Morning Note: Market News and an Update from Diageo.

Market News

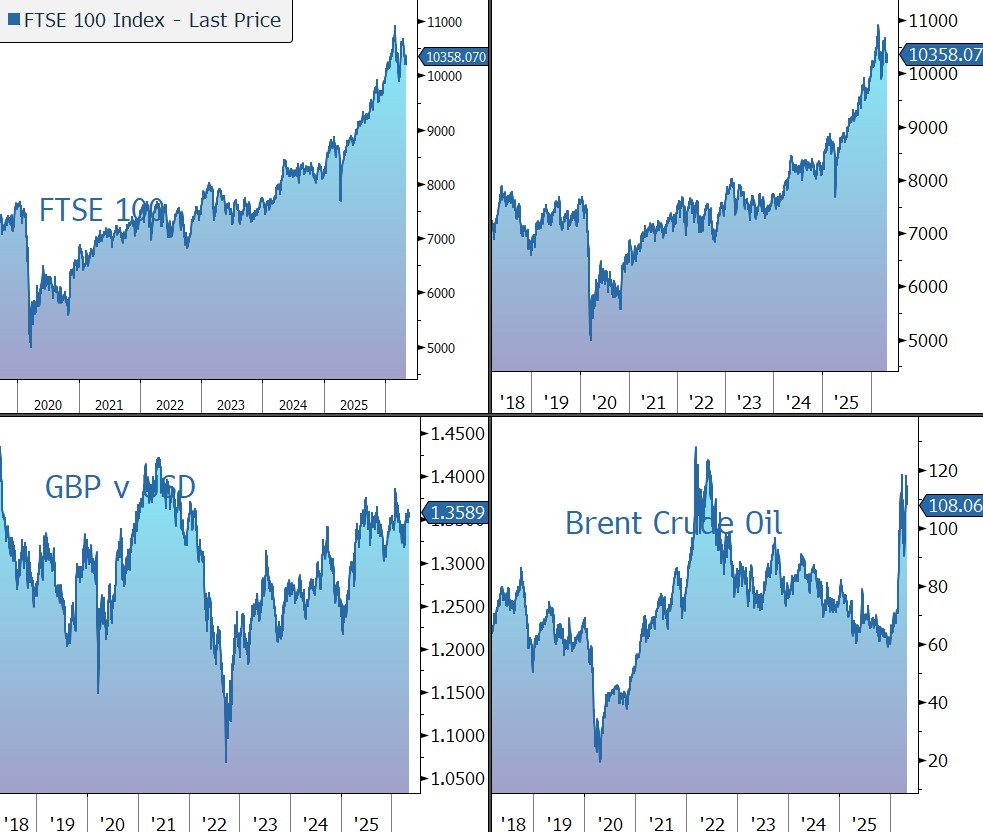

Stocks climbed to a record and Brent Crude fell to $108 a barrel after President Trump signalled progress toward a final agreement with Iran. The president said he would pause a US-led effort to help stranded ships exit the Strait of Hormuz. The naval blockade on Iranian ports will remain in force. Iran’s foreign minister met with China’s top diplomat in Beijing, just days before Trump is due to arrive for an expected summit with Xi Jinping. Gold moved up to $4,666 an ounce, while the yield on the US 10-year Treasury slipped to 4.38%.

US equities powered to a new high last night – S&P 500 (+0.8%); Nasdaq (+1.0%) – spurred on by tech stocks. Google owner Alphabet raised almost $17bn from debt sales for its latest AI push. This comes as Anthropic plans to spend about $200bn with Google over five years, according to the Information.

In Asia, equities also moved higher: Nikkei 225 (holiday); Hang Seng (+0.9%); Shanghai Composite (+1.2%). China’s services activity unexpectedly improved in April, a private survey showed, indicating firms were absorbing war-led price shocks. DeepSeek is nearing a $45bn valuation amid financing talks with a Chinese state-backed fund, the FT reported.

