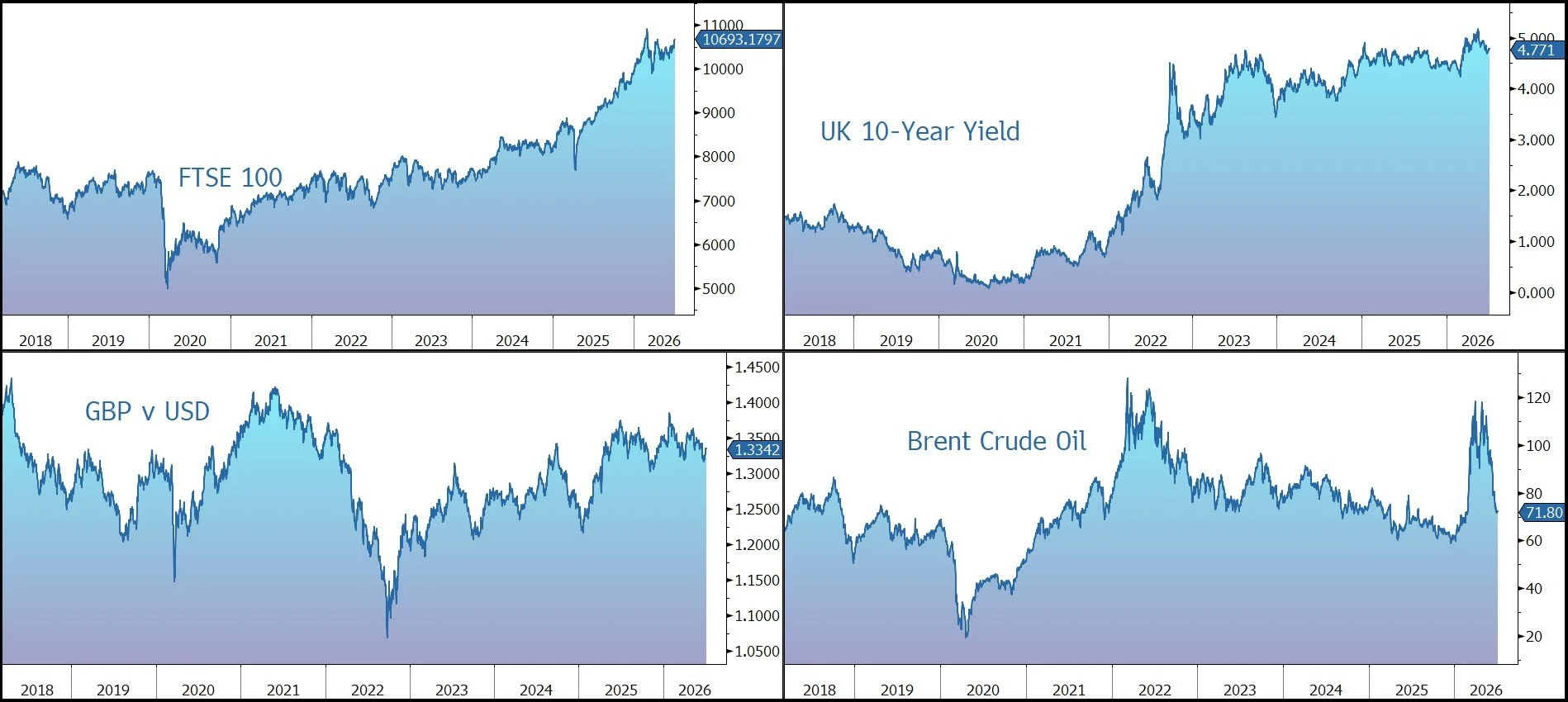

Shipping along a US-protected corridor near Oman in the Strait of Hormuz showed signs of recovering after some vessels earlier performed unexplained U-turns and detours. Iran said China and other friendly nations will get “special considerations” when Tehran sets fees for using the waterway OPEC+ signalled higher supplies. The oil price was little changed at $71.80.

Donald Trump may follow up with Vladimir Putin after he holds a bilateral meeting with Volodymyr Zelenskyy on the sidelines of this week’s NATO summit, senior US officials said.

The dollar rose ahead of the release of the last Federal Reserve meeting minutes. The yield on the US 10-year Treasury is 4.47%, while gold trades at $4,150 an ounce.

In Asia this morning, a rebound of technology shares stalled as investors turned cautious about the durability of the AI-driven rally: Nikkei 225 (flat); Hang Seng (+0.7%); Shanghai Composite (-0.1%); Kospi (-0.5%). Goldman revised its yen forecast to 165 per dollar from 155, ranking it among the most bearish forecasters surveyed by Bloomberg.

Equity-index futures for Wall Street benchmarks pared gains they made on Friday, when US markets were shut for a holiday. The S&P 500 is currently expected to open little changed this afternoon. Attention is shifting to the earnings season for signs that technology companies can turn their investments on AI into profits.

