Morning Note: Market News and an Update from Nvidia.

Market News

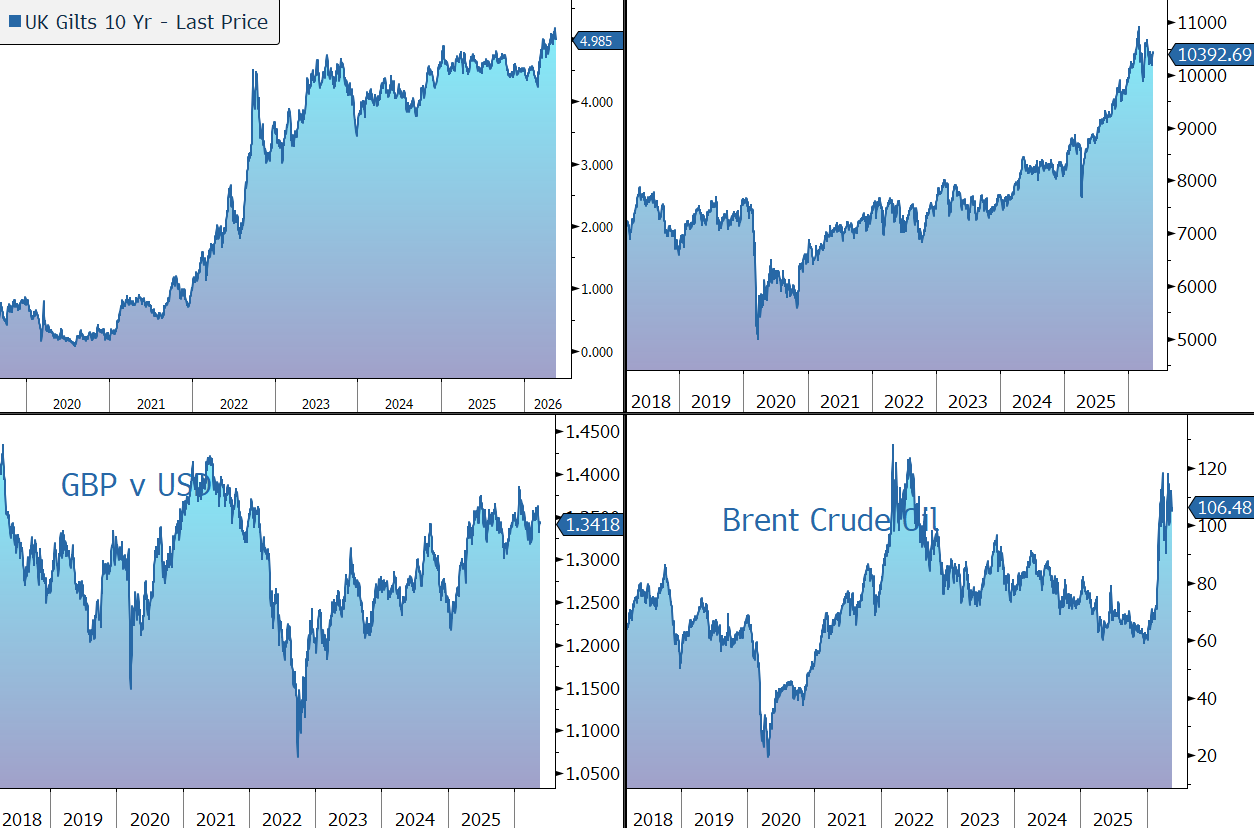

Brent Crude inched higher $106 a barrel after plummeting yesterday, as President Donald Trump said the US is in the ‘final stages’ with Iran. Vice-President JD Vance reported ‘significant progress’ in negotiations, yet both sides’ positions on Iran’s highly enriched uranium and enrichment timeline remain unresolved. Global stockpiles of crude and products are being drawn down at a record pace this month as the war drags on, Goldman said, with visible inventories contracting by an 8.7m barrels a day so far in May.

The FOMC Minutes from 29 April leaned hawkish, as expected. They showed broader support for patience, but the majority said some policy firming was likely appropriate if inflation persists. However, many still saw further rate cuts ahead as likely appropriate if the conflict ends and inflation pressures dissipate. The yield on the US 10-year Treasury has fallen back to 4.60%, while gold trades at $4,525 an ounce.

US equities rose last night – S&P 500 (+1.1%); Nasdaq (+1.5%) – as investors flocked back to the artificial intelligence trade and a clutch of upcoming IPOs kept enthusiasm for the technology sector elevated. Nvidia (see below) slipped post-market after its sales forecast drew a lukewarm response from investors despite a dividend increase and an $80bn buyback. SpaceX filed publicly for its Nasdaq listing, revealing billions in losses and a super-voting share plan allowing Elon Musk to keep control of the company.