The FTSE 100 is currently up 1.4% at 10,358, while Sterling trades at $1.3590 and €1.1585. UK 10-year gilt yields remained above 5%, close to levels last seen in 2008, as investors anticipated potential Bank of England interest rate hikes to tackle inflation. Attention is also on tomorrow’s local elections, with polls suggesting a possible setback for PM Keir Starmer’s Labour Party.

Private credit offers significant benefits to the financial system but remains untested in a severe economic downturn, Bank of England Governor Andrew Bailey wrote in the FT.

Source: Bloomberg

Company News

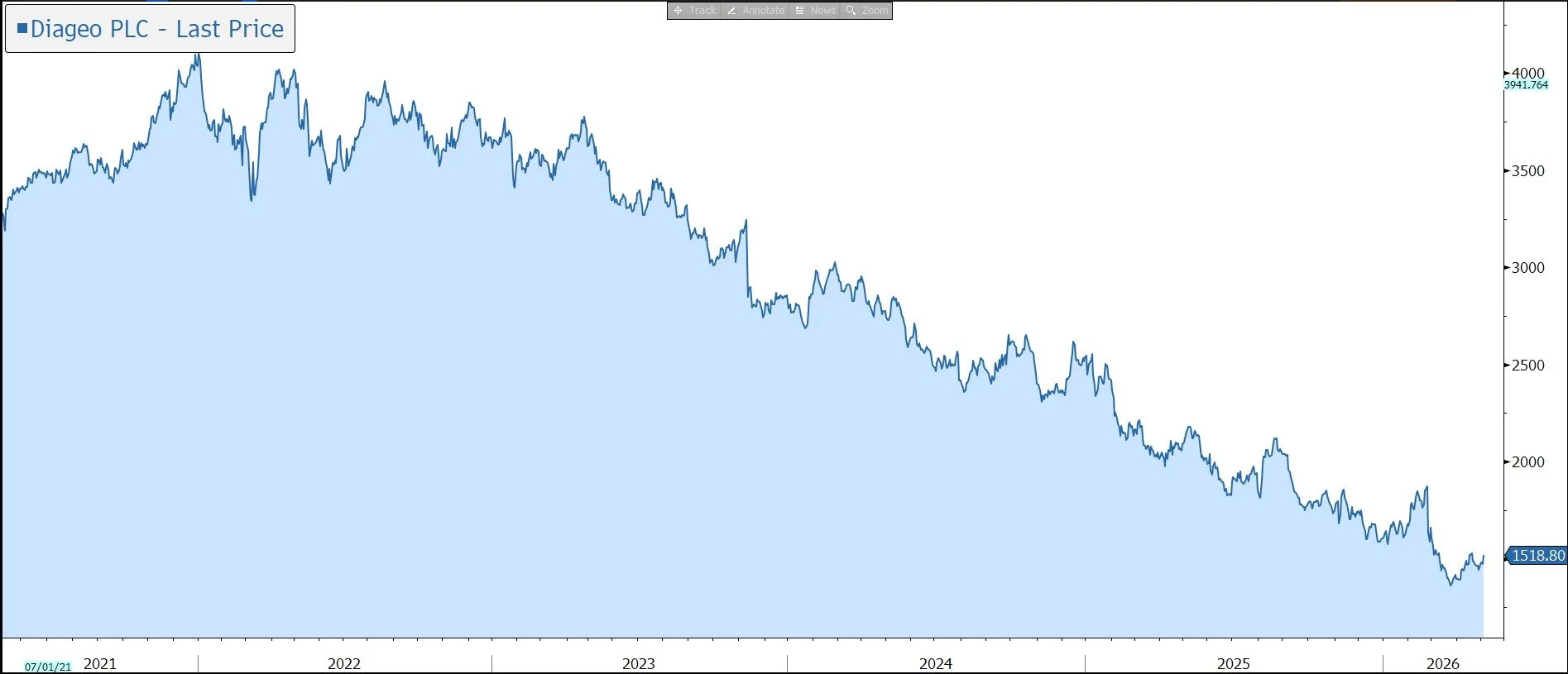

Diageo has released a trading statement for the three months to 31 March 2026, the third quarter of its financial year to 30 June 2026. The company posted surprising sales growth, albeit helped somewhat by one-off factors. Performance was driven by strong growth in Europe, Latin America, and Africa, offset by weakness in North America and China. The cost cutting programme is on track to deliver c.$300m savings and guidance for the full year to 30 June 2026 has been reiterated, including $3bn of free cash flow generation. Ahead of the analysts’ call, the shares have been marked up 4%.