The FTSE 100 is currently 0.4% higher at 10,717, while Sterling trades at $1.3345 and €1.1680. The Board of easyJet and US investment firm Castlelake have reached an agreement in principle on the key financial terms of a recommended cash offer of 690p a share, or £5.2bn. In early trading this morning the shares are up 10% to 615p.

Source: Bloomberg

Alternative Fund Update – BH Macro

Diversification across asset classes is a critical element of managing your investments. At Patronus, when we construct a portfolio, we look to allocate a proportion of capital to so-called ‘anti-fragile’ investments that provide shelter in difficult times when other (‘fragile’) asset classes (such as equities and bonds) are struggling to generate a positive return. We believe BH Macro is one such investment.

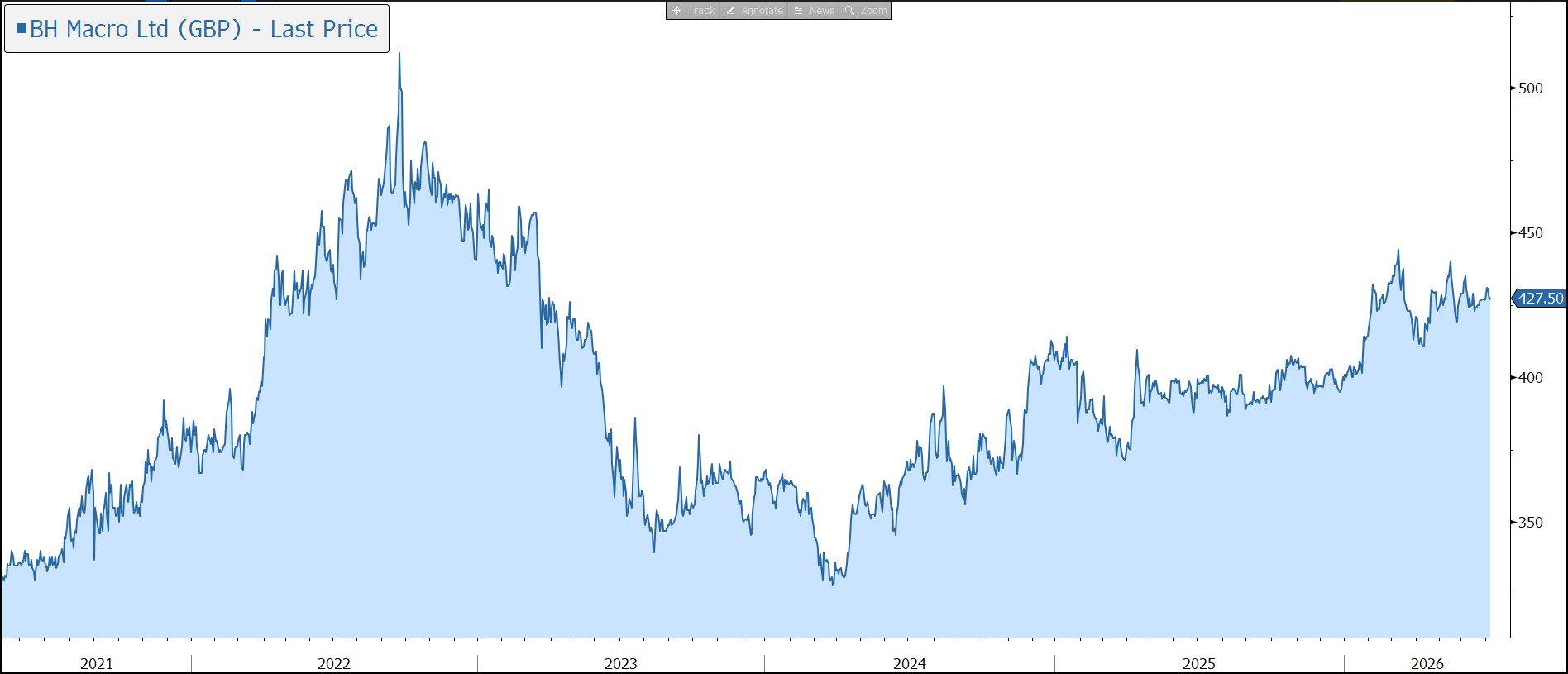

BH Macro (BHMG) is a London-listed closed-ended investment company that invests substantially all its assets in the ordinary shares of the $12bn Brevan Howard Master Fund. This is Brevan Howard’s longest running fund and one of the most successful hedge funds of all time in terms of the absolute amount of money returned to investors.

Following the 2021 merger with BH Global (Brevan Howard’s other listed investment strategy), a larger, more liquid, entity with the same investment policy was created. There are sterling and dollar classes available and total company assets currently stand at around £1.5bn. Fund fees are made up of a fixed component (management fee and operational services fee) of 2% and a 20% performance fee subject to a high-water mark. As a result, the total Ongoing Charges Figure (OCF) can fluctuate significantly due to the performance fee.

