Morning Note: Market News and Updates from Atlas Copco and Assa Abloy.

Market News

Equity markets are trading lower as investors continue to shy away from chipmakers on concerns that AI has driven unrealistic valuations. The main US indices fell last night – S&P 500 (-0.5%); Nasdaq (-1.5%) – and are expected to notch up further losses at the open this afternoon. Alphabet fell 4% after it was reported that Google is months behind on delivering its Gemini 3.5 Pro AI model. SpaceX fell post-market after the company scrubbed the test launch of its Starship rocket from its facility in South Texas when some of its engines didn’t fire up.

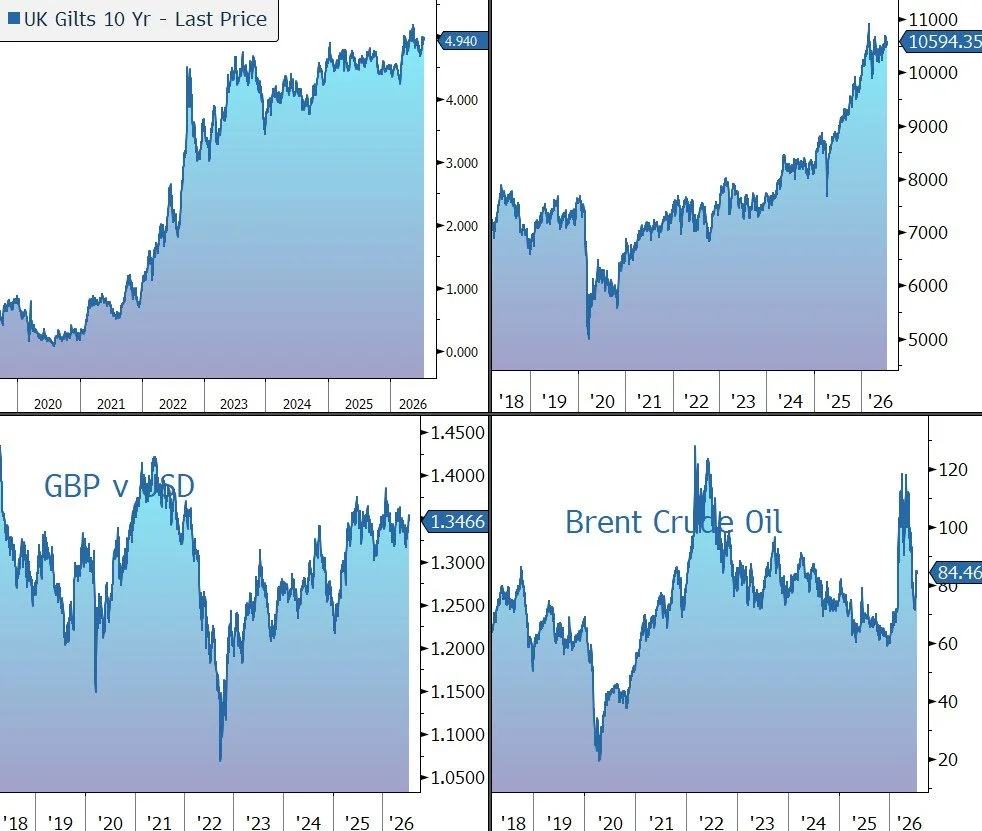

The negative sentiment continued in Asia this morning: Nikkei 225 (-4.0%); Hang Seng (-2.0%); Shanghai Composite (-2.6%); Kospi (-6.4%). Given its minimal tech exposure, the FTSE 100 is an outlier and is currently trading 0.3% higher at 10,594.

The US completed a fifth consecutive day of strikes against Iran, including on an oil tanker near Iran’s main export terminal. Tehran earlier fired at American bases in Kuwait and Jordan. Brent crude trades at $84.30 a barrel.

