Morning Note: Market News and an Update from BP.

Market News

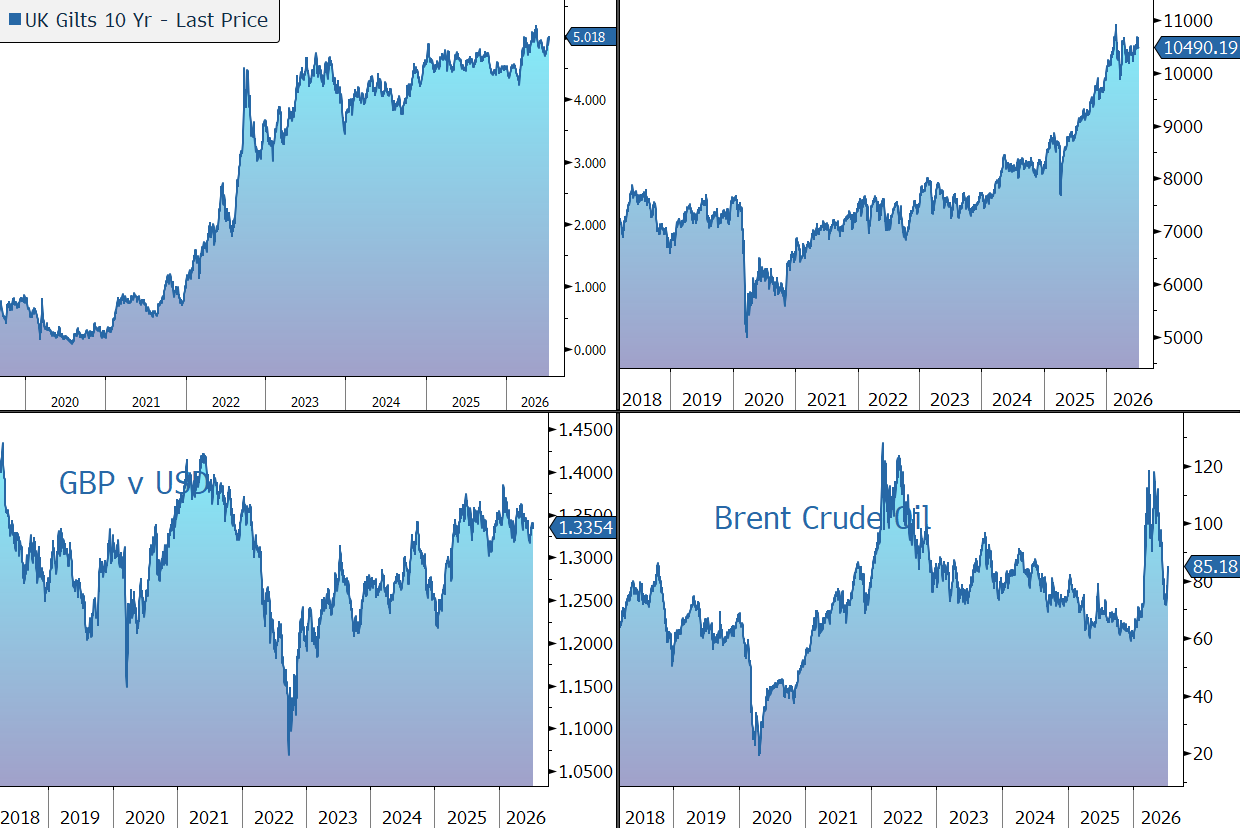

Brent crude has climbed to $85 a barrel, bringing gains for the week to more than 10%, after President Trump reinstated a blockade on Iranian vessels transiting the Strait of Hormuz and announced that all other cargo passing through the waterway would be subject to payment requirements. The blockade is scheduled to take effect at 4pm Eastern Time today. Trump called for a 20% reimbursement on cargoes, saying the US should be compensated by countries benefiting from its efforts to secure the strait.

Traders see a 50% chance of a US rate increase in July ahead of key inflation data today and testimony by Kevin Warsh. Christopher Waller said a hike may be needed in the near term if underlying inflation persists. The yield on the 10-year Treasury moved up to 4.63%, while gold trades at $4,025 an ounce.

The geopolitical concerns pushed US equities lower last night – S&P 500 (-0.8%); Nasdaq (-1.6%). JPMorgan, BofA, Goldman, and Wells Fargo all report this evening.

