Morning Note: Market News and Updates from Adidas and Tritax Big Box REIT.

Market News

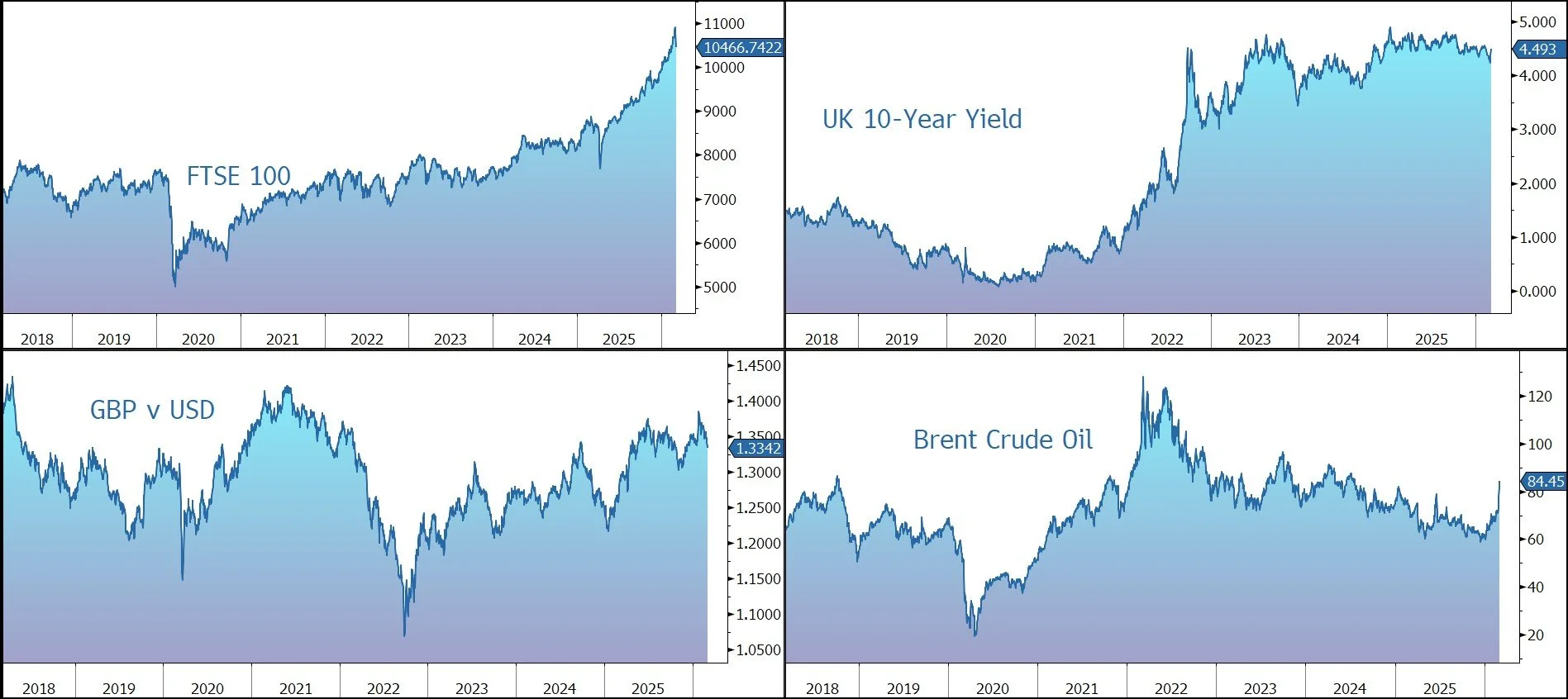

Asset price volatility remains heightened as the US-Israeli conflict with Iran entered its fifth day.

The oil price extended gains as fresh attacks flared in the Middle East and traders weighed Donald Trump’s plan to insure and escort tankers passing through the Strait of Hormuz. ING said US Navy escorts would risk being ‘sitting ducks’ for Iran. Brent Crude currently trades at $83 a barrel.

