Morning Note: Market News and Updates from Walmart and Deere.

Market News

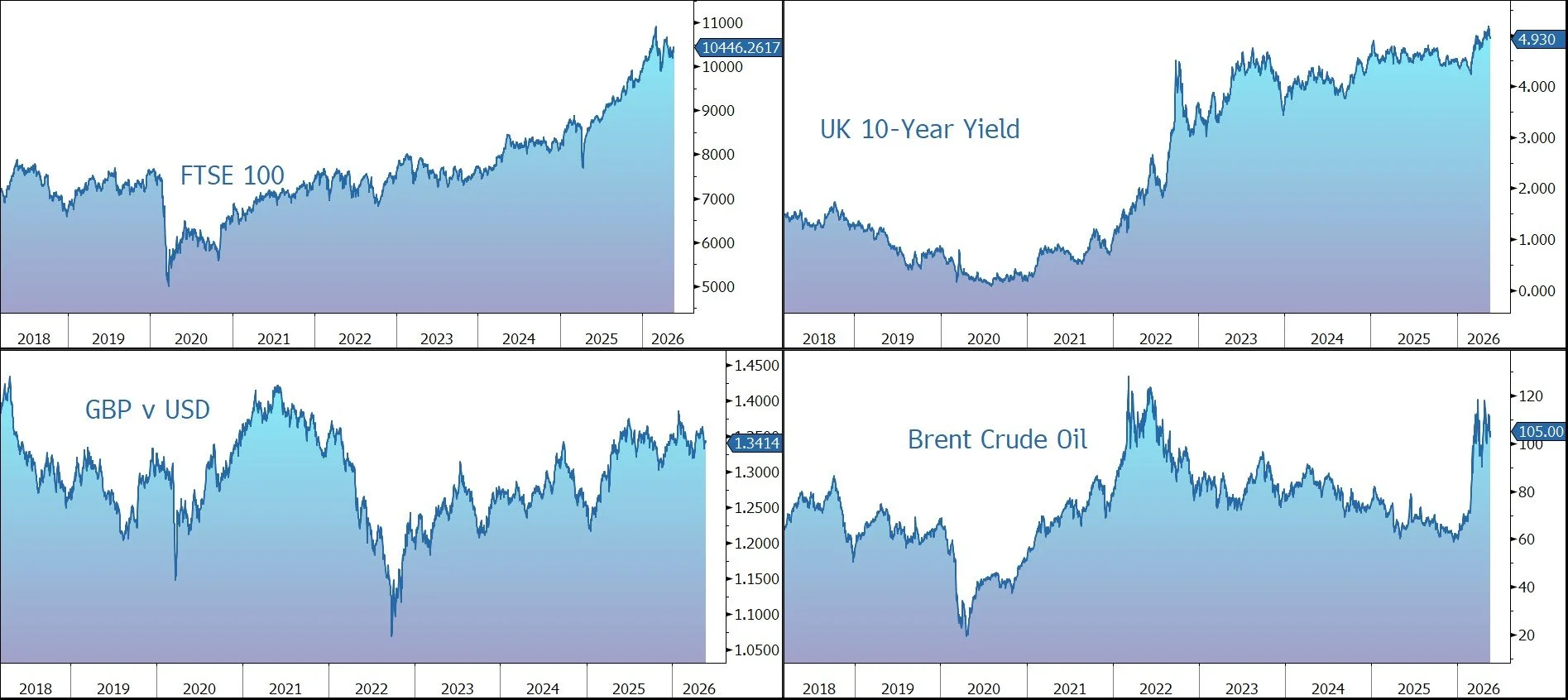

US-Iran talks recorded “some good signs” and narrowed differences on certain issues, yet the Strait of Hormuz and verification mechanisms remain unresolved. Brent Crude trades at $105 a barrel, while gold is $4,520 an ounce.

US equities edged up last night – S&P 500 (+0.2%); Nasdaq (+0.1%) – and continued to rise in the futures market. In Asia, equities rose as investors rotated into a broader set of AI-linked companies: Nikkei 225 (+2.7%); Hang Seng (+0.8%); Shanghai Composite (+0.9%). DeepSeek has told investors in its $10bn funding round that it will prioritise breakthrough AI research and open-source model development over near-term commercialisation.

The FTSE 100 is currently 0.3% higher at 10,446, while Sterling trades at $1.3425 and €1.1565. The UK’s deficit last month totalled £24.3bn, the highest April level in six years, while retail sales fell 1.3% as the Iran war drove up global energy costs. Although UK consumer confidence edged up in May to -23 from -25 in April, beating a pessimistic consensus estimate of -28, it remained weak and consistent with a bleak near-term consumer outlook, as higher energy prices and tighter financial conditions resulting from the Iran war put a renewed squeeze on household budgets.

