Morning Note: Market News and an Update from Heineken.

Market News

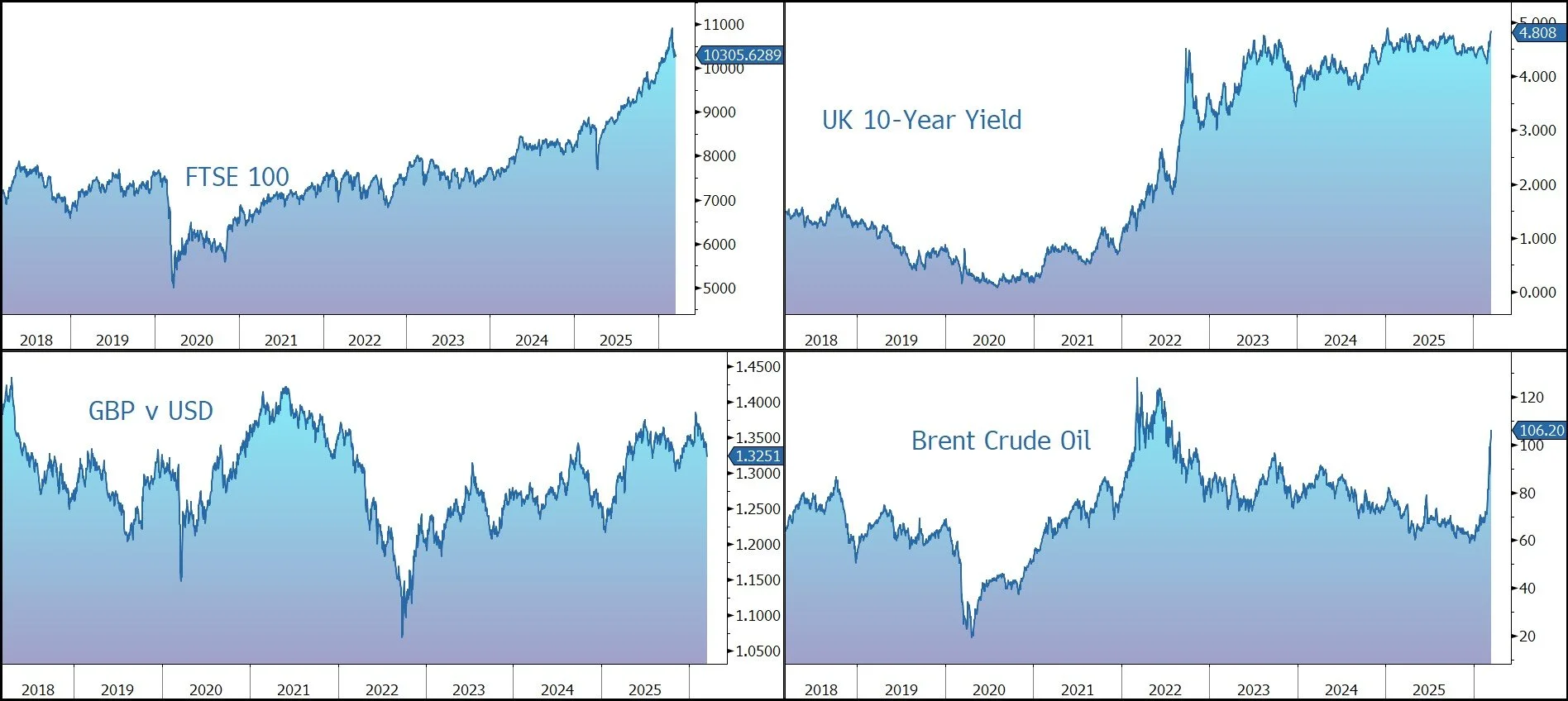

Equity markets stabilised and crude oil gave up part of its early surge as President Trump raised pressure on nations to help reopen the Strait of Hormuz and said the US was talking to Iran. The President said his planned summit with Xi Jinping may be delayed if China doesn’t assist in unblocking Hormuz. European leaders pressed Trump on his end-game strategy during a recent G-7 call, people familiar said.

