Morning Note: Market news and an update on Unilever's ice cream demerger.

Market News

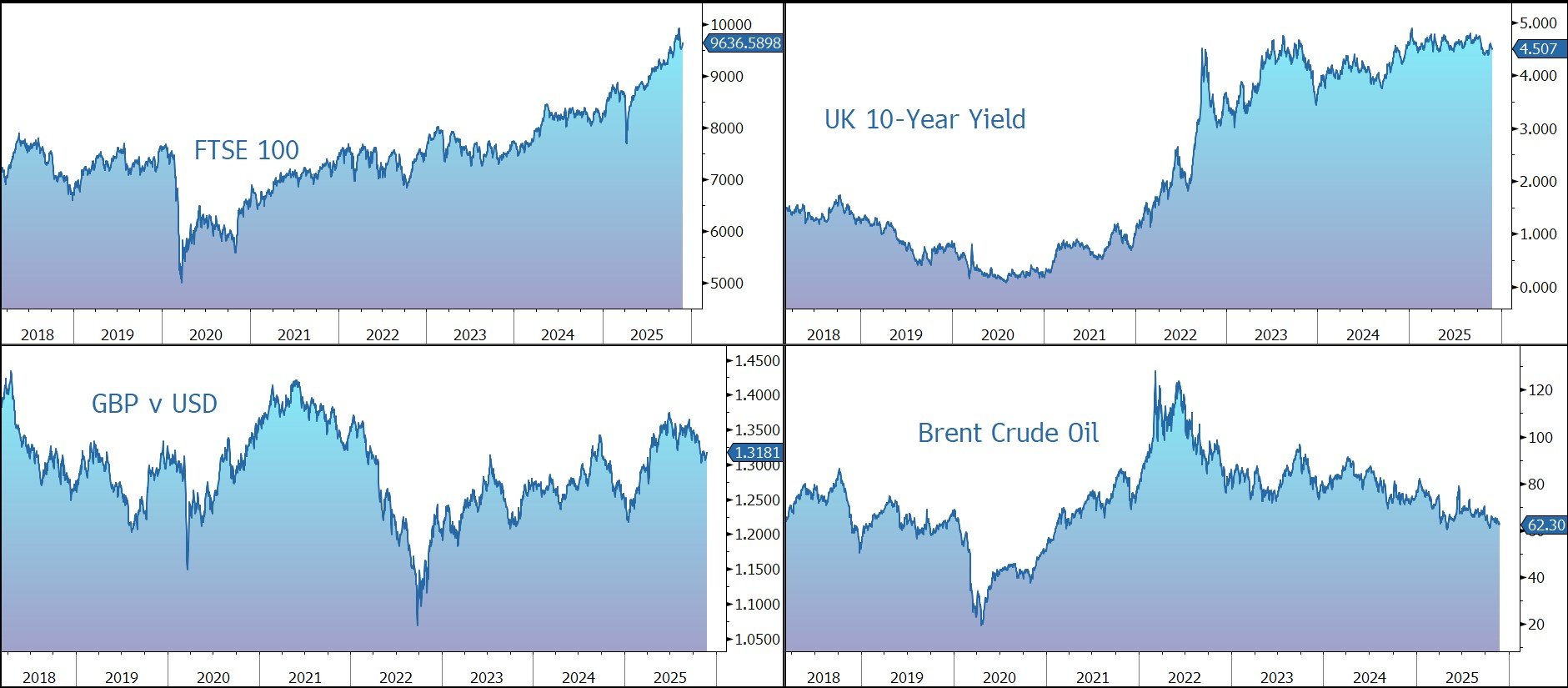

Although there have been reports Ukraine has accepted a revised US peace deal, neither Ukraine nor Russia officially confirmed delegations participated in recent talks. Donald Trump directed his envoy Steve Witkoff to meet with Vladimir Putin in Moscow next week as part of efforts to finalise a peace plan for Ukraine. Goldman said a peace deal may shave off $5 from its base case oil price. Brent Crude currently trades at $62 a barrel.

The UK Budget will be announced at lunchtime. According to reports, Chancellor Reeves has asked banks to make public endorsements of the statement, as she prepares to spare the sector from a tax raid. The Budget expected to include a slew of tax hikes to fill a £20bn hole, but higher levies have been a hard sell to voters struggling with affordability, another issue the chancellor is focused on. The minimum wage has been hiked by 4.1%, potentially adding pressure to UK inflation. Sterling trades at $1.3180 and €1.1385, while 10-year gilts yield 4.51%.

