Morning Note: Market News and an Update from Halma.

Market News

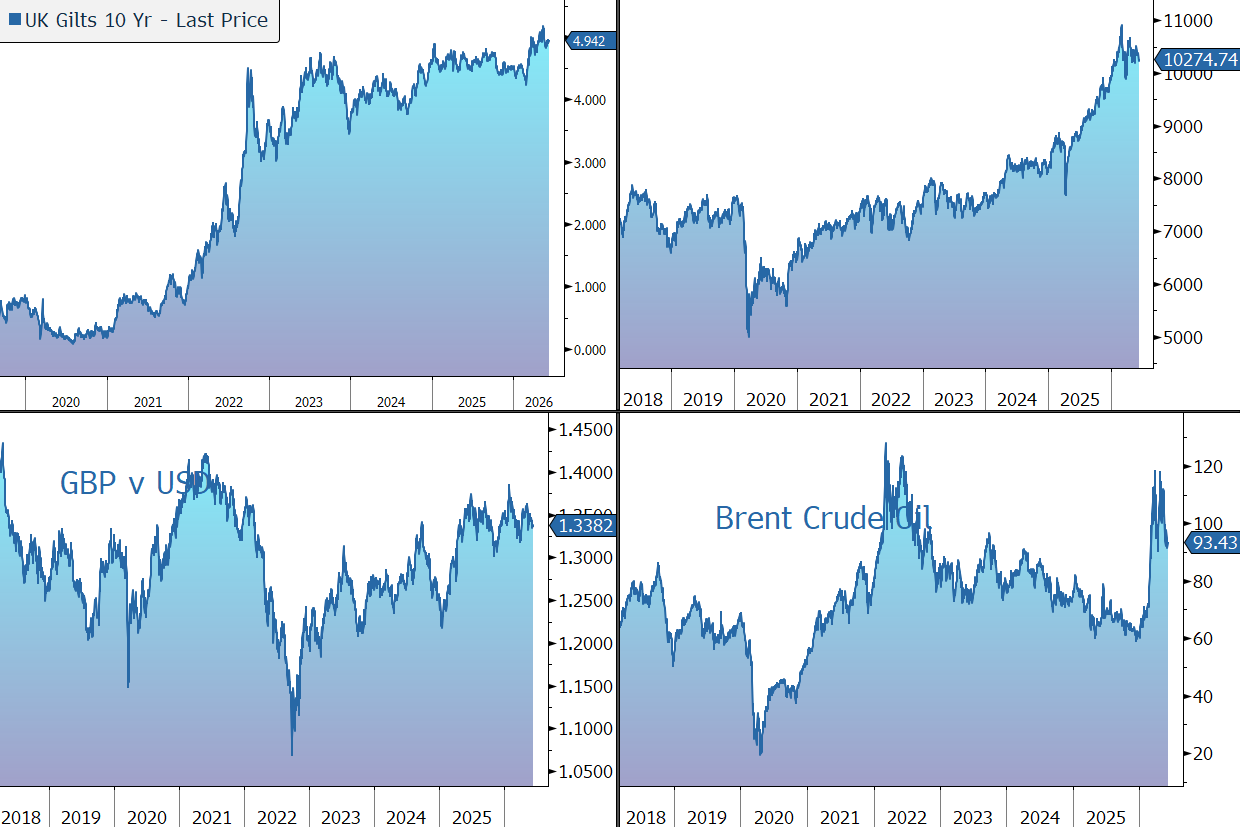

Global equities fell to a more than one-month low as a technology-led selloff deepened and the war in Iran showed little sign of ending. The US completed strikes against “multiple” Iranian targets for the second straight day. Donald Trump told Fox News the bombing would stop shortly but resume the next day if no deal is reached. Trump said more than 200 commercial ships and 100 million barrels of oil have exited the Strait of Hormuz. Brent Crude rose to $93.50 a barrel.

US inflation jumped to 4.2% in May, in line with market expectations, and up from 3.8% in April. Core inflation, which strips out volatile items, such as food and energy, only ticked up from 2.8% to 2.9%. The yield on the US 10-year Treasury sits at 4.55%, while gold fell again and currently trades around $4,100 an ounce.

The ECB is expected to raise rates by a quarter-point, judging it can no longer ignore the upswing in inflation caused by the Iran war. Christine Lagarde will probably be more emphatic that a second hike is coming, Bloomberg Economics said.

