Morning Note: Market News and Updates from InterContinental Hotels and Vonovia.

Market News

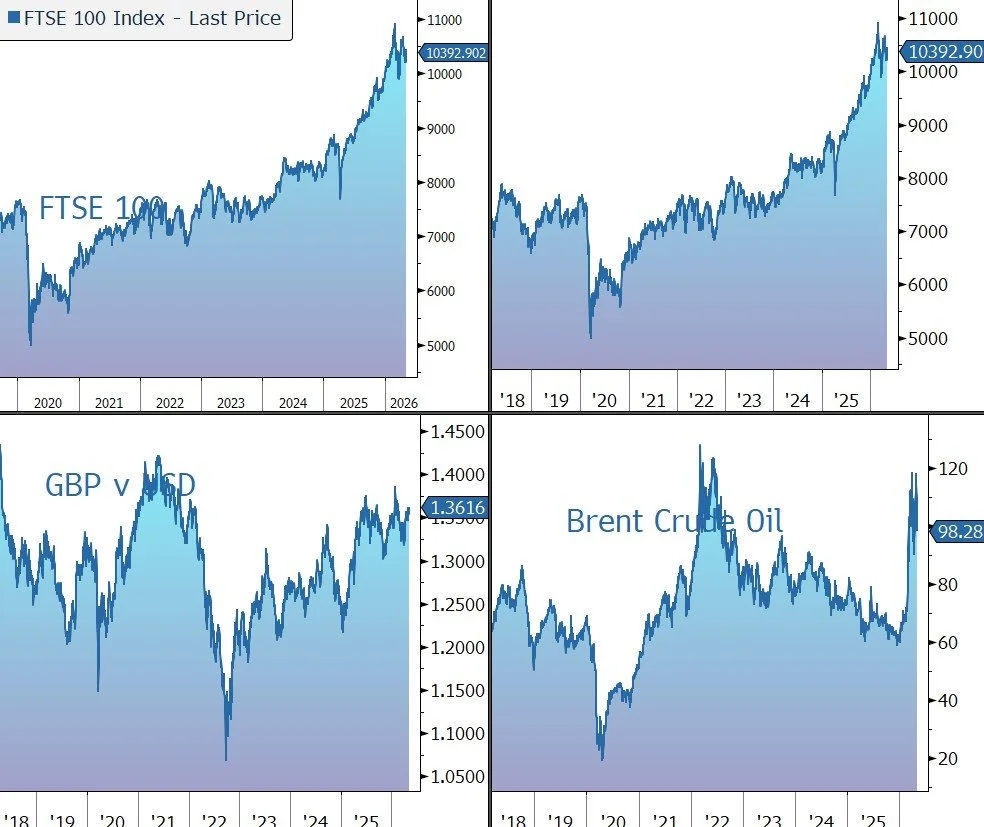

Risk assets jumped as hopes for a US-Iran agreement triggered a sharp decline in oil prices - Brent Crude is below $100 a barrel – and helped ease inflation worries. Reports indicated that the US had sent a one-page Memorandum of Understanding through Pakistani mediators aimed at formally ending the conflict and potentially allowing the gradual reopening of the Strait of Hormuz. Tehran is expected to respond in the coming days after confirming it was reviewing a US peace proposal, while more comprehensive negotiations over Iran’s nuclear program are reportedly expected later.

However, Federal Reserve Bank of Chicago President Austan Goolsbee warned that inflation has not continued to cool toward the US central bank’s 2% target and has instead accelerated since the outbreak of the war. Gold is trading at $4,750 an ounce following a 3% jump during yesterday’s session, while the yield on the US 10-year Treasury has fallen back to 4.35%.

US equities rose last night: S&P 500 (+1.5%); Nasdaq (+2.0%). In Asia, markets also moved higher: Nikkei 225 (+5.6% to an intra-day high); Hang Seng (+1.5%); Shanghai Composite (+0.5%). South Korea, a bellwether for tech investments, surpassed Canada as the world’s seventh-largest equity market by value.

The FTSE 100 is currently trading 0.5% lower at 10,393, held back by the fall in the large oil stocks. Shell released Q1 results slightly above expectations and announced a new $3bn share buyback. Companies trading ex-dividend today include Admiral (2.69%), Glencore (1.12%), RELX (1.80%).

