Morning Note: Market News and an update from Croda.

Market News

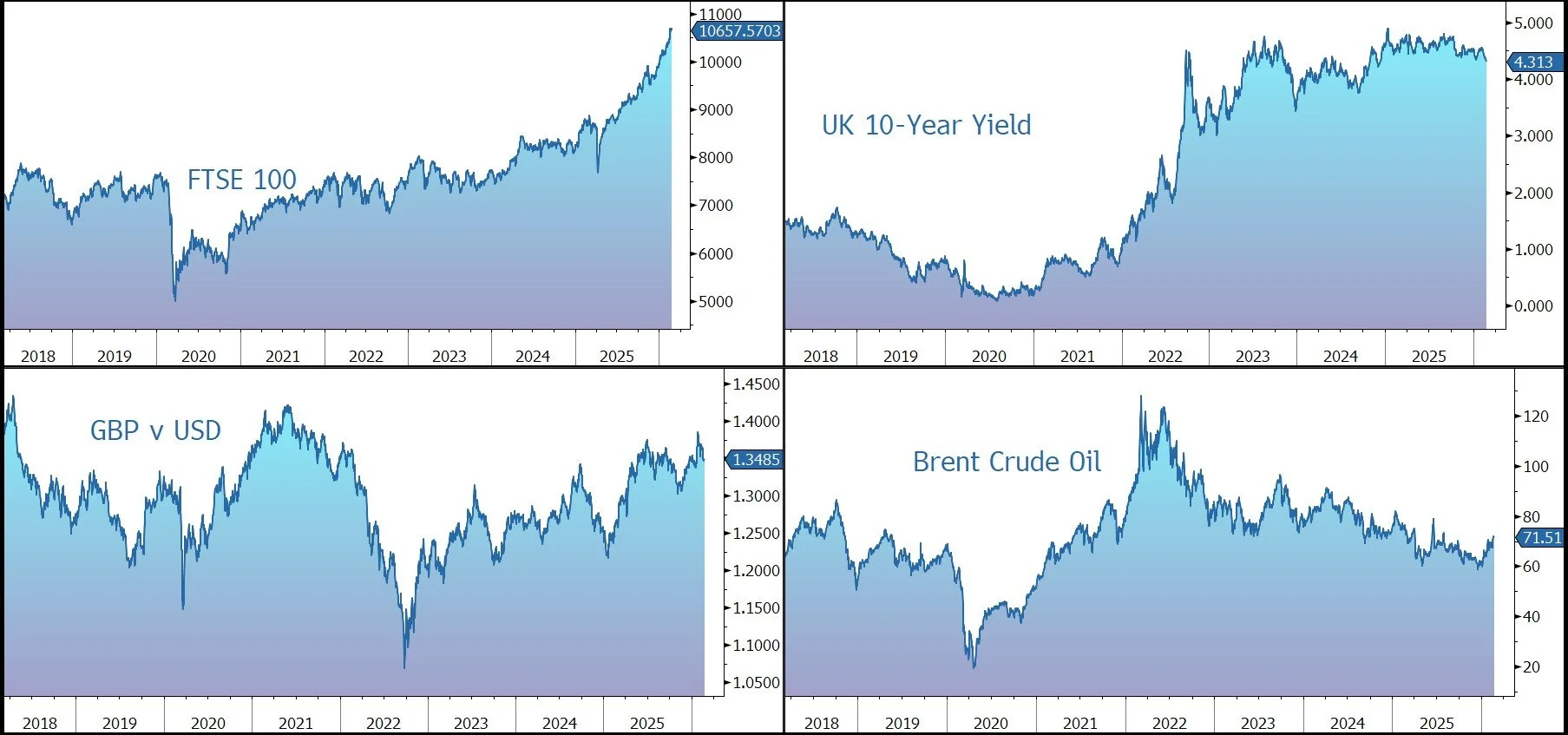

Donald Trump’s new 10% global tariffs went into effect. An EU assessment found his latest levy policy would push duties on some EU exports above levels allowed under their trade agreement. Trump’s preparing new national security investigations that could pave the way for additional tariffs. The uncertainty pushed the 10-year US Treasury yield down to 4.05%. Gold has run into some profit taking this morning following yesterday's surge. It currently trades at $5,175 an ounce.

US equities fell last night on AI fears – S&P 500 (-1.0%); Nasdaq (-1.1%). IBM fell 13%, its worst day since 2000, after Nassim Taleb warned of software bankruptcies and Citrini issued a bearish report. Governments should tax AI to cushion the impact of sweeping job losses, Alap Shah, co-author of the Citrini report, told Bloomberg TV.