The oil shock may threaten to unleash a wave of global inflation and put central banks in a tough spot. The Federal Reserve’s Neel Kashkari, who’d pencilled in one interest-rate cut this year, said the attacks on Iran make him less certain about that. The 10-year Treasury yields 4.08%. Gold has risen back above $5,170 per ounce, recovering some losses from the previous session.

US equities staged a partial recovery but still ended the session lower last night – S&P 500 (-0.9%); Nasdaq (-1.0%). However, in Asia this morning, stocks fell heavily led by South Korean (-12%), as mounting concerns over the war triggered an exodus from some of the world’s best-performing markets. Nikkei 225 (-3.6%); Hang Seng (-2.0%); Shanghai Composite (-1.0%). The S&P futures currently predict the US will be down 0.3% at the open this afternoon.

The FTSE 100 is currently 0.3% lower at 10,466, while Sterling trades at $1.3345 and €1.1505.

Source: Bloomberg

Company News

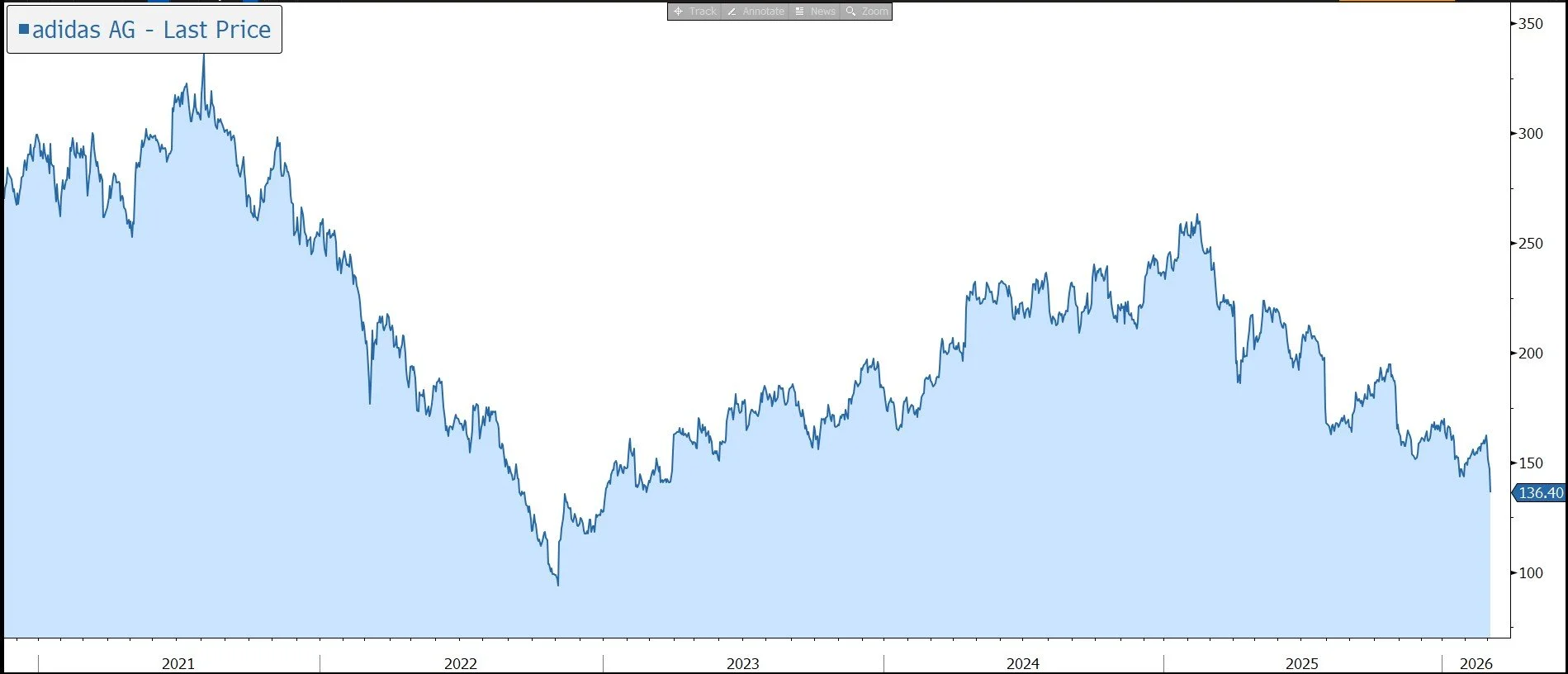

Adidas has released full-year 2025 results, with further detail than that provided with the January trading update. The results were strong, driven by a successful turnaround of the business. The dividend was raised by 40% and the €1bn share buyback programme is ongoing. However, guidance for 2026 was slightly below what the market was expecting, and in response the shares have been marked down by 6% in early trading.

Adidas is a multi-brand sporting goods company. Its products have traditionally had a broad global appeal from serious athletes, casual athletes to sports fashion, and from mid-price to high-price points. As a result, the group should be well placed to benefit from the continued focus on health and fitness, the rising middle class in emerging markets, and fashion trends in sportswear.

The group’s year-on-year results were impacted by the previous initiatives to reduce inventory levels following the termination of the adidas Yeezy partnership with rapper and fashion designer Kanye West. Having completed the sale of the remaining Yeezy inventory in 2024, the company’s results for 2025 do not include any Yeezy revenues.

