Morning Note: Market News and an Update from Shell.

Market News

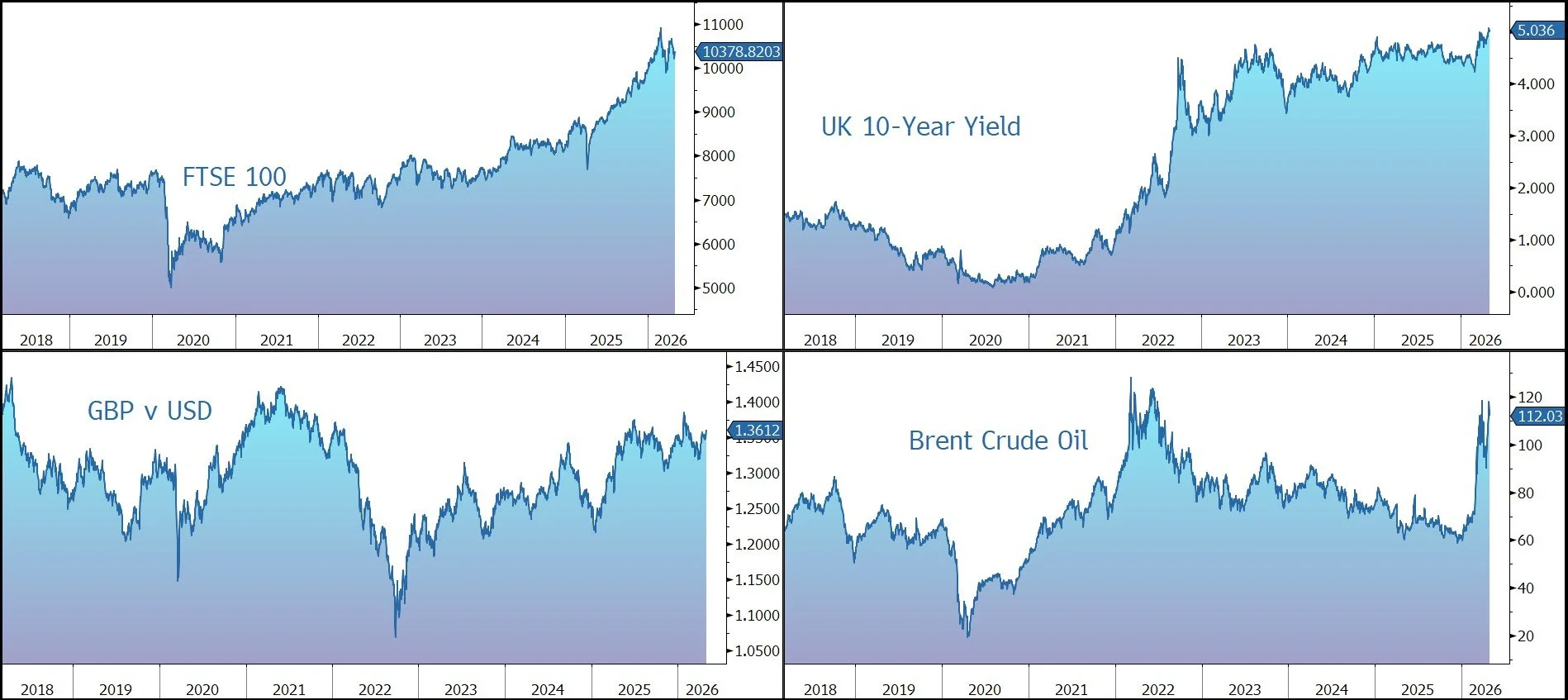

Brent Crude remains firm at $110 a barrel, amid dimming prospects for a US-Iran peace deal and expectations that the Strait of Hormuz would not reopen anytime soon. Gold is trading just below $4,600 an ounce, while the yield on the US 10-year Treasury 4.39%.

US equities rose last night – S&P 500 (+1.0%); Nasdaq (0.9%) – spurred on by a 9% rally in Google owner Alphabet. Apple rose 3% after-hours after posting revenue and guidance ahead of market expectations.

