Morning Note: Market News and an Update from Unilever and Nike.

Market News

President Trump told reporters the war “could end in two to three weeks,” adding that Tehran “does not have to make a deal” for Washington to conclude operations. The White House said the President will address the nation at 9pm Eastern Time.

Iran has “the necessary will to end this war,” but expects certain requirements to be met “especially the essential guarantees to prevent the recurrence of aggression,” the Islamic Republic’s President Masoud Pezeshkian told the President of the EU Council António Costa in a call Tuesday. The UAE is lobbying for a military coalition to reopen the Strait of Hormuz by force, the WSJ reported. In the meantime, Hormuz vessel flows are ticking gently higher even as the strait remains effectively closed to most commercial shipping without clearance from Iran.

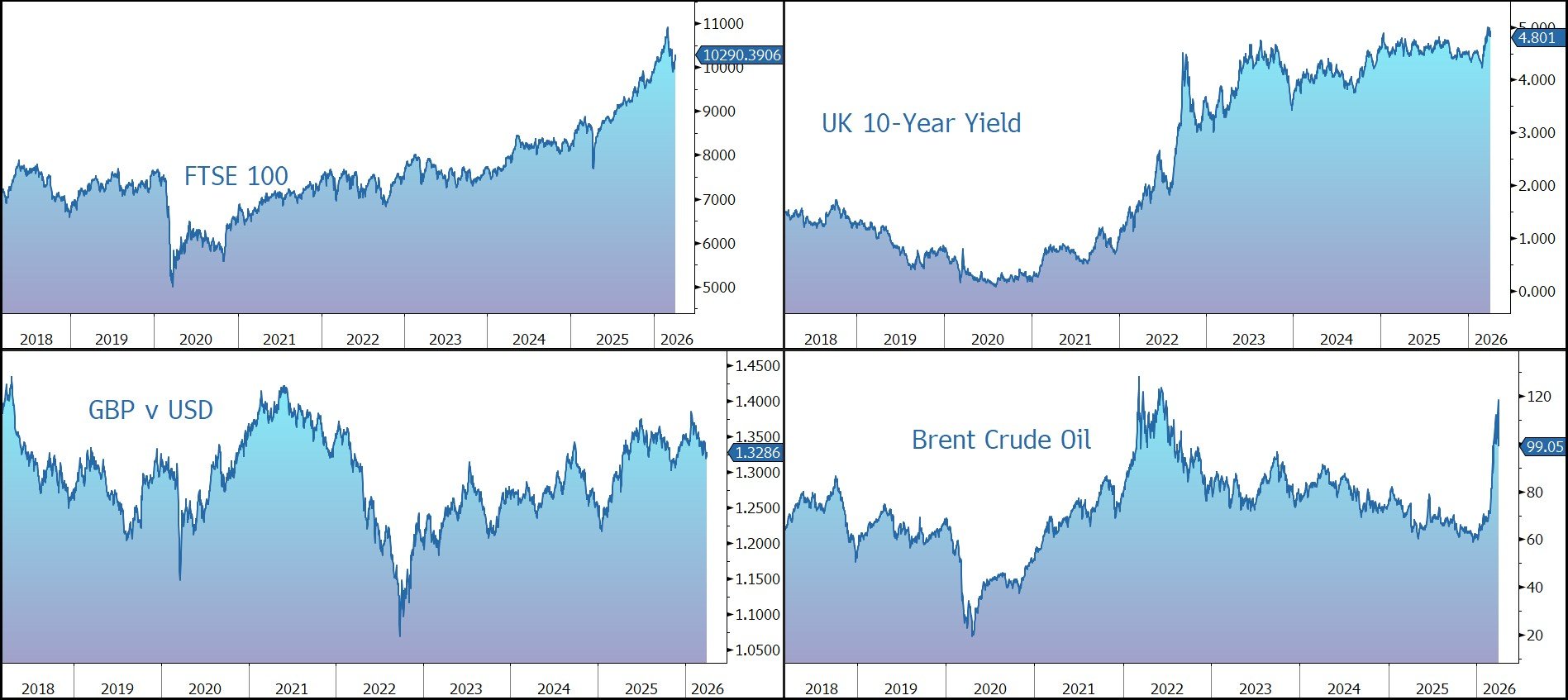

Brent Crude fell back below $100 a barrel. The dollar edged lower and the yield on the US 10-year Treasury has fallen back to 4.27% as optimism grows that a resolution would ease crude oil flows and support economic growth. Gold continued its recent recovery and currently trades at $4,720 an ounce.

