Morning Note: Market News and an Update from Delta Air Lines.

Market News

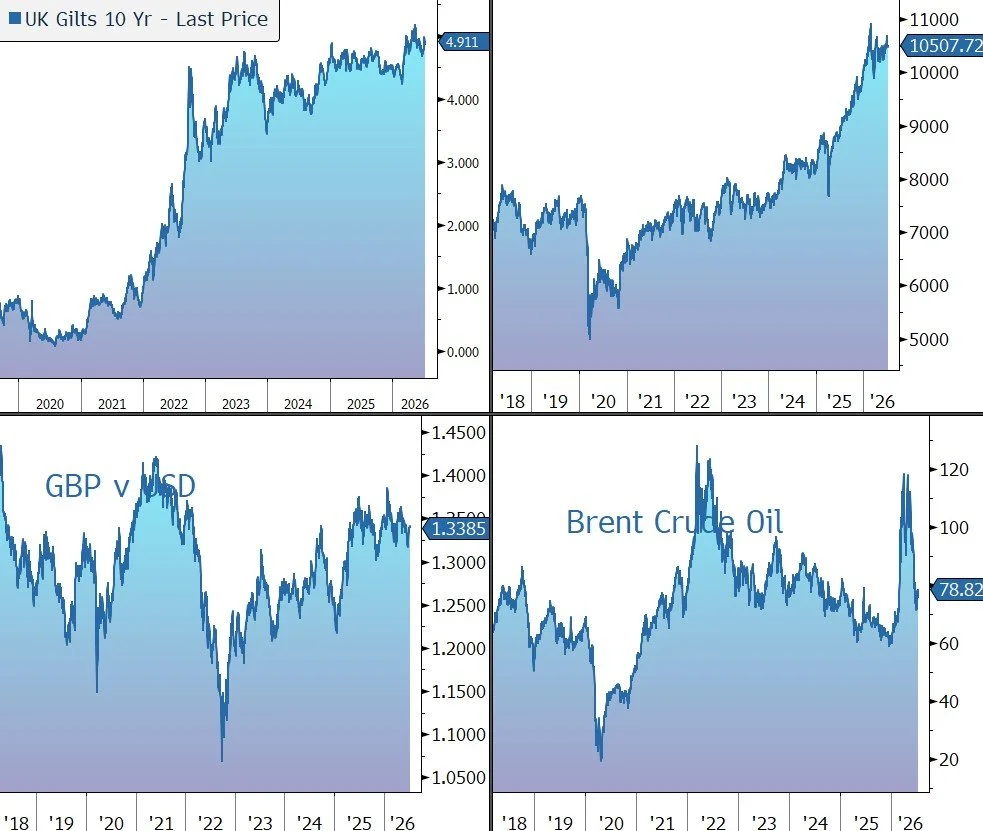

Markets have started the week in a risk-off mood after the US and Iran exchanged fresh missile strikes over the weekend amid ongoing tensions over shipping through the Strait of Hormuz. The US carried out its fourth strike in a week against Iran on Sunday in retaliation for an Iranian attack on a Cyprus-flagged container ship. Tehran declared that the Strait of Hormuz would be closed ‘until further notice’. Brent Crude climbed about 4% to around $79 a barrel.

The US 10-year Treasury yield rose to 4.59% on increased inflation concerns, while gold drifted down to $4,060 an ounce. Key US inflation data this week may provide further clues on the Federal Reserve’s interest rate policy outlook.

Asian equities retreated this morning: Nikkei 225 (-1.9%); Shanghai Composite (-2.1%); Kospi (-8.9%). SK Hynix fell the most on record as investors shifted to its newly listed ADRs, driving the Kospi lower. The yen weakened to 162 versus the dollar after Reuters reported that Japan has no plans to change GPIF’s allocation.

The FTSE 100 is currently 0.3% lower at 10,484, while the S&P 500 (-0.5%) and Nasdaq (-1.3%) are expected to open down this afternoon. The Q2 corporate earnings season kicks off this week, with announcements from the US banks, ASML, Richemont, Johnson & Johnson, Experian, Atlas Copco, and Assa Abloy.

On the political front, Andy Burnham is set to become the new Labour party leader when the leadership contest ends on this Friday and is expected to be officially appointed as prime minister on Monday 20 July. Sterling trades at $1.3385 and €1.1730, while the 10-year Gilt yields 4.91%.