Voters in England, Scotland, and Wales head to the polls in a key test of support for Keir Starmer as Labour’s popularity declines due to policy missteps and tax increases. Bank of England officials joined private forecasters in questioning rosy economic data, warning it may be misleading and complicate rate decisions, people familiar said. Sterling trades at $1.3620 and €1.1575, while 10-year Gilt yields have fallen back below 5%.

Source: Bloomberg

Company News

InterContinental Hotels Group (IHG) has released Q1 2026 results which were better than expected, with very strong trading performance, benefiting from the company’s diverse global footprint and better than expected demand in most regions around the world. Room development momentum has continued, with underlying signings and openings ahead of last year. Growth has continued into April, and the company is confident of achieving consensus growth forecasts and profit expectations. The shares have been a strong performer over the long term and in response to today’s update they are up 3% in early trading ahead of the analysts’ meeting.

IHG owns a portfolio of 21 attractive brands across all price tiers (including Crowne Plaza, InterContinental, Holiday Inn, and Six Senses) and has a strong operating system, both of which drive customer loyalty and pricing power. The group operates a highly scalable, asset-light model, based on franchising and management contracts, with low capital intensity and high returns. The model also means the group doesn’t own hotels or bear the operational costs of running them. The company is focused on delivering industry-leading net rooms growth over the medium term. It currently has a 4% global market share and a 10% share of the new room pipeline. At the end of March 2026, the global estate was just over a million rooms across 7,014 hotels, with 66% in midscale segments and 34% in upscale and luxury. Annual gross revenue generated by the group’s hotels is more than $35bn.

Long-term growth is being driven by a rising global middle class with a desire to travel – Oxford Economics forecasts this cohort to nearly double in size to over 670m households by 2035, with China accounting for almost half of the growth. Global leading hotel brands are expected to continue the long-term trend of taking market share. In periods when developers are adding less new supply, revenue growth from existing room inventory is expected to be stronger, as are conversion opportunities, which IHG has proven highly successful at capturing.

The group’s medium- to long-term financial framework targets:

· high single-digit growth (i.e. 7%-9%) in fee revenue, through a combination of growth in RevPAR (revenue per available room, the key measure of industry performance), system size, and ancillary revenue. In addition, the company expects 100-150 basis points of fee margin expansion annually on average. This excludes the positive margin impact of the credit card business.

· 100% conversion of adjusted earnings into adjusted free cash flow, supporting investment in the business to optimise growth, sustainably growing the ordinary dividend and returning surplus capital.

· 12-15% adjusted EPS compound annual growth rate, including the assumption of ongoing share buybacks.

From the start of 2026, the trading currency of the group’s shares on the LSE changed from Sterling to US dollars. The move does not affect the nominal currency of the shares, which remains in Sterling, nor does it impact IHG’s London listing or its New York ADR listing. Shareholders based in the UK will continue to receive dividend payments in Sterling. The company’s aim is to better align its share price with its financial performance – the company already reports its results in US dollars – and simplify investment appraisal.

In the first quarter of 2026, the company delivered very strong trading performance, benefiting from a diverse global footprint and better-than-expected demand in most regions around the world. This resilience has been helped by a heavy weighting to domestic and intra-regional travel.

Global revenue per available room (RevPAR) grew by 4.4%, ahead of the 3.3% growth expected by the market. Growth in occupancy – up 1.5 percentage points – was supplemented by an increase in pricing, with average daily rate up 2.0%.

By sector, global rooms revenue on a comparable basis was strongest in Groups (+7%) and Business (+6%), with Leisure (+1%) lagging.

There is still a wide regional variation across the business.

· In Americas (the group’s largest division), RevPAR was up 3.6%. The US (+3.4%) saw notable strength on top of good growth this time last year. With a continuation of good trading in the second quarter to date, the rolling 8 weeks to 2 May in aggregate, which normalises for the timing shift of holiday periods within March and April, indicated a further improvement in RevPAR growth to that reported for the first quarter.

· The diverse EMEAA region grew by 5.6% despite challenges from the conflict in the Middle East. Growth moderated through the quarter, easing from +7% in the first two months to around +2% in March. This was driven by the Middle East sub-region, which accounts for 5% of IHG's system size globally.

· Greater China RevPAR rose by 5.7% with a further acceleration following a return to growth in the prior quarter, supported by strong leisure demand over the Chinese New Year festive period and an improvement in Business travel.