Equity markets have bounced. Last night in the US, the main indices moved higher – S&P 500 (+2.9%); Nasdaq (+3.8%) – and continued to rally after the market close. Asian stocks jumped the most in a year and bonds extended gains: Nikkei 225 (+5.2%); Hang Seng (+2.3%); Shanghai Composite (+1.5%).

The FTSE 100 is currently up 1% at 10,290, while Sterling trades at $1.3280 and €1.1456. Gilts are strong, with the yield on the 10-year falling to 4.74%.

OpenAI raised $122bn at an $852bn valuation, its largest funding round yet, with most of the capital coming from Amazon, Nvidia, and SoftBank.

Source: Bloomberg

Company News

Yesterday afternoon, Unilever announced an agreement to combine its food business with food company McCormick & Co. Although the deal was struck at a reasonable valuation and creates a strong company with a complementary portfolio of brands, the structure of the transaction was unwieldy. In particular, the impact of stranded costs on the margin and the loss of a stable cash generative business. Furthermore, Unilever shareholders will be left with a direct 55% stake in a new US-listed company which they may not be allowed or want to hold, creating a potential overhang for the shares. In response, the shares fell by 7%.

Unilever is one of the world’s leading suppliers of consumer goods, with annual sales of more than €50bn. Its products are low-ticket, repeatable purchases, with 3.4bn people using a Unilever brand every day. With unique routes to market, the company has an unrivalled emerging market presence and generates more than half of its sales from those parts of the world expected to experience strong long-term growth in demand. In particular, the group’s 62% holding in India-listed Hindustan Unilever Limited provides exposure to the largest consumer goods company in India.

Following last year’s demerger of its Ice Cream unit Magnum, in which it has retained a 19.9% stake, Unilever is focused on four fairly equally-weighted Business Groups: Beauty & Wellbeing (25% of 2025 sales), Personal Care (26%), Home Care (23%), and Foods (26%).

As part of its ongoing simplification strategy, yesterday afternoon Unilever announced the combination of its Foods division with McCormick to create a global flavour powerhouse. The combined business will house leading, iconic brands including McCormick, Knorr and Hellmann’s, and high growth potential brands including Cholula, Maille, and Frank’s, as part of a global portfolio with revenue of $20bn.

Given the size difference between the two businesses, the transaction is expected to be structured as a tax-efficient Reverse Morris Trust transaction and is intended to be tax-free for US federal income tax purposes to Unilever and its shareholders, thereby mitigating some of the overall transaction-related tax costs.

Unilever and Unilever shareholders will receive:

- a proportionate mix of McCormick’s existing voting and non-voting common stock, equating to 65.0% of the fully diluted combined company equity, equivalent to $29.1bn based on the last 1-month volume-weighted average McCormick share price of $57.84. Unilever shareholders will directly own 55.1% of the combined company equity. Unilever will own a 9.9% stake as an investment on the balance sheet, which over time, and not earlier than one year after closing, it intends to sell down in an orderly and considered manner. McCormick shareholders will own 35.0%.

- $15.7bn in cash, subject to certain closing adjustments, that will offset one-off separation and tax costs, pay down debt to its current level of c.2.0x net debt/EBITDA following closing, and support a €6bn of share buyback programme expected to run between 2026 and 2029.

The transaction reflects an enterprise value of $44.8bn for Unilever Foods, equivalent to an EV/Sales ratio of 3.6x and a 13.8x EV/EBITDA multiple based on the last 1-month volume-weighted average McCormick share price of $57.84 which is in line with the current trading multiple for Unilever, and in line with the most attractive foods company valuations.