In 2025, revenue was up 13% in currency-neutral terms to a record €24.8bn, compared to guidance for double-digit currency-neutral revenue growth. Excluding the Yeezy impact growth was 10%. Performance was driven by double-digit growth in all markets and channels, as well as in both Performance and Lifestyle.

In Q4 2025, revenue rose by 11% in currency-neutral terms to €6.1bn. Including the impact of Yeezy sales in the prior year, growth was 10%.

The company has been very good at managing the right product in the right amount – it has managed to keep full-price sell-throughs high and discounts under control.

By region, Europe, the company’s largest market, grew by 10% in the year. Elsewhere, sales were: North America (+10%); Emerging markets (+17%); Latin America (22%); Greater China (+13%).

By channel, strong sell-through rates at retail partners and increased shelf space allocations continued to drive wholesale revenues, which increased 12%. The direct-to-consumer (DTC) business rose by 14%, with e-commerce 16% and own retail 13%.

By category, footwear was 12%, driven by many categories, including Running, Training, Performance Basketball, and Sportswear. Elsewhere apparel and accessories grew by 15% and 6% respectively.

The gross margin grew by 80 basis points to 51.6%, despite the negative impacts from unfavourable currency developments and higher tariffs.

The operating margin improved from 5.6% to 8.3% in 2025, pushing up operating profit by 54% to €2,056m. This is above the company guidance of ‘around €2.0bn’, which was upgraded at the Q3 stage from €1.7bn-€1.8bn.

The group’s balance sheet is robust. Although net debt rose from €3.6bn to €4.3bn, the company gearing fell to 1.4x net debt to EBITDA. Inventories were up 17% on a currency neutral basis to €5.8bn, reflecting the company’s planned top-line growth and earlier product purchases related to the FIFA World Cup 2026.

The board has proposed a dividend of €2.80 per share, up 40% versus the previous year, and within the range of 30% to 50% of net income from continuing operations.

Given the strong brand momentum, the company’s robust fundamentals, its healthy balance sheet and strong cash flow generation, as well as management’s confidence in the future development of the business, the company is undertaking a €1bn share buyback programme which it expects to complete this year.