US equities moved lower – S&P 500 (-1.6%); Nasdaq (-2.0%) – and a gauge of the so-called Magnificent Seven mega-caps dropped for a fourth day, touching the lowest level since mid-April. OpenAI is considering drastic price cuts to win customers from Anthropic, the WSJ reported. Jim Chanos called SpaceX’s public offering a “hopes-and-dreams IPO,” with a valuation that defies business fundamentals. The offering is said to be over four times oversubscribed.

In Asia, equities were mixed: Nikkei 225 (+0.1%); Hang Seng (-1.2%); Shanghai Composite (-0.5%). The FTSE 100 is currently 0.2% higher at 10,275, while Sterling trades at $1.3380 and €1.1585.

Source: Bloomberg

Company News

Halma has today released results for the financial year to 31 March 2026. The figures came in above market expectations as the company delivered on all its key performance indicators. The dividend was raised by 7%. Looking ahead to the current financial year, strong growth is expected to continue, driven by the photonics business, albeit at a slower rate than last year. The company also revealed that a fifth of its revenue comes from a single client. In response, despite the knock-out results, the shares have been marked down by 10% in early trading.

Halma is a global group of 50 or so life-saving technology companies, with a focus on safety, healthcare, and the environment. The group’s technology is used to save lives, prevent injuries, and protect people and assets across a broad range of sectors including commercial and public buildings, utilities, healthcare/medical, science/environment, process industries, and energy/resources.

Products include control panels for fire safety systems, corrosion monitoring systems, gas detection systems, moisture control systems, and blood pressure monitoring systems. As a result, the company is highly diversified across different industrial cycles.

The main growth drivers include increasing health and safety regulation, demand for healthcare from an ageing population, and demand for life-critical resources. Strong market positions deliver upgrade and replacement sales opportunities as customers seek to maintain regulatory compliance and conform with best practice. As a result, customer spending is often non-discretionary and drives sustained demand throughout the economic cycle. Over time, this has driven consistent profit growth and shareholder returns.

Over recent months, although Halma’s companies have continued to experience varied conditions in their end markets and operate in an increasingly uncertain economic and geopolitical environment, the business has delivered broad-based growth.

During the year to end-March 2026, revenue grew by 14.9% to £2,582m, helped by a 1.0% contribution from M&A, offset by a 2.7% currency headwind. The organic increase was 16.6%, versus guidance of growth in the mid-teens at constant currency.

One of the group’s companies, Avo Photonics, delivered premium growth amounting to eight percentage points of the group’s 17% organic revenue growth. The company was acquired in 2011 and has benefitted from a close relationship with a large “hyperscaler” technology customer, which accounted for 20% of group revenue in the latest financial year. Halma is using this period of premium growth to further invest in other growth opportunities.

Growth was broad-based across all three sectors. The Environmental & Analysis Sector delivered a particularly strong year (+35.7%), which was well spread across the portfolio including premium growth in photonics. Revenue growth in the Safety Sector was 6.5%, with good performance across all its subsectors, which follows two strong years of adjusted profit growth. Healthcare delivered a good performance (+6.3%), supported by a continued and steady recovery in healthcare markets.

The adjusted operating margin rose by 110 basis points to 22.7%, versus guidance of ‘around 22%’. This excludes the one-off profit from the Nuvonic transaction (UV disinfectant systems) which was completed in the first half of the group’s financial year.

The group’s return on total invested capital rose from 15.0% to 16.2%, towards the upper end of the 12%-17% target range and well above its estimated weighted average cost of capital of 10.2%.

Halma has a fantastic dividend track record, having increased the payout by 5% or more every year for the last 47 years. Today, the group has declared a payout of 24.74p, 7% higher than last year.

Cash conversion was strong at 93% and just above the group’s target of 90%. Net debt rose from £536m to £769m, with financial gearing of only 1.16x net debt to EBITDA, well within the target of ‘up to 2x’.

This enables continued investment, both organically and by acquisition, to support continued growth. R&D investment rose by 13% to £123m, representing 4.7% of revenue. The group made five acquisitions in the year for a maximum total consideration of £447m. Since the year-end, two further deals have been made for £75m and the pipeline remains ‘healthy’.

Looking forward, the group has made a positive start to the new financial year with a strong order book and order intake ahead of revenue and last year. The company currently expects to deliver low double-digit percentage organic constant currency revenue growth in this financial year, including premium growth of approximately five percentage points from the photonics business. Adjusted EBIT margin is expected to be in line with the 2026 financial year (excluding the one-off from the Nuvonic transaction).

Source: Bloomberg