Morning Note: Market News and Updates from Experian and Johnson & Johnson.

Market News

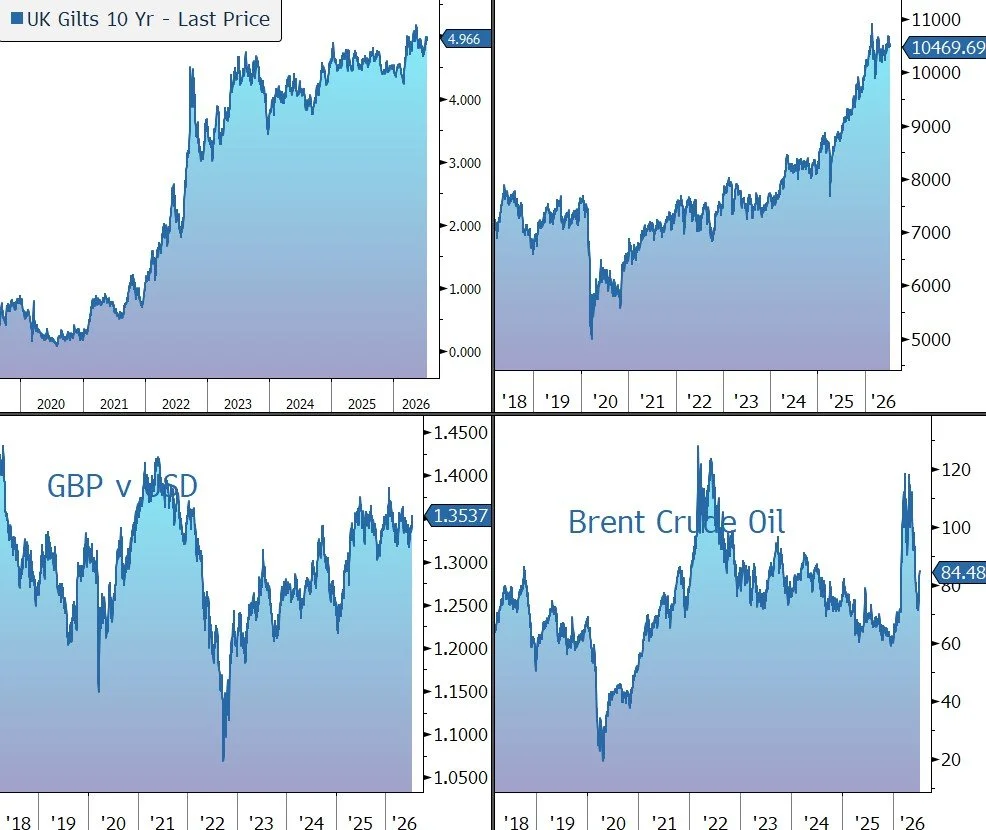

Brent crude ($85 a barrel) stayed close to a one-month high as the US stepped up its military campaign against Iran in an effort to safeguard shipping through the Strait of Hormuz. US forces carried out fresh airstrikes, targeting Iranian missile storage facilities and launch sites near the strategic waterway. Gold trades at $4,025 an ounce, while the yield on the US 10-year Treasury is 4.57%.

US equities moved higher last night – S&P 500 (+0.4%); Nasdaq (+0.6%) – led by gains in the communication services, consumer discretionary, and financial sectors. However, in Asia this morning, markets fell, dragged down by semiconductor stocks, as investors became more sceptical that the AI-driven rally can withstand lofty valuations: Nikkei 225 (-2.8%); Shanghai Composite (-2.0%); Kospi (-6.4%). South Korea will today announce measures to address the controversy over leveraged ETFs tied to Samsung and SK Hynix.

TSMC raised its full-year revenue and capex forecasts, underscoring resilient AI chip demand. Separately, the company plans to invest an additional $100bn in the US, an American official said. The shares fell by 4%.

The FTSE 100 is currently 0.4% lower at 10,470. ABB has announced a recommended cash acquisition of Rotork for 506p a share, representing a 73% premium to last night’s close, valuing the company at £4.1bn. BHP posted solid full-year production, but warned copper output will fall in the year ahead as grades decline at its flagship Chilean mines.

Sterling rose to a one-year high – $1.3535 and €1.1805 – after reports that Shabana Mahmood will be named UK chancellor by incoming Prime Minister Andy Burnham, easing concerns that Burnham could instead appoint Ed Miliband, who is widely seen as favouring a more expansionary fiscal approach.