The objective of the fund is to generate consistent long-term appreciation through active leveraged trading on a global basis. The fund pursues a multi-trader model that includes a combination of macro directional and macro relative value strategies which mainly focus on economic change, monetary policy, and market inefficiencies. Exposure is predominantly to global fixed income and currency markets, with peripheral exposure to other asset classes, such as equities, credit, commodities, and digital assets. The fund seeks to achieve positive returns, uncorrelated with other markets and with low volatility. The underlying philosophy is to construct strategies, often contingent in nature, with superior risk/return profiles, whose outcome will often be crystallised by an expected event occurring within a pre-determined period of time.

The decision to hold the shares depends on whether the fund will provide capital protection during periods of market stress. In this regard, it has a good track record when equity markets are falling and has shown correlation with market volatility. Since inception in 2007 to April 2026, in the 20 worst performing months for equities, the BH Macro NAV has produced 17 positive monthly returns. The fund really proved its worth in 2020 (Covid-19: NAV (+28%) vs. FTSE 100 (-11.6%)) and in 2022 (Ukraine: NAV (+22%) vs. global equities (-8%) and UK bonds (-15%)). Since inception, the annualised NAV return is 8.2%, with NAV volatility (i.e., annualised standard deviation of returns) of 8.2%.

Risk management has helped reduce the number and extent of negative outcomes. Risks are minimised by diversifying exposures, sensible trade construction, and strict stop-losses. As a result, capital has been protected when things have gone against the manager and drawdowns have been significantly lower than other asset classes.

However, over time the BH Macro share price has been more volatile than the NAV, with significantly larger drawdowns – a risk of the investment trust structure. For a number of reasons, the shares have lingered at a sizeable discount over the last few years.

Most notably, in February 2023, and in response to persistent requests from its shareholders, the company placed £312m of new Sterling shares to increase the liquidity of the stock and spread the company’s fixed costs over a wider base. However, the move caused some indigestion and the shares moved from a 19% premium to a 19% discount at its low point in March 2024. The overhang was exacerbated by the merger of two of the company’s largest shareholders, Rathbones and Investec. Although the Takeover Panel has given clearance that the combined entity is not under any obligation to make sales of the stock, it has gradually reduced its holding from 29% at the start of 2024 to 16.4% on 22 May 2026.

Against this backdrop, on 29 June 2026, Brevan Howard Capital Management (the Manager) launched a new private fund to invest and trade in strategies and funds managed by the Manager, including BH Macro itself. The new private fund is explicitly designed to invest and trade in BH Macro shares. The fund has the ability to buy BH Macro shares, of either currency class, directly on the London Stock Exchange. This creates a new, consistent ‘buyer of last resort’ that can help soak up excess supply in the market. The fund will finance these purchases by redeeming its direct holdings in the Brevan Howard Master Fund. Effectively, the manager is shifting internal capital from the private master fund into the public BH Macro shares whenever the public shares are trading at an attractive discount. This sends a clear message that the Board will not let the discount persist.

By establishing a fund that can actively trade these shares, the manager can essentially arbitrage the discount themselves. This signals to the market that the manager believes the shares are undervalued, which typically acts as a floor for the share price and discourages short-sellers or aggressive discount hunters.

At the same time, the company will continue to buy back its shares. In fact, earlier in the year the Board increased its annual buyback allowance from 5% to 14.99% of shares in issue. Previously, if the Company bought back more than 5% of its shares, it had to pay a 2% penalty fee to the manager. The Board has successfully negotiated the removal of this fee for 2026, meaning they can now buy back nearly 15% of the shares without incurring extra costs.

Since the programme was initiated, and up until 30 June 2026, the company has bought back 77.5m shares, or 21.4% of the total. The buyback has been accretive to the NAV to the tune of 2% and has had a positive impact on the size of the discount. The main negative is that the move potentially reduces the liquidity of the shares. Given the 16.4% Rathbones holding, the 14.99% buyback authorisation, and potential demand from the new private fund, the liquidity of the shares may become an issue for potential shareholders. This is further compounded by a broader trend across the UK wealth management sector, where rapid corporate consolidation has created mega-firms managing pools of capital that are increasingly too large to deploy into a £1.5bn trust without hitting strict underlying position limits.

Another discount control mechanism is the Class Closure Resolutions which can be triggered if the average month-end discount to NAV for a share class exceeds 8% over a calendar year. Such votes were triggered in 2025 and 2026 when 98.22% and 96.23% of shareholders respectively voted against the Sterling class closure.

In the first half of this year to 26 June, the NAV is up 2.9%. This comes against a backdrop of strong equity markets (MSCI Global in Sterling terms: +10%), highlighting that BH Macro can move sideways or drift downward during extended periods of grinding bull markets. However, as a result of the action taken by the company, the discount has reduced from 9.5% to 5.9%, and the share price has risen by 7.0%.

We remain very positive on the company given its portfolio diversification attributes at a time when the macro-economic and geopolitical backdrop remains challenging. Global uncertainty continues to weigh on markets, especially owing to an evolving and increasingly complex conflict in the Middle East. President Trump continues to act unconventionally both domestically and on the international stage. Looking ahead, it remains to be seen what impact this will have on the November 2026 midterm elections. We believe this all provides a rich opportunity set for macro trading.

Source: Bloomberg