Source: Bloomberg

Company News

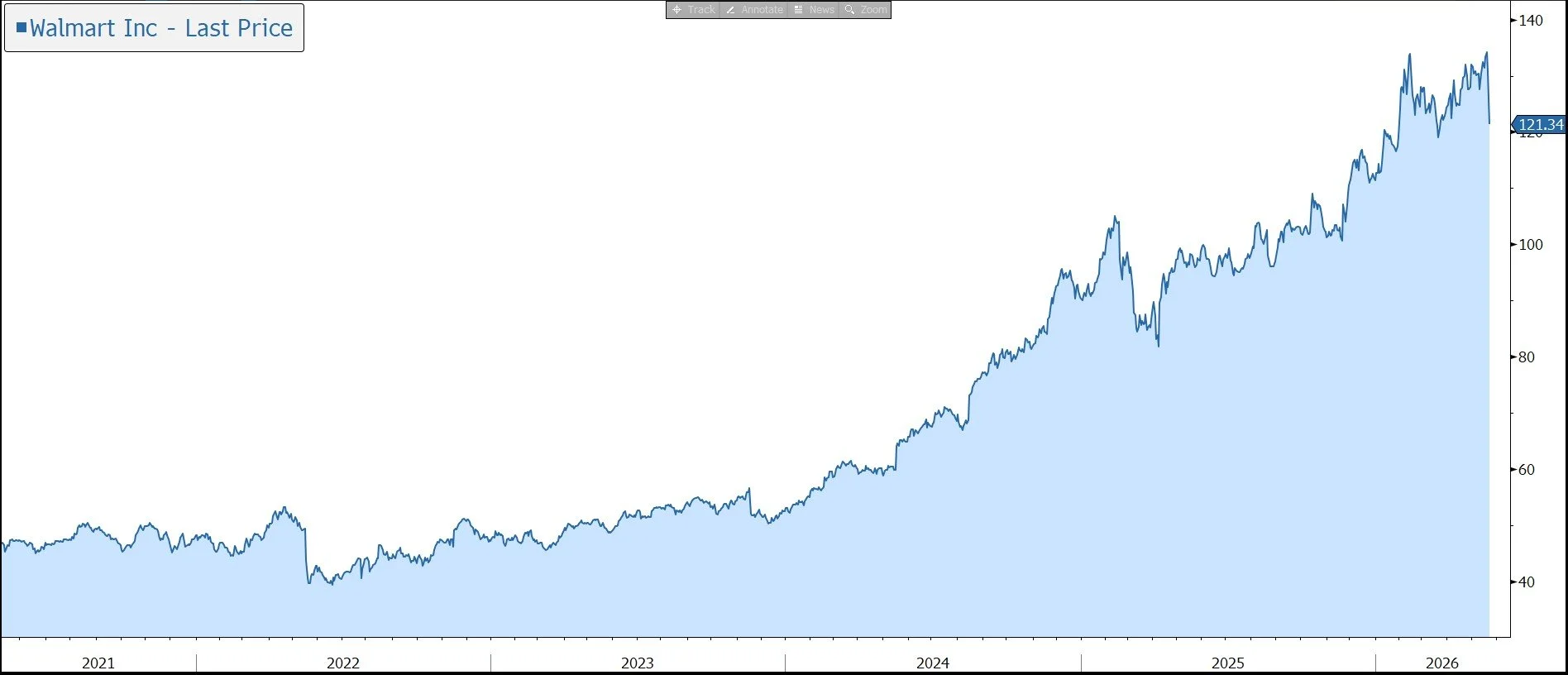

Yesterday lunchtime, Walmart released results for the three months to 30 April 2026, the first quarter of its financial year to 31 January 2027. The group generated strong sales growth and earnings in line with market expectations. However, given the uncertain macro-economic backdrop, the company has maintained its guidance for the full-year at a level that was considered prudent when it was initiated earlier in the year. In response, the shares were marked down 7%.

Walmart operates more than 10,900 stores and numerous e-ecommerce websites under 46 banners in 19 countries. In the face of strong competition, the group’s strategy is ‘to lead on price, invest to differentiate on access, be competitive on assortment, and deliver a great experience’. This means the company can often weather economic storms better than others. As the largest importer of container goods in the US, Walmart is heavily exposed to tariffs and has been raising prices in response.