In Asia, equities were mixed: Nikkei 225 (+3.1%); Hang Seng (-0.6%); Shanghai Composite (-0.8%). South Korea’s Kospi advanced by 8%. SoftBank surged after people familiar said OpenAI may pursue an IPO in coming weeks

The FTSE 100 is currently 0.3% lower at 10,392. Companies trading ex-dividend today include Bunzl (2.22%), Imperial Brands (1.45%), Shell (0.89%), Tritax Big Box (1.33%), and Whitbread (2.50%). Rachel Reeves backed away from a proposal to cap the prices of essential groceries after receiving backlash from supermarkets, the FT reported. The chancellor will today detail a package of measures to ease cost-of-living pressures. Sterling trades at $1.3430 and €1.1570, while the 10-year Gilt yield has slipped to 5.0%.

Source: Bloomberg

Company News

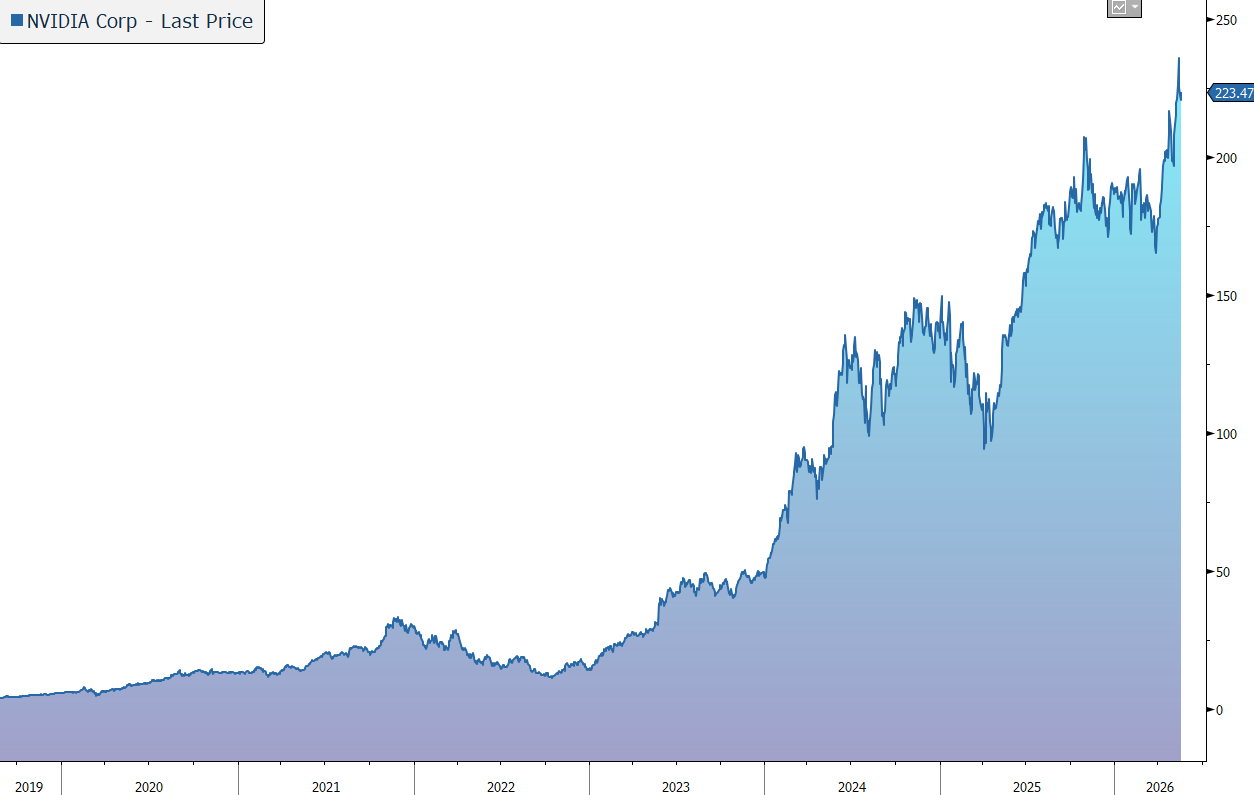

Last night NVIDIA released results for the three months to 26 April 2026, the first quarter of its financial year to January 2027. The figures came in ahead of market expectations and the company increased its dividend and announced an $80bn share buyback. However, despite the blockbuster guidance, the shares fell slightly in after-hours trading as investors weighed the lofty valuation against an already priced-in beat.

