Morning Note: Market News and updates from Reckitt Benckiser and Brown-Forman.

Market News

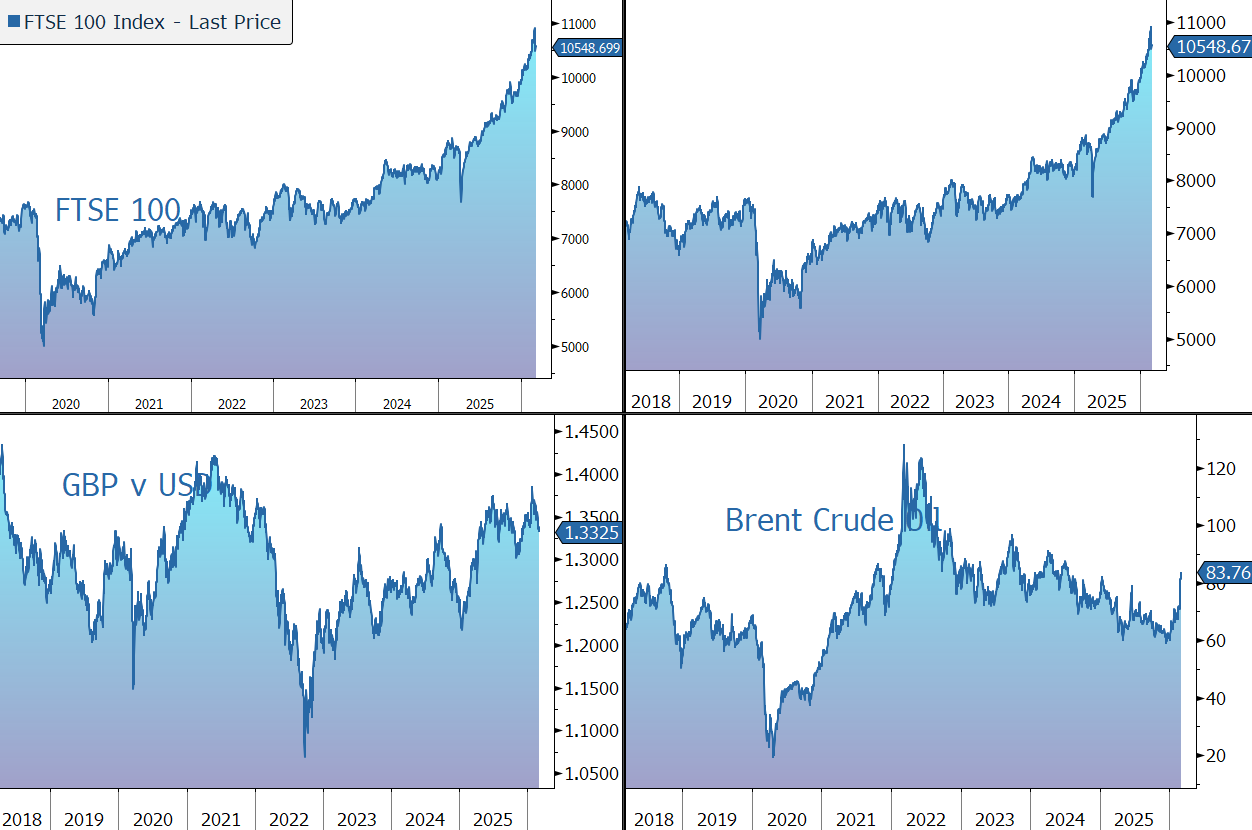

Gold trades at $5,160 an ounce, extending gains from the prior session, as investors continue to monitor escalating tensions in the Middle East. A bipartisan resolution aimed at limiting President Donald Trump's ability to prosecute the war in Iran failed in the US Senate.

The 10-year Treasury yields 4.13%. On the economic front, US services activity rose to a more than 3½-year high in February, while private-sector employment growth exceeded expectations. US money-market funds swelled to a record $8.3 trillion after the attacks on Iran fueled haven demand, Crane Data showed.

The oil price is up 3% at $83 a barrel. China asked its largest oil refiners to suspend exports of diesel and gasoline, people familiar said, as the Iran conflict disrupts crude inflows.

US equities rose last night: S&P 500 (+0.8%); Nasdaq (+1.3%). Broadcom expects its AI chip sales to top $100bn next year. The company forecast quarterly revenue above estimates and unveiled a $10bn share buyback.

