Morning Note: Market News and an Update from Newmont Corp.

Market News

US equities slipped last night – S&P 500 (-0.3%); Nasdaq (-0.3%). Walmart was little changed following the release of results that included a cautious outlook, while Deere & Co surged by 11% following strong earnings and a raised its full-year profit outlook. Johnson & Johnson is said to be preparing a potential sale of DePuy Synthes at a possible valuation of over $20bn.

In Asia this morning equities also fell: Nikkei 225 (-1.1%). The yen dipped after Japan’s core CPI rose at the smallest gain in two years. The data bolsters the case for a cautious Bank of Japan, according to Bloomberg Economics.

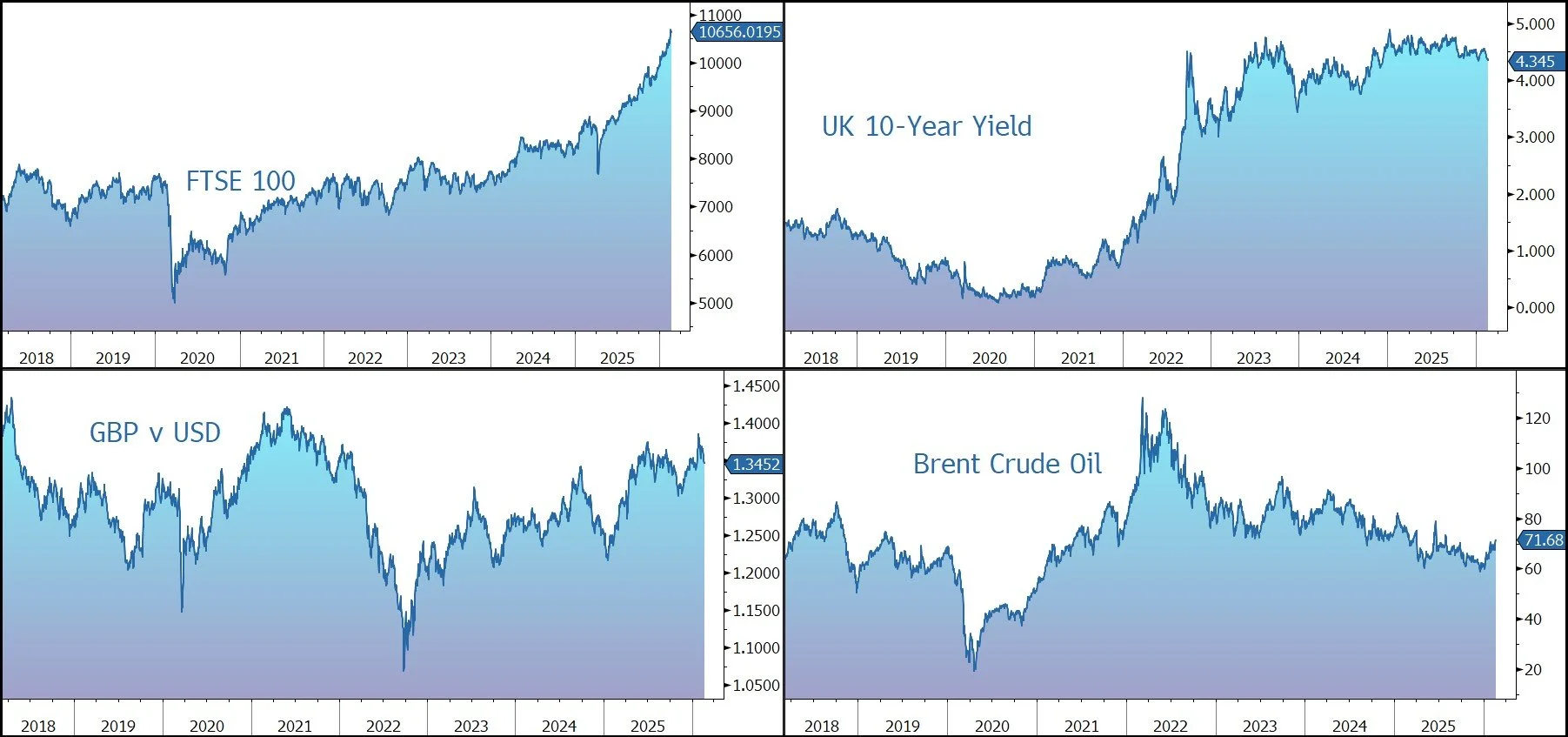

The FTSE 100 is currently 0.3% higher at 10,656. Britain recorded a budget surplus of £30.4bn in January, its biggest ever, as tax revenue surged. Retail sales started the year with the fastest growth in 20 months. Sterling trades at $1.3450 and €1.1435.

