Morning Note: Market News and an Update from Anheuser-Busch InBev.

Market News

Stocks pulled back from record highs and the dollar strengthened as tension in the Middle East escalated, fuelling inflation concerns. The US and Iran exchanged fire in the Persian Gulf, jolting a fragile four-week-old ceasefire. The American military fought off attacks as it facilitated the passage of two US-flagged vessels through the Strait of Hormuz. Donald Trump said the war may last another two to three weeks in comments to Salem News Channel.

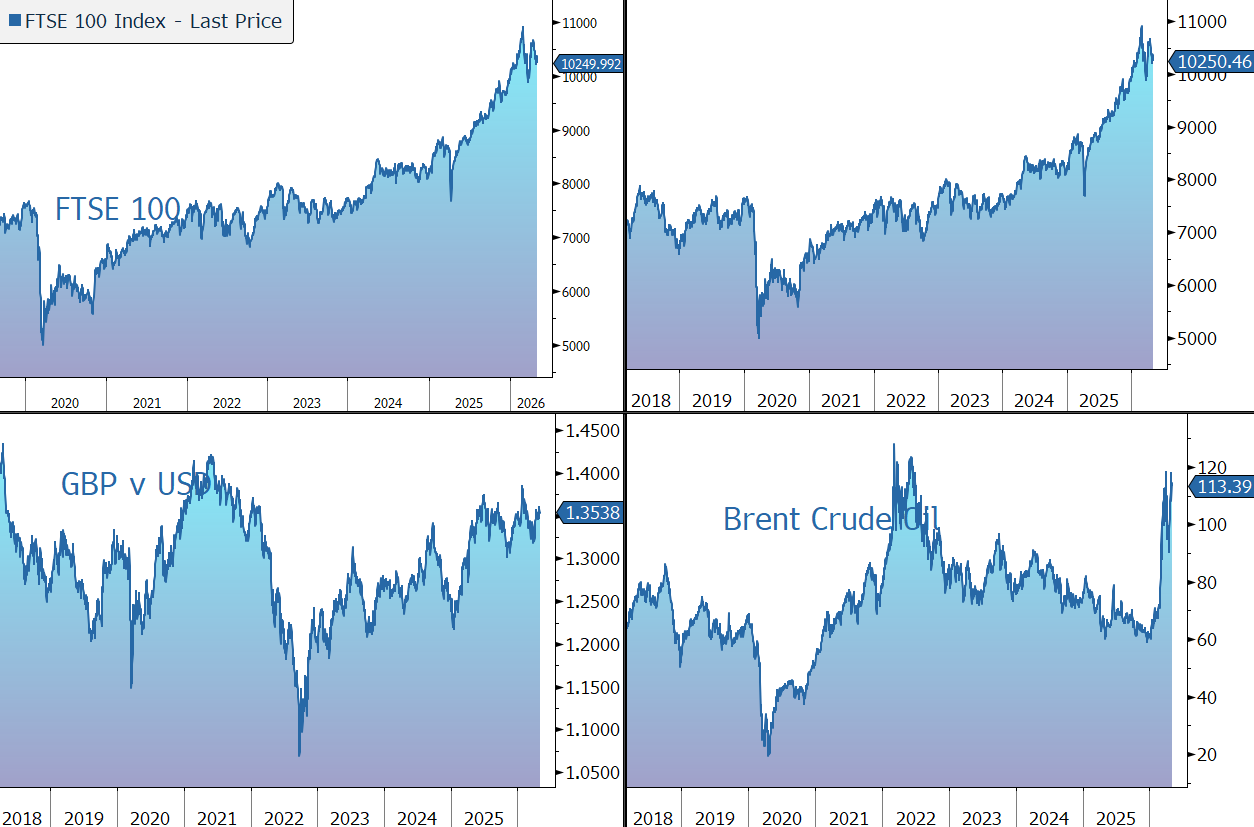

A rally in oil saw the global benchmark Brent Crude rise to $113 a barrel. Global inventories are being drawn down rapidly, Goldman said, with stocks expected to fall to about 98 days of demand by the end of May from 101 days at present. Following a 2% drop yesterday, gold is steady at $4,550 an ounce, while the yield on the US 10-year Treasury is 4.44%

US equities fell from their high last night: S&P 500 (-0.4%); Nasdaq (-0.2%). Big tech was mostly lower though Amazon fared best on its logistics announcement. The main gainer was Energy. In Asia, trading was thin with Japan, China and South Korea all closed for holidays. The Hang Seng fell by 1.1%.

The FTSE 100 is currently down 0.4% at 10,250, while Sterling trades at $1.3540 and €1.1580. HSBC missed estimates after setting aside money for fraud-related exposure and the Middle East conflict. Pre-tax profit for the first three months of the year was $9.4bn, lower than expectations of $9.6bn. The shares are down 5% in early trading.

The European Central Bank’s Joachim Nagel sees a case for a rate hike without marked inflation progress. Europe is facing “a stagflationary shock,” EU Economy Commissioner Valdis Dombrovskis said. The 10-year German Bund yield is currently 3.08%, back up toward recent highs.