Diageo is a leading global drinks company, with a portfolio of iconic brands including Johnnie Walker, Smirnoff, Captain Morgan, Baileys, Tanqueray, and Guinness. The company owns 13 billion-dollar brands across a broad range of categories. The group is an integrated operator, producing and supplying drinks at a variety of price points across strong global distribution routes. The company has been positioned to benefit from the trend towards premiumisation – including its 34% stake in Moet Hennessy, the group generates more than 60% of its sales from high margin, premium brands. Diageo also has a strong presence in under-penetrated emerging markets, where the number of people of legal purchasing age is set to increase by over 600m by 2030. Wealth is also increasing in these regions, with the middle class expanding, and consumers shifting from local products to higher-margin international brands.

However, the global industry environment has been challenging. In addition to a rebasing of consumer spending in the aftermath of the pandemic spending boom, the sector faces potential headwinds from weight-loss drugs, health warnings, Gen-Z moderation, and cannabis consumption.

The data the company is currently seeing shows penetration and frequency of spirits consumption as broadly stable, including among younger cohorts, with the more meaningful change being a reduction in servings per occasion rather than outright disengagement from the category. This implies that the biggest consumption headwind may be cyclical, not structural, and that a macroeconomic upturn could be an inflection point for the sector. In the meantime, however, consumer weakness is holding back the premiumsation trend.

In the medium term, we expect the structural tailwinds to offset the headwinds, leading to positive industry growth. In addition, Diageo is focused on strengthening the resilience of its business through operational improvement, productivity gains, the introduction of innovative new products, and strategic investment to win market share. The first phase of the company’s Accelerate programme is progressing well and involves several targets including:

- to sustainably deliver $3bn free cash flow p.a. from this financial year (FY2026), increasing as the business performance improves.

- cost savings of $625m over the next three years, with 50% of the benefit expected to drop through to operating profit and the remainder reinvested in future growth.

- deleveraging the balance sheet to be well within the target range of 2.5x-3.0x net debt/EBITDA no later than FY2028. This will be delivered through a combination of organic growth and positive operating leverage, combined with tighter capital discipline, and selective disposals.

- opportunities for ‘substantial changes’ to the portfolio by offloading assets that are not ‘core or strategic’. In particular, the company is looking to offload capital intensive businesses that don’t add synergy to the group that can be sold for an attractive price.

At the beginning of the year, Sir Dave Lewis became the company’s new CEO. Lewis was the top man at Tesco and spent 27 years at Unilever. Despite having never worked in spirits before, expectations are high that his strong brand and marketing background can help turn Diageo’s fortunes around. Early in his tenure, Lewis highlighted that he can ‘already see significant opportunities for Diageo to act more decisively to enhance its competitiveness and broaden the portfolio offering leading to higher growth’. As the company refines its new strategy to deliver stronger shareholder value, the ‘immediate priorities … are clear’:

- Build competitive category strategies, winning with relevant brands – some brands need to be positioned at lower price points, to broaden the customer base, so the portfolio is fit for all stages of the economic cycle.

- ‘Customer, customer, customer’ – the CEO has admitted the company’s internal operations, systems, and processes are ‘not fit for purpose’ and that Diageo had not been ‘best in class’ in how it engages with retailers. More investment is needed in the ‘customer relationship’.

- Redesign of the Diageo operating framework to drive sustainable returns. It looks like there will be a shift away from profit margin to focus of increasing volume, expanding the gross profit pool, and generating free cash flow.

Progress on the re-design of the new strategy and the shaping of a more competitive operating framework is well underway. The company is on track to share a Strategy Update with shareholders alongside the full-year results in August. One early snippet was reported in the FT last week: an increased focus on canned cocktails. This is a fast-growing market, albeit competitive and profit margin dilutive. It is unclear whether the company will expand via acquisition or through the extension of existing brands.

