Morning Note: Market News and an Update from Scottish Mortgage IT.

Market News

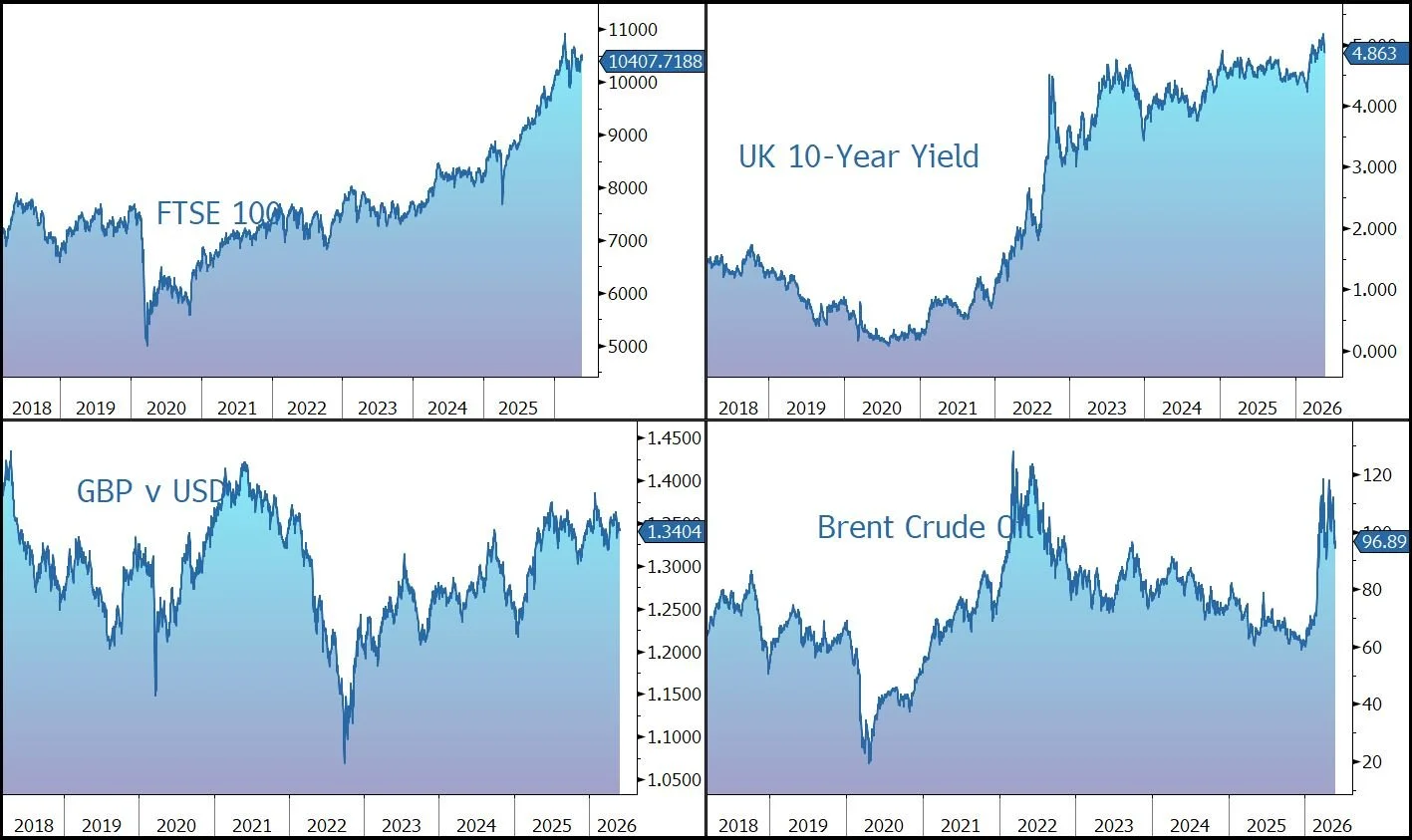

Brent Crude has climbed above $97 a barrel, rebounding from losses in the previous session as renewed hostilities between the US and Iran weakened expectations for a near-term peace agreement. US forces reportedly struck an Iranian military site believed to pose a threat to American troops and commercial shipping routes through Hormuz, while also intercepting Iranian drones. Meanwhile, Iran’s Revolutionary Guard said it had targeted a US airbase.