The combined company will have a distinctive, attractive profile within the industry, with leading positions in growth categories and a quality financial model of superior growth, supported by strong gross margins. Combined pro-forma sales are $20bn, with a growth target of 3%-5%, and an operating margin of 21%, with potential to expand to 23%-25%.

The combined company expects to realise approximately $600m of annual run-rate cost synergies (driven by procurement, manufacturing, and SG&A) net of growth reinvestments, with full value expected to be achieved by the end of year three. Incremental cost and revenue synergies of $100m will be reinvested to further drive growth.

McCormick intends to fund the cash component of the purchase price through a combination of cash from its balance sheet and proceeds from new debt issuance. Upon closing, the combined food company’s net leverage is expected to be an elevated 4.0x or less, although it is expected to maintain an investment grade credit rating and return to 3.0x net within two years.

The combined company will be led by the McCormick CEO and CFO, with senior management representation from Unilever Foods.

McCormick will retain its existing name, global headquarters, and NYSE listing. The company will establish international headquarters in the Netherlands and is planning a secondary listing in Europe.

Completion is expected by mid-2027, subject to McCormick shareholder approval and the receipt of required regulatory and other approvals. The main antitrust scrutiny is likely to revolve around the impact on consumer pricing.

The deal does not include the Indian Foods business which has a different make-up of local brands. This makes the ‘New McCormick’ less attractive to some growth investors who wanted exposure to the Indian middle class. However, since Hindustan Unilever (HUL), in which Unilever holds a majority 62% stake, trades at a much higher multiple than the rest of the group, keeping it within Unilever actually helps protect Unilever's remaining valuation multiple.

Following the separation of its Foods division, Unilever will become a leading pure-play Health and Personal Care (HPC) business spanning Beauty, Wellbeing, Personal Care, and Home Care. Resources will be focused towards categories with strong structural growth and the highest returns. 25 Power Brands account for 78% of revenue. The pro-forma portfolio generated revenue of €39bn in 2025 and delivered a compound annual growth rate of 5.4% underlying sales growth in the last three years, alongside a gross margin of 48% and an underlying operating margin of 19%.

Unilever has reaffirmed its commitment to and confidence in delivering on its medium-term value creation algorithm, with mid-single digit underlying sales growth, underpinned by at least 2% underlying volume growth and continued modest improvement in operating margin. The company’s capital allocation framework remains unchanged, prioritising disciplined investment behind organic growth and productivity, and allocating €1.5bn a year to bolt-on acquisitions. Capital returns will include a dividend payout ratio of approximately 60%, alongside €6bn of share buy‑backs expected to run between 2026 and 2029.

Unilever expects €400m-€500m of stranded costs as a result of separating the Unilever Foods business. Restructuring costs will amount to €1.2bn, of which €500m, incurred over 2027 to 2029, will be allocated to offset the stranded costs. Part of the costs will also be allocated to strengthened distribution channels in smaller markets.

Overall, while the initial share price fall reflects short-term technical selling and ‘separation anxiety,’ the creation of a focused HPC leader and a global Flavour powerhouse offers a clearer long-term value proposition once the initial equity overhang clears.

