Morning Note: Market News and an Update on Winton Trend Fund.

Market News

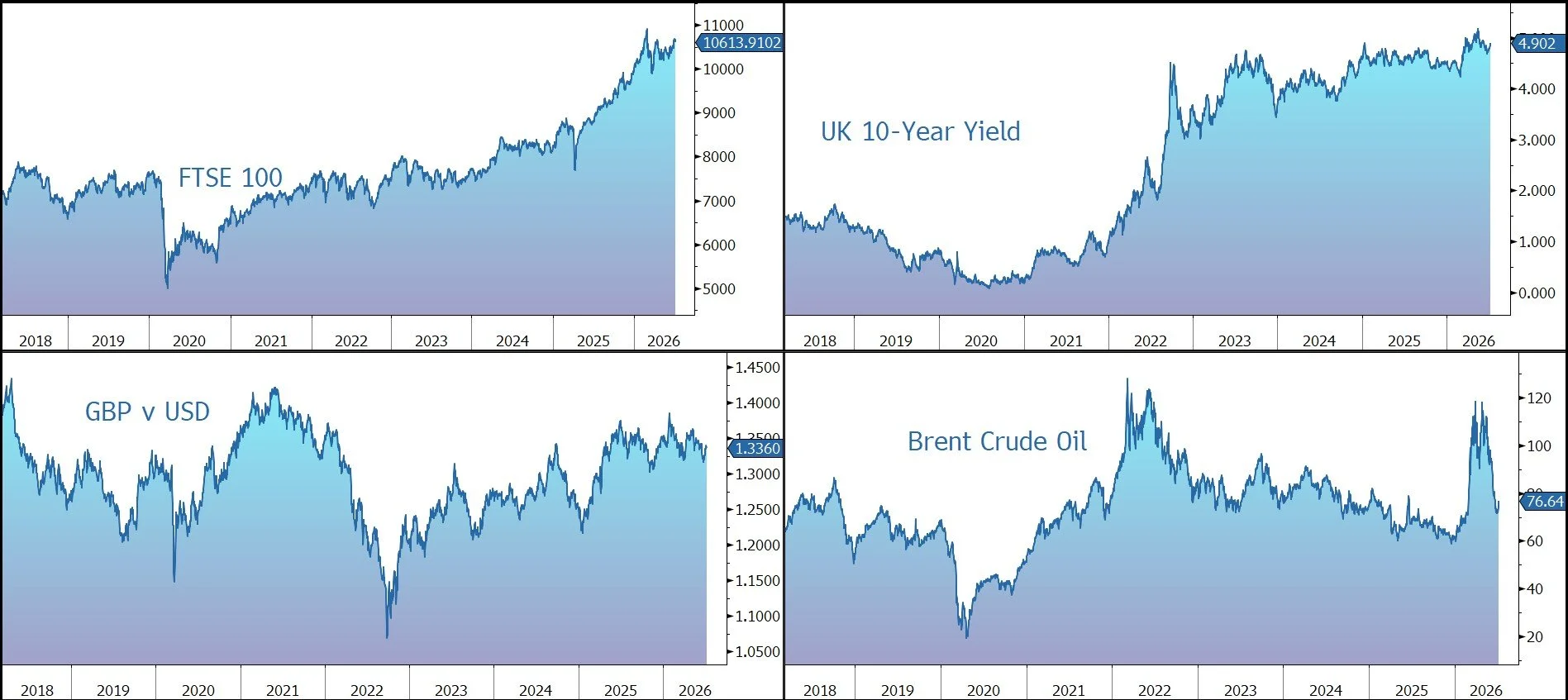

The US military launched fresh air strikes on Iran following recent attacks on ships transiting the Strait of Hormuz. The renewed escalation threatened the interim US-Iran peace deal and drove Brent Crude up 4% to $76.50 a barrel, stoking inflation fears and raising prospects for interest rate hikes. The US also revoked a waiver allowing Iran to sell crude on global markets, while the latest hostilities discouraged shipowners and regional producers from using Hormuz, raising the risk of renewed disruptions to global energy supplies. Gold fell back to $4,120 an ounce.

Minutes from the Fed’s June meeting are expected to show stronger support for higher interest rates, reflecting a growing focus on persistent inflation, Bloomberg Economics said. The yield on the US 10-year Treasury is 4.55%.

US equities traded lower last night – S&P 500 (-0.5%); Nasdaq (-1.2%) – with weakness concentrated in technology and semiconductor names. Microsoft is said to be starting to replace OpenAI and Anthropic with its own AI models in products like Excel and Outlook. In Asia this morning, equities also fell: Nikkei 225 (-2.1%); Shanghai Composite (-0.5%); Kospi (-5.3%). Alibaba jumped by 11% on an optimistic earnings report.

