Morning Note: Market News and an Update from Compass Group.

Market News

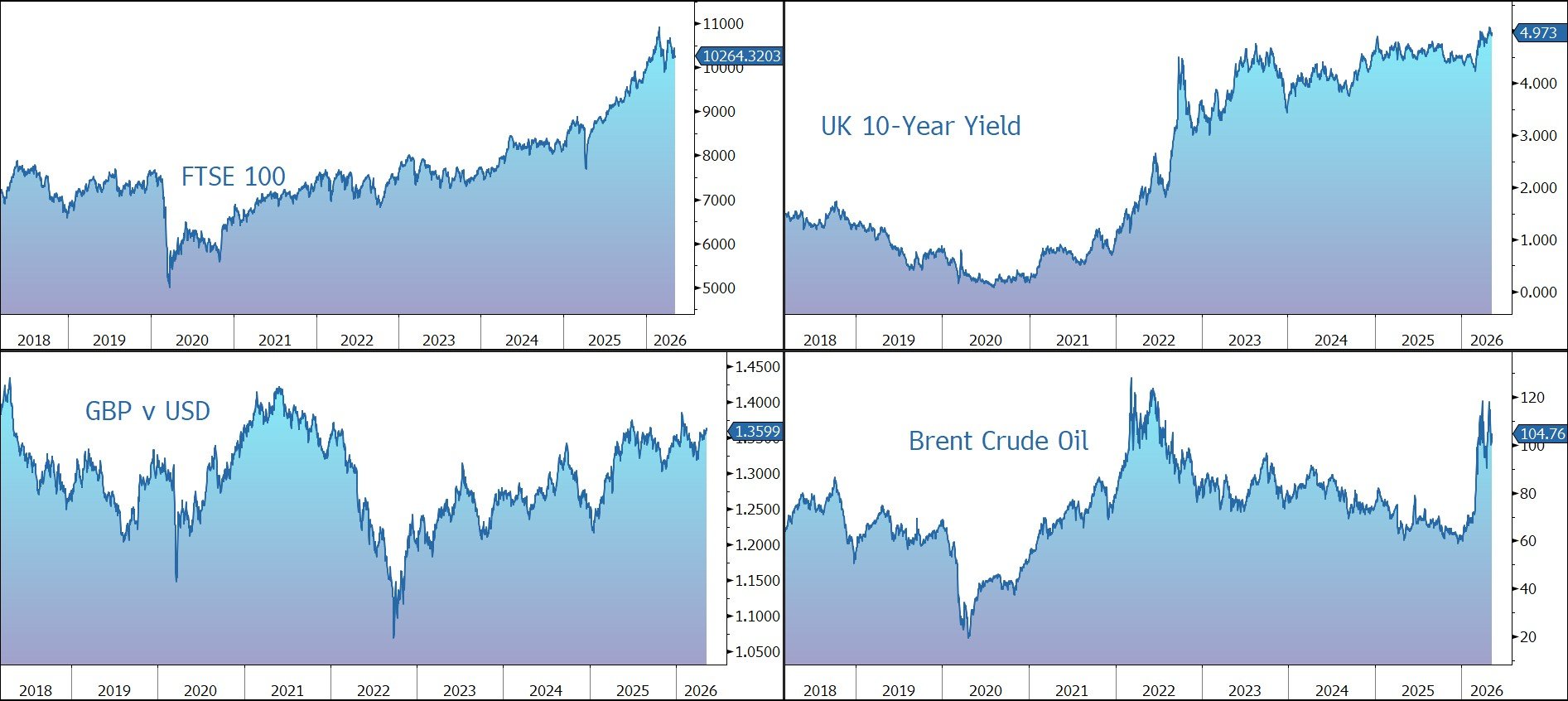

The oil price jumped - Brent Crude futures are currently $105 a barrel – along with the dollar after Donald Trump said Iran’s response to his proposal to end the conflict was ‘ totally unacceptable’. The Wall Street Journal said Tehran offered to transfer some of its uranium stockpile to a third country but refused to dismantle its nuclear facilities. Iran’s semi-official news agency Tasnim denied the report. The UK and France will lead a meeting today to discuss a Strait of Hormuz escort mission once there’s a stable ceasefire.

Trump is expected to press Xi Jinping over China’s approach to Iran and flesh out plans for a new trade board when the two meet this week in Beijing, US officials said. A successful summit may boost Chinese equities which have lagged their Asian peers.

Friday’s US non-farm payrolls came in at 115k, well above the forecast of 65k but below the previous month’s 178k. The unemployment rate of 4.3% was in line with expectations. In addition, the Michigan Consumer Sentiment survey showed confidence fell to a record low. Markets continue to expect the Fed to keep interest rates largely unchanged through the rest of the year. The yield on the US 10-year Treasury is 4.39%, while gold has slipped to $4,675 an ounce.

In Asia, equities were mixed: Nikkei 225 (-0.5%); Hang Seng (+0.1%); Shanghai Composite (+1.1%). US equities are currently expected to drift slightly lower at the open this afternoon. Alphabet is on the verge of overtaking Nvidia as the world’s most valuable company. It’s also planning to issue yen bonds for the first time.