In Asia this morning, shares erased earlier losses: Nikkei 225 (+0.7%); Hang Seng (+0.7%); Shanghai Composite (+1.4%); Kospi (+0.7%). In Japan, bonds climbed after the nation’s finance minister suggested including JGBs in a tax-free investment programme. Japan’s 20-year bond auction attracted strong demand.

The FTSE 100 is currently 0.3% lower at 10,490. Rachel Reeves is set to deliver her final Mansion House speech on Tuesday, warning that plans to boost growth require maintaining market credibility. The address is widely seen as a coded message to incoming PM Andy Burnham. Sterling trades at $1.3360 and €1.1725, while the 10-year Gilt yield has moved back above 5%.

Source: Bloomberg

Company News

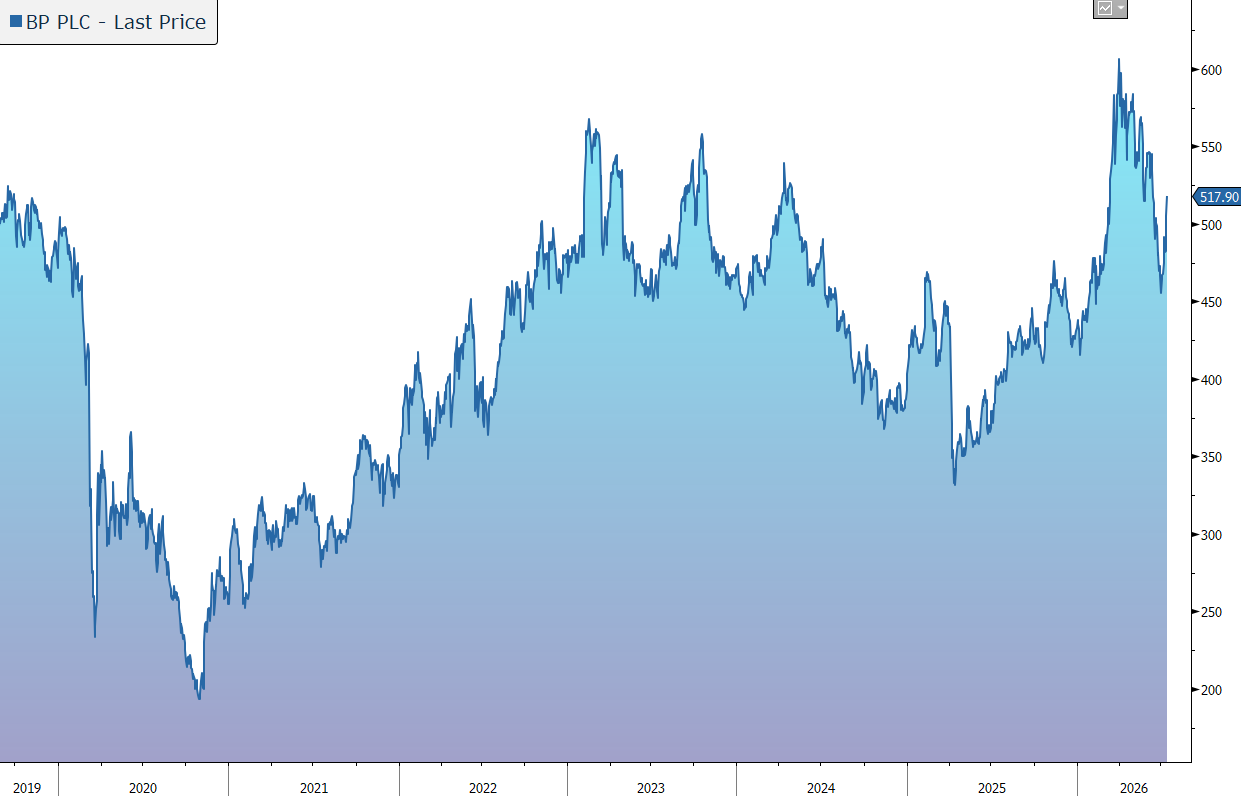

BP has today released a trading statement ahead of its results scheduled for 4 August. The update provides a brief summary of current expectations for the second quarter of 2026, including data on the commodity price environment as well as group performance during the period. The release points to strong oil prices and refining margins, offset by weak natural gas prices. The oil trading result is expected to be slightly higher than the ‘exceptional’ result in the previous quarter. As expected, we will have to wait until the full results next month for news on the group’s financial position and dividend. The shares are up 3% in early trading, helped by the sharp rise in the oil price over the last day or two.