The dollar, the haven of choice during the conflict, gained, while the yield on the US 10-year Treasury ticked back up to 4.51%. Gold has fallen below $4,400 an ounce, hitting a two-month low, as inflationary and interest rate concerns remain in focus.

Lisa Cook, a member of the Federal Reserve Board of Governors, said inflation is headed in the wrong direction and she would be prepared to hike rates if that persists. Philip Jefferson said he expects prices to cool this year, though higher energy costs are keeping risks tilted to the upside. A key test comes later today with the release of the April PCE index, the Fed’s preferred inflation gauge. The forecast is 3.8%, a slight uptick from 3.5% in March.

US equities were little changed last night – S&P 500 (+0.02%); Nasdaq (+0.07%) – although the market is currently expected to open slightly lower this afternoon. Salesforce fell after the company gave a lukewarm revenue forecast. In Asia, equities declined: Nikkei 225 (-0.5%); Hang Seng (-1.3%).

The FTSE 100 is currently trading 0.8% lower at 10,408. Companies trading ex-dividend today include AB Foods (1.10%), Diploma (0.27%), Intertek (1.95%), Kingfisher (2.89%), National Grid (2.53%), and Severn Trent (2.43%). Sterling trades at $1.3410 and €1.1545, while the 10-year Gilt yields 4.87%.

The EU will broaden the use of import quotas and tariffs against China to shield its industrial sectors from the threat of Chinese imports, Stéphane Séjourné, vice president of the European Commission, told the FT.

