Morning Note: Market News and an Update from Sodexo.

Market News

Donald Trump threatened Iran for charging fees in the Strait of Hormuz after earlier expressing optimism about a deal. Meanwhile, signs of activity are emerging, with two Japanese tankers heading toward the strait. Israel will hold direct talks with Lebanon next week, but Benjamin Netanyahu said strikes on Hezbollah targets will continue. As Trump tries to extricate himself from the war, fault lines are appearing in his close relationship with Israel.

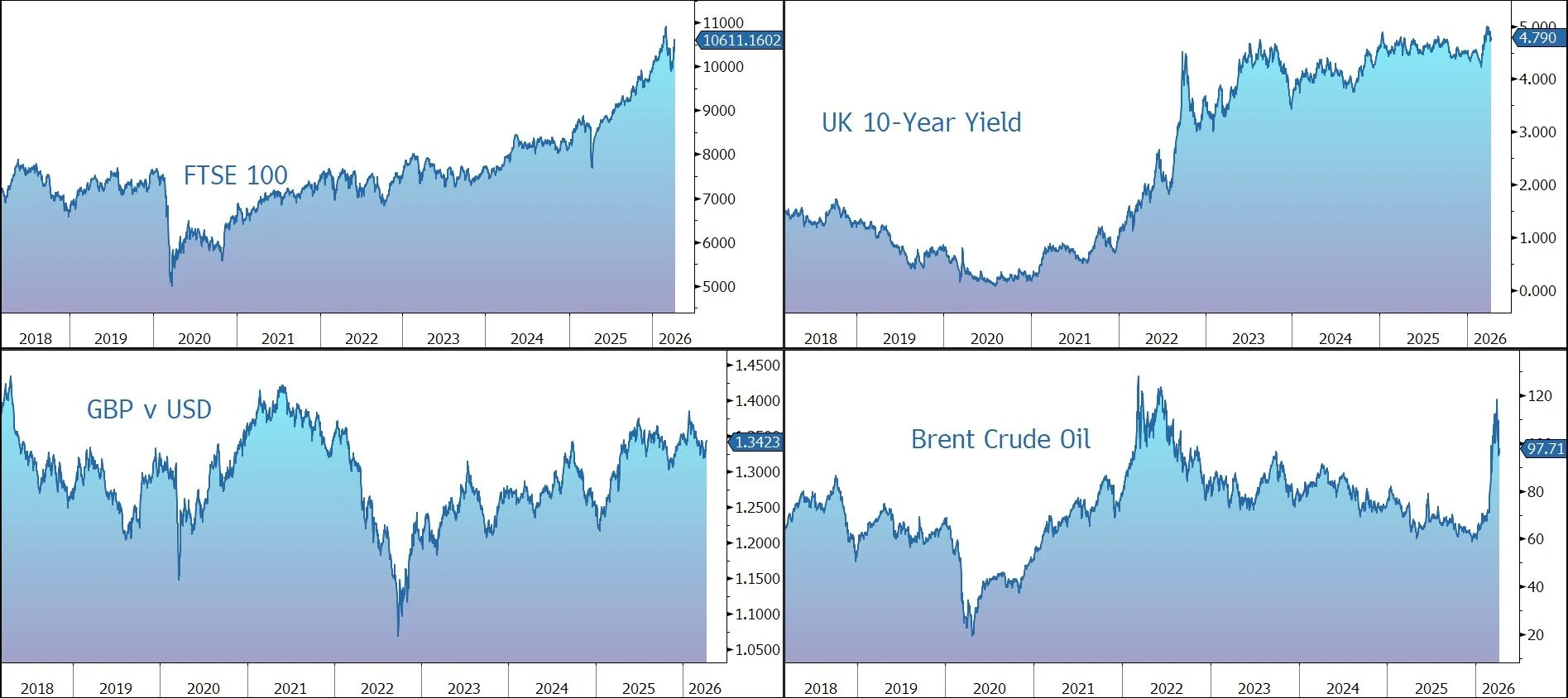

Brent Crude trades at $97 a barrel, giving up earlier gains as traders positioned ahead of ceasefire talks scheduled for the weekend. However, the FT reports that Forties Blend, a marker for immediate delivery, hit almost $147 a barrel yesterday as refineries sought to secure oil cargoes.