The yield on the 10-year US Treasury note steadied around 4.56% and was on track to finish the week little changed, as investors balanced softer US inflation data against the escalating conflict between the US and Iran and its potential impact on the interest rate outlook. Gold is trading just below $4,000 an ounce.

Andy Burnham will take over as prime minister next week after a decade outside national politics. He is expected to back North Sea oil and take control of Thames Water. Sterling trades at $1.3470 and €1.1766, while the 10-year Gilt yields 4.94%.

Despite a record trading quarter, Bank of America, Wells Fargo, Citi, Goldman. and Morgan Stanley collectively cut headcount by 10,000+ in Q2 — the largest quarterly decrease since at least 2020.

Source: Bloomberg

Company News

Yesterday lunchtime Atlas Copco released Q2 2026 results which were better than the market forecast. Order growth in the semiconductor market was particularly strong, although demand across many other sectors was also firm. Looking forward, in the near term the group expects customer activity to remain at the current strong level. In response, the shares, which are listed in Sweden, were marked up by 4%. We remain positive on the long-term outlook for the company as it is a quality compounder exposed to attractive growth trends.

Atlas Copco is a world-leading manufacturer of innovative compressors, vacuum solutions, generators, pumps, power tools, and assembly systems. The group has a diverse customer base made up of general manufacturing (22%), process industry (20%), electronics/semis (16%), construction (12%), auto (10%), and other sectors (20%). The products help the customer increase operational performance, save energy costs, reduce contamination, cut down on failures in the field, lower noise levels, and extend service intervals. They are almost always critical to its customers’ operations.

As a result, the company provides exposure to a broad range of trends: demand for increased energy efficiency and reduced emissions; increased use of lightweight materials in transport industries; the transition from petrol to electric vehicles; increased use of demanding materials and production environments in processes for semiconductor and industrial production; increased production automation and smart factories; demand for improved ergonomics; and increased demand for digitally-supported service offers. Overall, the company will therefore play a role in the effort to reorganise and improve the resilience of supply chains, bring manufacturing closer to domestic markets, and increase automation in the face of higher labour costs or deteriorating demographics. Finally, over time the vacuum business should benefit from the expansion of the North American semiconductor manufacturing market.

Product innovation lies at the heart of the business, with recent events highlighting the group’s ‘factory of the future’ initiatives, including advanced battery-powered torquing tools, automated dispensing systems, and vision-enabled machine systems. In the current environment, energy efficiency is a key driver of innovation – a new hybrid generator is capable of delivering up to an 80% reduction in fuel consumption compared to standard diesel units.

The company is a giant in its niche – it is three times the size of its nearest competitor in Compressors and has a near-50% market share in semiconductor vacuum. The group is also the No.1 in most Industrial and Power equipment niches in which it operates.

The target is to increase revenue by 8% p.a., primarily through organic means, complemented by selective acquisitions of companies in or close to existing core competencies. Using a decentralised structure, the company lets these small bolt-on companies run autonomously while plugging them into its global service network.

The group operates an asset-light strategy – only components that are critical to the performance of the equipment are manufactured in-house. The company has integrated itself with its customers and can provide rapid and extensive support to their installed base of equipment. Almost 40% of revenue (and c. 60% of operating profit) is generated from service (i.e., spare parts, maintenance, repairs, consumables, accessories, and rental). This is more stable than equipment sales and provides a strong base for the business and greater resilience in difficult times. The cost of the group’s equipment is low relative to the customer’s overall operating costs, and as a result, the company has strong pricing power, helpful when trying to pass on raw material cost inflation or tariffs. Atlas Copco is based in Sweden and reports in Swedish Krona (SEK).

The Wallenberg Family (through its holding company, Investor) is the largest shareholder of Atlas Copco, having overseen its entire history, and has a member on the Board. The business is run for the long term in a way that ensures it is passed on to the next generation in better shape than it was inherited, with a focus on consistent operational culture, financial prudence, and sensible capital allocation.