During the three months to the end of April, total revenue increased by 5.9% on a constant currency (CC) basis to $177.8bn, a touch ahead of the market expectation of $175bn. Growth was made up of a 3.0% increase in transactions (i.e., volume) and 1.1% rise in average ticket (i.e., price). eCommerce sales were up 26% globally, led by store-fulfilled pickup & delivery and marketplace, while global advertising sales were up 37%. Membership fee revenue grew 17.4% globally.

In the US, comparable sales increased by 4.1% (ex-fuel) to $117.2bn, with strong growth in grocery and health & wellness. Sam’s Club, the trade business, generated revenue of $20.5bn, up 3.9% in comparable terms (ex-fuel), led by grocery and general merchandise. Outside of the US, the International business grew by 10.1% at CC to $35.1bn, with broad-based strength across markets.

Group gross margin rose by six basis points to 24.3%, led by the US. This reflected benefits from favourable merchandise category mix and business mix led by advertising, partially offset by higher fuel costs in our supply chain. The group kept a tight rein on costs and adjusted operating income rose by 5.1% at CC to $7.5bn. Adjusted EPS was up 8.2% to 66c, in line with the market forecast.

Global inventory was up 8.9% to $62.6bn. There was a free cash outflow of $1.9bn driven by the timing of inventory receipts and a $1.7bn increase in capital expenditures to support the group’s omnichannel growth strategy. During the quarter, the company raised $4.25bn in long-term debt for general corporate purposes at favourable rates. Net debt ended the quarter at $47.4bn.

Excess cash is returned to shareholders through dividends and buybacks. During the quarter, the group has bought back $2.1bn of its shares, leaving $28.2bn of its $30bn repurchase authorisation. In the last quarter, the dividend was increased by 5% to $0.99.

Guidance for the financial year to January 2027 has been reiterated. Consolidated net sales growth of 3.5%-4.5% at constant currency. Operating income growth is expected to be 6%-8%, while Adjusted EPS is expected to come in at $2.75-$2.85. For the current quarter, net sales and adjusted operating income are expected to grow by 4%-5% and 7%-10%, respectively, both slightly below market expectations.