The Fed’s Stephen Miran dialed back his calls for how deeply rates should be cut in an interview with a Substack blog. The 10-year Treasury yield ticked up to 4.07%, while gold moved back above $5,000 an ounce. Goldman says central banks remain eager to buy gold, despite a dip in December purchases due to market volatility.

Brent Crude trades at $71 a barrel, the highest since August after Donald Trump gave Iran 15 days at most to make a deal over its nuclear program. The president is weighing a limited early strike to drive Tehran to the negotiating table, the WSJ reported.

Europe’s five biggest military spenders are set to jointly develop low-cost air defence weapons based on lessons from Ukraine. The initiative is expected to be announced as early as today.

Source: Bloomberg

Company News

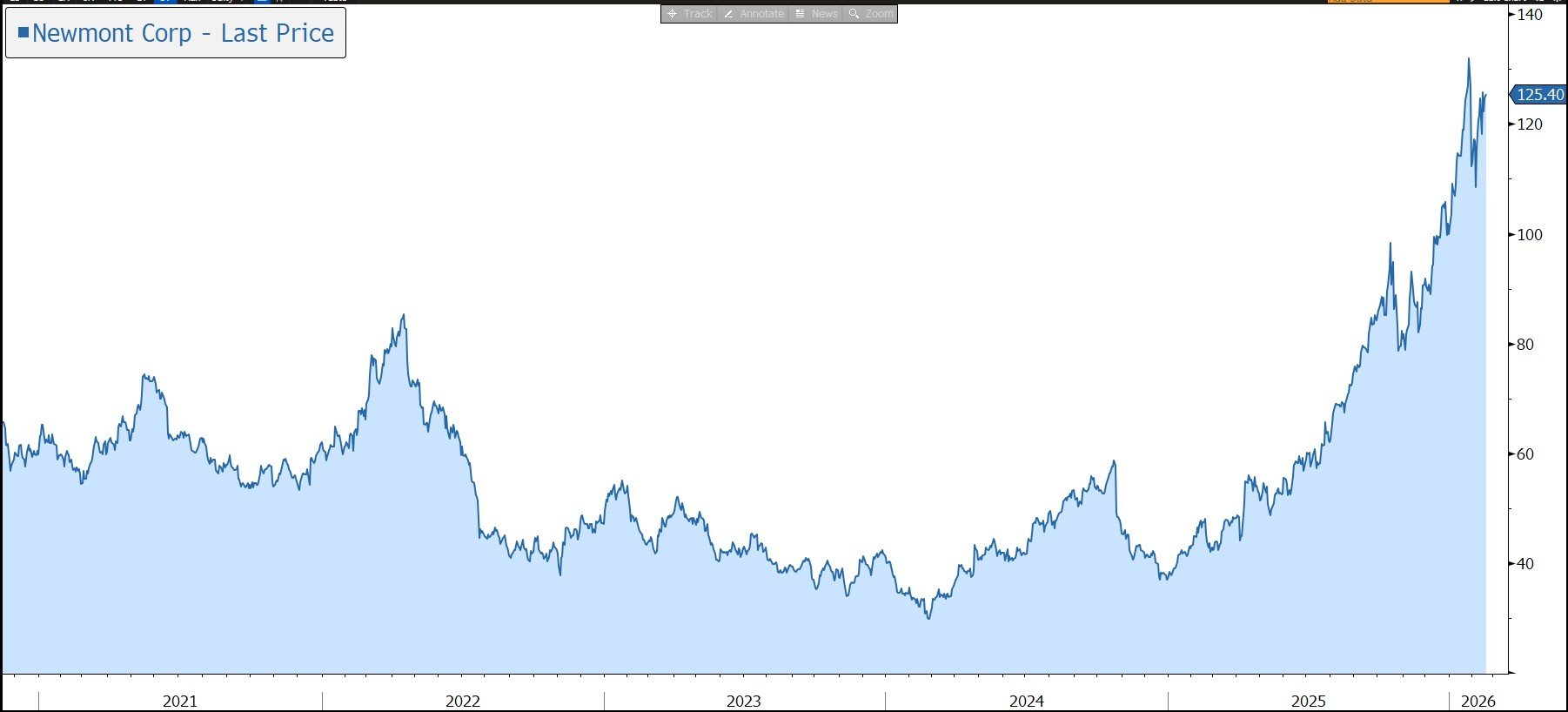

Yesterday lunchtime Newmont Corp. released full-year 2025 results which came in above market expectations driven by the strong gold price and good cost control. Despite a decline in production, the business delivered a record $7.3bn in free cash flow and continued to return capital to shareholders. The company also provided 2026 guidance – seen a trough year – and announced an enhanced capital allocation framework. Production is expected to dip again in 2026, while costs are projected to rise. In response, the shares fell by 3%.