During the second quarter of 2026, the overall demand for Atlas Copco’s equipment and services improved notably and order intake in the quarter was better than expected. The company saw very strong demand for vacuum equipment, sharp growth for gas and process compressors, and solid growth for industrial compressors.

Revenue increased by 9% in the quarter to SEK 45.0bn, above the market forecast of SEK 43.9bn. In organic terms, which excludes M&A (+4%) and currency (-3%), revenue was up 8%. This compares to a flat result in the previous quarter. The group continued to see positive price growth across all segments. Order intake was up 26% in organic terms in the quarter to a record SEK 50.95bn. The result was primarily driven by increased demand for products to the semiconductor industry, although most other industries generated solid growth as well. North America was particularly strong (+49%). China also enjoyed strong growth in most product lines.

Atlas Copco operates through four divisions or ‘Techniques’, with the performance in the latest quarter as follows:

· Compressor Technique (45% of 2025 sales) is the world leader in the provision of compressed air and gas solutions, such as industrial compressors, gas and process compressors and expanders, air and gas treatment equipment and air management systems. During the latest quarter, organic revenue and orders rose by 3% and 19%, respectively. Order volumes for gas and process compressors recorded a sharp increase, while demand for industrial compressors improved, resulting in solid order growth.

· Vacuum Technique (22% of sales) provides vacuum products, exhaust management systems, valves and related products. Organic revenue rose by 19%, while orders jumped by a stellar 59%. Order intake for vacuum equipment increased sharply, primarily driven by record orders from the semiconductor industry, while scientific and general industrial vacuum applications generated significant growth as well. On the analysts’ call the CEO revealed that to meet the sheer volume of customer demand for advanced and mature semiconductor nodes, Atlas Copco is currently working to more than double their production capacity at certain key semiconductor-focused factories. Although this will impact near-term margins, the medium term upside is attractive.

· Industrial Technique (16% of sales) provides industrial power tools, assembly tools, machine vision solutions, quality assurance products, and the associated software and service. Organic revenue and orders both rose by 11%. Order volumes for industrial assembly equipment and vision solutions increased in both the general industrial and automotive markets.

· Power Technique (17% of sales) provides a range of portable air and power, industrial and portable flow solutions. The business unit also provides specialty rental and service through global network. Organic revenue and orders rose by 9% and 14%, respectively. The demand for portable compressors, portable pumps, and generators increased, resulting in solid order growth for power equipment.

Atlas Copco generates attractive margins, with gross margin above 40%, providing some shelter against rising raw material costs, and operating margin above 20%. In Q2, adjusted operating profit increased by 12% to SEK 9.46bn, above the SEK 9.25bn market forecast. The margin rose by 60 basis points in organic terms to 21.0%, predominately explained by a combined volume, price, and mix effect, and to a lesser extent by a favorable currency effect, while dilution from recent acquisitions affected the margin negatively. On the analysts’ call, the company said there is scope to push up the margin further as volume scales up. EPS rose by 8% to SEK 1.45.

The return on capital employed is very high. Although it has slipped over the last 12 months from 26% to 24%, it is still well above the group’s 20% target and 8.0% cost of capital. The group continued to consolidate its industry with acquisitions, with 29 deals closed in 2025 and a further nine in the first half of 2026.

The company has a robust balance sheet and continues to generate strong operating cash flow (+11% to SEK 6.8bn in Q2). Net debt ended the quarter at SEK 22.3bn, well above the SEK 16.5bn of a year ago, mainly due to acquisitions. However, financial gearing is a very comfortable 0.5x net debt to EBITDA, while interest-bearing liabilities have an average maturity of 4.1 years. The dividend policy is to pay out 50% of net income. For 2025, the group approved an ordinary payout of SEK 3.00 per share, in line with the previous year, and an extra distribution of SEK 2.00 per share, resulting in a total combined dividend of SEK 5.00 per share to be paid in two equal installments and equivalent to a 2.8% yield. We believe this sends a strong signal of management confidence.

