Morning Note: Market News and an Update from AstraZeneca.

Market News

In a national address, President Trump declared the core strategic objectives in Iran were “nearing completion” after 32 days of Operation Epic Fury. The President gave no clear exit timeline but said the US is nearing “finishing the job” and revived threats to strike Iranian power plants. Trump claimed Iran sought a ceasefire and that talks were “going very well”. Tehran’s foreign ministry called the assertion “false and baseless.

China and Pakistan issued a five-point initiative calling for an immediate ceasefire, swift peace talks, and restoration of normal navigation through the Strait of Hormuz. Chinese Foreign Minister Wang Yi stated: “China is willing to work with Pakistan to overcome difficulties, remove obstacles, bring the fighting to an end as soon as possible… and open the window for peace talks.” Pakistan has offered to host US-Iran discussions.

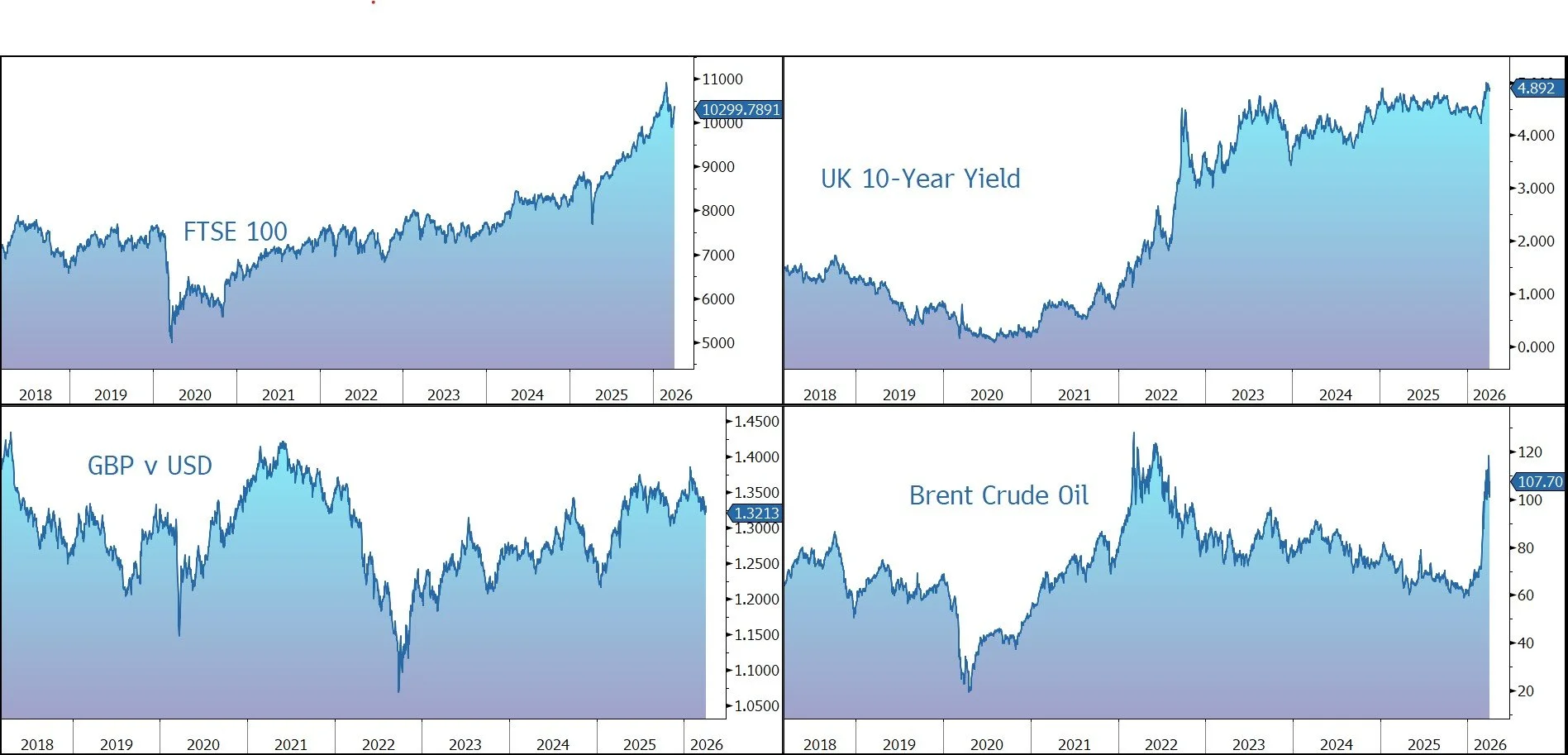

Having fallen below $100 a barrel in the previous session, Brent Crude has risen back up to $107, while other asset classes have sold off. The yield on the US 10-year Treasury moved up to 4.38%, while the gold price is down 2.5% at $4,640 an ounce.

US equities made gains last night – S&P 500 (+0.7%); Nasdaq (+1.2%) – but have sold off since Trump’s speech. The futures market is currently signalling a 1% decline at the open this afternoon. In Asia, equities also declined: Nikkei 225 (-2.4%); Hang Seng (-1.2%); Shanghai Composite (-0.8%). China’s central bank withdrew cash from its financial system in March for the first time in a year, amid signs of an economic rebound.