In Asia this morning, stocks bounced, with South Korea leading gains following government intervention: Nikkei 225 (+1.9%); Hang Seng (+0.3%); Shanghai Composite (+0.6%). China set its annual economic growth goal at a range of 4.5%-5.0%, the least ambitious expansion target since 1991. The country continues to grapple with a host of economic challenges: weak domestic consumption, a population headwind, major dislocations in the property sector and global trade tensions.

The FTSE 100 is currently 0.3% lower at 10,549, while Sterling trades at $1.3320 and €1.1490. Stocks trading ex-dividend include Rio Tinto (2.65%) and Personal Assets Trust (0.25%). The UK 10-year gilt yield continued to climb – it is currently 4.44% - as investor attention returned to inflation risks.

Source: Bloomberg

Company News

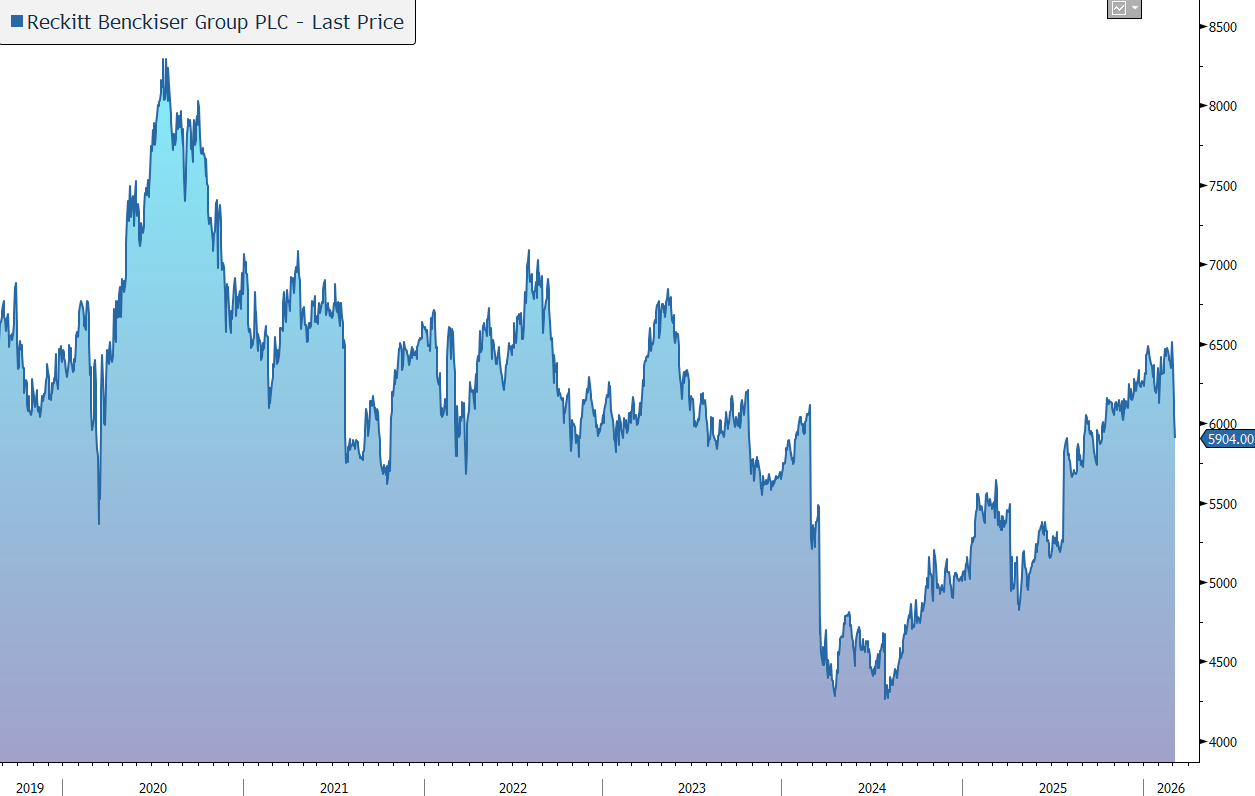

Reckitt Benckiser has released full-year 2025 results which were slightly ahead of market expectations, driven by a good final quarter, particularly in emerging markets. The company is now confident of achieving more fixed cost savings than targeted from its Fuel for Growth programme. The dividend was raised by 5%. The main negatives are ongoing weakness in Europe and the prospect of a soft Q1 due to a weak cold and flu season. Ahead of the analysts’ meeting the shares are down 2%.