Source: Bloomberg

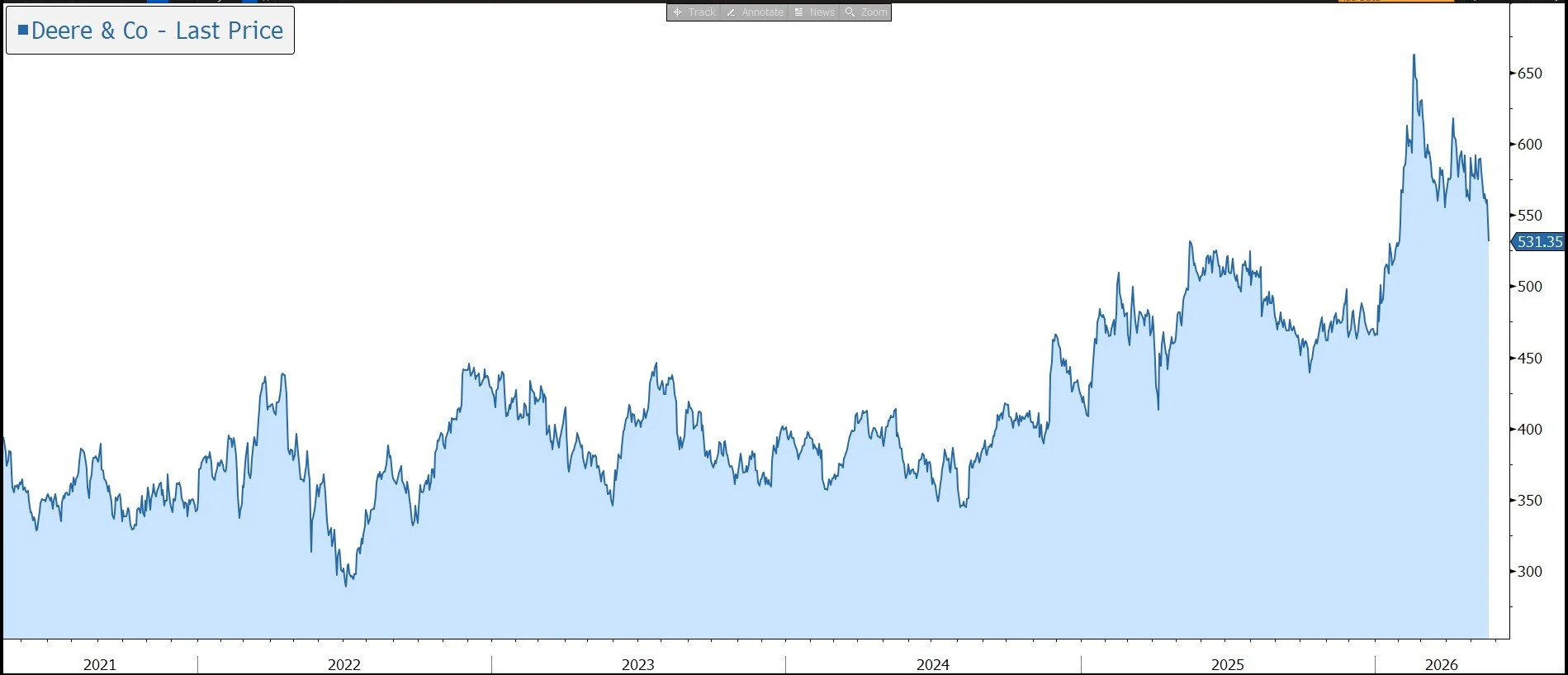

Yesterday lunchtime, Deere & Company released results for the three months to 3 May 2026, the second quarter of its financial year to end-October 2026. Despite ongoing market challenges, the numbers were solid, demonstrating the strength of the group’s diversified portfolio. Sluggish demand for large farm machinery was made up for by growth in smaller farm equipment and construction machinery. Guidance for the full year was reiterated. In response, the shares were marked down by 5% in US trading hours.

Deere is a global agricultural and construction equipment company with annual sales of almost $46bn. The group has a strong track record of innovation, a comprehensive distribution infrastructure, and global after-market capability. The group’s strategic aim is to outpace industry growth and generate a mid-cycle operating margin of 15%.

The business is benefitting from broad trends based on population and income growth, especially in developing nations, which are driving agricultural output and infrastructure investment. In addition, technological advances and agricultural mechanisation are expanding existing markets and opening new ones by helping customers increase their productivity, profitability, and sustainability.

The company believes it has incremental addressable market opportunities of more than $150bn that can be targeted through engaging with more customers and increasing levels of connectivity. The focus is on helping customers manage higher costs and increasingly scarce inputs, while improving their yields, using Deere’s integrated technologies.

However, in the near term, conditions in the global agricultural and construction sectors have been challenging because of higher interest rates, the Middle East conflict, squeezed farming incomes, and lower government support. More farmers have switched to renting tractors and other equipment, and Deere has been forced to streamline field inventory.

During the latest quarter, worldwide net sales and revenue rose by 5% to $13.4bn, while net sales were also up 5% to $11.8bn, just above the market forecast. Net income fell by 2% in the year to $1.77bn, while EPS declined by 1% to $6.55, above the market forecast of $5.70.

The Production & Precision Agriculture segment includes large and certain mid-size tractors, combines, cotton pickers, sugarcane harvesters and loaders, and soil preparation, seeding, application and crop care equipment. During the latest quarter, sales fell by 14% to $4.5bn, as a result of lower shipment volumes, partially offset by the positive effects of foreign currency translation. Operating profit declined by 39% to $706m, due to lower shipment volumes and higher production costs. The margin slumped from 22.0% to 15.7%.

The Small Agriculture and Turf segment includes certain mid-size and small tractors, as well as hay and forage equipment, riding and commercial lawn equipment, golf course equipment, and utility vehicles. During the quarter, sales rose by 16% to $3,485m, due to higher shipment volumes. Operating profit rose by 25% to $719m, due to higher shipment volumes and favourable price realisation. The margin rose from 19.2% to 20.6%.

Construction & Forestry sales grew by 29% to $3,790m, while operating profit rose 48% to $561m primarily due to higher shipment volume and favourable price realisation, partially offset by higher production costs.

The group’s Financial Services division reported adjusted net income grew by 18% to $190m, due to favourable financing spreads and favourable derivative valuation adjustments, partially offset by the impact of a lower average portfolio.

Deere’s balance sheet is fairly robust, with net debt of $54bn, a level consistent with supporting a credit rating that provides access to low cost and readily available funding. The group has a policy to raise its dividend “consistently and moderately”, targeting a 25%-35% payout ratio of mid-cycle earnings. The latest annual dividend was raised by 10% to $6.48 per share.

Looking forward, the company believes 2026 will mark the bottom of the large agricultural equipment cycle. While ongoing margin pressures from tariffs and persistent challenges in the sector remain, the group’s commitment to inventory management and cost control, coupled with expected growth in small agriculture & turf and construction & forestry, positions the company to effectively manage the business.

Against this backdrop, net earnings are forecast to be in the range of $4.5bn-$5.0bn. By division, net sales are expected to decline by 5%-10% in Production & Precision Agriculture and be 15% and 20% higher in Small Agriculture & Turf and Construction & Forestry, respectively.

Source: Bloomberg