The FTSE 100 is currently trading 0.2% higher at 10,264. Keir Starmer will make an effort to save his premiership in a speech today. Labour’s disappointing results in local elections have pushed Reform’s Nigel Farage closer to power. Sterling slipped to $1.3605 and €1.1550.

Source: Bloomberg

Company News

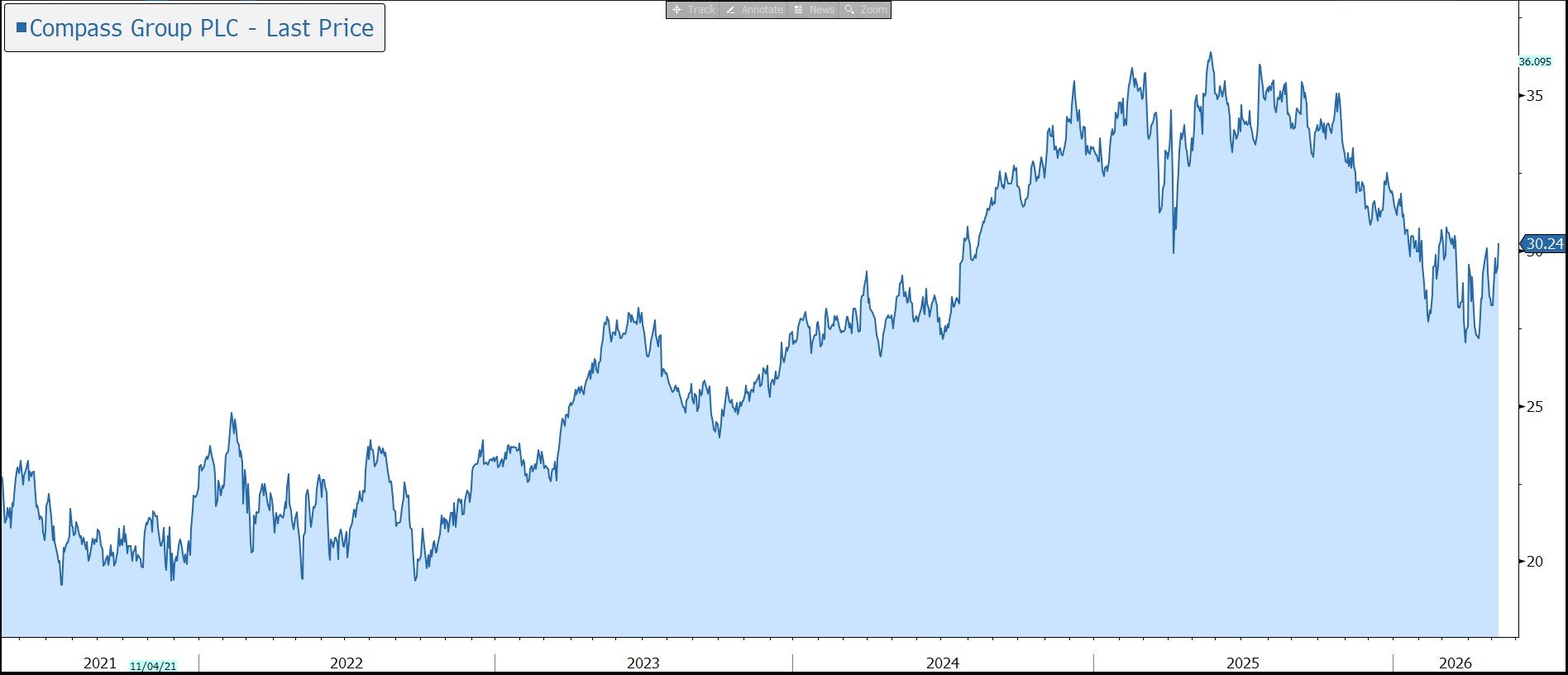

Compass Group has released results for the first half of its financial year to 30 September 2026 which were better than the market expectation and raised its full-year guidance. Strong margin progression has been driven by consistent execution and the strength of the group’s business model. With financial gearing slightly above the target range, we are unlikely to see a resumption of share buybacks any time soon. However, we believe the current strategy of reinvesting in the core business, both organically and via M&A, is a good allocation of capital and will generate strong cash flow over time. Ahead of this morning's call, the shares are trading up 3%.

Compass is the world’s largest foodservice company, operating in around 30 countries, serving over 5.5bn meals a year. The group also operates a targeted support services operation, which accounts for 15% of revenue, and a third-party food purchasing business. The company reports in US dollars, but its shares are listed in the UK.

The company operates in a $360bn global market, which has expanded by a third in the last four years, despite exits from 15 countries, with the help of acquisitions in segments which increase its captive audience. Matching the historical industry growth of 5% p.a., the market could reach $600bn by 2035.

As the largest player (albeit with less than a 15% share), the company’s scale provides a vital advantage over smaller players in terms of buying power. It is the fastest growing major operator, with the highest level of retention, and the highest margins in the industry.