The dollar gained ahead of US inflation data – the year-on-year print for March is expected to hit 3.4%, versus February’s 2.4%. The yield on the US 10-year Treasury sits at 4.30%, while gold slipped to $4,750 an ounce.

US equities were firm last night – S&P 500 (+0.6%); Nasdaq (+0.8%). In Asia, equities also moved higher: Nikkei 225 (+1.8%); Hang Seng (+0.5%); Shanghai Composite (+0.7%). TSMC’s quarterly revenue rose 35% to $35.6bn, suggesting AI chip demand remained intact during the first weeks of the Iran war. China’s producer prices climbed for the first time in more than three years in March even as consumer inflation cooled more than expected.

The FTSE 100 is currently little changed at 10,611, while Sterling trades at $1.3418 and €1.1480.

Source: Bloomberg

Company News

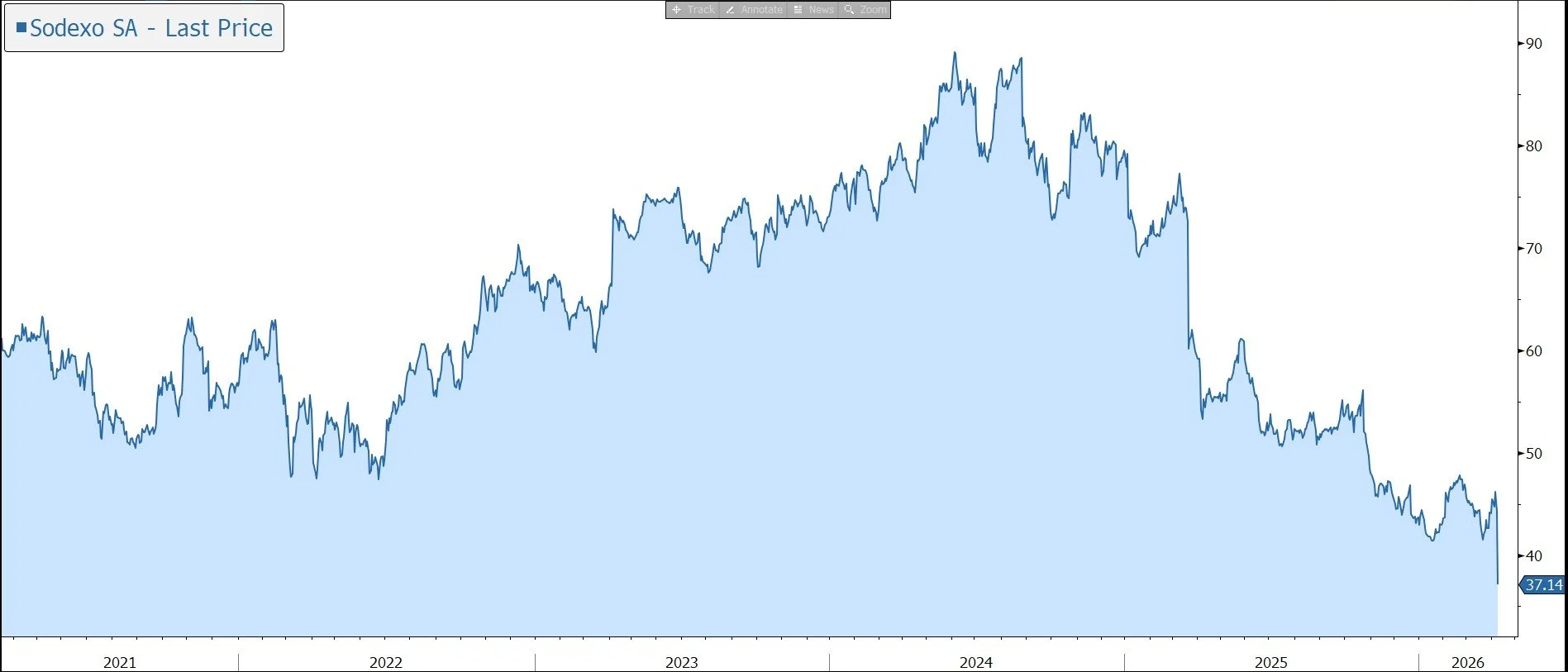

Sodexo has this morning released results for the first half of its financial year to August 2026 (FY 2026). The company has suffered slower than expected organic growth and a step-down in its margin. The new CEO has admitted the company has underperformed due to under-investment and poor execution. Guidance for the full year has been revised down and the shares are currently trading 15% lower this morning.