In the meantime, the company has highlighted that trading conditions in the three months to 31 March 2026 remained challenging, reflecting macroeconomic and geopolitical uncertainty as well as weak consumer confidence in many markets.

Reported net sales rose to 2.3% to $4,477m. Organic net sales (which exclude M&A and currency movements) rose by 0.3%, driven by 0.4% growth in organic volume and negative price/mix of 0.1%. However, the results were well ahead of the market expectation for a 2.3% decline, helped somewhat by the timing of Easter and the Chinese New Year, combined with advance sales ahead of the upcoming FIFA World Cup.

North America, the group’s largest market, remains the biggest challenge, where market conditions are soft and Diageo’s offer needs to be more competitive. Actions are already underway to address this. During the quarter, organic sales fell by 9.4%, including a 15.4% decline in US Spirits due to tough year-on-year comparatives.

The company generated strong organic net sales growth in Europe (+8.8%, led by Guinness in Great Britain and Ireland), Latin America and Caribbean (LAC, +16.2%, with some benefit from buy-in ahead of the World Cup and Easter timing), and Africa (+17.1%, despite a 3.1% decline in price/mix). Finally, Asia Pacific fell by 0.8%, driven by continued weakness in Chinese white spirits, which more than offset low-single-digit growth in international premium spirits in the region.

As expected, this update only covers sales, so there is less detail on profitability or the group’s financial position. The main comment is that the Accelerate programme is on track to deliver c.$300m savings by end of June.

At the last balance sheet date (31 December 2025), net debt stood at $21.7bn, with financial gearing of 3.4x net debt to adjusted EBITDA. The company remains committed to returning to its target range of 2.5x-3.0x ‘no later than’ FY2028 and by then gearing will be in the middle of the range.

This will be helped by the sale of the company’s shareholding in East African Breweries and its shareholding in the Kenyan spirits business, expected to raise $2.3bn. On completion in H2 calendar year 2026, net debt to adjusted EBITDA will be reduced by 0.25x. In March, United Spirits Limited (owned 56% by Diageo) announced the sale of its 100% stake in Royal Challengers Bengaluru (RCB) cricket team for a total consideration of INR 166.6bn ($2bn). The market’s expectation is that Diageo will receive a special dividend from USL for its share of the after-tax proceeds.

In the meantime, and in order to create more financial flexibility, the company has rebased its dividend – a saving of $1.2bn. The company is committed to growing shareholder distributions over time and is targeting a 30%-50% payout policy going forward, with a minimum floor set for the dividend of 50c p.a., 52% lower than last year and a yield of 2%. An interim payment of 20 cents was declared at the time of the results in February.

Diageo has a long-term track record of coping with tariffs. On a positive note, last week President Trump announced the removal of Tariffs and Restrictions on Whisky. The company has previously disclosed that a 10% tariff rate would drive a $150m gross profit impact (2.5%), with roughly half mitigated by internal actions. That leaves the 15% tariff on imports from Europe, the gross impact of which is $50m.

Although the company is mindful of continued geopolitical uncertainty, including the impact of the ongoing conflict in the Middle East on energy, supply and distribution, the guidance for the financial year to June 2026 has been reiterated:

· Organic sales are expected to be down by 2%-3%.

· Organic operating profit growth is expected to be to be flat to up low-single-digit. This includes the impact of tariffs and the faster rate of cost savings, with 50% of the Accelerate savings now expected in this financial year.

· free cash flow guidance of $3bn, before c.$100m one-off working capital impact expected at the end of FY2026 from inventory build ahead of the SAP S/4 HANA ERP system implementation in early FY2027.

The recent collapse of merger talks between rivals Pernod Ricard and Brown-Forman is positive for Diageo as it removes the threat of a newly enlarged challenger. A tie-up would have created a more formidable, with a larger whiskey portfolio, greater scale, and the ability to leverage each other’s distribution networks in key markets.

Source: Bloomberg