In Asia this morning, shares mostly bucked a US sell-off: Nikkei 225 (+0.9%); Hang Seng (-1.8%); Shanghai Composite (+0.9%). Indian IT Stocks followed US Tech lower after the Citrini AI Scare.

The yen weakened after the Mainichi reported that PM Sanae Takaichi voiced apprehension over any further rate hikes in a meeting with Kazuo Ueda last week. China added 20 Japanese firms to an export ban list in an escalation of bilateral tensions.

The FTSE 100 is currently 0.2% lower at 10,658. Standard Chartered is little changed after the bank missed earnings and announced a $1.5bn share buyback. Sterling trades at $1.3475 and €1.1440.

Brent Crude rose toward $72 a barrel on Tuesday, its highest level in nearly seven months, as investors closely monitor a new round of talks between the US and Iran. President Trump said on Monday that he would prefer reaching an agreement with Iran, with talks set to resume on Thursday, but warned of a “very bad day” for Tehran if a nuclear deal fails to materialise.

Source: Bloomberg

Company News

Croda International has released 2025 results which were ahead of market expectations, helped by growth in its consumer care and life sciences divisions. The company has nudged up its dividend and set out a new three-year financial framework. In response, the shares have been marked up by 5% in early trading.

Croda generates annual sales of £1.7bn from high performance ingredients and technologies. Its products are found in pharmaceuticals, sun protection creams, and agricultural products. The company’s portfolio is positioned to align with emerging megatrends such as the move to sustainable ingredients and the increased use of biologics.

However, over the last few years, Croda’s performance has been impacted by a number of factors which has driven the share price down from over £100 to around £30:

· Fall-off of Covid-19 benefits: sales of high-margin lipids used in mRNA vaccines vanished as the pandemic receded, creating a massive earnings hole.

Destocking: During the supply chain crisis, customers over-ordered. As things stabilised, they aggressively slashed inventories, causing Croda’s volumes to fall

Weak demand in agriculture (Crop Protection) and Industrial Specialties further pressured margins.

Under-utilised factories and a shift toward lower-margin products (like Fragrances) impacted profitability.

The company launched a transformation programme to enhance growth and efficiency. In 2025, the group realised £28m of gross benefits, versus a target of £25m, on the way to a 2028 target of £100m. 89% of sales are now to consumer, pharma, and agriculture markets compared with 73% in 2019.

In 2025 group sales rose by 6.6% at constant currency (cc) to £1.7bn, benefitting from a 9.6% increase in volume, offset by a 3.0% price decline. In the final quarter sales rose by 5%.

The company operates across three divisions. In the Consumer Care business, sales rose by 8% in cc terms to £973m. Fragrances and Flavours (+15%) continues to outperform peers, and growth in Beauty (+4%) was supported by more robust consumer sentiment in North America in the second half year.

In Life Sciences, sales rose by 8% in cc terms to £532m. Crop Protection (+14%) benefited from a recovery in demand from larger customers following an extended period of destocking, and Pharma (+4%) delivered its strongest performance of the year in the final quarter despite the US regulatory environment continuing to create uncertainty for our customers.

Industrial Specialties sales fell by 2% in cc terms to £195m.

The group’s operating margin rose by 20 basis points to 17.4%. Although margins are still significantly below their medium-term potential, they improved in both key businesses, Consumer Care and Life Sciences. Profit before tax rose by 6% to £276m, ahead of the £268m market expectation.

Free cash flow fell by 5% to £162m, with an improvement in the second half helped by lower working capital and capital expenditure. The balance sheet is robust – net debt fell slightly to £524m, leaving financial gearing at only 1.3x net debt to EBITDA. The full-year dividend was raised by 0.9% to 111p.

Based on current market conditions, the company has set out a new three-year financial framework which involves:

· consistent sales growth: 3%-6% organic sales growth CAGR 2026-28

· enhanced profitability: adjusted operating margin >20% (vs 17.4% in 2025) for full year 2028

· growing cashflows: free cash flow-to-sales ratio >12% (vs. 9.5% in 2025) for full year 2028

· improving Return on Invested Capital: >10% (vs. 8.2% in 2025) for full year 2028.

For this year, the company is guiding to organic sales growth of 3%-6%, a further increase in adjusted operating margin, and adjusted operating profit in line with current market expectations (£320m).

Source: Bloomberg