Source: Bloomberg

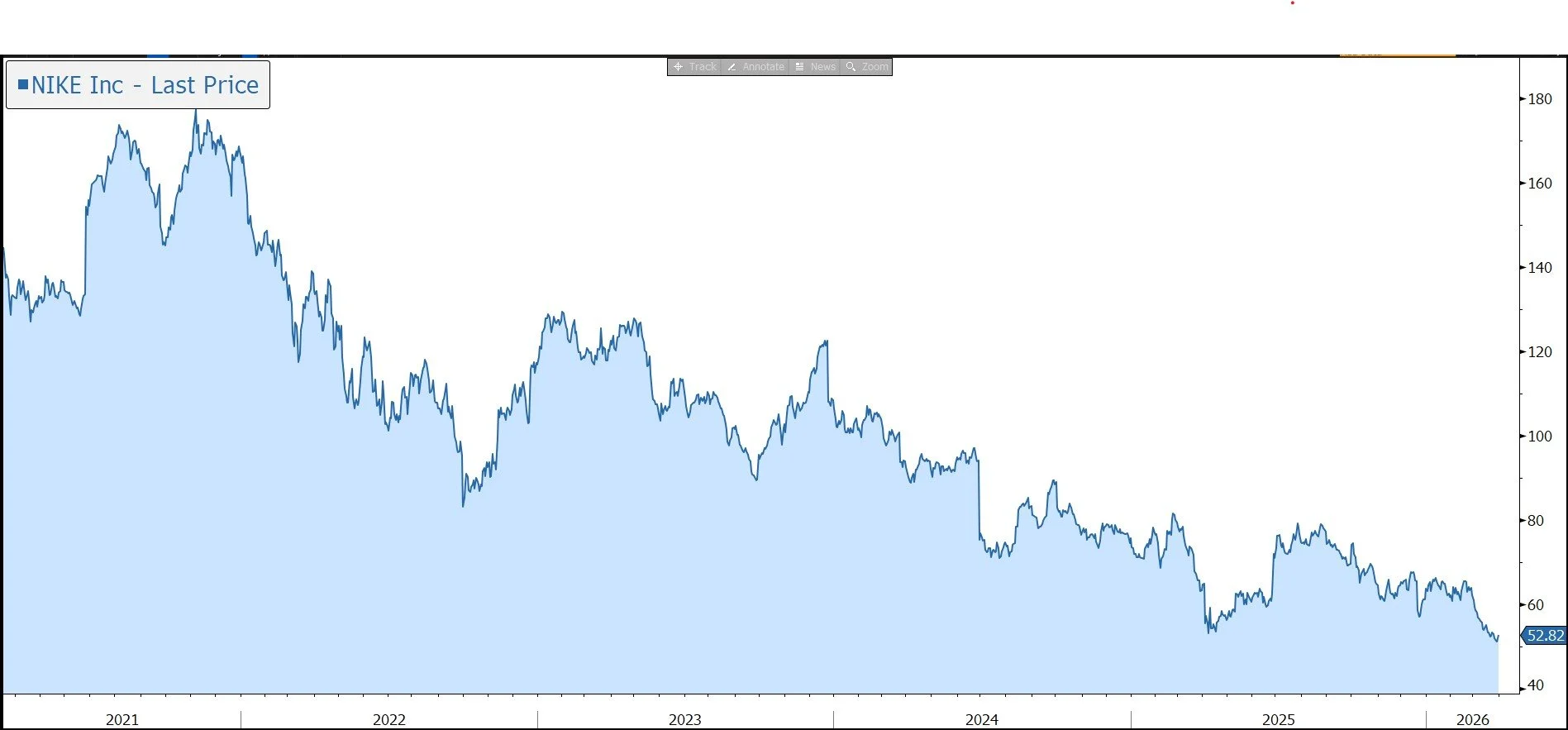

Last night, Nike released results for the three months to 28 February 2026, the third quarter of its financial year to end May 2026. The figures were broadly in line with management expectations driven by the areas the group prioritised first in its recovery plan: Running, Wholesale and North America. However, progress elsewhere – notably Greater China, EMEA, and Sportswear – remains slow, with the recovery taking longer than management would like. As a result, the company has issued disappointing guidance for the rest of the calendar year. In response, the shares were marked down 9% after hours.

Nike is the world’s leading sports footwear and apparel company. Its products are sold at various sporting goods retailers, as well as company-operated stores and websites. In the long term, the company should be well placed to benefit from increased consumer demand for healthier living. Nike has a strong brand and an impressive track record of product innovation.

However, over recent years, the company made a number of strategic errors, the impact of which were exacerbated by a subdued macroeconomic backdrop, intense promotional activity, and the emergence of competition from new brands such as On and Deckers’ Hoka. In particular, there was:

· an over-reliance on key ‘classic’ product franchises (Air Force 1, Air Jordan 1, and Dunk) at the expense of new innovation.

· an overly aggressive push away from a wholesale-driven model to a direct (in particular digital) model which alienated third-party retailers who are essential to elevate the brand and grow the total marketplace.