US equities moved from a loss last night to end the session higher – S&P 500 (+0.9%); Nasdaq (+0.7%) – as bets on a December Fed rate cut increased. Mag 7 names were mostly better though Nvidia was a notable decliner amid Google competition concerns. In Asia this morning, equities were mainly firmer: Nikkei 225 (+1.9%); Hang Seng (+0.1%); Shanghai Composite (-0.2%). The FTSE 100 is currently 0.3% higher at 9,636.

Kevin Hassett, the front-runner to be the next Federal Reserve chair, told Fox News he would accept the post if asked. Futures contracts tied to the Fed benchmark show 80% odds of a quarter-point cut in December, compared with 30% just days ago. The 10-year Treasury yield drifted down towards 4%, while gold continued its recent recovery and trades at $4,165 an ounce.

Source: Bloomberg

Company News

Unilever is in the process of demerging its Ice Cream business, The Magnum Ice Cream Company (TMICC), a company incorporated and headquartered in The Netherlands, to become a new listed company. Shareholders will be given 1 TMICC share for every 5 Unilever shares held. Unilever currently expects the new shares will begin trading in the Netherlands, London, and New York on Monday 8 December.

In 2024, TMICC generated sales of €8bn, just under 14% of Unilever’s group sales. However, it generated a lower-than-average operating margin, meaning it only accounted for 9% of operating profit and 7% of free cash flow.

TMICC owns six of the world’s top 10 ice cream brands including Magnum, Ben & Jerry’s, Cornetto, and Wall’s, with a market share of 21%.

The US is by far the company’s biggest market (22% of sales in 2024), well ahead of its second and third biggest markets, Turkey and the United Kingdom (8% and 7% of sales respectively).

The market is fairly mature. According to Euromonitor, Unilever’s ice cream organic sales growth averaged 3.6% between 2015 and 2019. More recently, between 2019 and 2024, growth has picked up to 3.9%. However, this was wholly driven by pricing (+4.5%), which made up for a 0.6% volume decline.

With a focus on premium products, the company of targetting 3%-5% organic sales growth compared to 3%-4% for the overall market. As well as the big ice cream players, competition also comes from own-label producers and confectionery giants expanding into ice cream, such as Ferrero, Mars, and Mondelez.

Ice Cream has distinct characteristics compared with other consumer goods products such as lower price points per kilo in retail due to the presence of private label, the need for a supply chain and point of sale that supports frozen goods, greater seasonality, and higher capital intensity (Magnum has 3m freezer cabinets). As a result, TMICC’s gross margins are only 35%, low by the standards of other consumer goods, but also five percentage points below the number two player Froneri, a JV between Nestle and private equity firm PAI.

Underlying operating margins have averaged 12.6% between 2019 and 2024, with the company guiding to 60 basis points (bps) of improvement in 2025 to 12.4%.

At the EBITDA margin level, the aim is to generate 40-60bps of growth a year from volume (80bps), pricing (120bps), and productivity (100bps), offset by reinvestment (-50bps) and cost inflation (-200bps). Raw material price volatility is a key risk.

As a standalone, more-focused company, the new management team will have operational and financial flexibility to allocate capital to drive growth. The business is already making significant operational changes that are expected to drive stronger performance, including optimising its manufacturing and logistics network and developing flexible distribution channels. The biggest opportunities lie in club stores and the supply chain in the US and the out-of-home market in Latin America, China, India, and SE Asia.

There is a €500m cost savings programme derived from three sources: €350m-€380m from supply chain savings, €70m-€100m from overheads reductions, and €30m-€50m from tech-enabled productivity. The plan is to reduce overheads as a percentage of sales to 11% from 13% in the medium term.

The cashflow target of €0.8bn-€1.0bn compares to the €0.6bn FCF delivered on average in the last three years. The company will start life with net gearing of 2.4x net debt to EBITDA, with a target to remain between 2.0x-2.5x. In the near term, cash flow will be somewhat constrained by increased capex, the buyout of the India business, and separation costs, but in time there may be scope for a share buyback. The company will pay a dividend and has set a payout ratio of 40%-60% of adjusted net income, with the first payment to be paid in 2027 for the 2026 dividend.

The mid-point of the sales and margin guidance would generate net income growth of 8%-9%. Combined with a dividend yield of 2-3% would give a total shareholder return of 10%-12%.

There are other risks on top of those highlighted above including the impact of GLP-1 drugs on ice cream consumption, political risk as a result of Ben & Jerry’s independent board of directors, the stock overhang from Unilever remaining a c.20% shareholder, and the near-term flow back from shareholders who don’t want to hold a small weighting.

Existing Unilever shareholders should note the company expects to complete a share consolidation on 9 December. This is a mechanical reduction in the total number of Unilever shares intended to restore the Unilever share price to approximately its pre-demerger value and ensure comparability of EPS and DPS.