In Asia, equities nudged higher in holiday-thinned trading: Nikkei 225 (+0.4%). The yen has bounced sharply versus the dollar after Japanese officials sent firm signals about possible intervention. Finance Minister Satsuki Katayama said the timing to take ‘decisive’ action in the market was nearing. Although the Finance Ministry has not formally confirmed intervention, the sharp and sudden move led traders to widely attribute the action to government support. The yen is currently around 156 vs. the dollar, having bottomed at 160.72, its highest level since July 2024.

All of the large European stock markets are closed for a holiday today. The UK is open but closed on Monday. The FTSE 100 is currently 0.4% lower at 10,338. Diageo is firm following news that President Trump is to remove the Tariffs and Restrictions on Whisky. The company has previously disclosed that a 10% tariff rate would drive a $150m gross profit impact (2.5%), with roughly half mitigated by internal actions. The company is scheduled to release a trading update next Wednesday.

Sterling firmed to $1.3605 and €1.1595 after the Bank of England held its Bank Rate at 3.75% in an 8–1 vote, but several policymakers signalled they could still consider additional rate increases in the future. The BoE described current rates as ‘reasonable’ and reiterated it ‘stands ready to act as necessary’ to steer CPI inflation toward its 2% medium-term target. The 10-year Gilt yield is currently touch above 5%.