Source: Bloomberg

Investment Fund News

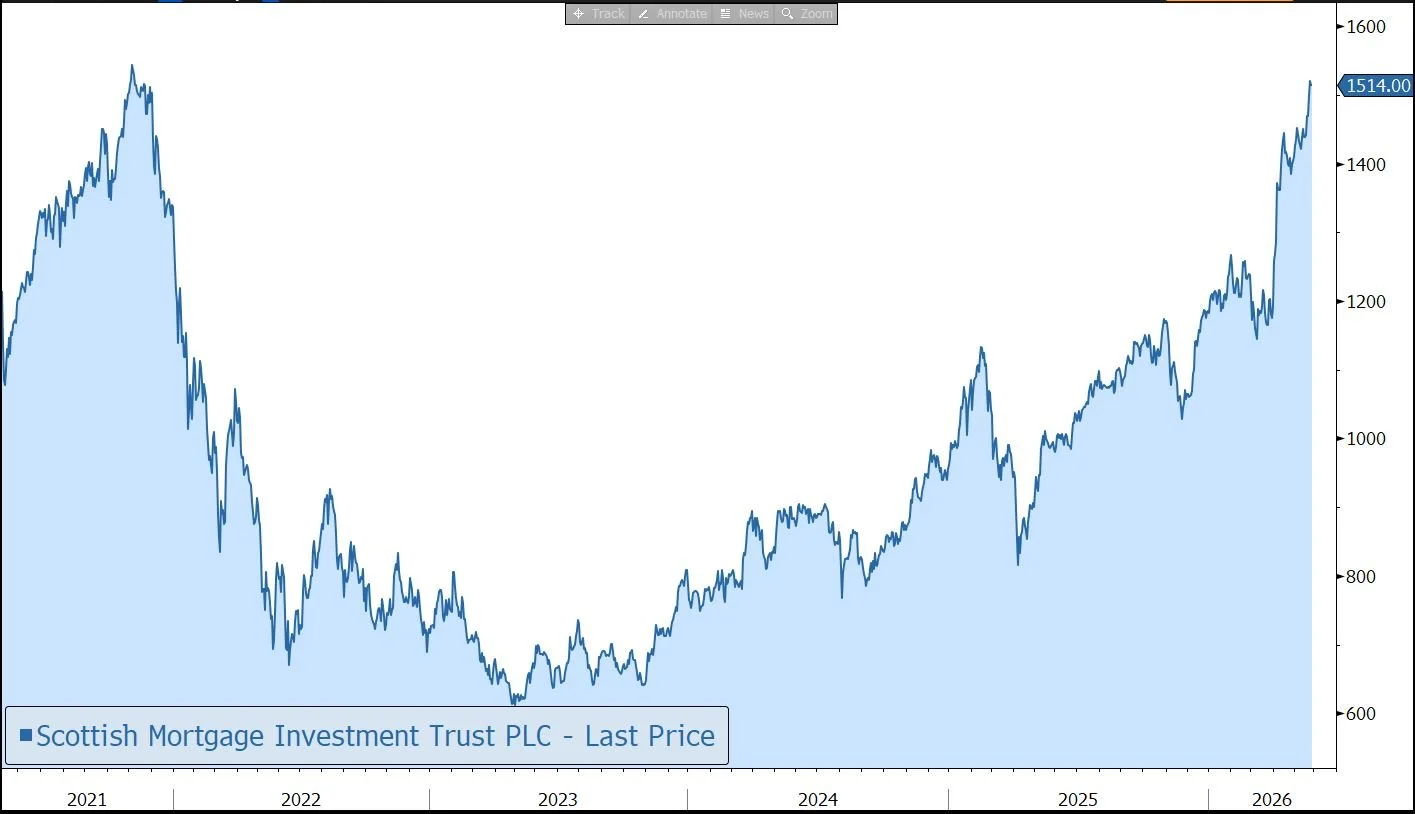

Scottish Mortgage Investment Trust is a £17bn global equity investment trust run by Tom Slater and Lawrence Burns, two highly regarded fund managers at Baillie Gifford. The fund has a strong long-term performance record compared to its benchmark to beat the FTSE All-World Index (in sterling terms) on a rolling 5-year basis. The Fund is actively managed, with an 88% deviation from the index, and an average holding period of more than five years. The manager believes that over long time periods, it is through supporting and holding just a small number of extraordinary companies that exceptional returns can be achieved. However, investing in such companies at the forefront of structural change means share price volatility is inevitable, for both the companies the fund owns and the trust itself.

Yesterday, the company released results for the financial year to 31 March 2026. During the period, the NAV rose by 27.4%, above the 18.0% increase for the benchmark index, while the share price was up 26.8%. The long-term performance track record remains impressive – over the last ten years, the NAV is up 435% (with the share price up 380%), versus 234% for the benchmark.

The Manager believes the investment landscape will be shaped by key themes of resilience, adaptability, and innovation. In a volatile world, resilience is a strategic advantage, allowing companies to adapt and emerge stronger. The Manager’s focus remains on identifying ‘outlier’ companies capable of delivering exceptional returns. The fund currently holds a small number of high conviction ideas – there are just over 100 holdings, although the top 30 account for 83% of assets.

Beneath the recent geopolitical turbulence and upheaval of the old-world order, the Manager believes a transformation of a fundamentally different kind is underway. The acceleration of artificial intelligence into a global infrastructure buildout is, in the Manager’s judgment, the most important structural change in the global economy since the emergence of the internet, and we are still in its early stages. The businesses at the infrastructure layer of the AI transition compounded through the geopolitical turbulence, largely unaffected by it. Those more exposed to cross-border commerce, consumer confidence, or the competitive pressures of a Chinese economy running on weak demand fared very differently. They paid the price for a world that shifted faster than their valuations had assumed.

SpaceX was by far the largest single contributor to returns during the year, adding a 14.9% absolute contribution. At the year end, it represented over 19% of the Company’s assets, a degree of concentration which is highly unusual, and represents a staggering near-20x return on investment. The Manager highlights that SpaceX should no longer be thought of as an aerospace contractor but as a dual monopoly: the world's dominant launch provider and a global connectivity utility with the potential for software-like margins. SpaceX is a private company, but in April it filed the documentation with regulators to go public, targeting a mid-June listing on the stock market. Continued strong operational execution has led to a significant upward revaluation during the year. As at 31 March 2026, the fund is holding SpaceX at a valuation of $1.25tn, with the position marked up during the first quarter as the manager saw the secondary market recalibrate and rebase to the merged valuation of SpaceX/xAI. The current carrying value sits below the $1.75tn figure reported in the press as the independent third-party provider S&P Global values private holdings based on verifiable transactions, not press speculation. The Manager also highlighted that Scottish Mortgage’s closed-ended structure means it faces no redemption pressures and will not be a forced seller of SpaceX at the point of listing, allowing the trust to hold the position securely through the post-IPO lock-up period and beyond. However, Baillie Gifford does not yet know what restrictions will apply to existing shareholders post-listing, how long any lock-up period will last, or whether Scottish Mortgage will be subject to the same terms as other pre-IPO investors.

