Morning Note: A Round-up of Global Financial Market News.

Market News

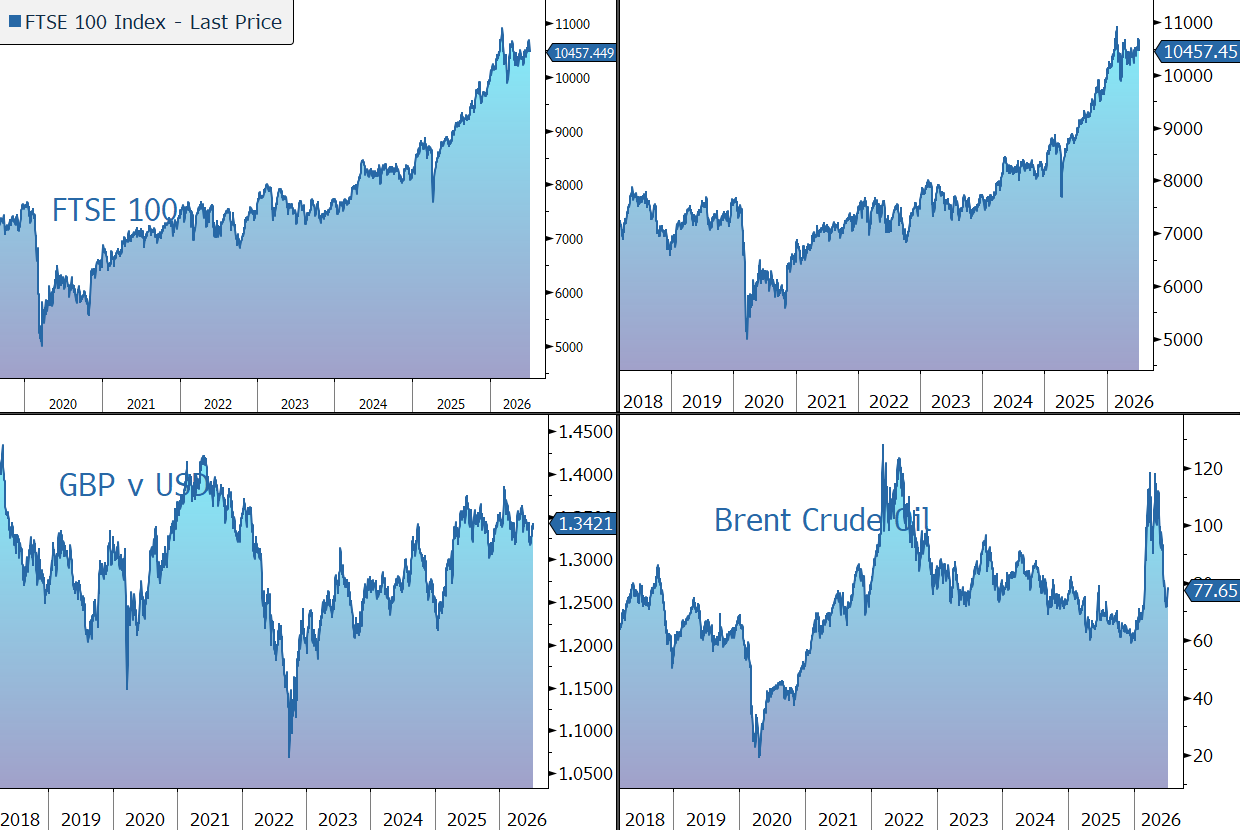

Brent Crude trades at $78 a barrel, up nearly 10% for the week, after the US military confirmed it had carried out strikes on Iran for a second straight day, intensifying tensions and fuelling concerns over energy supplies from the Middle East. Iran launched missiles and drones at US bases in Kuwait and Bahrain, state-run Press TV reported. Traffic through the Strait of Hormuz came to a near standstill amid the hostilities.

Gold has rallied back above $4,100 an ounce, while the yield on the US 10-year Treasury is 4.57%. The minutes from the Federal Reserve’s June meeting showed that only a few policymakers favoured a rate increase, though officials expressed growing concern over inflation. Markets continue to price in at least one rate hike by the end of 2026. Investors are now awaiting the latest weekly jobless claims and existing home sales data for fresh guidance on the interest rate outlook.

US equities closed off their lows last night – S&P 500 (-0.3%); Nasdaq (+0.2%) – and are expected to open higher this afternoon. In Asia this morning, markets were mixed: Nikkei 225 (+1.4%); Hang Seng (-0.6%); Shanghai Composite (+1.7%); Kospi (+0.6%). SK Hynix’s US listing was said to be more than seven times oversubscribed, sending its Seoul-listed shares higher.

The FTSE 100 is currently 0.3% lower at 10,457. Companies trading ex-dividend today include BAT (1.32%) and Halma (0.41%). Sterling strengthened to $1.3420 and €1.1734, while the 10-year Gilt yields 4.93%.

AstraZeneca has been marked down by 8% following news that its Wainua drug, made in partnership with Ionis, failed to meet the main goal of reducing cardiovascular deaths and recurring heart problems in a late-stage trial.

Donald Trump said Spain agreed to pay more after he threatened a trade embargo during the NATO summit. Meanwhile, Switzerland believes there’s a “good chance” of securing a lasting deal with the US at 15% tariff rates.

Source: Bloomberg