BP is a global integrated energy company undertaking a strategic reset involving a reduction of capital expenditure, a reallocation of spend away from low carbon activities, and a significant cost reduction programme, all of which will drive improved cash flow and returns to support a stronger balance sheet and, in time, growth investment and increased shareholder distributions.

The share price has been fairly volatile of late as a result of the conflict in the Middle East, and its impact on the oil and gas price, and issues related to the Chairman.

In May, BP abruptly dismissed its Chairman Albert Manifold over serious governance and conduct concerns, the second major executive conduct exit in three years following CEO Bernard Looney’s 2023 departure. Manifold fiercely disputes the decision, leaving the company exposed to a high-profile legal battle. Despite the chaos, new CEO Meg O’Neill – the first outsider to lead BP – is continuing the strategic reset, reorganising the group into simpler upstream and downstream units to drive efficiency. However, if the governance uncertainty continues to suppress BP’s valuation, the company risks becoming a prime target for a hostile takeover.

For now, in the Upstream business (i.e. exploration & production), the company is increasing investment to $10bn p.a. (split 70% oil; 30% gas) and targetting returns of more than 15%. The portfolio will be strengthened, with 10 new major projects expected to start up by the end of 2027, and a further 8-10 by 2030. Production is set to grow to 2.3m-2.5m barrels a day in 2030, albeit still below the 2019 level. The aim is to generate structural cost reductions of $1.5bn and an additional $2bn of operating cash flow by 2027. As a result, the cash flow from the group’s production barrels is expected to be significantly higher due to the ‘high-grading’ of the portfolio.

The Downstream division (i.e. refining & marketing) is being high-graded and will focus on ‘advantaged’ and integrated positions. The focus will be on operating performance with a target to consistently improve refining availability to 96%. Capital investment will be $3bn p.a. by 2027, with a target of $2bn in cost savings. Overall, the aim is to generate an additional $3.5bn–$4.0bn of operating cash flow in 2027 and returns of more than 15%. Following a strategic review, last December the company announced an agreement to sell a 65% shareholding in Castrol for an enterprise value of $10.1bn, with expected net proceeds of $6.0bn, which will be used to reduce net debt. BP will retain a 35% stake in a new joint venture, providing exposure to Castrol’s growth and future optionality.

Investment in the group’s ‘transition’ businesses is being slashed from $5bn p.a. to $1.5bn–$2bn p.a., with less than $0.8bn p.a. in low carbon energy. The focus will be on fewer but higher-returning opportunities and more efficient growth. There will be selective investment in biogas and biofuels. In renewables, the focus will be capital-light partnerships, while there will be limited further projects in hydrogen and Carbon Capture & Storage. The group is targeting an annual structural cost reduction of more than $0.5bn in low carbon energy by 2027.

Back to today’s update. In the three months to 30 June 2026, the commodity price backdrop was mixed: Brent crude averaged $103.85/barrel (compared to $81.13/barrel in the previous quarter); US gas Henry Hub averaged $2.90/mmBtu (vs. $5.05/mmBtu); and the refining margin averaged $29.6/barrel (vs. $16.9/barrel). The environment has been volatile as a result of ongoing geopolitical uncertainty and the company believes that even when the conflict ends it will take months for the oil and gas supply/demand balance to normalise.

As a rule of thumb, the company has disclosed that: a $1 movement in Brent has a $340m profit impact, a $0.1 movement in Henry Hub has a $40m profit impact, and a $1 movement in the refining margin has a $550m profit impact.

By division, the company has disclosed:

· Reported upstream production in the second quarter is expected to have fallen from 2,339 mboe/d to 2,170-2,220 mboe/d due to seasonal maintenance predominantly in the Gulf of Mexico and the effects of disruption in the Middle East. Full-year underlying upstream production is still expected to be lower due to effects of disruption in the Middle East.

· In the gas & low carbon energy segment, price realisations, compared to the prior quarter, are expected to have an impact of +$0.5bn to +$0.7bn, including the impact of price lags and the changes in non-Henry Hub natural gas marker prices. The gas marketing and trading result is expected to be broadly flat compared with the first quarter.