Brent traded around $104 a barrel after earlier climbing as high as $106.50 following US strikes on military targets on Kharg Island, the terminal that handles almost all of Iran’s oil exports. Highlighting pressure on global supply, the IEA said oil from last week’s record 400-million-barrel reserve release will be made available immediately in Asia.

The US Core PCE Price Index, the Federal Reserve’s preferred inflation gauge, rose by 3.1% in January, in line with expectations. The Fed, ECB, and Bank of England are expected to hold rates steady this week, adopting a cautious tone along with the other 18 central banks setting policy. Of the big three, only the Fed is projected to cut borrowing costs anytime soon. Bond yields remain elevated – the 10-year Treasury currently yields 4.27%. The dollar declined slightly, while gold slipped below $5,000 an ounce.

In Asia this morning, markets were mixed: Nikkei 225 (-0.2%); Hang Seng (+1.4%); Shanghai Composite (-0.3%). China’s key economic indicators fared better than forecast to start the year. Industrial production climbed 6.3% in the January-February period from a year ago, while fixed-asset investment unexpectedly expanded 1.8%. Retail sales rose 2.8% in the first two months.

US equities are currently expected to be up 0.5% at the open this afternoon. The FTSE 100 is currently 0.4% higher at 10,306, while Sterling trades at $1.3245 and €1.1575. 10-year Gilts yield 4.75%.