The shares of industry peer Compass Group have been marked down by 3%. However, although there is some negative readacross given the macro weakness Sodexo points to in some sectors, the vast majority of this warning is stock specific. Compass vastly outperforms Sodexo across the board in terms of operating metrics. In fact, given that Sodexo is now undergoing a period of restructuring, Compass is likely to benefit in competing business pitches. We are next scheduled to hear from Compass at the time of its results on 11 May.

Sodexo is a global supplier of food services and associated facilities management (FM) support functions. The company generates annual sales of around €24bn and is listed on the French CAC 40.

In a stark admission, the group’s new CEO has said the company has underperformed the market and its main competitors. The root causes have been building over time and relate primarily to under-investment and execution: commercial intensity, decision-making and prioritisation, and consistency in delivery. Following a thorough review of its contracts and assets, the company has disclosed short-term financial implications reflected in both its first-half results and in the revised outlook for Fiscal 2026. The company is planning to present a roadmap and mid-term ambition at an investor update in July.

In the six months to end February 2026, revenue fell by 3.7% to €12.0bn. Stripping out the impact of currency (-5.3%) and M&A (not material), organic growth was 1.7%. Pricing contributed 2.4% to growth, while like-for-like volume growth was around 0.2%. Client retention stood at 93.4%. Net new business was at around -0.6%, reflecting prior-year contract losses, mainly in Education and Corporate Services, particularly in North America.

Organic growth was also impacted by a 0.3% effect from a contract reclassification in North America Business & Administrations, following a renegotiation and renewal.

Food services grew at 0.8% organically, affected by past Education contract losses, while FM services delivered 3.6% growth, driven by new contract ramp-ups in Europe and Rest of the World.

In North America, revenue fell by 1.8% in organic terms, mainly reflecting contract losses in Education and Business & Administrations and, to a lesser extent, changes in scope on certain contracts.

Europe was up 2.8% organically, supported by Healthcare & Seniors, while Education remained softer. In the Rest of the World, growth was 9.2%, driven by new contract ramp-ups and strong underlying dynamics notably in India, Australia and Brazil.

Underlying operating profit fell by 26.5% at constant exchange rates to €442m, with the margin down by 140 basis points to 3.7%. The sharp decline reflects operational challenges and mix effects, lower operating leverage linked to softer growth dynamics and the acceleration of investments to strengthen execution. It also reflects the effects of the review of contracts and assets, including specific contract-related provisions, in the light of their actual performance and current market conditions.

The group experienced a free cash outflow of €243m, broadly stable year-on-year, reflecting seasonal working capital patterns and higher capital expenditure, notably one-off client investments linked to contract renewals. Net debt ended the period at €3.6bn, corresponding to a net debt to EBITDA ratio of 2.7x. This reflects the typical seasonality of cash flow in the first half, as well as a lower EBITDA base. Sodexo expects a seasonal improvement in net debt in the second half.

The company has lowered its guidance for the full year to reflect prevailing operating conditions:

· organic revenue growth is now expected to be between 0.5% and 1.0%, versus 1.5%-2.5% previously. The adjustment reflects weaker first-half commercial momentum, as well as lower volumes expected in an uncertain external environment.

· underlying operating profit margin is now expected to be between 3.2% and 3.4%, below the previous guidance to be ‘slightly lower than Fiscal 2025’. This reflects softer top-line growth, execution challenges in certain areas, acceleration of investments to strengthen execution, and the impact of the review of contracts and assets.

· reflecting the level of Other operating income and expenses already recorded in the first half, and based on the ongoing review of contracts and assets, Sodexo now expects Other operating income and expenses in Fiscal 2026 to amount to around -€300m.

· considering the lower EBITDA level implied by the revised guidance, the group now expects to end Fiscal Year 2026 with a net debt to EBITDA ratio above its target range of 1x-2x.

Source: Bloomberg