The group provided brief commentary on the near-term outlook, highlighting that it expects customer activity will remain elevated at the current strong level.

Source: Bloomberg

Assa Abloy has today announced its Q2 2026 results which highlighted the benefit of a decentralised operating model against a backdrop of ongoing global geopolitical tensions and macroeconomic uncertainty. The results came in ahead of market expectation, with an acceleration in organic sales growth and a strong quarterly margin. Importantly, the group reported a small sales growth in the key North America Residential segment. In response, the shares are up 4% in early trading, against a weak overall market backdrop.

Assa Abloy is the global leader in access solutions to physical and digital places, with a portfolio of well-known global and local brands, such as Yale, Union, HID, and Lockwood. Products include doors, sensors, locks, alarms, fencing, gates, and identity systems. Products are either offered on a standalone basis or combined to form a complete, full-service access offering.

The key long-term drivers of the $100bn industry are:

· increased demand for safety and security

· movement of people and demographic change

· increased wealth in emerging markets

· the shift to digital and electronic technologies which have grown at 4-5x the rate of mechanical products over the last 10 years

· the development of sustainable buildings to meet climate change objectives

· the shift towards touchless (hygienic) activation points, automated doors, and location services

· constantly changing local market regulations which make it difficult for smaller operators to compete.

As the brand leader in most markets, with a large installed base, robust pricing power, and strong distribution channels, we believe Assa Abloy is well placed to take advantage of these trends. The strategy is to actively upgrade the installed base, generate more recurring revenue, increase service penetration, and expand exposure to emerging markets. The group’s broad offering is also well suited to address the fast-growing data centre market.

Assa Abloy has a strong track record of innovation and continuously enhances its offering with new products, solutions, and technologies. The aim is to generate a quarter of sales from products launched in the last three years.

The company has a decentralised operating model and a strong track record of cost control. The latest Manufacturing Footprint Programme (MFP), the group’s tenth, was launched last year, and is proceeding to plan. It is expected to generate annual savings of about SEK 1bn (c.60 basis points of margin) from 10 factory closures and 1,300 headcount reductions. The company has already hinted at the initiation of MFP 11.

Overall, the long-term financial target is to generate annual sales growth of 10%, half organically and half from acquisitions. An operating margin of 16%-17% is the target over the business cycle, although the aim is to be towards the upper end of the range in the coming years. Management has previously said it needs to generate organic top-line growth of 3% to offset inflation and drive the margin forward. The group is on track to exceed its target to generate SEK 25bn of profit from SEK 150bn of sales in 2026, while the 2030 target is SEK 41bn of profit from SEK 250bn of sales.

Assa Abloy is a textbook example of late cycle business – locks are one of the last things in a building and are changed when you’ve moved. The current macroeconomic environment is mixed, especially in the residential market that accounts for a third of sales. However, strong exposure to the aftermarket and operational agility continue to be a great advantage.

During the three months to 30 June 2026, ongoing global geopolitical tensions and macroeconomic uncertainty have impacted many customer segments and geographies. In this environment, the company has once again shown resilience and strong execution.

Net sales rose by 3% to SEK 39.3bn, a shade above the market forecast of SEK 39.1bn. In organic terms, which strips out the impact of acquisitions & disposals (+2%) and a currency headwind (-3%), sales rose by 4%. This was an acceleration versus the 2% reported in the previous quarter. Growth was made up of 2% volume and 2% price growth.

The group continues to actively upgrade the installed base by shifting customers from mechanical to electromechanical and digital solutions. Organic sales in the regional divisions in this category grew 8% in the quarter, driven by demographic changes – a digitally-native younger generation and an aging population in need of care, are accelerating the need for more convenient, reliable, and efficient electromechanical and digital solutions.

The company is organised into three regional units and two global divisions.

· The EMEIA region delivered organic sales growth of 5%, driven by very strong growth in Central Europe and strong growth in the Nordic region.