Reckitt is a global leader in health, hygiene, and nutrition. Trusted brands, such as Dettol and Lysol, continue to benefit from the shift to healthier and more hygienic lifestyles, particularly in emerging markets. To help ease the pressure on state-funded healthcare systems, we are seeing a transition to self-care and growth of over the counter (OTC) brands such as Mucinex, Nurofen, and Gaviscon, all of which are owned by Reckitt. A focus on immunity, mental health, and overall well-being is expected to drive growth of the group’s preventative treatments, such as vitamins, minerals, and supplements (VMS).

Reckitt is currently refocusing its portfolio and simplifying its organisation to drive accelerated growth and value creation.

Core Reckitt includes a portfolio of 11 market-leading (No.1 or No.2), high margin Powerbrands across four categories of Self-Care, Germ Protection, Household Care, and Intimate Wellness. Brands include Mucinex, Strepsils, Gaviscon, Nurofen, Lysol, Dettol, Harpic, Finish, Vanish, Durex, and Veet. Over the last three years this portfolio has delivered 5% revenue CAGR and in 2025 generated a gross margin above 60%.

Reckitt operates across three geographies: North America, Europe, and Emerging Markets, with the latter expected to grow in the high-single digits.

The company is undertaking a fixed cost optimisation initiative to unlock efficiencies and deliver at least a three percentage points reduction in fixed costs by the end of 2027, of which half were achieved by the end of 2025. The group now has confidence in achieving a fixed cost base below the initial 19% target by the end of 2027. Part of the savings are being reinvested into the supply chain and R&D.

Overall, from 2026 the company believes it will have the portfolio, geographic footprint, and execution capabilities for Core Reckitt to consistently deliver 4%-5% like-for-like (LFL) net revenue growth, while consistently delivering annual EPS growth and creating value for shareholders.

At the end of 2025 the company sold its Essential Home business, a portfolio of non-core brands such as Air Wick, Mortein, Calgon, and Cillit Bang. The $4.8bn transaction was fairly complex – it included up to $1.3bn of contingent and deferred consideration, and Reckitt retained 30% of the business. As part of the deal, shareholders received a $2.2bn (£1.6bn or 235p a share) special dividend and the shares underwent a 24-for-25 consolidation.

The company’s third leg is Mead Johnson Nutrition which includes infant formula brands Enfamil and Nutramigen. The company is currently ‘evaluating opportunities’ for the business.

Back to today’s results. In 2025, reported revenue rose by 0.3% to £14.2bn, including a currency headwind (-2.9%) and disposals (1.8%). Stripping out these impacts, LFL growth was 3.4%, versus the 3%-4% company guidance. Excluding Essential Home unit, LFL growth was 5.0%, with growth made up of price/mix (4.1%) and volume (0.9%).

In the final quarter, sales rose by 5.4% in LFL terms, above the market expectation of 4.7%. Growth was made up of price/mix (5.6%) and volume (0.2%).

Full-year growth was led by Emerging Markets (+14.6%), with China growing faster boosted by the e-commerce channel. In Developed Markets, Europe fell by 0.2% (and by 4.5% in Q4), impacted by a challenging consumer environment and the timing of cold & flu incidence with price/mix growth driven by our premiumisation strategy. North America rose by 0.2%, with improved momentum in H2 reflecting strong growth in non-seasonal brands and enhanced execution

The company enjoyed improved market share performance – 51% of the top Category Market Units held or gained share, with % for the core Hygiene and Health business.

Core Reckitt grew revenue by 5.2% to £10.2bn, made up of 3.7% growth in price/mix and 1.5% volume growth. Growth was ahead of the 4%-5% medium-term target and accelerated in the second half. In the final quarter, LFL growth was 5.9%.

In the Core product segments LFL growth was enjoyed at Germ Protection (+8.4%), Intimate Wellness (+12.5%), and Self-Care (+3.0%), offset by Household Care (-0.4%). The company benefitted from recent innovations across the business.

In the smaller non-core divisions, Mead Johnson Nutrition, net revenue rose by 3.8% on a LFL basis to £2,119m, as the business lapped the significant impact of the 2024 tornado. This compared to guidance of low-to-mid single digits and was made up of price/mix of 6.1%, offset by a 2.3% volume decline. Essential Home net revenue fell by 6.3% to £1,852m prior to the completion of the divestment on 31 December 2025.