The portfolio is global and so offers good geographic diversification. The high weighting to the US (c. 58%) brings exposure to the global centre of entrepreneurial excellence but also to a highly-rated stock market. The most difficult area of the portfolio this year was China, although the real issue was not tariffs. It was what happens when well-capitalised companies fight for market share in an economy where domestic consumption is barely growing. The Fund has maintained exposure to selected Chinese companies where compelling opportunities exist, notwithstanding a more challenging domestic economic backdrop and heightened competitive dynamics.

At the end of March 2026, the largest holdings in the Fund were: SpaceX (19.3%); TSMC (5.7%); ByteDance (4.7%); MercadoLibre (Latin American e-commerce platform, 4.0%); Stripe (3.9%). During the year, the Manager initiated a number of new positions: AppLovin (whose AI-driven advertising platform is scaling rapidly); MongoDB (the database infrastructure business that underpins an increasing share of AI-native application development); Figma (design tool for building websites, apps, and digital services), CATL (the world's largest battery maker, which supplies electric vehicle and energy storage companies), and Anthropic (a company at the heart of the transition from narrow AI tools to genuinely capable systems). These new positions were funded from reductions in Roblox, Meta Platforms, and PDD Holdings, and the complete sale of HeartFlow, Kinnevik and Wayfair.

The Manager believes the long-term risk taking, essential to economic and social progress, is continuing to migrate to private markets. At the end of March 2026, the fund had 41.6% of its assets in 53 unquoted investments, providing exposure to early-stage businesses that investors would not usually be able to gain access to. SpaceX is clearly a key example. Although this increases the level of volatility in the Fund, the Manager believes these investments provide the potential for asymmetric returns, with a maximum 100% loss set against the potential for unlimited upside. The Fund’s private company exposure tends to be weighted to the upper end of the maturity curve, focussed on late-stage private companies which are scaling up and becoming profitable.

The Company recently updated its investment policy to provide the Managers with limited additional flexibility to invest in private companies when the portfolio is above the Fund’s 30% limit, through an additional capacity of up to £250m. This ensures the company is not forced to forgo attractive new or follow-on investment opportunities in exceptional private businesses, while maintaining robust guardrails and oversight.

Scottish Mortgage is in a robust financial position. The Fund continues to deploy a ‘strategically appropriate’ level of gearing in the portfolio as the Board believes this offers a potential source of additional value for shareholders over time. However, during the year, the level of gearing naturally reduced to 11% of NAV, reflecting the growth in the portfolio rather than a reduction in absolute borrowing. The Company undertook a number of refinancing actions, maintaining a diversified and flexible debt structure. The overall cost of debt remains low at 3.6%, well below the 10-year Gilt yield.

Although the focus of the Fund is capital growth, the company has committed to paying a small dividend – with these results, a full-year payout of 4.57p has been declared, up 4.3% on last year. The yield is currently 0.3%.

The size of the Fund helps to keep costs low, with an ongoing charge of 0.33% for the year and no performance fees. This is much less than most actively managed funds invested in public equities and significantly less than private equity funds.

Having traded at or around NAV for years, since 2022 the shares have traded at a discount, which widened to around 20% in 2023. In response, the Company has been buying back its shares – more than £3bn since the beginning of 2024 – and as a result the discount to NAV narrowed substantially, although it remained sizeable (9.5%) at the year end. However, more recently, the shares have moved to a premium (currently 8%), driven by the potential upward movement in the perceived value of SpaceX ahead of its IPO. In response, Scottish Mortgage has been issuing shares at a premium since the year end.

Given its growth/technology bias, this equity fund is at risk from falling stock markets, particularly if highly-rated stocks fall out of favour or their valuations are questioned. The use of gearing, combined with investment in private companies, and the concentrated nature of the portfolio also leads to significantly greater volatility compared to the peer group. We note that the 5-year performance track record – 12.8% NAV growth versus 68.2% for the index – still feels the drag of the brutal 2022 growth-stock crash, while during the downturn in 2008/09, both the NAV and the share price fell by around 40%.

Source: Bloomberg