Source: Bloomberg

Company News

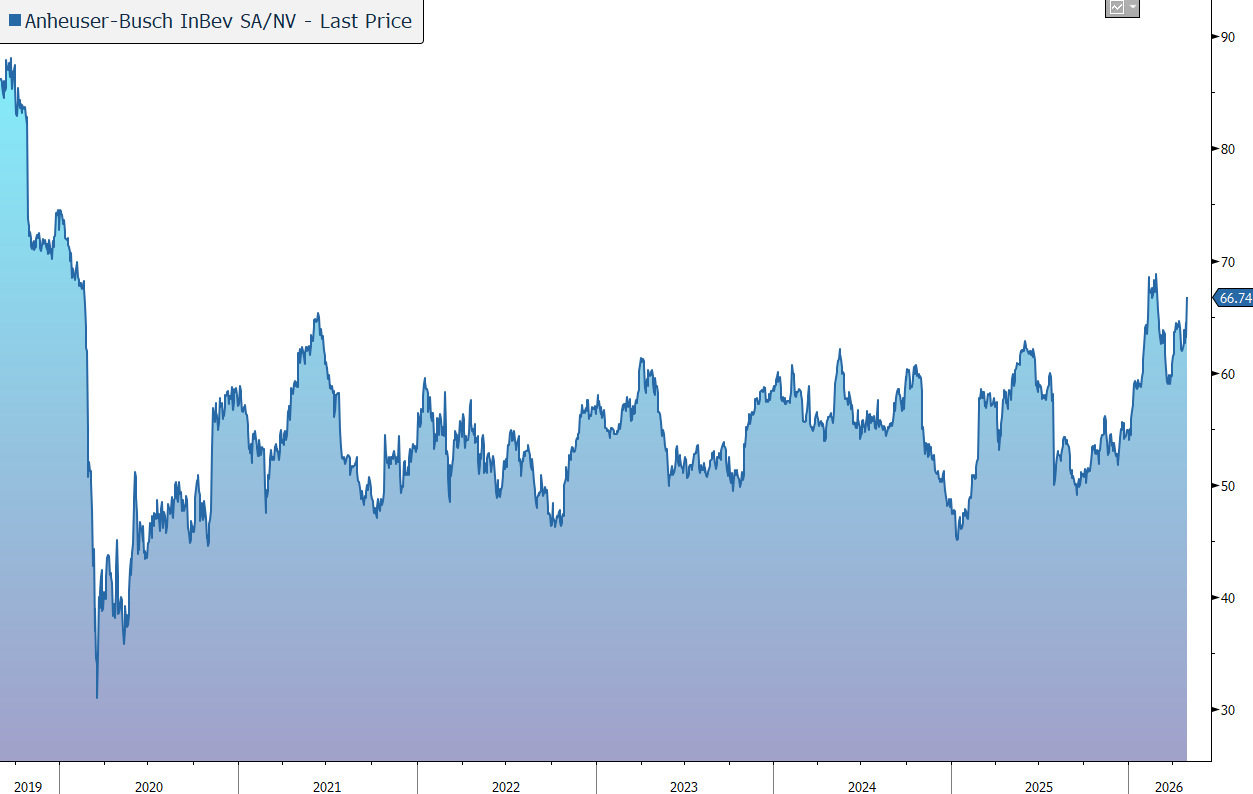

Anheuser-Busch InBev has this morning released Q1 results which were ahead of market expectations, driven by broad-based volume growth, revenue management, and positive mix. Full-year profit guidance has been confirmed. In response, the shares are up 6% in early trading.

AB InBev is a global brewing company with more than 500 beer brands, including Budweiser, Stella Artois, Becks, Corona, Modelo, and Leffe. The group’s premium portfolio represents over 30% of revenue and continues to benefit from the global trend to ‘drink less, drink better’. New products continue to contribute to growth, with the group’s innovation portfolio making up 10% of revenue. The portfolio has been expanded to address key consumer trends in health and wellness (low and no alcohol) and into products beyond beer (i.e. hard seltzers and canned cocktails). In 2025, the company generated sales of more than $59bn.

In the three months to 31 March 2026, revenue grew by 5.8% in organic terms to $15.3bn. Revenue per hl was up 4.5%, driven by revenue management and positive mix from premiumisation and Beyond Beer. Total volume rose by 0.8% during the quarter, when the market was expecting a decline. The result was made up of beer up 1.2% and non-beer down 1.9%.

Organic volume growth in EMEA (+1.3%) and Middle Americas (+4.8%) offset a decline in South America (-0.3%), North America (-3.1%), and Asia Pacific (-0.4%). The group enjoyed record high first-quarter volumes in Mexico, Colombia, Brazil, South Africa, and Peru. The company estimates to have gained or maintained market share in 75% of its markets.

Combined revenue of the group’s global mega brands (Budweiser, Stella Artois, Corona, and Michelob Ultra) grew by 8.2% outside their home markets.

The premium portfolio grew revenue at 11% The global no-alcohol beer portfolio continued to outperform, delivering 27% revenue growth in the quarter. Beyond Beer continued to add profitable growth, increasing revenue by 37%, led by the global expansion of Flying Fish and by Cutwater in the US.

Investment in direct-to-consumer ecommerce platforms continued to pay off and the group now generates 72% of its revenue through B2B digital platforms. There was a 55% increase in Gross Merchandise Value from sales of third-party products through the BEES Marketplace to reach $1.1bn.

EBITDA, the group’s key measure of profitability, grew by 5.3% in organic terms to $5,437m, better than the market forecast for growth of 2.6%. The margin slipped by 15 basis points to 35.6%, as disciplined overhead management enabled increased sales and marketing investments and offset transactional currency headwinds. Underlying EPS rose by 8.8% on a constant currency basis to 97c.

The group’s priority for capital allocation is to invest behind its brands and to take full advantage of organic growth opportunities. In 2026 the company expects to spend between $3.5bn and $4.0bn. Second is deleveraging the balance sheet back towards the optimal level of 2x net debt to normalised EBITDA – at the end of 2025, the ratio was 2.87x. The final priority is the return of excess cash to shareholders in the form of dividends and share buybacks – a $6bn share buyback programme was announced in October 2025, of which $1.4bn has been completed. The full year dividend was €1.15 (1.7% yield).

Looking forward, the group continues to expect EBITDA to grow in line with its medium-term outlook of 4%-8%.

Source: Bloomberg