The adjusted gross margin rose by 10 basis points to 60.8%, in line with expectations and including the impact of tariffs. Adjusted operating margin rose from 24.5% to 24.9%, driven by fixed cost reduction from Fuel for Growth and efficiencies from our simplified operating model. The result was slightly below the market expectation. The adjusted operating model of the Core business rose by 90 basis points to 26.7%. Adjusted EPS rose by 1.1% to 352.8p.

The company increased investment in supply chain and R&D capabilities, with full-year capital expenditure of 4.2% of net revenue, above the guided range as the group pulled forward planned investments.

Free cash flow generation fell by 23% to £1,709m, including £179m of one-off cash costs relating to transformation and restructuring. Financial gearing fell from 2.0x net debt to adjusted EBITDA to 1.6x, versus the guidance of ‘below 2x’. The dividend has been lifted by 5% to 212.2p (3.6% yield), with the aim to deliver sustainable growth in future years.

Reckitt is currently buying back its shares, with a £1bn programme to be completed by next summer. As highlighted above, this is in addition to the capital return associated with the Essential Home deal. The company recently completed the second tranche of the buyback and will commence the final tranche soon.

Guidance for 2026 has been initiated.

· Core Reckitt – LFL revenue growth in the 4%-5% medium-term guidance range. Q1 is expected to be impacted by a weaker cold and flu season. A continued challenging environment is expected in Europe.

· Mead Johnson Nutrition - low-single-digit LFL net revenue growth, with a mid-single-digit LFL decline in Q1 as the company laps the retailer inventory rebuild in North America in Q1 2025.

· The company reiterated its ambition to deliver long-term, sustainable EPS growth, acknowledging in 2026 the headwind from the dilution resulting from the divestment of Essential Home.

The company continues to monitor the evolving situation around global tariffs and the potential impacts on its supply chain and cost base. We note that Reckitt has five factories in the US and makes more than half of its US sales volume locally. The company also sources some over-the-counter products from Mexico and condoms from Southeast Asia. In the medium term, the company already has plans in place to increase its US production footprint – when its North Carolina factory comes online in 2027, the percentage of sales manufactured locally could rise to 75%. At present, the company sees an immaterial annualised impact on its COGS base which it is confident it can mitigate over the short to medium-term through several levers including pricing power and limited imports from China into the US.

The legal case against the company (and industry peer Abbott) relating to its cow’s milk-based infant formula is ongoing. As of early 2026, there were around 800 active cases in the Multi-District Litigation. Reckitt continues to vigorously defend these claims and believes the lawsuit’s claims are not supported by scientific evidence. However, the threat of sizeable damages continues to hang over the share price and prevents the company from offloading its Nutrition division. We expect the company to seek some form of settlement.