The company issued guidance for 2026. The target is for currency-neutral revenue to increase at a high-single-digit rate, reflecting growth of around € 2.0 billion in absolute terms and further market share gains in all markets. Operating profit is expected to increase to around €2.3bn, despite around € 400 million negative impact from US tariffs and unfavourable currency developments

Over the mid-term, over three-year period 2026-2028, the company is targeting currency-neutral revenues to grow at a high-single-digit rate every year and operating profit to increase at mid-teens CAGR. Increased cash returns will be driven by strong cash generation

There is some frustration that the 10% margin target is being pushed back further into 2027 or 2028, rather than being achieved in a World Cup year.

Source: Bloomberg

Property News

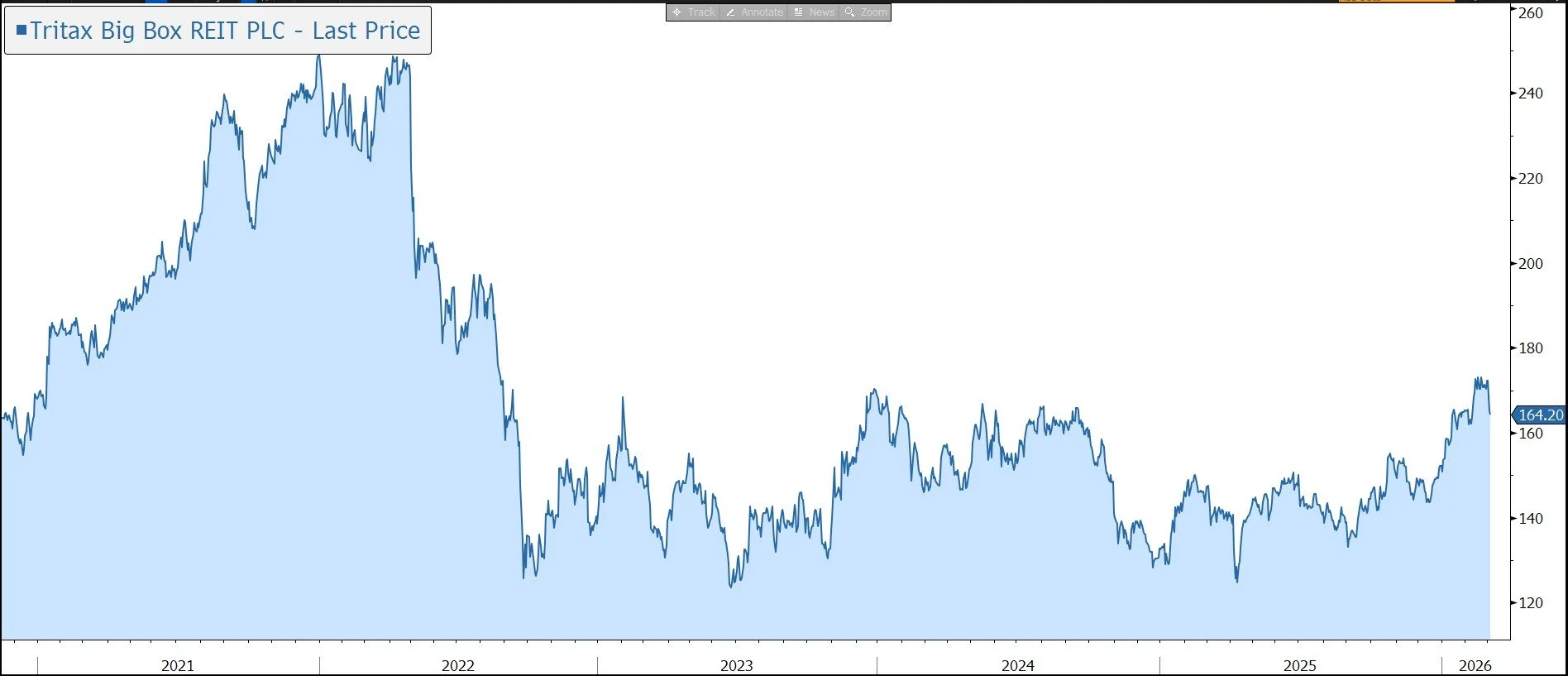

Last week, Tritax Big Box REIT released its 2025 results which highlighted strong momentum across the business. The dividend was raised by 4.4% and the company delivered a total accounting return of 5.5%. Earlier in the week, the company joined the FTSE 100 index. The shares currently trade on a 12% discount to NAV, which rose by 1.2% in the year, and offer a dividend yield of 4.8%.