The FTSE 100 is currently 0.5% lower at 10,614, while Sterling trades at $1.3370 and €1.1695. The Lloyds (formerly Halifax) house price index showed prices were up 0.2% in June, suggesting the market may have started to turn a corner. UK hiring stabilised in June, with permanent placements returning to pre-Iran war levels and demand for temporary staff surging, according to a survey by the Recruitment & Employment Confederation and KPMG. Pay growth also accelerated. The 10-year Gilt yield moved up to 4.88%.

Source: Bloomberg

Alternative Fund Update – Winton Trend

Diversification across asset classes is a critical element of managing your investments. At Patronus, when we construct a portfolio, we look to allocate a portion of capital to so-called ‘anti-fragile’ investments that provide shelter in difficult times when other (‘fragile’) asset classes (such as equities and bonds) are struggling to generate a positive return. We believe the Winton Trend Fund is one such investment.

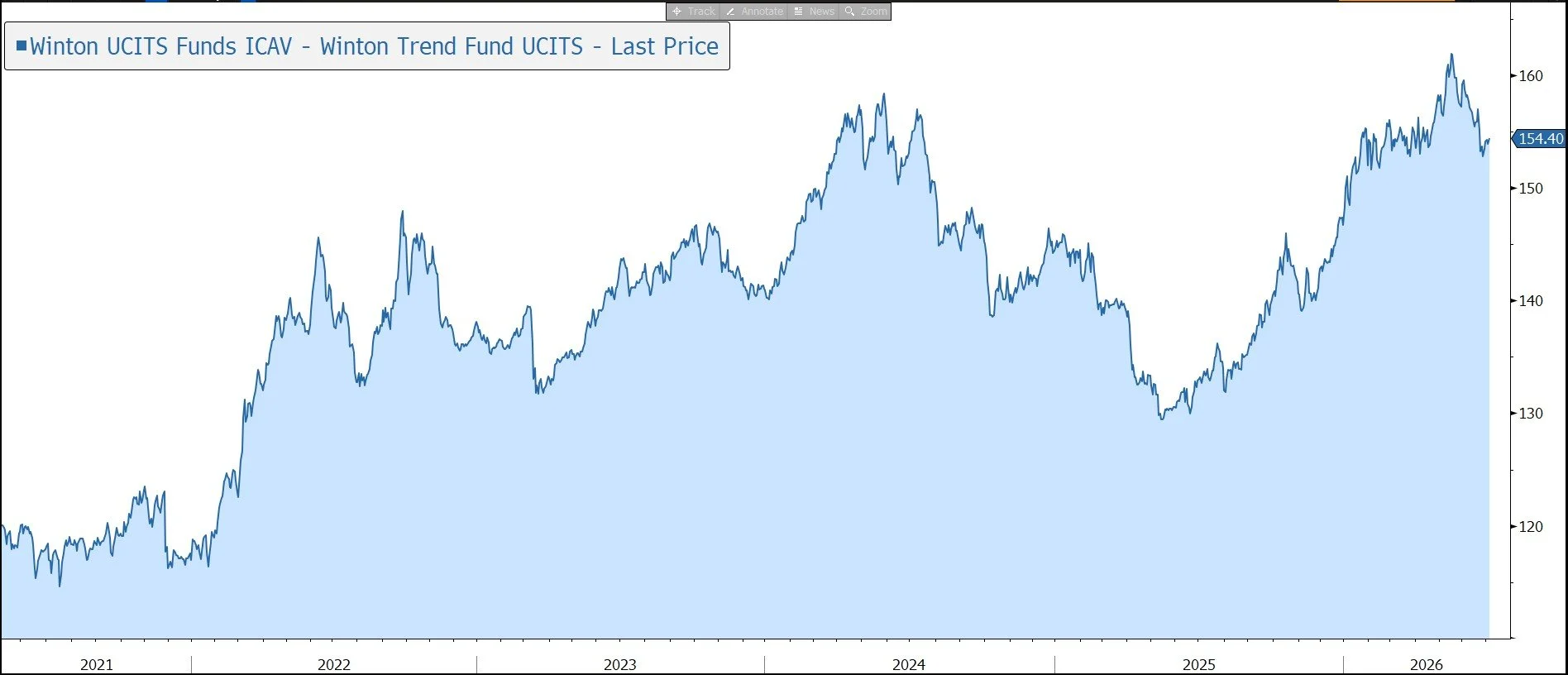

Winton Trend is an actively managed fund which seeks to achieve long-term capital appreciation through a trend following strategy. The manager invests in a diversified portfolio of financial contracts (derivatives) that provide a return linked to the performance (up or down) of certain share indices, bonds, commodities, and currencies. Although the fund has a relatively short track record (since July 2018), it has performed very well in times of market stress.

Total assets in the UCITS vehicle currently stand at around $1.1bn, while the overall trend strategy has assets of $3.7bn.

· The correlation to equities and bonds is low.

· The fund employs a low level of leverage.