The FTSE 100 is currently 0.5% lower at 10,300, while Sterling trades at $1.3210 and €1.1460. The conflict in the Middle East will push up the cost of energy for producers and disrupt supply chains, the Food and Drink Federation has warned. JPMorgan economist Allan Monks scaled back his forecast to one Bank of England rate hike this year — in June — after Andrew Bailey signaled a more cautious stance.

Source: Bloomberg

Company Update

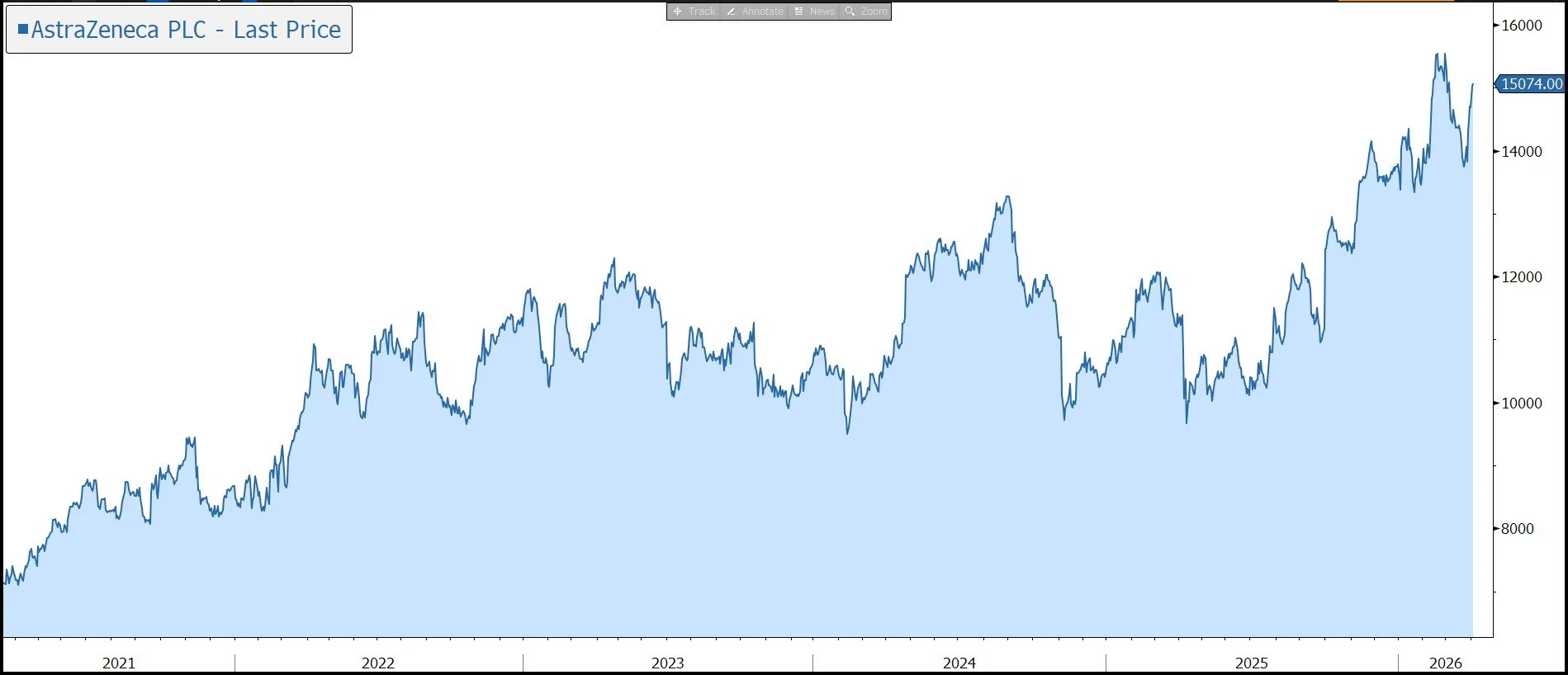

Over the last couple of weeks AstraZeneca has announced a stream of mainly positive news from its R&D pipeline. Combined with robust performance from the existing pharmaceutical portfolio, this provides a strong platform to achieve both its 2030 revenue target and sustainable growth beyond.

AstraZeneca (AZ) is a global, science-led biopharmaceutical company. The main growth driver has been the group’s key Oncology franchises (including Tagrisso, Lynparza, Enhertu, Imfinzi, and Calquence), which have been supplemented by the other growth platforms of Respiratory & Immunology (R&I), Cardiovascular, Renal, & Metabolic diseases (CVRM), Vaccines & Immune Therapies (V&I), and rare diseases (via the $41bn acquisition of Alexion).

The group’s (tough) ambition is to deliver $80bn of revenue by 2030, up 8.3% p.a. from a 2023 base of $45.8bn. This will be driven by growth across its existing portfolio through geographic expansion and follow-on indications, as well as new products currently in late-stage development, offset by the loss of patent exclusivity in some existing products. The group expects to launch 20 new medicines before the end of the decade, with some products having the potential to generate more than $5bn in peak-year revenue.