The scope for growth from first-time outsourcing and share gains is significant – nearly 75% of in-house catering is still self-operated or managed by regional players. Companies and other institutions are open to outsourcing as they seek to reduce operating costs, cope with increased complexity, improve health and safety protocols, and ensure resilient food supply chains. As a result, Compass is well placed to consolidate its position as a trusted, financially strong provider, able to offer clients and consumers safe and innovative solutions. As a result, the company has an excellent pipeline of new business.

Management therefore believes net new business growth can be sustained at 4%-5%, above the historical level of 3%. This comes on top of like-for-like volume and price growth.

Although there are threats – permanently increased levels of working from home and online learning, rising unemployment (exacerbated by AI), increased competition from delivery providers, and reduced volume driven by weight-loss pills – we believe Compass is well placed to cope as a result of its diversified and defensive revenue mix, decentralised business model with predominantly local sourcing and supply chain, and a higher level of volume protection in contracts.

Compass may be a ‘physical reality’ beneficiary of the shift to AI. With 90% of operations in tangible services—like food prep and hospital sanitisation—its core business remains immune to digital replication. As ‘white-collar’ displacement expands the available labour pool, Compass should benefit from reduced wage inflation and improved margins. Strategically, Compass is using Agentic AI to slash middle-management and administrative overhead, deploying agents to manage logistics and scheduling for its 500,000+ global staff. Partnering with Google/Gemini, it has integrated AI kitchen managers that adjust inventory in real-time, cutting food waste by 15-20%.

Overall, the company has a significant runway for long-term growth. Management is confident in sustaining mid-to-high single-digit organic revenue growth, ongoing margin progression, and profit growth ahead of revenue growth.

In the six months to 31 March, revenue grew by 10.7% to $25.0bn, a touch above the market expectation of $24.8bn. Organic revenue – a combination of like-for-like volume growth, price, new business, and client retention – grew by 7.2% versus the company’s full-year guidance of ‘around 7%’.

The group benefitted from strong outsourcing trends, with net new business growth of 3.8%, just below the group’s 4%-5% target range, although growth is expected to accelerate in the group’s second half. Annualised new business wins totalled $4.1bn, up 11% year on year, with half generated from first-time outsourcing Client retention was 96%. Pricing moderated as anticipated to 2.7%, while like-for-like volume continued to contribute positively (+0.7%) to growth.

The group’s largest region, North America (67% of revenue), grew by 7.2% in organic terms, with a margin of 8.4%. Business & Industry continues to be the fastest growing sector, increasing organic revenue at a double-digit rate. In the International division, organic revenue was up 7.1%, with a margin of 6.1%. The strongest growth was in Sports & Leisure as the group successfully leveraged its expertise in North America and the UK in other markets.

During the latest half-year, the group’s margin grew by 20 basis points to 7.4%, driven by overhead leverage and M&A synergies. This is despite the cost of mobilising new contracts wins and some inflationary pressures. Underlying operating profit grew by 12% to $1,839m, versus $1,810m expected, while EPS was up 12% to 72.8c, just above the consensus forecast of 71.8c. The business continued to generate strong free cash flow, up 11% to $825m in the half-year, and spent $0.8bn, 3.4% of revenue, on capex.

As Compass focuses on the significant structural growth opportunities in its core markets, it has stepped up its M&A activity to expand its portfolio of brands, focusing on digital innovation and delivered-in solutions. Integration of the most recent deal, the $1.7bn acquisition of Vermaat, is progressing well. This adds a leading premium food services business in Europe which will be used to create a strong growth platform in a region which has consistently underperformed North America on both organic growth and margin. More recently, following the acquisition of Pro Care Management in Germany for $270m, Compass now operates Group Purchasing Organisations (GPO) in five of its top ten markets.

As a result, the company’s financial leverage has increased: net debt to EBITDA was 1.7x at 31 March 2026, as expected just above its medium-term target of 1.0x-1.5x. Compass anticipates its leverage will be above 1.5x at the end of FY2026, having peaked at the half-year stage, before falling in FY2027.

Although this clearly reduces the amount of excess cash flow available for share buybacks in the near term, we believe reinvesting in the core business is good capital allocation and will generate strong cash flow and returns over time. In the meantime, the company continues to pay an attractive dividend – the interim FY2026 payout was increased by 13% to 25.5c.

Following a strong start to the year, Compass has raised its guidance for FY2026 – it now expects constant currency underlying operating profit growth of ‘above 11%’ (vs. ‘around 10%’ previously), driven by organic revenue growth of around 7%, around 2% profit growth from M&A (including Vermaat), and ongoing margin progression. Although the revenue target still appears conservative, the company does face some tough year-on-year comparatives in FY2026.

From 1 April, the company changed the trading currency of its ordinary shares on the LSE from sterling to US dollars. This transition aligns the group’s share price trading currency with its reporting currency, reducing FX volatility in the share price and simplifying the investment case for global investors. The change has not affected the group’s FTSE index inclusion or its LSE listing. Dividends will continue to be paid in sterling unless shareholders elect to receive them in US dollars.

Source: Bloomberg