Morning Note: A Round-up of Global Financial Market News.

Market News

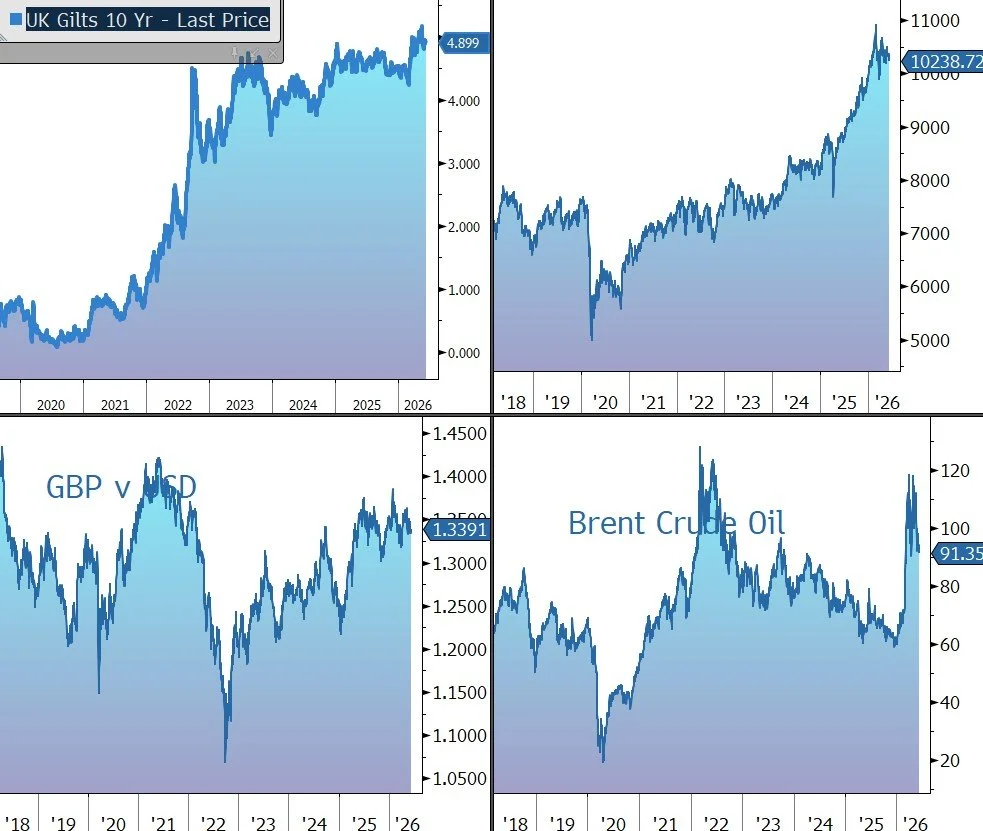

The US launched new strikes against Iran following the downing of an American helicopter, driving oil prices higher and fuelling inflation concerns. The latest escalation has cast doubt on the durability of a fragile ceasefire and the prospects for a broader peace agreement, while extending the near-complete closure of the Strait of Hormuz. Brent Crude is currently $92 a barrel.

Gold extended its recent decline – it is currently $4,200 an ounce – on expectations quicker inflation may lead to more Federal Reserve rate hikes. There is a key US inflation reading later today. CPI is expected to run hot, according to Bloomberg Economics, though core inflation may be more subdued. The yield on the US 10-year Treasury is 4.54%. The ECB will almost certainly hike rates by 25bps at its meeting starting today.

US equities fell back last night during a volatile session – S&P 500 (-0.3%); Nasdaq (-1.0%) – with technology shares under pressure.

In Asia, equities also declined: Nikkei 225 (-1.9%); Hang Seng (-0.6%); Shanghai Composite (-0.4%). South Korea’s Kospi, a barometer of artificial intelligence investment, led regional losses, tumbling 6.3%. TSMC’s sales rose 30% in May thanks to sustained AI chip demand.

The FTSE 100 is currently little changed at 10,239, while Sterling trades at $1.3390 and €1.1585. The UK Treasury continues to resist a push to speed up an increase in defence spending, days before the government unveils its military investment plan, people familiar said.

Source: Bloomberg