Source: Bloomberg

Company News

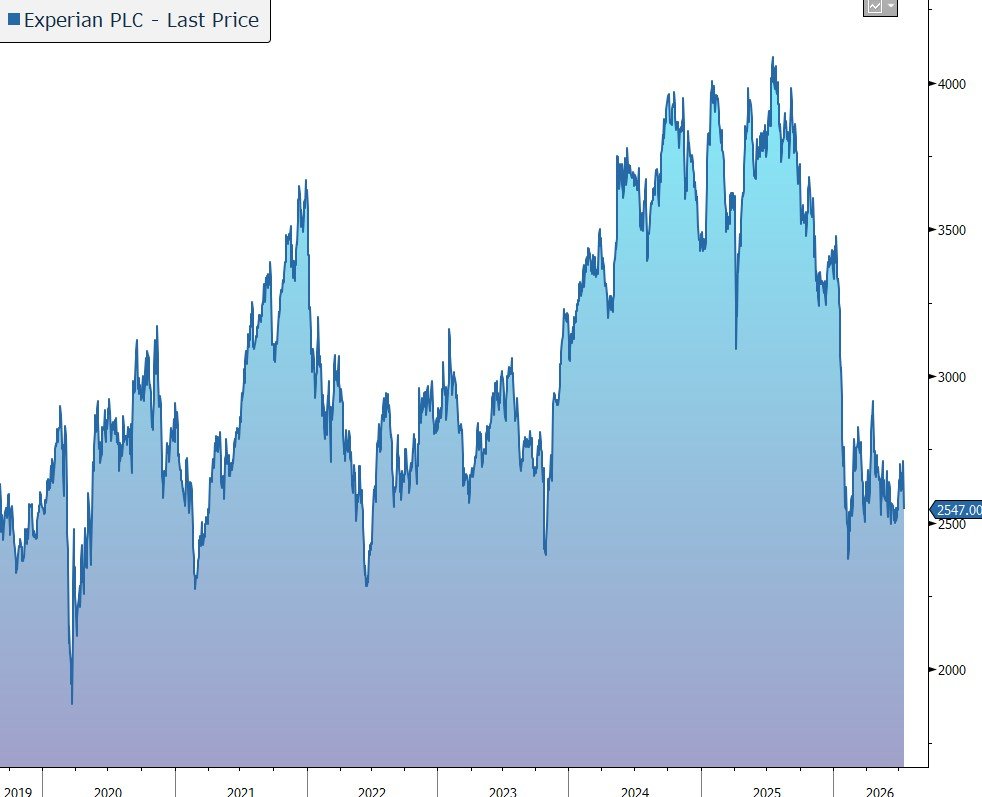

Experian has today released results for the three months ended 30 June 2026, the first quarter of its financial year to 31 March 2027. Performance was robust, albeit a slight slowdown versus the previous quarter, and the guidance for the full year is unchanged. In response, the shares have been marked down by 6% in early trading.

Experian is a global information services company that helps businesses to manage credit risk, prevent fraud, target marketing offers, and automate decision-making. The group also helps individuals check their credit report and credit score and protect against identity theft. The company has credit data on 1.4bn people and 200m businesses. The ownership of such rich, unique, and valuable data has become more important in an increasingly digital world, and the group is targeting a total addressable market of more than $140bn.

Experian operates an attractive business model where its customers supply the company with raw credit history data for free. The company aggregates it, applies analytics and tools, and sells it back to the customers as a credit report. The industry operates as an oligopoly with high barriers to entry because of large historical databases and regulatory know-how.

The company has shifted from simply selling data to selling enhanced decision tools and analytics software which are essential in automating customers’ decisions, helping to reduce costs, and managing risk. As a result, customer relationships are very ‘sticky’, with renewal rates of 90%, and revenue is very resilient. The business has a long history of weathering uncertainty – notably, revenue grew in organic terms in both the Great Financial Crisis (GFC) of 2008 and the COVID-19 pandemic of 2020. Although credit application volumes slow in a recession, we believe the company has a natural hedge of risk management and asset protection products, as well as exposure to healthcare and other defensive segments.