· The Americas reported organic sales growth of 4%, supported by continued strong growth in the non-residential segment and Latin America. Importantly, the group saw a small sales growth in the North America Residential segment.

· Global Technologies (a separate global division) reported organic sales growth of 4% in the quarter with strong sales growth in most areas, partly offset by weaker project-related businesses in Europe.

· Entrance Systems (a separate global division) achieved 4% growth driven by Pedestrian and Perimeter Security.

· Asia Pacific declined by 4%, due to the weak sales in Greater China and Korea.

Operating income rose by 9% to SEK 6.68bn, above the market forecast of SEK 6.42bn. The operating margin rose from 16.2% to a 17.0%, albeit 50 basis points was driven by SEK 220m of one-offs including reversal of acquisition earn-outs, gains from divestments, and tariff refunds. Underlying operating leverage was 32%. EPS grew by 12% to SEK 3.98.

Operating cash flow rose by 16% to SEK 6.3bn, while cash conversion was 106%. The group’s financial position remains robust, with net debt to EBITDA of 2.2x. Looking forward, gearing is expected to fall rapidly thanks to strong free cash flow generation.

There was no dividend announcement today. For 2025, the company declared a payout of SEK 6.40, up 8.5%, equating to a yield of 2%.

M&A will continue to be a core driver of growth, with over 900 potential acquisition targets identified globally. The focus is on acquiring new customers in the core business, extending the core offering, accessing new technologies to deepen the group’s competitive position, and increasing service capacity. However, there is some concern that recent M&A has been skewed towards lower value-added segments (e.g. DIY, window and door hardware components, fencing products, gates, padlocks, cylinders, etc). Although these acquisitions fit the purpose of growing earnings at lower multiples than the group average, they also dilute the group’s exposure to the fast-growing and structurally more attractive electromechanical and mobile segments, potentially posing a risk to the long-term valuation multiple.

The 2023 purchase of HHI filled a strategic gap in the group’s US residential business. Although that market remains subdued, the business is performing well. Cost synergies have been achieved, though sales synergies have yet to be fully realised given market conditions. The group still expects HHI to be a 16% margin business (vs. <10% at present) as volumes recover. A strategic review of the non-core HHI plumbing business is being undertaken, which could potentially fetch $1bn. Elsewhere, M&A activity remained buoyant with 23 deals in 2025 and eight in the first half of 2026. The pipeline remains strong, and the group still plans to make its usual 15-20 acquisitions per year.

In May, long-time major stakeholder Investment AB Latour executed a SEK 2.5bn (0.7%) disposal of Assa Abloy stocks at around the current price (SEK 303). The institutional order book was reportedly multiple times oversubscribed, indicating that secondary market demand for the stock remains robust even as the primary holder divested to pare down its own corporate debt.

Assa Abloy doesn’t usually provide guidance but highlights that it remains confident in the company’s ability to navigate varying market conditions. On the call, the company said July is currently tracking June’s strong run-rate. The company is confident it can pass through any raw material cost increases through higher pricing – full-year price is still expected to be north of 2%. A continued focus on innovation, operational excellence, cost discipline, margin expansion, and strategic acquisitions, combined with a strong financial position, provides a solid foundation for continued profitable long-term growth and value creation.

The risk to this optimism is driven by a combination of rising interest rates, labour shortages, and tariffs. Management is dedicated to mitigating any impact from potentially negative changes in demand, through local agility and focus on cost-control. Assa has previously said that during both the global financial crisis in 2008/09 and the Covid-19 pandemic, its decentralised operational model and agile cost base provided flexibility. In addition, the group’s large exposure to after-market service and its structural pricing power leaves the business better positioned to navigate through uncertain times.

Structural tailwinds from the transition to electromechanical locks, increasing recurring and service revenue, data centre growth (collectively 60% of the business) and pricing should drive 5% organic growth.

Source: Bloomberg