Source: Bloomberg

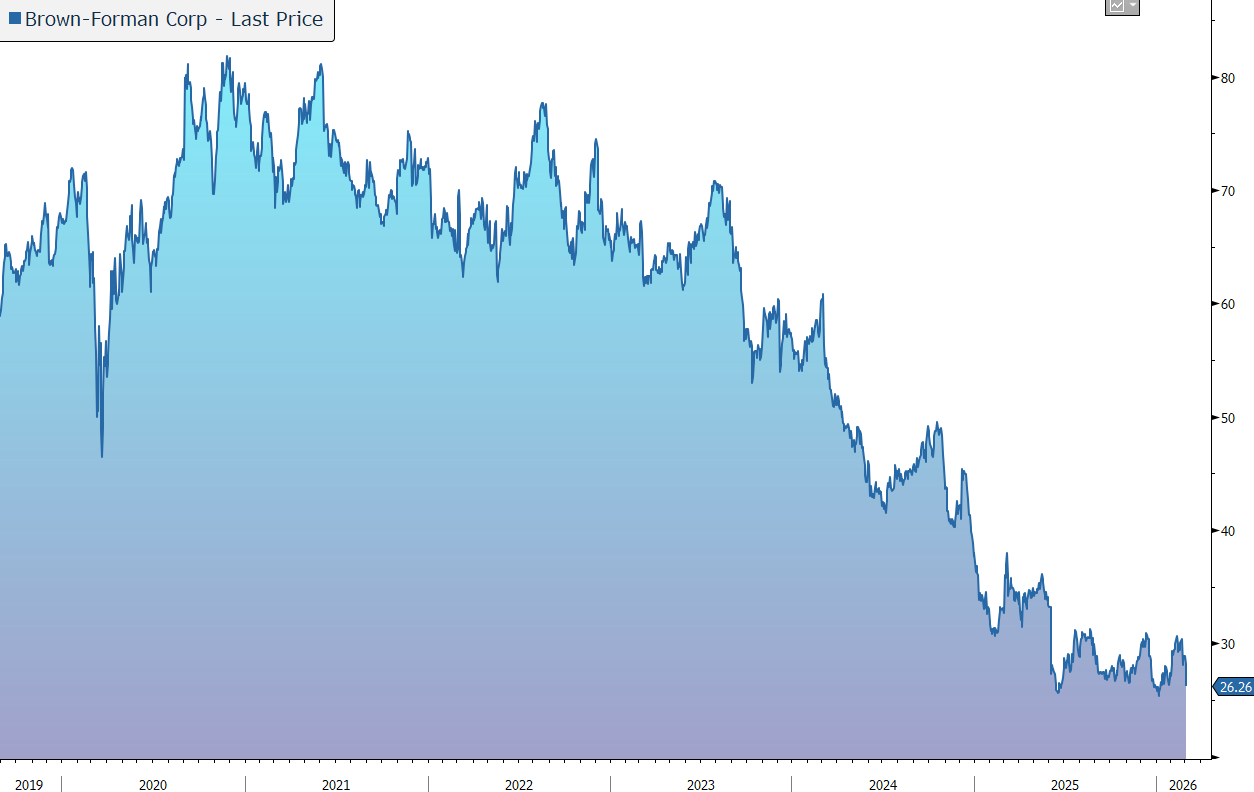

Yesterday lunchtime Brown-Forman released results for the three months to 31 December 2026, the third quarter of its fiscal year to end April 2026. Against a challenging operating environment, the figures were better than market expectations and the dividend was raised by 2%. Despite the ‘beat’, guidance for the full year was reiterated and commentary on the analysts’ call was fairly downbeat. In response, the shares were marked down by 7%.

Brown-Forman is a US-listed spirits producer, which owns a portfolio of more than 40 premium brands including Jack Daniels. To take advantage of the premiumisation trend, the group has upgraded its portfolio over time towards the American whiskey and tequila categories and sold off non-core brands (such as Finlandia and Sonoma-Cutrer).

In the latest quarter, net sales, excluding excise taxes, rose by 2% to $1,056m, above the market forecast of $998m. On an organic basis, sales were up 1%. That leaves organic sales flat in the first nine months of its financial year

From a geographic perspective, net sales growth in the year-to-date in Emerging markets (+15%) and the Travel Retail channel (+7%) was more than offset by declines in the US (-1%) and Developed International markets (-6%).

Net sales for whiskey products were up 1% on an organic basis led by innovation. The launch of Jack Daniel’s Tennessee Blackberry, the positive effect of foreign exchange, and the growth of Jack Daniel’s Tennessee Apple in Brazil were partially offset by declines of Jack Daniel’s Tennessee Whiskey and Jack Daniel’s Tennessee Honey.

Net sales for the Tequila portfolio fell by 7% in organic terms, with Herradura down 12% driven by lower volumes in the US as the tequila category remains competitive. el Jimador’s net sales fell 4%, driven decline in the US and Mexico, partially offset by higher volumes in Colombia

Net sales for the Ready-to-Drink (RTD) portfolio increased by 6% in organic terms.

The gross margin remains high and rose by 80 basis points in the quarter to 60.6%. That leaves it up by 50% basis points to 59.9%, driven by the positive effect of acquisitions and divestitures and the positive effect of foreign exchange, partially offset by higher costs (-40bps) and unfavourable price/mix (-90bps).

Operating income was flat in organic terms in the quarter at $340m and down 3% to $905m in the financial year to date. Diluted EPS rose by 1% in the quarter to 58c, well above the market forecast of 47c.

In the financial year to date, free cash flow has risen from $299m to $628m. The company has a strong balance sheet, with net debt of $2.4bn. A regular quarterly cash dividend has been paid for 82 consecutive years and has increased for 42 consecutive years. For the latest quarter, a payout of 23.10c was reaffirrmed, up 2% on last year. The $400m share repurchase programme was completed in December 2025.

Looking forward, the company continues to anticipate the operating environment for fiscal 2026 will be challenging, with low visibility due to macroeconomic and geopolitical volatility as the business faces headwinds from consumer uncertainty. Despite the latest quarter coming ahead of market expectations, the company only reiterated its guidance for the full year for an organic low single-digit decline in both net sales and operating income.

Source: Bloomberg