Tritax Big Box REIT is the UK’s largest real estate investment trust focused exclusively on high-quality logistics real estate. The company serves as a critical backbone for the UK economy, providing the ‘big-boxes’ and urban distribution centres that power modern e-commerce and retail supply chains.

Tritax operates a specialised ‘build-to-suit’ and acquisition model. It owns, manages, and develops massive distribution centres – often exceeding 500,000 sq ft – that are strategically located near major motorways, rail hubs, and ports. The company has also diversified into urban logistics (now 20% of assets) and datacentres.

We believe the long-term outlook for the sector remains favourable, supported by the continued growth in e-commerce, the consolidation of logistics networks into fewer, larger, more modern and efficient buildings, and the need to build resilience into supply chains. At a time when occupiers need a robust and flexible supply chain, the assets are essential to their business and cannot be easily replicated. We note that property costs are a small percentage of total operational costs for a retailer – more important is having the right location.

The business focuses on three primary growth drivers:

Investment Portfolio: A collection of high-quality, standing assets that provide resilient, inflation-linked, or fixed-growth rental income.

Development Pipeline: Tritax owns the UK’s largest logistics land platform, allowing them to build new facilities at a significant yield-on-cost advantage compared to buying finished assets, with a 6%-8% yield target (versus 5.25% for pre-existing assets). The group aims to minimise risk by primarily undertaking developments which are pre-let to a tenant – speculative development is 3% of asset value.

Active Asset Management: This involves lease renewals, building extensions, and ESG upgrades to drive rental ‘reversion’ (i.e. increasing rent to current market levels).

Over the last two years, the company has tilted its strategy towards:

1. urban logistics – Through the £1.1bn acquisition of UK Commercial Property REIT (UKCM) and a major portfolio purchase from Blackstone, Tritax has expanded into ‘urban logistics.’ These smaller, last-mile hubs are closer to major cities, capturing the high demand for rapid delivery services. The integration of the Blackstone portfolio is now complete. The deal is expected to generate mid-single-digit EPS accretion in 2026. As part of the deal, Blackstone owns an 8.6% stake in BBOX, locked up until end 2026.

2. Data Centre – Recognising that their land holdings often have the power and connectivity required for digital infrastructure, Tritax is currently developing a major 107MW data centre at Manor Farm, near Heathrow, with a further 1GW pipeline. The company is employing a ‘powered shell’ model – they are not taking on the operational risk of the servers themselves but only providing the building and the massive power connection. Phase 1 is targeting exceptional returns with a 9.3% yield on cost to Tritax Big Box shareholders, considerably higher than the 6-8% target for logistics. Fundamental to this target is the JV with electricity supplier EDF Renewables. The market is currently awaiting a final determination from the Secretary of State, which is expected by 17 March.

At the end of 2025, the £7.9bn portfolio was spread across more than 100 logistics assets and around 128 investment tenants, with a weighted average unexpired lease term of 10.2 years. The largest tenant is Amazon, representing 13% of rental income.

The logistics market is uncertain – industry vacancy is 8% - with customers reluctant to enter into build-to-suit agreements due to the lack of macroeconomic visibility. Vacancy levels at Tritax were stable at 5.6%, with a decline in underlying vacancy offset by that inherited as part of the Blackstone asset acquisition.