Regarding the potential opportunities and threats posed to the business by AI, we would highlight that AI is only as good as the data it’s trained on. Large Language Models can’t see private bank accounts or individual credit histories due to strict regulatory frameworks. As a result, we believe Experian is relatively well placed given its hard-to-replicate proprietary datasets with scope to accelerate product innovation and increase operational efficiency, ultimately enhancing margins. AI has made identity theft and fraud incredibly easy to scale (e.g. deepfake voices for bank authorisation or AI-generated synthetic identities), forcing banks and other businesses to upgrade their defences. In 2025, Experian’s fraud prevention tools, such as Ascend, helped clients avoid $19bn in losses. Furthermore, AI generated a 10%-15% uplift in coding productivity in FY2026. Labour costs, at 32% of revenue, are over 300 basis points lower than two years ago. For now, however, given the uncertainty over the development of AI and its impact on traditional business models, the market remains undecided and the share price remains depressed.

We note the announcement earlier in the year from Fair Isaac (FICO), the company behind the credit scores that lenders use, of the launch of a new Direct License Program for mortgages. Traditionally, Experian (along with its rivals) acts as the middleman, ‘marking up’ FICO scores and re-selling them to lenders. FICO’s new programme allows lenders to bypass the credit bureaus to some extent, threatening a high-margin revenue stream. That said, FICO still cannot generate a score without the bureaus’ raw data.

Although the company is listed in the UK, it reports its results in US dollars.

In the latest quarter, the group delivered revenue growth of 8% at constant exchange rates. In organic terms (i.e., underlying before M&A), growth was 7%, in the middle of its full-year guidance range of 6%-8% and compares to the 9% growth in the previous quarter. Growth was driven by new product innovation, client wins, and consumer expansion.

The company continued to leverage its scaled proprietary data assets, strong technology foundations and deep expertise to deliver on its strategic priorities and crystallise new AI opportunities. As planned, the company largely completed its cloud migration in North America and Brazil and remains on track to deliver material cost savings as dual-run costs begin to decline.

All regions contributed to organic revenue growth during the quarter. In the group’s largest division, North America, which accounts for more than two-thirds of revenue, organic growth was 7%. B2B organic revenue growth in the region was 11%. Financial services generated strong growth, driven by Ascend analytics solutions, fraud prevention products, mortgage, and stable underlying client activity. Consumer Services delivered a 2% decline in underlying organic revenue, as anticipated, following the initial wind down last quarter of two long-term mass data breach support contracts.

Growth in EMEA/Asia Pacific was only 1%, impacted by a strong prior-year comparison from several large software deliveries, albeit the company continued to advance key initiatives. Elsewhere, Latin America and UK & Ireland grew by 12% and 5% respectively.

By division, B2B revenue (73% of the total) was up 9% in organic terms, driven by new product innovation and key client wins. Within B2B, Financial Services and Verticals were up 9% and 7% respectively. The Consumer Services unit (27% of revenue) only grew by 2% in organic terms due in part to tough year-on-year comparatives.

This was a revenue update, so there was no commentary on profitability or the group’s financial position. As a reminder, the business is very cash generative, and the company ended its financial year to 31 March 2026 with financial leverage of 1.7x net debt to EBITDA, below the target range of 2.0x-2.5x.

Cash flow is sensibly reinvested in organic and strategic investments that generate attractive returns. The company has a good track record of growing its dividend – in the last financial year, the payout was raised by 11% – and is buying back its own shares, with up to $1bn expected to be repurchased in the current programme.

For FY2027, the group continues to expect to deliver another year of double-digit Benchmark EPS growth, underpinned by total revenue growth of 8–11%, organic growth of 6–8%, and margin expansion at the higher end of its medium-term framework of 30-50 basis points, at constant currency, driven by operating leverage, the reduction in dual-run costs, and continued AI-led productivity gains.