Source: Bloomberg

Company News

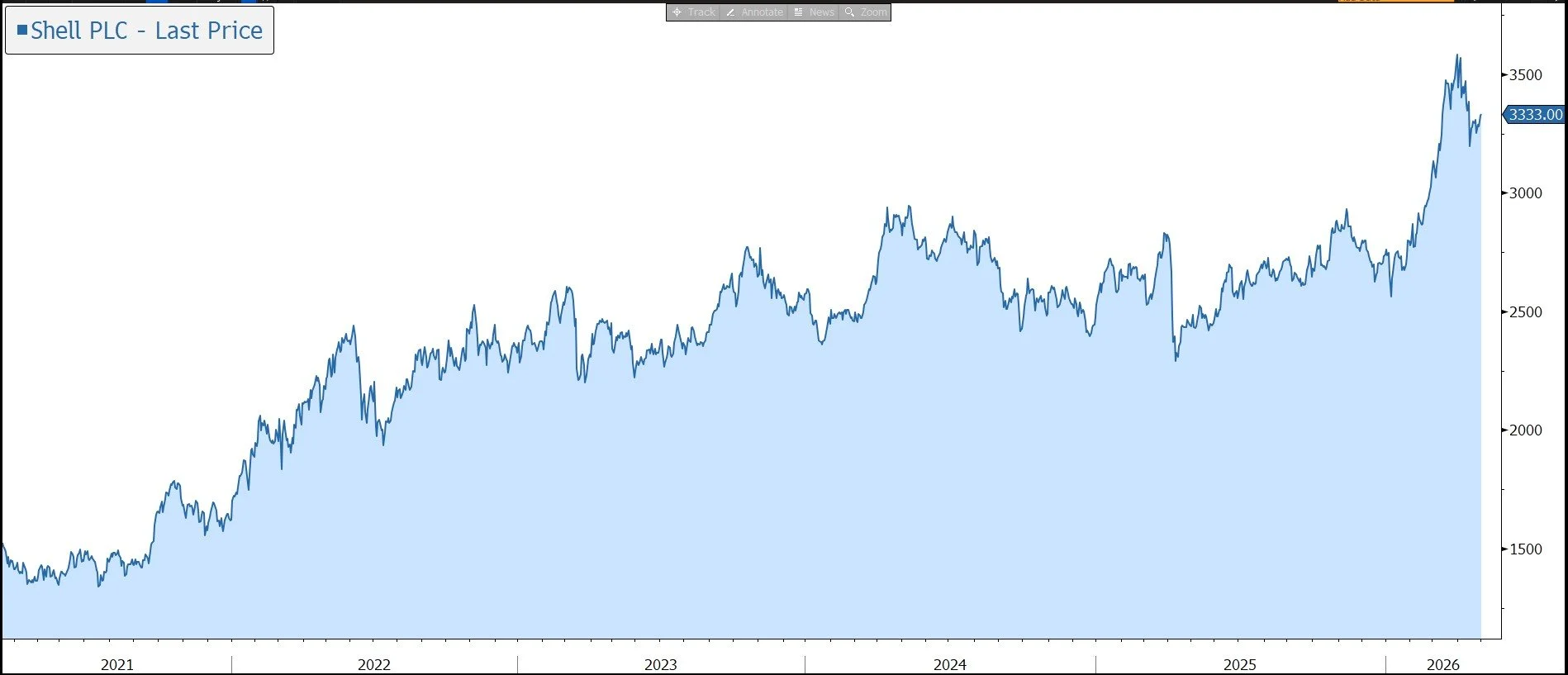

Earlier in the week Shell announced a $16.4bn acquisition of Canadian energy company ARC Resources. The deal adds complementary oil and gas assets in a shift back toward stable, democratic jurisdictions for long-term supply. It helps address the group’s shrinking reserve life and is expected to be free cash flow accretive from 2027. With 75% of the transaction cost funded from the issue of new Shell shares, the company retains cash reserves for dividends and share buybacks.

Shell has agreed to acquire Canadian energy company ARC Resources for an equity value of US$13.6bn, plus $2.8bn in net debt and leases, resulting in an enterprise value of $16.4bn.

The transaction increases Shell’s exposure to long-duration, low-cost, and top quartile low carbon intensity shale gas and liquids production in Canada’s Montney basin in British Columbia and Alberta. The assets overlap Shell’s existing footprint in Canada: Groundbirch in British Columbia and Gold Creek in Alberta. The deal also complements Shell’s existing LNG footprint and extensive downstream businesses including refining, chemicals, fuel retail, aviation, lubricants, and low-carbon solutions.

We note current media reports that a number of private equity companies are bidding to acquire a share of Shell’s 40% stake in LNG Canada, although the company has said it is not necessarily looking at reducing its equity interest but is keen to generate cash from lower-return parts of its business and where it is not the natural owner.

ARC will add 370 kboe/d of production to Shell’s 2.8m b/d output. It means its production CAGR will increase from 1% to 4% between 2025 and 2030 and supports its aim to sustain material liquids production of 1.4m barrels per day towards 2030 and beyond. The deal also adds 2bn barrels of oil equivalent proved plus probable reserves at the end of 2025. Last year, 40% of ARC’s production was liquids, which accounted for 70% of its revenue, and 60% was gas.

The transaction is expected to bring annualised synergies of around $250m within a year of closing. Shell expects to absorb the additional organic cash capital expenditure within its existing capex ceiling, post 2026. The cash capex range for 2027 to 2028 will remain unchanged at $20bn–$22bn. As a result, the deal is expected to generate double-digit returns and be accretive to free cash flow per share from 2027.

The acquisition will be financed by a 25%/75% mix of CAD 8.20 cash and 0.40247 Shell ordinary shares per ARC share (228m new Shell shares). It represents a 20% premium to ARC’s 30-day VWAP. This means Shell is using its highly-valued stock as currency while keeping its cash reserves for shareholder buybacks.

The boards of both companies have unanimously supported the transaction, which is expected to close in the second half of 2026, subject to ARC shareholder, court, and regulatory approvals.

Importantly, the company’s shareholder distribution policy remains unchanged, with distributions of 40%-50% of CFFO through the cycle via the company’s 4% progressive annual dividend growth and buybacks.

Although the timing of this deal against the backdrop of the Middle East conflict looks strange, we believe it is positive. It helps to address the one major criticism that has dogged the stock: its shrinking reserve life – at present Shell is facing a projected production shortage of roughly 350,000 to 800,000 boep/d by the early 2030s as older fields mature. In addition, with an eye on security of supply, the deal signals a shift back toward stable, democratic jurisdictions for long-term production.

Source: Bloomberg