Morning Note: A Round-up of Global Financial News.

Market News

The Iran war entered its second week with no resolution in sight, with President Donald Trump demanding Tehran’s unconditional surrender. Meanwhile, Iran appointed Mojtaba Khamenei to succeed his father as Supreme Leader, signalling that hardliners remain firmly in control. As things now stand the US, Israel, and Iran look to be increasing their willingness to commit to sustained conflict.

An Iran-linked bulk carrier was the only commercial vessel to transit the strait of Hormuz in the past 24 hours. On Saturday, China’s Sino Ocean was the last commercial ship not linked to Tehran to make the trip.

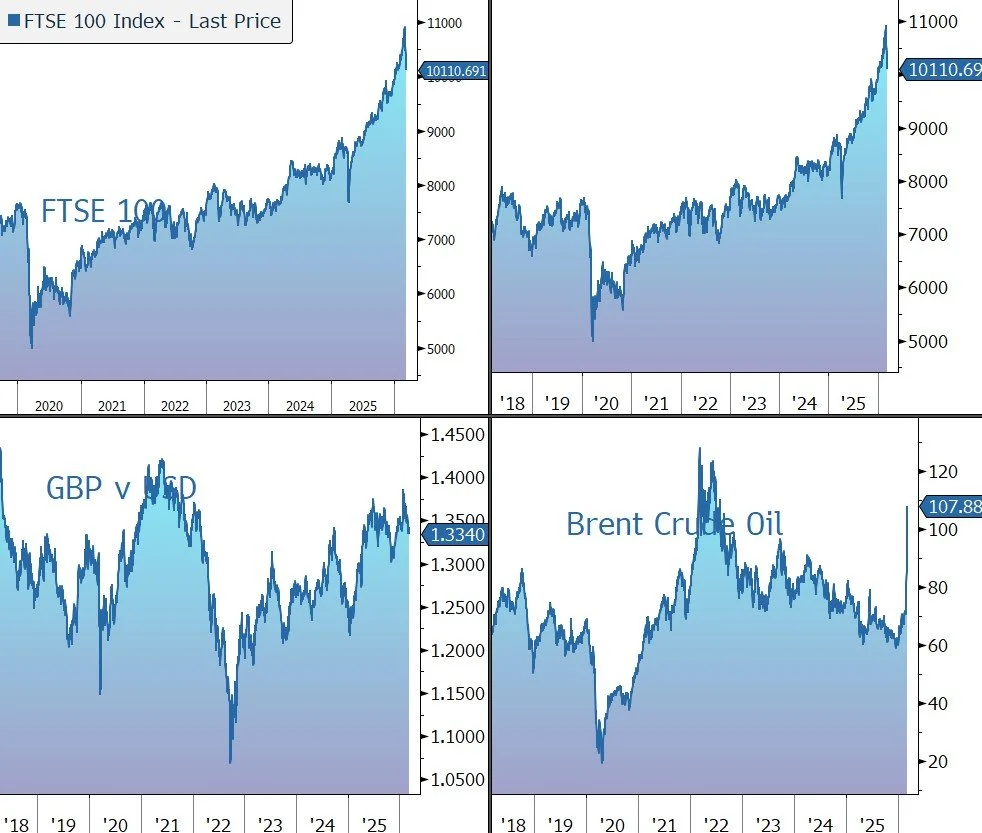

Brent crude has surged 15% to $105 a barrel, amid production cuts from major Middle Eastern producers. The price pulled back from $119 following an FT report that Group-of-Seven countries will discuss a possible joint release of petroleum from reserves.

Crude has the potential to decline over the medium term as supply chains adjust — especially if Saudi Arabia and the UAE manage to divert some of the oil that used to flow through the now choked off Strait of Hormuz to alleviate the current hit to supplies. However, oil traders are positioning for higher oil prices for longer – the December Brent futures contract is trading above $78 a barrel, more than $13 above where it sat a month ago.

In Asia this morning, the Nikkei 225 Index tumbled 5.2% to close at 52,729, hitting its weakest levels in two months.

Japan relies on the Middle East for around 95% of its oil supplies with about 70% coming via the Strait of Hormuz, making the country particularly vulnerable to oil shocks. Other Asian markets also fell: Hang Seng (-1.4%); Shanghai Composite (-0.6%).

Elsewhere, the S&P futures currently expect the US market to open 1.5% lower this afternoon. The FTSE 100 is currently 1.5% lower at 10,111. BP and Shell are among the small number of risers.

The US dollar climbed although other traditional safe havens fell: the yield on the US 10-year Treasury note has risen to around 4.2%, reaching its highest level in nearly a month, while gold slipped to $5,100 an ounce.

On the economic front, the US payroll data for February came in well below market expectations. The figure was minus 92k, versus +55k expected and +130k the previous month. The 4.4% unemployment rate was slightly worse than the 4.3% forecast.

The UK 10-year gilt yield has surged to above 4.70%, reaching its highest since mid-October, as investors assess rising inflation risks. Traders are now pricing a interest rate hike as the next move from the Bank of England. Sterling trades at $1.3310 and €1.1550.

UK gas prices continues to rise – it has almost doubled to more than 150 a therm since the start of the war. As it stands, this will feed through to a sharp rise in gas and electricity prices when the next Ofgem energy price cap begins on 30 June. Keir Starmer pledged to help UK households with soaring energy bills.

Source: Bloomberg