· The annualised volatility is the rate at which the price of a fund increases or decreases for a given set of returns. It is measured by calculating the standard deviation of the fund’s monthly returns. It is currently 9.5%. The manager seeks to mitigate against sharp reversals – positions decrease when volatility increases; the system naturally takes profits.

· Despite periodic bursts of outperformance for faster systems, Winton believes the evidence still suggests stronger performance for slower systems over most investment horizons. The fund continues to trade a blend of speeds with the twin aims of maximising risk-adjusted returns and portfolio diversification.

· The fund is relatively low cost: 1% OCR (of which Management fee is 0.80%) and no performance fee.

The manager highlights that although trend-following strategies are often associated with strong performance in difficult times for the stock market, the strategy can also perform well at the same time as equities. What is more important for trend followers is the diversity of the trends on offer – the strategy tends to perform strongly when there are large moves relative to volatility in markets across multiple sectors. Managers can therefore increase the consistency of a trend-following strategy’s returns by maximising the range of idiosyncratic trends in which the strategy can participate.

Although it is difficult to predict where trends will come from, an investor can identify the types of environments where trend-following works well. These are environments where there is a high level of uncertainty that leads to large market moves that are difficult to price in.

Last year, a cross-sectional trend-following system in equity indices was introduced. The system had been traded in Winton’s Diversified Macro CTA since 2021 and is designed to be non-directional, taking long positions in outperforming indices and short positions in underperforming indices. The system has had low correlation with the strategy’s directional trend-following in stock indices and other sectors historically. The allocation to the signal is intentionally small, with the aim of modestly improving the overall strategy’s Sharpe ratio, while retaining the performance properties associated with directional trend following.

Overall, we believe the decision to hold the fund depends on whether it will perform well and provide capital protection during periods of market stress. Clearly, 2022 was such a year, with a marked pick-up in risk and volatility as a result of Russia’s invasion of Ukraine. The fund achieved an 18% positive return – outstanding in the context of the heavy fall in both equities (-8% for the MSCI World Equity Index in Sterling terms) and UK bonds (-15% for the Bloomberg/Barclays Bond Indices UK Govt 5-10 Year Index). On this measure, a typical 60/40 equity/bond portfolio was down by 10.8%.

Trend-following funds tend to struggle when a market moves sideways or oscillates and when there is a sharp reversal in a trend.

The Winton Major-Market Trend strategy was broadly flat in the second quarter of 2026 as profits from equity indices and currencies were offset by losses from agricultural commodities and energies.

This brought the year-to-date return to +5.0% and the five-year annualised return to +5.7%.

First-half performance was slightly behind the peer group. The SG Trend Index was up 8.5% (with returns ranging from +1% to +25%), as top performers benefited from the largest exposures to uptrends in equity indices.

Looking at the performance of Winton Trend in the second quarter in detail:

· Long positioning in equity indices was the top contributor to performance over the quarter as an AI-fuelled rally lifted stocks higher. Asian indices, most notably Japan and Taiwan, led gains in the sector, with more modest profits accruing in North America. A new exposure to European banks was added in the quarter and was another source of profits in the sector, while cross-sectional trend following added to the gains.

· Currencies were another source of gains for the strategy. Short positioning in the Japanese yen versus the US dollar was the top contributor to performance, with the currency hitting a 40-year low against the US dollar towards the end of the quarter.

· Agricultural commodities weighed on returns, most notably in cocoa markets where the strategy was on the wrong side of rallying prices amid expectations of a strong El Niño.

· Having been a notable contributor to performance through the first quarter, energies weighed on returns in the second quarter of the year. Long oil and oil products were the main source of losses in the sector as prices fell to near pre-war levels.

· Profits across the US yield curve - most notably at the short end – were insufficient to offset losses elsewhere in the fixed income sector. Short German and Australian bonds were among the top detractors as yields fell amid easing inflationary pressure.

In terms of positioning, the strategy headed into the third quarter with short positioning in fixed income, precious metals and agricultural commodities, alongside long exposure to equity indices, base metals and energies. These positions will continue to adapt systematically to the prevailing trends as markets price in ever-developing geopolitical and macroeconomic news. Overall, the portfolio remains well diversified.

At the end of 2025, co-CIO Carsten Schmitz retired from Winton and left the investment industry for personal reasons. Simon Judes had continued as CIO, with Nick Thomas-Peter – a senior member of the investment team for over a decade – appointed to a new role of Deputy CIO. Thomas-Peter worked on the development and scaling up of the firm’s mid-frequency futures and equity businesses. Although Schmitz had overseen the development of many of Winton’s key strategic initiatives, we were pleased to see an orderly transition.

We remain positive on the fund given its portfolio diversification attributes. At a time when the geopolitical and macro-economic outlook is uncertain and the prospects for other asset classes remain unclear, we believe an allocation to Winton Trend Fund could continue to help mitigate any losses suffered elsewhere in portfolios.

Source: Bloomberg