IHG continued to open new hotels and sign more rooms into its pipeline as owner demand for its world class brands continues to increase. 2025 was one of the group’s biggest ever years for both openings and signings. Since then, in Q1, 14.9k rooms across 82 hotels were opened, up 2% year-on-year.

Gross system growth was 6.6% year-on-year (and +1.4% YTD), while after removals, net system size growth was 5.0% year-on-year (and +0.9% YTD). Demand for quick-to-market conversions to IHG’s brands continues to be high, representing 35% of openings and more than half of signings in the quarter. This is a big positive given the time to open is much shorter than with a new build.

IHG signed 21.4k rooms (163 hotels) in the quarter, up 6%, in underlying terms excluding the acquisition of Ruby, a premium urban lifestyle brand. This included the first signing for the new Premium brand Noted Collection in EMEAA and the arrival of the Essentials conversion brand Garner into Greater China. This leaves a global pipeline of 343k rooms (2,347 hotels), up 3% year-on-year, and 33% of the current system size, providing good growth visibility. Around 50% of the global pipeline is under construction.

As usual at this stage of the year, the group doesn’t provide an update on profitability or its financial position. The asset-light model means IHG has low investment requirements and a negative working capital cycle. The group operates a conservatively leveraged business model and maintains strong liquidity. At the end of 2025, net debt was $3.3bn, with gearing of 2.5x net debt to EBITDA, at the lower end of its 2.5x-3.0x target range.

The group is returning surplus capital through share buybacks. A $900m programme was undertaken in 2025 and a further $950m programme is expected to be completed by the end of 2026, with $240m repurchased so far. In addition, the 2025 dividend was raised by 10% to 184.5c (1.2% yield). In total, the company expects to return more than $1.2bn to shareholders in 2026, amounting to 5% of the current market cap.

Looking ahead, the company’s comparable on-the-books global revenue for Q2 indicates continued growth, with the impact of the Middle East conflict and some wider disruption to international travel flows expected to be more than offset by increases in demand elsewhere. While still early, management’s confidence of achieving full year consensus growth forecasts and profit expectations is underpinned by the strength of the company’s performance year-to-date. IHG has also confirmed its mid-term target to generate compound growth in adjusted EPS of 12%-15% annually on average.

Source: Bloomberg

Property News

Vonovia has released its Q1 2026 results which highlight a good start to the year with performance in line with expectations. Full-year guidance for 2026 and 2028 have been reiterated. Despite the improved sector outlook, the shares have been weak over recent weeks, tracking the upward move in bund yields, driven by inflation concerns arising from the conflict in the Middle East and slightly higher financing costs. Ahead of this afternoon’s analysts’ call, they are down 1% in early trading, leaving them on a 52% discount to NAV.

Vonovia is Europe’s largest residential real estate company with a market cap of around €19bn. The group owns around 531k units worth around €84.7bn across Germany (c. 85%), Sweden, and Austria. The group also manages a further 76k units owned by others. Despite its size, in Germany Vonovia still only owns 2% of a highly fragmented market. The focus is on multi-family housing for low- and medium- income tenants in metropolitan areas. The aim is to benefit from residential megatrends such as urbanisation, energy efficiency, and demographic change.

Following a number of acquisitions, Vonovia now enjoys the benefits of increased scale – over the last 12 years, its adjusted EBITDA operations margin has risen by 20 percentage points to 80% and its cost per unit has fallen by two thirds.

Following the appointment of its new CEO earlier in the year, the company introduced some new strategic priorities including tighter leverage targets, enhanced disclosure, improved transparency, and an amended dividend policy.

In the first quarter of 2026, adjusted EBITDA rose by 1.4% to €711.6m, meeting expectations. Vonovia is well on track to achieve its target for 2026 and notes that, based on experience, sales activities tend to gain momentum over the course of the year. Adjusted earnings before tax (EBT) – the group’s preferred profit metric – fell by 4.1% to €462.2m, primarily impacted by c. €20m in higher financing costs. Operating free cash flow (OFCF) – the key figure for internal financing and thus liquidity management – was down 43% to €363.9m, primarily due to a net working capital reduction of c. €200m resulting from the ramp-up of investments and the acquisition of a manage-to-green portfolio.