Source: Bloomberg

Company News

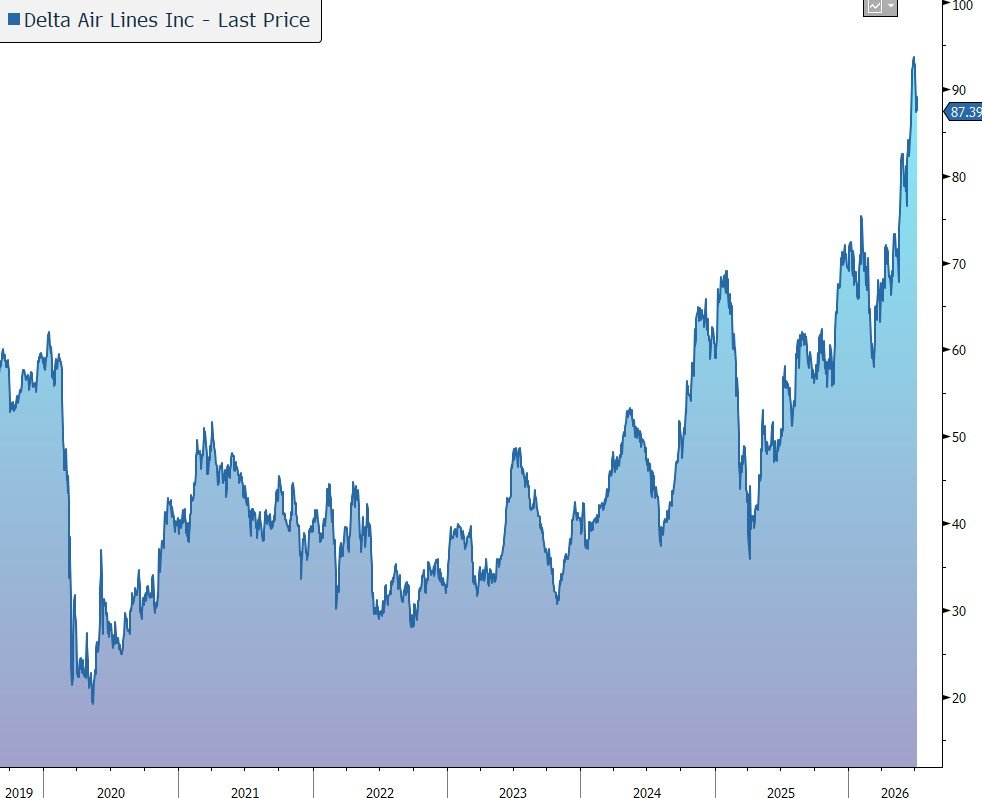

Last Friday, Delta Air Lines released second-quarter results which were better than market expectations driven by broad demand strength and strong execution. The company reiterated its full-year guidance despite a multi-billion dollar fuel headwind. In response to the update, the shares were marked down by 2%

Delta is one of the world’s largest global carriers with a fleet of around 1,300 aircraft that are varied in size and capabilities, providing flexibility to adjust aircraft to the network. The group has acquired new and more fuel-efficient aircraft with increased premium seating to replace older aircraft and has reduced fleet complexity with fewer fleet types.

In the first half of 2026, the group took delivery of 11 new aircraft. With an industry-leading global network, Delta and the Delta Connection carriers offer service to more than 300 destinations on six continents.

During the second quarter, the company generated performance ahead of expectations while absorbing the highest quarterly fuel expense in its history, reflecting broad demand strength, growing brand preference, and momentum across a diversified revenue base. Looking forward, the company is confident that recent fare gains can hold even as fuel prices ease from this year’s highs.

Operating revenue grew by 14% to $17.7bn, a touch above the market forecast of $17.5bn. Capacity grew by 1%, while adjusted total unit revenue (TRASM) rose 12.7%.

Passenger revenue was up 13%, split between domestic (+15%), Atlantic (+8%), Latin America (+4%), and Pacific (+15%). Cargo revenue grew by 39%, while other revenue rose 50%.

Revenue is also split by main-cabin (+8%), premium products (+17%), Loyalty travel awards (+14%), and travel related services (+11%). As a result, Q2 2026, premium ticket revenue ($6.92bn) overtook main cabin revenue ($6.85bn) for the first time in Delta’s history

Adjusted operating expense rose by 20% to $16.1bn, of which adjusted non-fuel unit costs grew by 8% to $11.1bn. Adjusted fuel expense rose 77% to $4.4bn, with fuel price up 75% to $3.93 a gallon. As a result, the operating margin declined by 450 basis points to 8.8%, while EPS fell by 26% to $1.56, which was better than the market forecast of $1.48.

During the first half of the year, free cash flow came in at $1.4bn. The group further strengthened investment grade balance sheet through debt paydown, with net debt falling by $709m to $13.6bn. The group had already announced a 15% increase in its dividend, beginning in the September quarter.

For the full year, guidance for EPS has been reiterated at $6.50-$7.50, as has free cash flow of $3bn-$4bn, in line with the group’s long-term target. For the current quarter, the company expects mid-teens revenue growth, a double-digit operating margin (11%-13%), and EPS of $2.00-$2.50 (better than the current market forecast of $2.02). Non-fuel unit cost performance is expected to improve modestly from the June quarter with further progression in the December quarter as capacity growth begins to normalise.

Source: Bloomberg