Source: Bloomberg

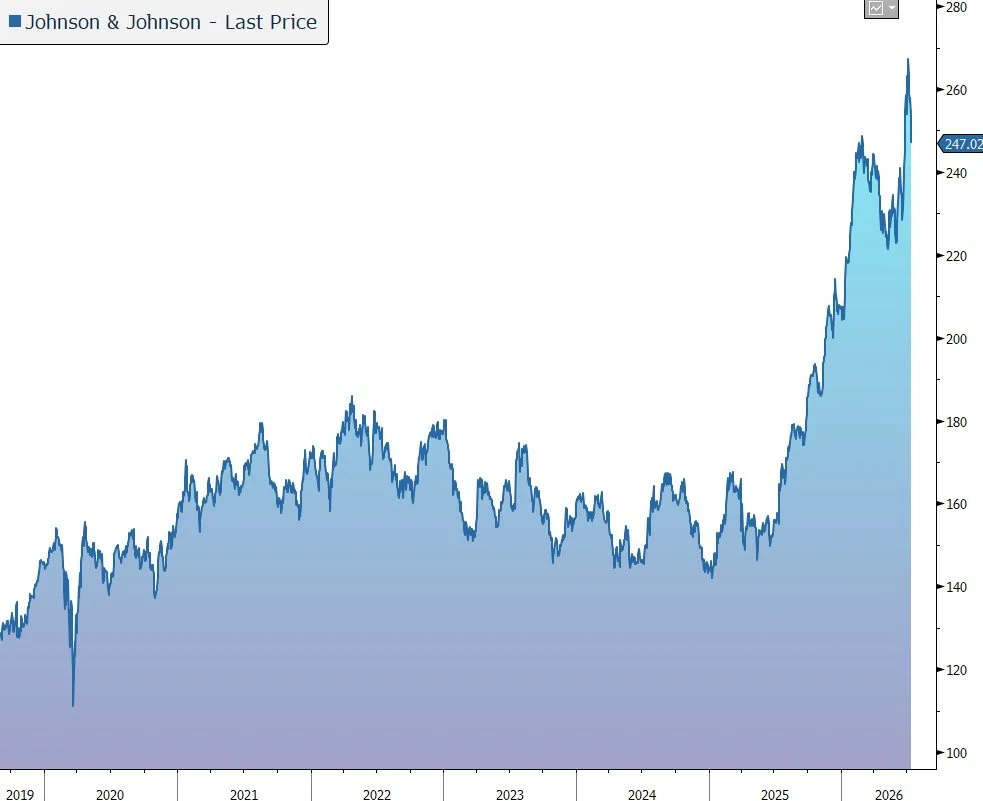

Yesterday lunchtime, Johnson & Johnson released Q2 results that were slightly better than the market expectation, driven by its strong oncology franchise. Guidance for the full year has been nudged up. In response, the shares were marked down 2% in US trading hours.

J&J is a global healthcare company with leading positions in Oncology, Immunology, Neuroscience, Cardiovascular, Surgery, and Vision. The group has 28 products/platforms, each with sales of more than $1bn. More than 75% of sales come from No.1 or No.2 global market share leading positions. The group’s strategy is to grow sales faster than the market, and to grow earnings faster than sales. Given its broad spread of businesses, J&J is considered the bellwether of healthcare companies, providing a good read-across for a range of other stocks.

J&J is undertaking a strategy of ‘shrink to grow’. The company’s former Consumer Health unit was spun off in 2023 and trades as a separate listed company, Kenvue. The company is also spinning off its orthopaedics business over the next year or so – the standalone DePuy Synthes will be the largest, most comprehensive orthopaedics-focused company in the world, currently generating sales of more than $9bn. In the meantime, J&J is also actively exploring a potential outright sale of the business.

During the three months to 30 June, reported sales grew by 6.6% to $25.3bn, a touch above the market forecast. On an adjusted operational basis, which excludes the impact of acquisitions and disposals, sales grew by 5.7%, with US domestic sales (+7.4%) outpacing international sales (+3.5%).

Innovative Medicine (i.e., Pharmaceuticals, 65% of sales) grew by 6.9% in the quarter to $16.4bn. Growth was driven by a broad range of products including cancer drug Darzalex and Neuroscience product Spravato. Growth was partially offset by an approximate 760 basis points impact from Stelara in Immunology.

MedTech (i.e., medical devices, 35% of sales) increased by 3.7% to $8.9bn, slightly short of market expectations. Growth was driven primarily by wound closure products and biosurgery products in Surgery, electrophysiology products and Shockwave in Cardiovascular, contact lenses in Vision, and trauma in Orthopaedics.

Adjusted EPS grew by 5% to $2.90, better than the consensus forecast of $2.85. J&J has raised its dividend for 63 consecutive years. In the current quarter, the payout was raised by 3% to $1.34 per share, implying a full-year yield of 2%.

J&J has a very strong balance sheet and ended the first half with net debt of $28.2bn on the back of free cash flow generation of $8.7bn in Q2. The group has consistently invested in organic growth – R&D spend was $3.7bn in the quarter – and, as a result, around 25% of sales come from products launched in the last five years.

Guidance for 2026 has been raised. Reported sales are expected to be $101.1bn (vs. $100.8bn previously), with growth in adjusted operational terms of 6.5% at the midpoint. Adjusted EPS is expected to be $11.68 (vs. $11.55 previously), up 8.2% at the midpoint.

Source: Bloomberg