In response, former senior executive (and 32-year Nike veteran) Elliott Hill returned to the company as CEO. Given that much of the recent corporate malaise was down to poor management/strategy, the hope is that Nike will return to its roots and the culture that made it so successful. The plan is to ‘lead with sport and put the athlete at the centre of every decision, leveraging athlete insights to accelerate innovation, design, and product creation’.

The group has accelerated its multi-year cycle of innovation and pulled forward several new products, especially in high-volume areas like running, training, football, sportswear, and Jordan. Inventory cleaning has been aggressive, removing stale product from the market although this has further to go. There has been a refocus on the wholesale market and a shift at Nike Digital to a full-price model, reducing the percentage of the business driven by promotional activity. Nike is also being aggressive in sports marketing across leagues, associations, teams, and individuals.

Overall, immediate action has been taken in areas that will make the most near-term impact. Although early results have been encouraging, the company has admitted change will take time and “turnaround efforts may hurt in short term”, with sales and gross margin in decline. Furthermore, progress is not expected to be linear as parts of the business recover on different timelines.

In the three months to 28 February 2026, revenue was down 3% on a currency-neutral basis to $11.28bn, in line with the market estimate of $11.23bn. Nike Brand sales were down 2% at $11.0bn, while as expected the Converse brand fell by 37% to $264m.

Once again, the Running category (+20%) was the standout performer. On the negative side, the ongoing removal of unhealthy inventory in the classics range was a five-point headwind to the results, while the digital channel is still too promotional.

By region, North America, which accounts for around half of sales, generated revenue growth of 3% in the quarter. The region has been the early focus on the group’s turnaround plan and the recovery so far provides encouragement for the group as a whole. Elsewhere, Europe, Middle East, & Africa (EMEA) fell by 7%, while Asia Pacific & Latin America (APLA) was down 2%.

As expected, headwinds in Greater China persisted, with revenue down by 10%. The decline was driven by competition from domestic brands. The company has now taken a number of unplanned actions including new management, increased innovation. and improved store layout. Although the company remain very positive on the long-term opportunity in China, management admits the recovery will take time.

Nike Brand sales are split into Direct sales (both online and through Nike-owned stores) and wholesale revenue from third party retailers. During the quarter, Nike Direct sales fell by 7% to $4.5bn, with digital down 9% and stores down 5%. Wholesale grew by 1% to $6.5bn, a decline in the rate of growth compared to previous quarters.

All categories were in decline: Footwear (-1%); Apparel (-4%); Equipment (-6%).

The company continues to see pressure from tariffs and its efforts to clear out aged inventory on its margins. The gross margin fell by 130 basis points to 40.2%, including a 315 basis points tariff impact. Selling and administrative expenses rose by 2%, with demand creation expense (i.e., marketing) flat, as higher sports marketing expense was offset by lower. Operating overhead expense rose 3%, primarily due to employee severance costs, partially offset by lower other administrative costs. EPS fell by 35% to 35c but was well above the market forecast of 28c, albeit helped by non-operational other income.

Inventories remain elevated across all geographies, albeit down 1% to $7.5bn, primarily reflecting a decrease in units and product mix shifts, partially offset by increased product costs, primarily due to higher tariffs in North America. The company had said inventories would be in a ‘clean’ position at this stage, although this is only the case in North America. The full inventory clean is now not expected until the end of the calendar year.

The group’s balance sheet remains strong – with a small net cash balance. During the quarter, the group returned just under $609m to shareholders through dividends. The payout in the latest quarter was 41c, up 2.5%.

The company now believes it has more confidence in its trajectory and is planning to host an investor day in the autumn at which it will lay out new medium-term targets. In the meantime, guidance has been provided for the rest of the calendar year. Over the near term, the net effect of the strategic actions will continue to result in lower revenue, gross margin pressure, and higher marketing expenses.

In the current quarter, revenue is expected to be down 1%-3%, at constant currency, with China down 18%. The gross margin is forecast to be down 25-75 basis points (including a 250 basis points tariff impact). The August quarter is expected to be the last quarter that tariffs have an impact, while the November quarter is expected to see gross margin expansion. Finally, the company now expects revenue to be down in the low single digits for the rest of the calendar year and EPS to be ‘flattish’, both well below the current market expectation.

Source: Bloomberg