NVIDIA is one of the world’s largest semiconductor companies, with a leading market share in Graphics Processing Units (GPUs). From its original focus on PC graphics, the company has expanded to several other large and important computationally intensive fields, leveraging its GPU architecture to create platforms for scientific computing, AI, data science, autonomous vehicles, robotics, and industrial AI.

NVIDIA’s Blackwell and newly announced Rubin architectures remain the industry gold standard. According to SemiAnalysis InferenceX benchmark results, NVIDIA Blackwell Ultra delivers up to 50x better performance and 35x lower cost for agentic AI compared with the NVIDIA Hopper platform. Rubin comprises six new chips to deliver up to a 10x reduction in inference token cost, compared with the Blackwell platform.

The company is benefitting as data centres make a platform shift from general computing, primarily using central processing units (CPUs), to accelerated computing, primarily using GPUs, which brings significant improvements in performance, energy efficiency, and cost.

Accelerated computing’s ability to significantly speed up machine learning and to deal with large data sets has enabled the development of generative artificial intelligence (AI), which offers human-like computing performance, and Agentic AI, AI systems that don't just chat, but can reason and execute multi-step tasks autonomously. This is driving significant investment in new enterprise applications, which is in turn driving new demand for accelerated computing. There has also been an increase in Sovereign AI, where nations build their own domestic AI infrastructure, which generates another source of revenue for NVIDIA.

A concern is Google’s AI ecosystem, which is not reliant on NVIDIA’s GPUs, creating a significant risk to the company’s ability to sustain such high market share and gross margins. To defend its moat, NVIDIA has executed an unprecedented capital deployment strategy, committing roughly $90bn to investments and partnerships. By funding a vast ecosystem, stretching from foundation model makers to ‘neocloud’ GPU infrastructure providers, NVIDIA is effectively anchoring the next generation of AI development to its proprietary hardware and software stack.

Another risk is that while demand for Rubin is described as unprecedented, the company remains highly dependent on TSMC’s CoWoS advanced packaging capacity, alongside a tight global supply of High Bandwidth Memory.

In the latest quarter, revenue rose by 85% to $81.6bn, above the company guidance of $78bn, plus or minus 2%, and the market forecast of $79bn. The result was 20% higher than the previous quarter.

The company has transitioned to a new reporting framework that better reflects its current and future growth drivers. NVIDIA has two market platforms: Data Center and Edge Computing.

During the first quarter, Data Center revenue rose by 92% to $75.2bn, driven by the ramp of the group’s Blackwell 300 products and demand for its InfiniBand, Spectrum-X™ Ethernet, and NVLink™ solutions. The division is divided into two sub-markets, Hyperscale and ACIE, which incorporates AI Clouds, Industrial and Enterprise. Hyperscale will include revenue from the public clouds and the world’s largest consumer internet companies. In the latest quarter, revenue rose by 115% to $38.9bn. ACIE addresses NVIDIA’s growth opportunity in diverse AI purpose-built data centers and AI factories across industries and countries. Revenue rose by 74% to $37.3bn.

Edge Computing highlights data processing devices for agentic and physical AI including PCs, game consoles, workstations, AI-RAN base stations, robotics and automotive. In the first quarter, revenue rose by 29% to $6.4bn. Growth was driven by robust Blackwell workstation demand, partially offset by slower consumer PC demand that was tempered by elevated memory and systems prices.

The gross margin is high. In the latest quarter, it rose from 60.8% to 75.0%, in line with the group’s guidance of 75%, plus or minus 50 basis points. Operating expenses rose by 49% to $7.45bn, in line with guidance, and primarily driven by higher compensation and benefits expense due to employee growth and compensation increases, compute and infrastructure costs, and engineering development materials for new product developments. Earnings rose by 140% to $1.87, ahead of the market forecast of $1.76.

The business is very cash generative, with free cash flow up 86% to $48.6bn in the three months to 26 April. The company’s balance sheet is very strong, with cash of more than $50bn at the end of the quarter. The cash is being used, in part, for shareholder returns. The company recently approved an additional $80.0bn to its share repurchase authorisation and increased its quarterly cash dividend from 1 cent per share to 25 cents per share.

For the current quarter, the company is guiding to revenue of $91bn, plus or minus 2%. This was above the consensus expectation of $87bn. A gross margin of 75.0%, plus or minus 50 basis points is forecast, and operating expenses of $8.3bn.

Source: Bloomberg