Newmont is the world’s largest gold company and a producer of copper, silver, zinc and lead. This follows a transformational period during which the company bought US-listed Goldcorp for $10bn and Australia’s Newcrest Mining for $17bn. The company also entered into the Nevada Gold Mines joint venture with Barrick Gold – its 38.5% stake provides exposure to the single largest gold-mining complex in the world. In order to retain focus, Newmont has also divested of non-core assets – in 2025 the company completed its portfolio optimisation programme which has generated $4.5bn of after-tax proceeds to date.

Newmont now operates a world-class portfolio of assets and prospects in favourable mining jurisdictions in Africa, Australia, Latin America & Caribbean, North America, and Papua New Guinea. The portfolio includes more than half of the world’s Tier 1 mines.

At the end of 2025, the company declared total reserves of 118.2m attributable gold ounces and resources of 148.7m attributable gold ounces. There is also significant upside from other metals, including more than 12.5m tonnes of copper reserves and 442m ounces of silver reserves.

The company says that every $100 an ounce change in the gold price adds just over $500m to the group’s revenue. With the current gold price ($5,000+ an ounce) well above the company’s conservative price assumption ($2,500 an ounce) and the expected cost of sales ($1,680 an ounce), Newmont should be able to generate significant cash flow over the medium term. As a result, the company provides an attractive way to gain exposure to the gold price, albeit with the operational and political risks that come with a production company.

The company’s enhanced capital allocation framework is designed to be sustainable through the commodity cycle while maximising total return of capital to shareholders, maintaining a flexible and resilient balance sheet, and focusing on high-return capital investments for long-term value creation. In order of priority, the company will:

· Undertake ongoing sustaining capital investment in its world-class portfolio

· Pay a sustainable through the cycle cash dividend

· Maintain a disciplined approach to development capital reinvestment

· Maintain an optimized capital structure through the cycle, anchored by a $1bn net cash target, with flexibility of plus or minus $2bn depending on market conditions. A minimum cash balance of $5bn will be maintained.

· Once the above priorities are complete, Newmont intends to deploy excess cash on share repurchases.

In 2025, attributable gold production fell by 14% to 5.9m ounces. The group also produced 135k tonnes of copper and 28m ounces of silver. Excluding the non-core assets held for sale, gold production was 5.7m ounces from the core Tier 1 portfolio, slightly above the company’s guidance.

The gold price has rallied sharply so far this year, driven by global geopolitical and macro-economic uncertainty, exacerbated by the Trump administration, continued central bank bullion buying, and concern over fiat currency debasement. During the year, Newmont realised a gold price of $3,498 per ounce, up 45%.

The group’s direct operating costs are made up of labour (50%), materials & consumables (30%), fuel & energy (15%), and other expenses (5%).

During 2025, total all-in sustaining costs (AISC) fell by 4% to $1,358/ounce (and below the 2025 target of $1,620) due to significant cost cutting. In addition, the surge in silver and copper prices acted as a massive discount on their gold production costs. As a result, cash profits (EBITDA) increased by 55% to $13.5bn, while adjusted net EPS rose from by 98% to $6.89. Q4 EPS was up % to $2.52, well above the market forecast of $1.94.

Capital investment fell 11% to $3.0bn, in line with guidance, although the company continued to progress major capital projects. The business generated a record free cash flow up 150% to $7.3bn. This left the group in a strong net cash position of $2.1bn, with $7.6bn of cash and $11.6bn in total liquidity.

During 2025 the company returned $3.4bn to shareholders during the year, including the repurchase of $2.3bn of its shares as part of its $6.0bn programme authorised by the Board through to October 2026. It also declared an annual dividend of $1.04 per share, or a yield of 1%.

Newmont released guidance for 2026. The group expects attributable gold production of 5.3m ounces, including over 3.9m gold ounces from its managed operations. Gold by-product All-in sustaining costs (AISC) are expected to be $1,680 an ounce, benefitting from profitable production of other metals. Sustaining capital expenditure (i.e. maintenance) is expected to be $1.95bn, with development spend of $1.4bn.

Source: Bloomberg