· In the oil production & operations segment, price realisations, compared to the prior quarter, are expected to have an impact of +$1.8bn to $2.1bn including the impact of the price lags on the group’s production in the Gulf of Mexico and the UAE. Exploration write-offs are expected to be around $0.5bn this quarter, primarily reflecting the impact of the sale of Bay du Nord in Canada (see below).

· In the customers & products segment, compared to the prior quarter, the customers segment has generated seasonally higher volumes, higher fuels margins and broadly flat integrated midstream performance. The products segment benefitted from stronger realised refining margins of $1.2bn-$1.4bn. The oil trading result is expected to be slightly higher than the ‘exceptional’ result in the previous quarter.

· The Q2 results are expected to include post-tax adjusting items relating to asset impairments of $1.0bn. These charges are primarily attributable to transition businesses in the gas & low carbon energy segment and are excluded from underlying replacement cost profit.

Further detail on operating cash flow, net debt, and shareholder distributions will be provided with the Q2 results on 4 August.

As a reminder, the company has a structural cost-reduction target of $6.5bn-$7.5bn by 2027, versus a 2023 base of $22.6bn. At the end of Q1 2026, $3.1bn had been achieved. Despite higher oil prices, investment discipline remains a key priority. Capital expenditure in 2026 is expected to be $13.0-$13.5bn, a level the company believes supports progressive long-term earnings growth.

By 2027, the aim is to generate compound annual growth in adjusted free cash flow of more than 20% at $70/barrel oil price and returns on average capital employed of more than 16%. Note the oil price is currently $85 a barrel.

The group is targetting $20bn of divestments by 2027. In 2026, proceeds of $9bn-$10bn are expected, including $6bn from the announced Castrol transaction, all significantly weighted to the second half. Earlier in the month, BP announced the sale of its 37.2% stake in the Bay du Nord offshore oil project in Canada. Given the pool of potential organic growth opportunities, there are no plans for major acquisitions.

The company’s first capital allocation priority is a resilient dividend, which is expected to increase by at least 4% per ordinary share a year. The Q2 dividend will be declared at the time of the results in August – current forecasts imply a full-year yield of just above 5%.

BP remains committed to maintaining a strong investment grade credit rating and a reduction in net debt to $14bn–$18bn by the end of 2027 (vs. $25.3bn as at Q1 2026). We note, however, the net debt figure doesn’t include lease liabilities ($13.5bn), Gulf of Mexico oil spill payables ($6.1bn), and hybrids ($13bn). Treating hybrids as 50/50 equity/debt, the gearing measure rises to nearer 40%, rather than the 24.7% disclosed at the Q1 stage.

In the second quarter, net debt is expected to fall to $22bn-$23bn. This reduction is after the payment of $2.9bn to redeem the €2.5bn perpetual hybrid bonds in June in line with plans to reduce hybrids by $4.3bn by end 2027. Remaining hybrid bonds are expected to be around $13bn at 30 June 2026. The debt movement also includes the payment for $1.1bn Gulf of Mexico settlement liabilities, which contributes to an expected working capital build in the range of zero to $1.5bn.

In a nod to these ‘other’ financial obligations, the company is currently not buying back its shares and is fully allocating excess cash to accelerate the strengthening of its balance sheet, a process that has accelerated with higher commodity prices. We believe this is the right decision – it saves $3bn a year and will create a strong platform to invest with discipline into the group’s ‘distinctive’ deep hopper of oil and gas opportunities.

We believe decarbonisation can’t happen at the flick of a switch – oil and gas will remain part of the global energy mix for decades, with demand driven by population growth and higher incomes, particularly in developing countries where the desire for energy intensive goods and services like cars, international travel, and air conditioning is rising. We also believe the production of the materials needed to transition to net zero can’t happen without hydrocarbons. At the same time, reduced investment in new production, partly because of environmental concerns, and natural decline rates, are increasingly leading to constrained supply.

Against this backdrop, investor disillusion with BP’s tilt towards low carbon energy, particularly in terms of capital discipline and returns (as evidenced by $17bn of impairments since 2023), and its mixed governance track record, has had a negative impact on the share price over the medium term relative to the peer group. However, the recent arrival of a new CEO, combined with operational high-grading, reduced financial gearing, and ongoing M&A speculation suggests that the valuation gap between BP and its peers should narrow.

Source: Bloomberg