Source: Bloomberg

Company News

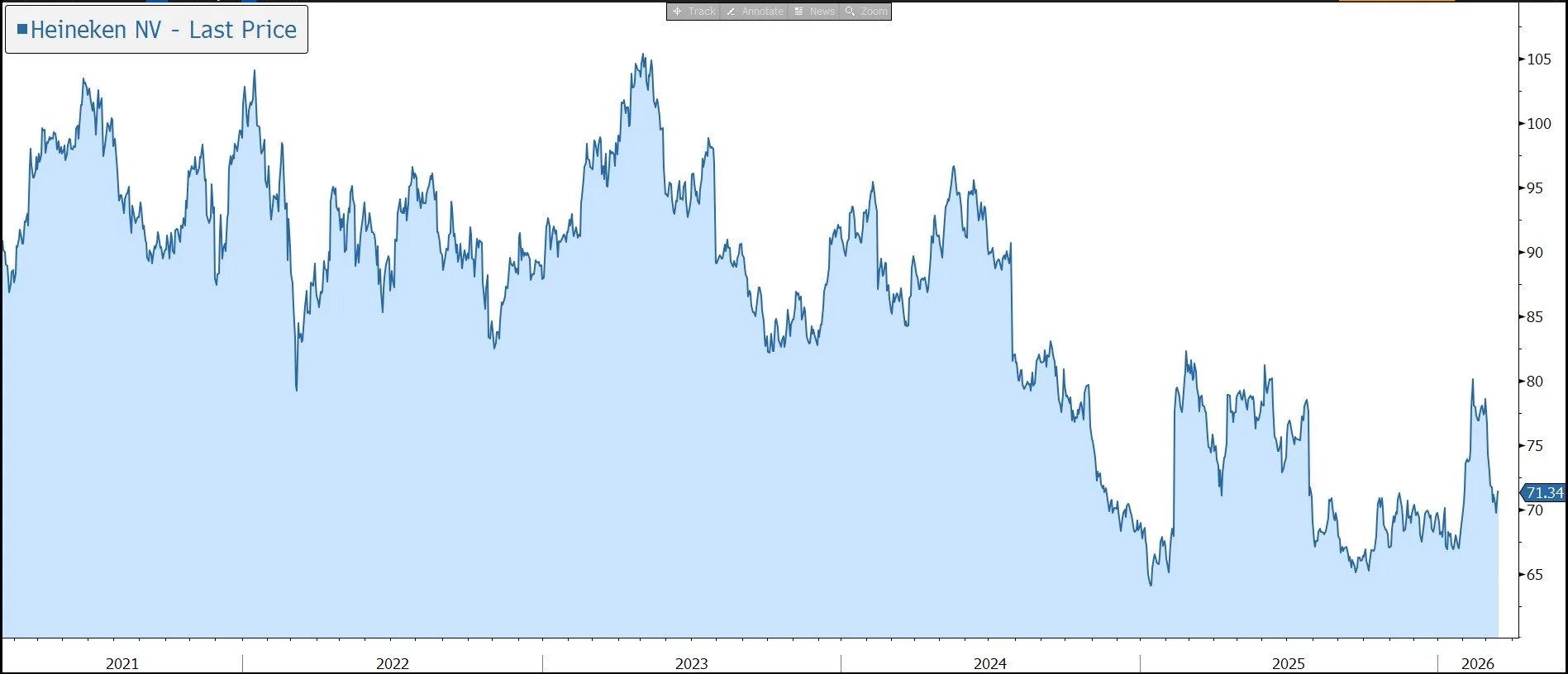

At the end of last week, the Heineken CFO, Harold van den Broek, participated in a fireside chat at the UBS Global Consumer & Retail Conference. The tone was generally one of resilience, although the session highlighted clear external headwinds and internal shifts. The company reiterated the thinking behind its 2%-6% operating profit growth guidance and talked about the process of appointing a new CEO. Heineken’s balance sheet is robust and the second tranche of its share buyback programme is underway. Given the lack of negative surprise, the shares traded up 2% on the day after the meeting.

Heineken is the world’s second largest brewer, generating net revenue of €29bn from a portfolio of iconic brands, many of which have been quenching the thirst of consumers for decades. In addition to the core Heineken brand, the company owns several well-known beers and ciders, including Sol, Tiger, Amstel, Murphy’s, and Strongbow, as well as more than 300 or so local brews. The company also owns around 2,400 pubs in the UK, runs a wholesaling operation in Europe, and has a strong global distribution capability. Over time, the group has expanded and developed its global footprint through investment in new breweries, partnerships, and acquisitions. It has also exited several businesses to refine the portfolio.

We believe the company is well placed to benefit from long-term growth opportunities in emerging markets (which generate 55% of revenue), where young and growing populations, low per-capita beer consumption, and increasing wealth are expected to drive growth. The company believes the biggest opportunity is in India, with strong prospects in Mexico, Brazil, China, Vietnam, and South Africa. Most recently, the group strengthened its position in Central America through the $3.2bn acquisition of the multi-category beverage portfolio and retail business of FIFCO, a deal that is expected to be immediately accretive to EPS.

The group generates more than 40% of its revenue from premium brands, which should outpace mainstream beer because consumers turn to better brands as they grow older and wealthier. Premium brands tend to have greater pricing power. Finally, the group is benefiting from the growth of low- and no-alcohol products, where it is the global leader, and products ‘beyond beer’ such as seltzers and ready-to-drink products.

We believe the shareholding structure, supported by family ownership, ensures the company is run for the long term and in the best interests of all shareholders.

In the near-term, however, the global industry environment is challenging, with headwinds from the impact of weight-loss drugs on alcohol consumption and the request by the US Surgeon General for alcoholic drinks to carry warnings of their links to cancer. Other structural threats include Gen-Z moderation and cannabis cannibalisation, while political risk comes from the proposed US tariffs.

However, these structural concerns are not set in stone – last summer, investment bank Jefferies commissioned a survey of 3,600 US consumers to better understand their attitudes towards alcohol, finding that although moderation was becoming increasingly important, money was the biggest impediment rather than health concerns. This implies that the biggest consumption headwind is cyclical, not structural, and that a macroeconomic recovery could be an inflection point. In addition, the industry has increased its lobbying to counter the message coming from health authorities.

Against that backdrop, Heineken’s EverGreen 2030 strategy is targeting 17 markets and fewer, bigger brands (5 global and 25 local). The aim is to grow ahead of the beer category’s +1% volume CAGR, which combined with pricing above input cost inflation, as well as positive mix, underpins the mid-single-digit revenue guidance. Productivity savings of €400m-€500m p.a. are expected to underpin organic profit growth ahead of sales growth. EPS growth is expected to outpace EBIT growth, while the cash conversion target is 90%.

At last week’s UBS Global Consumer & Retail Conference, the Heineken CFO, Harold van den Broek, presented a generally resilient tone, although the session highlighted clear external headwinds and internal shifts.