The most recent market data for the German residential sector suggests a phase of cautious stabilisation. While the broader economic recovery remains gradual, the structural supply-demand imbalance continues to drive a positive rent trend and improved assets values.

Vonovia’s core rental segment continued to benefit from a positive market environment. Earnings grew by 6.3% to €629.7m, despite having 4,000 fewer homes. The vacancy rate remains very low (2.3%) and highlights the ongoing mismatch between supply and demand. The trend towards higher rents continued, while the collection rate was over 99%. This includes all ancillary and energy costs, which management see as a strong sign of affordability.

The organic increase in rent was 4.0%, with new construction accounting for 0.4%. Like-for-like rental growth of 3.6% was driven by market-related factors (+2.6%) and investment in existing buildings (+1.0%). The monthly rent per square metre increased by 3.8% to €8.46. Going forward, under the regulatory system, rent growth is expected to follow inflation higher over time albeit with a lag. For 2026, rental growth is expected to be 4.2%. Further out, the expectation is ‘around 5%’ driven by an additional investment in modernisation.

The three non-rental segments are: development (-74% to €13.6m), recurring sales (-4.7% to €18.2m), and value-added services (+30% to €50.1m). Overall, the company is seeing continued signs of increased traction in these segments and is targetting multiple organic growth initiatives to develop non-rental activities. In 2028, the group estimates a contribution of 20%-25% of adjusted EBITDA, versus 13% currently.

Vonovia continued to sell properties of inferior quality or in non-core regions. The volume of recurring sales was 49% lower in the period (at 348), albeit with the fair value step-up at 42%.

Capital is being partly re-allocated toward the construction of new properties and the improvement of the existing portfolio to comply with environmental regulations which can drive higher rents. In Q1 2026 the group spent €442m (+8%), made up of maintenance, modernisation, and new construction.

Vonovia is aiming for a higher sales volume in 2026 compared to the previous year and also intends to increase the annual volume to between 3,000 and 3,500 units.

The company’s balance sheet remains stretched – loan-to-value (LTV) declined slightly from 45.4% to 45.1% but is still above the current 40%-45% target range. Given the higher interest rate environment, the company targeting more prudent leverage metrics for 2028 for Net debt/EBITDA (<12x vs 13.7x currently) and LTV (c. 40%). Deleveraging will occur via disposals, with the company currently reviewing minority positions in non-strategic participations both in Germany and abroad.

At present, the group’s long-term and well-balanced debt maturity profile provides a hedge against increasing financing costs: weighted average maturity (6.4 years); average cost of debt (2.1%); fixed/hedged (97%). The strategy is to roll over secured debt and repay unsecured bonds with disposal proceeds. After a promising start to the year, the war in the Middle East has led to increased volatility and slightly higher financing costs for the time being.

For the dividend, the company is pursuing a progressive policy, targetting a payout ratio of between 50% and 60% of adjusted EBT. For 2025, a payment of €1.25 per share was declared, 2.5% higher than last year. This amounts to a yield of 5.6% and will be paid in June.

The like-for-like market value of the portfolio rose by 0.3% to €84.7bn in the quarter. This follows a 3% increase in 2025, supporting management’s view that the market has now bottomed out. Since no portfolio valuation is planned for the first quarter, the net asset value (known as EPRA NTA), which is the real estate value excluding debt, increased only slightly to €46.57 per share at the end of March 2026. A comprehensive portfolio valuation will be carried out on 30 June.

Guidance for 2026 has been reiterated: EBT of €1.9bn-€2.0bn and adjusted EBITDA of €2.95bn-€3.05bn. The company has also reiterated its target for EBITDA in 2028 of €3.2bn-€3.5bn.

Greater visibility over the outlook for interest rates and property market valuations will be required for the shares to move higher. Clearly, government plans to ease its fiscal rules are unhelpful, with bund yields rising in anticipation of an increase in government debt, a trend that has been exacerbated by the inflation concerns as a result of the Middle East conflict. Not only does this increase the group’s borrowing costs (and reduce free cash flow) but it also has a negative impact on property values and makes bond proxies such as real estate relatively less attractive. In the meantime, however, we are comforted by the outlook for rental growth, the improved transaction market, and the ongoing substantial mismatch between Vonovia’s equity value (€2,361 for the German portfolio), the valuation in the direct real estate market (€3,500), and the cost of newly constructed properties (€5,600).

Source: Bloomberg