Beyond 2030, the company will seek to drive sustainable growth by continuing to invest in transformative new technologies and platforms that will shape the future of medicine. Management’s confidence is driven by the large number of readouts in 2027-29 for assets that are likely to reach peak sales beyond 2030, including camizestrant (breast cancer), rilvegostomig (oncology) and the haematology portfolio.

The aim is to generate a mid-30s core operating margin by 2026, versus 32% in 2023. Beyond 2026, the margin will be influenced by portfolio evolution and the company will target at least the mid-30s percentage range.

AZ currently invests more than 20% of sales in R&D and uses partnerships to gain access to innovative technology. The group has an attractive pipeline of potential new products, the success or failure of which will drive future profitability and the share price.

Recent news flow on the pipeline has mainly been positive – in 2025 the company delivered 16 positive Phase III study read-outs and 43 approvals in major regions. The company now has 16 blockbuster medicines (i.e. sales above $1bn). The momentum across the company is expected to continue in 2026, with results of more than 20 Phase 3 trial readouts and more than 100 Phase 3 studies ongoing.

In particular, we would highlight the following recent announcements:

- Tozorakimab (27 March) – the group’s first-in-class monoclonal antibody met primary endpoints in two Phase III trials (OBERON and TITANIA). The drug significantly reduced moderate-to-severe exacerbations in patients with Chronic Obstructive Pulmonary Disease (COPD). Unlike current treatments, Tozorakimab targets the IL-33 pathway to reduce both inflammation and mucus dysfunction, potentially shifting how the world’s third-leading cause of death is treated.

- Imfinzi (March 16) - received EU approval as the first and only perioperative immunotherapy for early-stage gastric and gastroesophageal cancers.

- Imfinzi (2 April) - positive high-level (interim) results for a ‘quadruple’ combination therapy for patients with unresectable hepatocellular carcinoma (HCC) who are eligible for embolization (TACE). Imfinzi plus Imjudo combined with Lenvatinib and TACE demonstrated a statistically significant and clinically meaningful improvement in progression-free survival in the EMERALD-3 Phase III trial.

- Efzimfotase alfa (31 March) - the company saw mixed but generally positive results for Efzimfotase alfa in treating hypophosphatasia (HPP), a rare genetic bone disease. The Mulberry and Chestnut trials showed significant improvements in bone health and safety for children. While the Hickory trial in adults missed its primary endpoint (due to a high placebo effect), AZ reported clinically meaningful benefits in specific sub-groups and plans to proceed with regulatory filings anyway.

Looking forward, the company is due to release key data from two pipeline assets: Baxdrostat (for the treatment of resistant hypertension) and Elecoglipron (an oral GLP-1 agonist for the weight-loss market).

As a reminder, AZ has a robust balance sheet and generates strong free cash flow. In 2025, net debt slipped from $24.6bn to $23.4bn, around 1.2x net debt to EBITDA. The company’s capital allocation priorities include investing in the business and the pipeline. To that end, the company increased capital expenditure by 47% in 2025, driven by manufacturing expansion projects and investment in IT systems, to support portfolio growth and build capacity for transformative technologies.

M&A remains central to the strategy. Earlier in the year, the company struck a deal worth up to $18.5bn to license drugs from China’s CSPC Pharmaceutical, including exclusive global rights outside of China to CSPC’s once-monthly injectable weight management portfolio.

AZ is also committed to a progressive dividend policy and intends to maintain or grow the payout each year. In 2025, the company raised its payout by 3% to $3.20, equating to a yield of 3%. In 2026, the company intends to increase the annual dividend to $3.30.

Political headwinds have eased somewhat, and the company struck a deal with the US administration. In return for a three-year exemption from pharmaceutical tariffs, AZ agreed to implement price-lowering measures in certain channels in the US and announced a huge $50bn investment in the US for medicines manufacturing and R&D. This includes the massive new Virginia manufacturing site (which broke ground in October 2025) focused on the company’s weight-loss and metabolic portfolio.

AstraZeneca has harmonised its share structure and now has a direct listing on the New York Stock Exchange in place of its US ADRs. This will increase the liquidity of the shares and makes the stock much more attractive to US institutional funds – it invites direct comparison with Merck or Eli Lilly, which typically trade at higher P/E multiples than European-listed peers. The company remains listed, headquartered, and tax resident in the UK.

Looking ahead to 2026, the company is guiding to total revenue growth in the mid to high single-digits (slightly better than expected) and Core EPS growth in the low double-digits, both at CER.

We believe the outlook for the pharmaceutical sector remains mixed despite the backdrop of an ageing population. Although the business provides some protection against macroeconomic uncertainty and R&D productivity is expected to increase with the help of AI, concerns over drug pricing are likely to remain a headwind, especially at a time when governments are looking for ways to reduce debt levels. However, with a pipeline of innovative products targeting unmet patient needs, that can justify higher pricing, AZ is well placed to generate above average revenue and earnings growth. This has been reflected in the strong long-term performance of the shares.

Source: Bloomberg