Earlier in the year, the company announced that its Chairman of the Executive Board and CEO Dolf van den Brink would step down from his position on at the end of May. The timing came as a surprise given the CEO’s recent commitment to the financial targets. At the UBS conference, the CFO was incredibly firm that this leadership change does not signal a pivot in strategic direction. The role will involve disciplined execution rather than strategic reinvention. The search for a successor is the Supervisory Board’s number one priority, but the management team is effectively ‘running on rails’ provided by the existing strategy. This strategy is not just the current CEO’s plan, but a collective blueprint co-authored by the entire Executive Team. That said, until there is more visibility over the appointment, the market will remain wary, especially given it is unclear whether the new CEO will be internal or external.

The CFO reiterated the thinking behind its operating profit growth guidance of 2%-6% - it is seen as a prudent target given weak consumer sentiment and uncertain macroeconomic backdrop, factors beyond the Heineken’s control. The company is instead focusing on things it can control such as building market share and reducing costs.

He explicitly mentioned that the situation in the Middle East doesn't make things easier, suggesting potential supply chain or energy cost pressures that could weigh on margins

Looking at the EverGreen 2030 strategy, the CFO painted a picture of a company transitioning from a federation of local units – a legacy of multiple acquisitions over the years – to a more centralised, data-driven machine.

He highlighted Freddy.ai, the company's in-house digital marketing agency. By centralising data and using AI for consumer insights, Heineken expects to significantly improve marketing efficiency, pricing agility, and speed-to-market across its global footprint.

Despite a mixed global economy, the company remains focused on premiumisation. The CFO noted that while only 25% of the portfolio is currently managed as global brands, they have identified five additional brands with the potential to scale globally, reducing reliance on the flagship Heineken brand.

During his chat, Van den Broek provided an update of current trading conditions around the world which highlight a wide divergence between markets.

- In Europe, the company struggled last year with a number of high-profile de-listings by major retailers across France, Germany, and the Netherlands. Heineken had pushed for significant price increases to cover input cost inflation and rising wages. Retailers resisted, leading to products being temporarily pulled from shelves. However, agreements for 2026 are largely settled. In a market where the consumer has become highly price sensitive, Heineken is using data from their digital backbone to see exactly where price hikes cause consumers to switch to private label or cheaper competitors. Consequently, the company is being more surgical with pricing in 2026 – raising prices on premium brands while being more cautious with mainstream local brands to avoid losing market share.

- In Vietnam, after a strong recovery in 2025, this year appears to have got off to a good start with a positive Tet (lunar new year) and skew to premium brands. However, the general shift to mainstream brands seen last year remains, with a negative mix impact on margins that has been incorporated into the group’s operating profit guidance.

- Mexico is the ‘gold standard’ for Heineken’s digital integration. However, the current trading environment was described as ‘improving but intensely competitive.’ After mistakes with pricing, the company is now using data to offer the right pack sizes at the right price points to keep consumers from switching to cheaper rivals.

- In Brazil, the recent capacity expansions are already being utilised to meet high demand and has led to increased distribution efficiency. This will hopefully improve the group’s management of stock levels where it struggled during periods of high demand.

- India was described as a large, untapped market opportunity that will develop slowly over the long term. The regulatory environment is becoming more predictable and allowed the company to plan longer-term infrastructure investment.

- Cambodia is currently struggling due to structural and competitive challenges that haven't yet bottomed out. The unit is in the ‘resolve’ bucket with a choice of ‘Fix, Partner, or Exit.’ Note the country only accounts for around 1% of group revenue.

Heineken has a robust balance sheet. At the end of 2025, financial gearing was 2.2x net debt to EBITDA, below the long-term target to be below 2.5x. Although capital investment is set to increase in some markets to support growth (e.g. India), overall, the company is past the peak, with capex/sales expected to fall back from 8% to 7%. There are also still significant opportunities to reduce working capital. As a result, the outlook for free cash flow is positive.

This all means the company can return capital to shareholders - the second €750m tranche of the group’s €1.5bn share buyback programme is expected to complete by next January.

Source: Bloomberg