The group’s portfolio offers a secure and growing income – 23% of rent is generated by leases having an unexpired term of more than 15 years and 25% from leases expiring within five years which provide near-term asset management opportunities.

In 2025, net rental income increased by 10.6% to £305.3m, slightly above company guidance of £300m. Growth was driven by a full contribution from the UKCM acquisition, attractive levels of asset management, and development-related rental growth offset by asset disposals.

The group achieved 4.2% EPRA like-for-like rental growth reflecting ongoing market rental growth and higher proportion of reviews.

The contracted annual rent roll increased by 15.1% to £360.9m, with £52.8m added by the UKCM portfolio acquired, offset by £24.1m from asset disposals. In addition, asset management initiatives secured £14.2m of additional contracted rent, with £6.9m from rent reviews, reflecting an average 10.4% increase in passing rent, and 35.5% increase across all open market reviews. Another £7.3m came from other asset management initiatives.

The acquired urban logistics assets delivered strong performance with an 18% increase in UKCM logistics assets contracted rent over the 19-month period since acquisition and multiple asset management initiatives underway across the Blackstone assets.

The growing rental stream and predictable cash flow means the group can adopt a progressive dividend policy, with the intention to pay out more than 90% of adjusted earnings. The 2025 payout has been lifted by 4.4% to 8.0p, equal to a yield of 4.8%. With adjusted EPS up 4.1% to 8.38p, the payout ratio was 95%.

Underlying vacancy is 2.3%, with a further 3.3% from recently-completed developments to give a total vacancy of 5.6%, with the potential to add additional rent of £14.7m per annum.

A 28% embedded portfolio rental reversion provides potential to capture £101m of additional rent, of which 73% has the potential to be captured in the next three years, supporting future earnings growth. The ambition is to grow adjusted earnings by 50% by the end of 2030.

Tritax continues to crystalise value through asset sales and recycle capital into higher-returning development and investment opportunities. In 2025, the group made £416m of disposals including the £204m of non-strategic UKCM assets highlighted above. 80% of UKCM non-strategic portfolio has now been sold or exchanged consistent with original guidance at the time of acquisition.

On the development front, the group is seeing positive progress across a range of logistics schemes, with a 55% increase in pre-let discussions compared to 12 months ago. In 2025, £3.9m of contracted rent was secured. There was 1.4m sq ft of development starts with a yield on cost of 7-8%. At the year-end, 1.8m sq ft was under construction with rental income potential of £19.6m, of which 53% has been pre-let.

Overall, the combination of record rental reversion and a significant development pipeline gives the group the capability to more than double its rental income over the long-term (to £750m).

The group remains financially robust – in 2025, LTV rose from 28.8% to 33.2%, reflecting the £1.04bn cash consideration paid for the Blackstone portfolio. This is in the middle of the 30%-35% target range – with substantial covenant headroom. On a pro-forma basis when including assets exchanged, but completing post year end, LTV is 32.7%. The current weighted average cost of debt is only 3.6% (up from 3.1% in 2024), with an average maturity of 4.3 years and 72.7% of drawn debt either fixed or hedged. Moody’s upgraded the company’s credit rating as a reflection of its growing scale, increased portfolio diversification and continued focus on resilient, high-quality logistics assets.

The portfolio equivalent yield remained broadly stable at 5.7%. The EPRA cost ratio fell from 12.6% to 12.4%, driven by UKCM synergies and efficient externally managed structure. Including vacancy costs, it rose from 13.6% to 13.8%, reflecting assumed vacancy from UKCM acquisition.

The EPRA Net Tangible Assets (NTA) per share rose by 1.2% to 187.76p. The total accounting return was 5.5%, or 8.5% excluding items considered non-recurring.

There are risks with the company: execution Risk (delays in planning permissions or power grid connectivity), financing risk if interest rates rise, and market risk driven by a slowdown in UK consumer spending that could dampen occupier demand.

Source: Bloomberg